One should always invest based on future earning prospects and not past earnings.

PBT grew from 34 cr for 9mFY24 to 76 cr for 9mFY25. Now thats a better metric than Quarterly fluctuations.

9 Likes

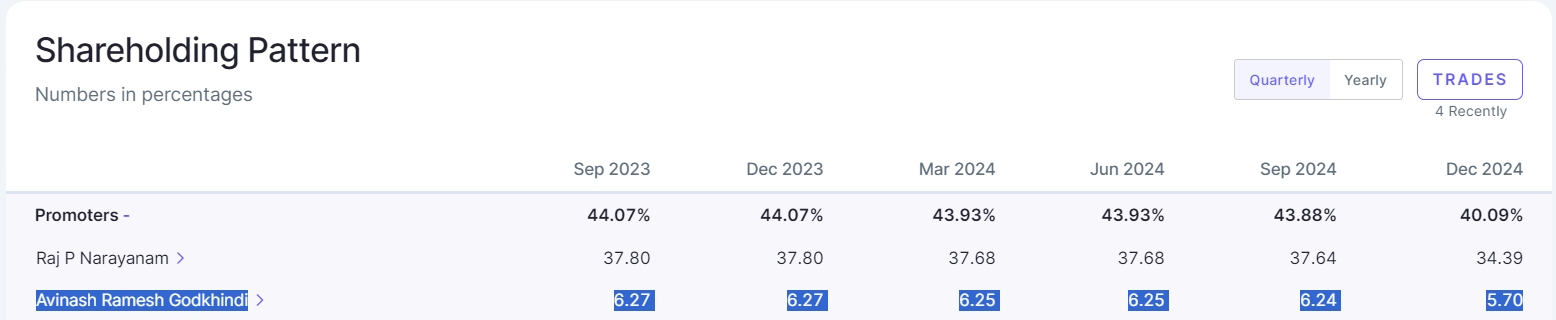

isn’t this reduction in stake due to QIP?

5 Likes

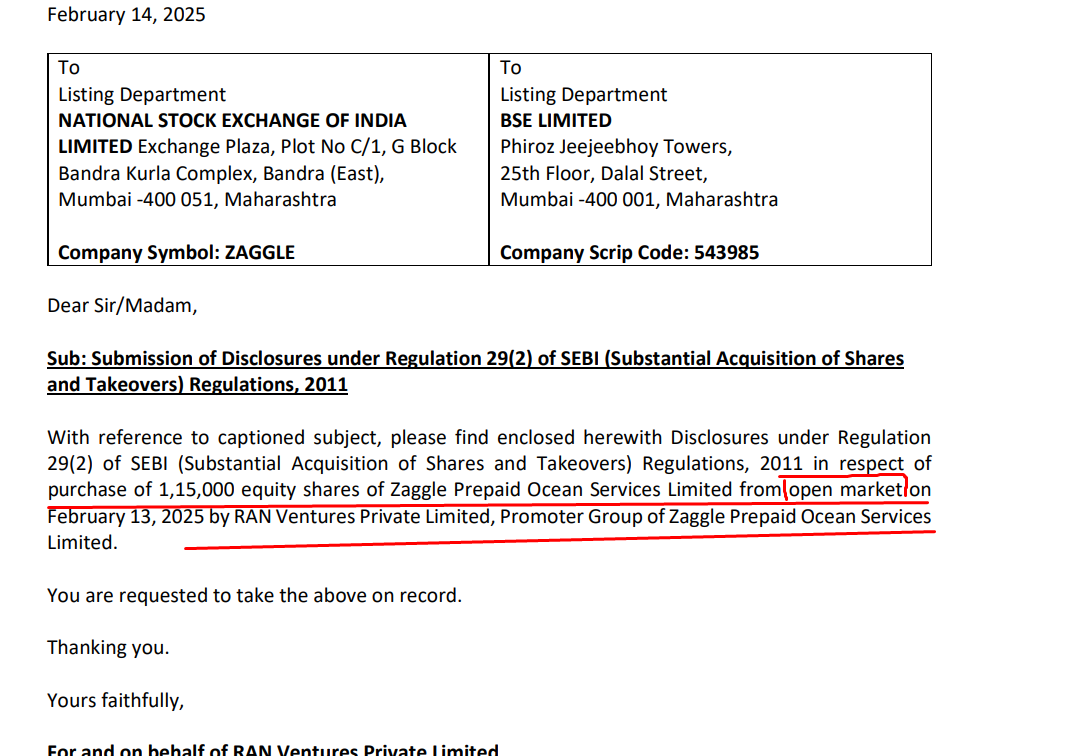

1,80,000 shares purchased from open market by the promoter group on 13th and 14th Feb 25

