Pursuant to Regulation 30 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, this is to inform you that Zaggle Prepaid Ocean Services Limited (Zaggle), has entered into an agreement with Indus Towers Limited.

1 Like

Companies in the D2C space is also something they should look to crack : Honasa seems like a good choice even though its not typical D2C but definitely a startup

5 Likes

From the below linked recent writeup: "This acquisition will help us enter the merchant network and cross-sell our expense management and accounts payable solutions,” Narayanam says. “The company we’re acquiring generates Rs 80-200 crore ($21.6-$24 million) in revenue and contributes Rs 45-50 crore ($5.4-$6 million) in EBITDA.” Zaggle declined to disclose the name of the company.

Read more at: Scaling Zaggle: Founder Raj Narayanam’s game plan for growth via acquisitions, automation | YourStory

So looks like they are acquiring something in the propel segment that could increase their margins there.

10 Likes

I’ve started disregarding all these award of orders ![]() . It’s not clear whether they are following the SEBI guideline of reporting orders which are >2% of revenues (of course, there is no restriction on reporting orders with <2% of impact on revenues but it’s just noise then).

. It’s not clear whether they are following the SEBI guideline of reporting orders which are >2% of revenues (of course, there is no restriction on reporting orders with <2% of impact on revenues but it’s just noise then).

A pertinent point was raised in the concall on why we aren’t seeing growth in program fees portion of revenues despite this flood of new orders. Zaggle’s promoters just seem to heavy into “promoting” with these deluge of award of orders or by repeatedly referring themselves as a “SaaS business”.

They have a good fintech business with lots of potential but all these things make me wary!

Disc - Invested

14 Likes

Let us have patience here. Most important is acquiring customers and while you may not be able to verify how big these order wins, we can both agree that the customers are big players. Once customer stickiness increases and they are convinced of Zaggle’s benefit, they will accept a raise in prices in a heartbeat. Right now, focus less on margins and more on rapid growth and market share.

9 Likes

Helios has completely exited Zaggle as per the latest disclosure of Feb, 2025.

Helios-Flexi-Cap-Fund-Monthly-Portfolio-as-on-28th-February-2025.xls (174 KB)

Current MF Holding:

6 Likes

A Framework to think about Zaggle

There are 4 levers of revenue growth for the company:

- The number of corporates onboarded

- The number of users that get added within the corporate.

- The number of solutions that the company can provide.

- The amount of spends which the users do on the cards.

Whereas the major cost drivers are the following:

- Voucher costs where gross margins are about 6-10%

- Cashback & Incentives to the tune of 65-70%

- Product development and acquisitions

As per its concalls, the co’s focus has been to:

- Cross sell product to existing users to generate more ARPU

- Cull the amount of cashbacks and increntives given

- Overall transition from Zaggle as a Product to a Platform

So let’s take it from the top.

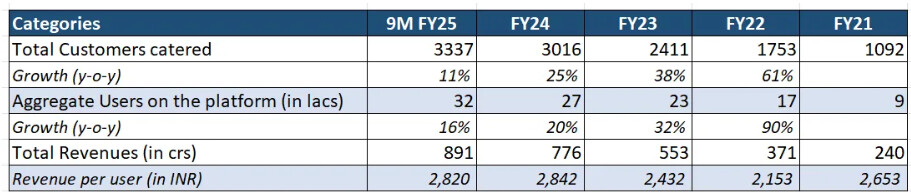

The no. of users on the platform had increased at a high pace during the past couple of years. The same is expected to increase during the next couple of years as existing corporates become more mature and engagement with recently onboarded corporates go live. The number and quality of customers give a strong indication that the co’s products has a definite use case.