3 Likes

Zaggle raised 595 crores through qualified institutional placement (QIP) at Rs 523.20 per share. The QIP took place last December and that is why the promoter holding has gone down

10 Likes

That is Due to QIP during December quarter. Also small amounts of change over an year not significant impact in resolve change of the promoter i believe.

4 Likes

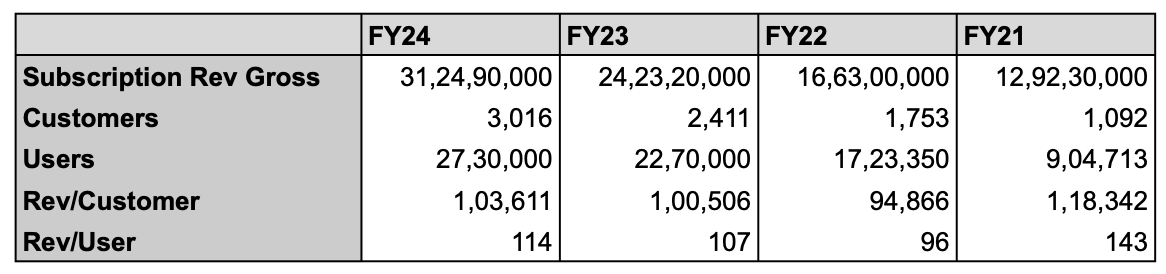

I have mentioned that Zaggle should not be considered a SaaS company as it charges a very, very low subscription fee of ~Rs100/employee/year to its customers.

what is your source of this figure of 100 ?

Because in the pre-ipo interview the mgmt has guided Rs. 250/employee/month

The only difference being that some corporates agree for billing all the employees while some negotiate only on active employees

1 Like

I’m dividing the no of users by the subscription revenues

From the latest Q3FY25, the figures are

- 3.16M users

- 89M in subscription revenues

Which is Rs 28.16/user. Prorated to an annual basis, that’s currently Rs 112.66. So it looks like FY25 will be similar to FY24, FY23, FY22 where the figure was Rs 114, Rs 107, Rs 96 respectively.

7 Likes

there was an interview by Omkar Capital there they mentioned as low as 100 per user as well.

2 Likes

The biggest problem with Zaggle is the poor cash flow operations (CFO).

If they grow fast they will come and dilute stake over the next 1 to 2 years again.

The market texture has changed. It was focussed on EPS growth 1 month back. Now incrementally it will look at cash flows and balance sheet where Zaggle scores poorly.

In the new reality the trailing valuations of 62x seem too expensive irrespective of growth.

9 Likes

Currently there is very little rationale…just panic . Nothing can be deduced from that . The stocks which have high PE or had more run ups are shrinking more . There is no reality in stock market just now…Better to wait and take decision when market settles .

14 Likes

So I finally got some time to think about valuation of Zaggle ![]()

Financial Projections

I collated assorted management guidances to build a future picture of how the financials will play out.

Summarizing all the management guidance below

- 58-63% sales growth for FY25. Taken 59.5% sales growth to calculate FY25 sales (Q3FY25 Concall)^

- 9-10% FY25 EBITDA margins, 10-11% FY26 EBITDA margins, longterm EBITDA margins of 15-16%. (Q3FY25 Concall)

- $1B revenue guidance by FY30 so I’ve projected out what a sales growth pathway from FY25 to FY30 with 8000 Cr target might look like (Q4FY24 Concall I believe)

- PAT margins are calculated by from FY24, FY23, FY22 average differential of 2.25% between EBITDA and PAT margins

- Shares outstanding assumes 0.56% growth in shares outstanding due to ESOPs and no further equity raises (based on 0.42% growth in shares outstanding from Q3FY24 to Q2FY25 - ignoring Q3FY25 due to big bump in shares outstanding due to QIP equity raise)

^Wanted to take midpoint which would have been 60.5% but accidently calculated midpoint at 59.5%. Too lazy to update and retake screenshots so I’ll leave it as it is because it doesn’t make much of a difference.

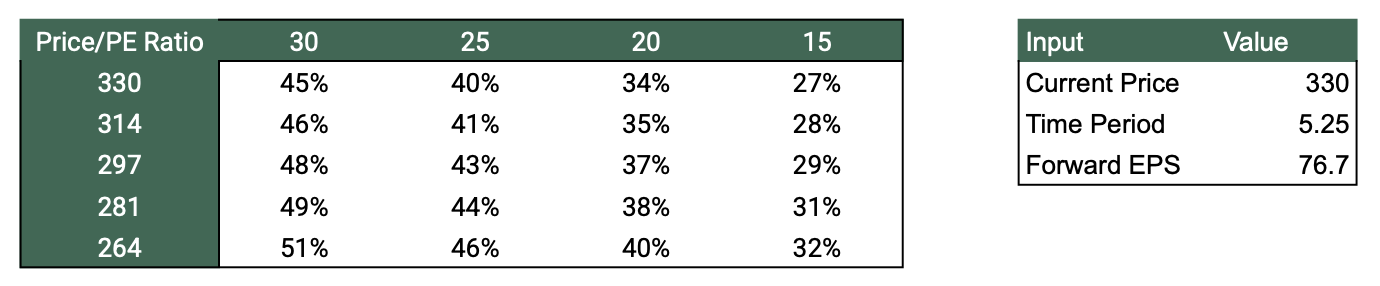

So what kind of returns can you expect in little assuming you hold to FY25 results? I’ve tabulated the returns below for different CMPs and PE ratios at which it will trade at.

So you can expect 27% to 51% returns depending on your entry price and the PE ratio at FY30. Not bad ![]()

But what if guidances don’t play out?

Management guidance is always the best case scenario, especially so far into the future (5 years!). I’ve projected out three scenarios below

Hit margin guidance but miss sales guidance

Instead of 8000 cr in sales, I project 4000 cr in sales by FY30 while keeping margin expansion pathway constant.

Gives us an projected EPS on Rs 38.35 in FY30.

At CMP of Rs 330, return would range from 27% to 11%. Not bad actually.

Hit sales guidance but miss margin guidance

Keeping sales guidance of 8000cr, I project margins settling at 12-13% instead of 15-16%

Gives us an projected EPS on Rs 59.33 in FY30.

At CMP of Rs 330, return would range from 21% to 38%

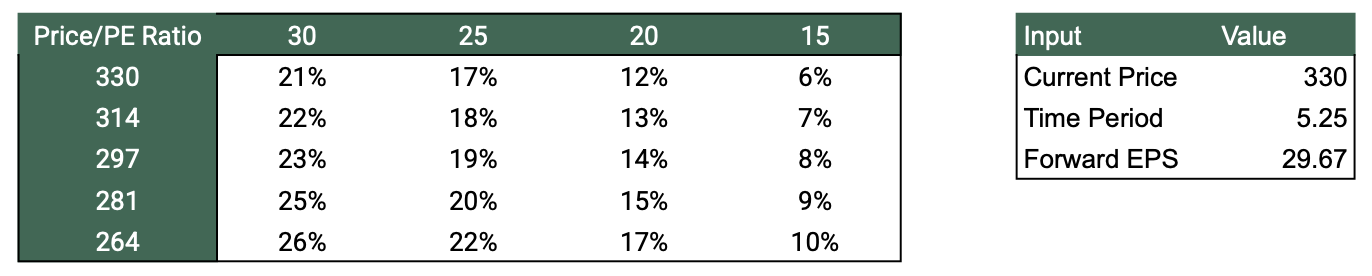

Both sales and margin guidance miss

I project sales to grow to 4000 Cr and margins settling at 12-13%

Gives us an projected EPS on Rs 29.67 in FY30.

At CMP of Rs 330, return would range from 6% to 21%

Final Words

Based on personal experiences in the software industry, I remain skeptical of management targets of 8000Cr in sales and margin targets of 15-16% by FY30.

However, even the reasonable worst case scenarios aren’t so bad. If Zaggle is still growing sales at 18% in FY30, it should command plausibly trade at a PE ratio between 20 to 25 which would give a return of 12% to 17%.

Not much safety but any outperformance from worst case scenario would likely result in market beating returns from CMP.

Disc: No positions yet but planning to take up a position when it stops hitting LCs ![]()

28 Likes

@vada_buffet Just a question here.

If we go buy guidance. wouldn’t we also need capital for expenses ?

eg:

For FY26 expenses would be = 1979×0.895 = 1771.205

So for the entire period expenses = 1979*.895 + 3166*.87 + 4749*.8575 + 6411*.85 + 8000*.845 = 20807.2425

Also going by the same, operating profit is going to be = 207.795+411.58+676.7325+961.65+1240=3497.7575

Lets assume all of the operating profit is available for expenses

Zaggle will still need = 20807.2425 - 3497.7575 ~= 17000 crore as operating expenses.

Wouldn’t we need debt/equity dilution for this ?

as a best case scenario lets assume debt at 10% pa

Shouldn’t this be accounted in PAT and EPS or while calculating returns ?

Please feel free to correct me if I am missing something

1 Like

Unsure if I got exactly what you are asking but if I understand your query correctly.

1979 cr is the sales of Zaggle for FY26. They would need 1771.205 cr for expenses (employee salaries, cost of gift card, cashbacks etc) so the sales would cover the expenses and then they’d have a EBITDA profit of 207.8cr after paying off expenses.

As a software company, they have almost no capex spend or need lots of debt. Like they don’t buy plants, equipment etc on a large scale or have large interest payments. So its mostly tax they need to pay on their EBITDA profit and they would have something 160 cr in PAT.

Of course, these are all accounting figures so actual cashflows will be different but with no capex spending that gets depreciated or amortized over years, PBT will track closely with net cashflow.

6 Likes

Program fees revenue growth although is one of the things I feel will bring ultimate PAT margin cushion for couple of years to come, one force acting against this plan is the new revenues coming in are of lower MDR nature like utility bills (BROME) and fuel surcharge (fleet business) so GMV growth on zaggle cards might be there but program fees growth might be tad slower.

Zaggle is in a bit of a fix that the best way they can charge for their service is via network card MDR and they cannot charge much in SaaS fees. They need to also acquire a payment gateway (technical challenge of its own) where they also make fee when customer mandatorily uses netbanking, UPI on zaggle PG

Disclosure: Significant investment since a long time.

1 Like

In case you guys have missed and need to keep mgmt accountable, chairman on zee business interview early in Jan before results announcement said they are looking for consolidated 80%-100% growth (including acquisition) https://www.youtube.com/watch?v=n5BVb7KX-KU see from 5:10 mark. but this idea was not repeated on the 7 Feb concall. What could be in their ‘merchant card software, payment infrastructure’ acquisition they mentioned in concall that could bring them that kind of growth?

I think the payment infra acquisition they mentioned is likely to be the completion of their majority Mobileware Technologies acquisition (which looks like stands at around 42% currently) but can that bring 80% growth with synergy? (mobileware had 16.99Cr topline in Fy24)

One confident news although is the promotors have increased some steak (not a lot) in the last few days

6 Likes

Payment infrastructure business is most likely Mobileware - I guess they’ll try and acquire at least 50% so that they can consolidate Mobileware’s financials into theirs.

Merchant card software would be some business like Qwikcliver (the market leader). Not Qwikcliver though, they’re too big for Zaggle to acquire ![]()

Acquisition multiples of SaaS companies are usually 3-4x sales so from their ~450cr acquisition kitty, they’ll get like ~100-150Cr of sales.

Not remotely close enough to do 60% growth in FY26 and it’ll take time for the cross selling/up selling revenue expansion to come in (if it comes in at all, there’s no guarantee of anything).

If the company is targeting 60% growth in FY26, then they will have to mostly rely on a repeat of Program (Prepaid cards) and Platform (Vouchers) segments.

Disc: Invested at a cost basis of ~331

4 Likes

3 Likes