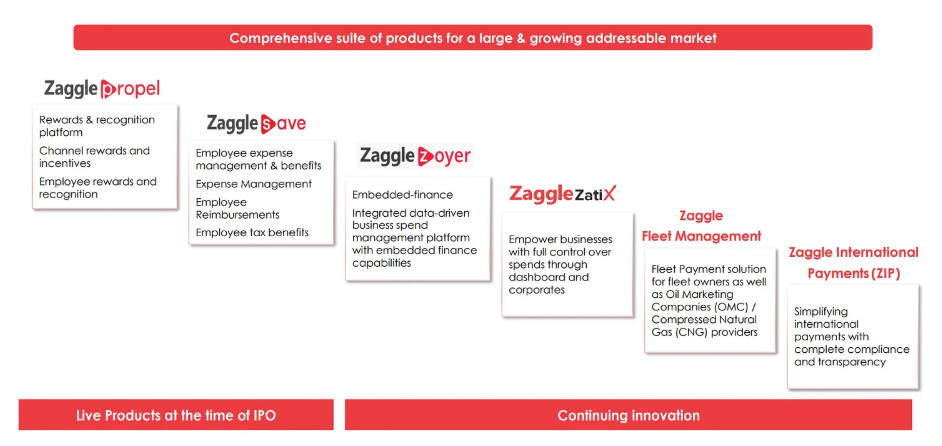

Zaggle’s ongoing transition from a product to a platform company is clear to see. From core products like Propel and Save to inhouse developments like Zatix, ZIP, fleet management etc. All this combined with a host of acquisitions from the IPO and QIP proceeds as people have mentioned in earlier threads. As of Q3 FY25, the co also launched in-app products across health and wellness wallet, cafeteria solutions, employee gadget solution etc.

There are a lot of expense management SaaS apps for expenses management, fleet management, vendor management, educational institution management etc. What Zaggle is trying to do is consolidate them under one platform. Kind of like a super-app.

All this is aimed at integrating Zaggle’s services across various touchpoints of a corporate’s expense heads. Thus subsequently increasing customer stickiness and cross-selling new solutions to existing clients to increase the ARPU.

An increase in revenue can come from increase in subscription fees which has been ~₹110 per year per user for the past two years. The company is pivoting to offer bundled solutions to companies so as to lock in higher fees. For example, giving Zepto both Save and Zoyer during sign-up. However, this is unlikely to lead to non-linear increase in subscription fees which is presently ~4% of revenue but flows down to P&L as pure profits. ~110 per year per user is low and maybe the present strategy is to give away the software for free in the hopes of capturing revenues from interchange fees and gift vouchers redemptions.

Another way of increase in profits is via higher program fees but this is dependent on employee spends; which in turn is dependent on how much cashbacks and incentives is given to users so that they spend via Zaggle credit cards and not via their personal ones. There is little operating leverage at play here and revenues and costs will increase almost hand in hand.

The blended interchange fee for the past 4 quarters was 1.71%. We expect this to come down in the following quarters. Why? Because this interchange %age varies across products. E-commerce has the highest margin at ~2.2% whereas groceries and fuel are lower. Hence increasing spends on lower fees items can push the margins further down. And given the recurrent nature of fuel (in fleet management segment) and grocery spends, it is likely that the contribution of these lower fees items will be higher.

All that said, program fees segment is expected to be the fastest growing in the next couple of years.

Currently the company enjoys EBITDA margins of 9-10% which is expected to increase to 11% in FY26. The primary reason for this is an increasing share of propel point/voucher in the total mix. The EBITDA margins in the Propel segment is 6-10% which is much lower than the interchange fees and thus brings the overall blended margins down. However, the Propel/ voucher program has a slab structure where post a certain threshold being reached in terms of sales of vouchers, merchants give better margins to the Co. This is only going to make an incremental impact though.

The challenge with the business is not in revenue growth but realizing whether it can realize higher margins and PAT in the next 3 years. At the current valuations of 63x PE, growth is well priced in.

The case for margins

‘Incentives & Cashbacks’ comprise of 28-30% of the annual expenses. Reduction under this head is the only substantial way margins can be increased. But there is unlikely to be a sudden drop in the same due to the people switching from Zaggle to their personal cards as explained above.

At the current valuations, the stock is richly valued. No regrets if stock rallies cause I can’t find a way how they could scale earnings more than the current premium justifies.

That’s my two cents. Cheers!

9 Likes

How is it richly valued.

Are you assuming PAT will growth slower than topline ?

1 Like

What I am saying is that at 63x PE, growth is well priced within the stock. The uncertainty is whether the margins will increase by good 300-500 bps for the profit to grow non-linearly with the revenue. At the moment, none of verticals’ unit economics is such that they can grow the margins to such an extent (refer my earlier thread). You will only stand to make money from the investment if the earnings grow more than what is priced in the market. That will require operational leverage which is not there in this business as of now or atleast not visible to me. Except in the software fees segment. But that also is currently 4% of the revenue mix so not much impact expected out of it.

3 Likes

My question is how are you saying that it’s fairly valued. If PAT growth is 60% ie without operating leverage, its forward PEG of 1x…

In case you have DCF, please share with me

Here’s my take on valuations:

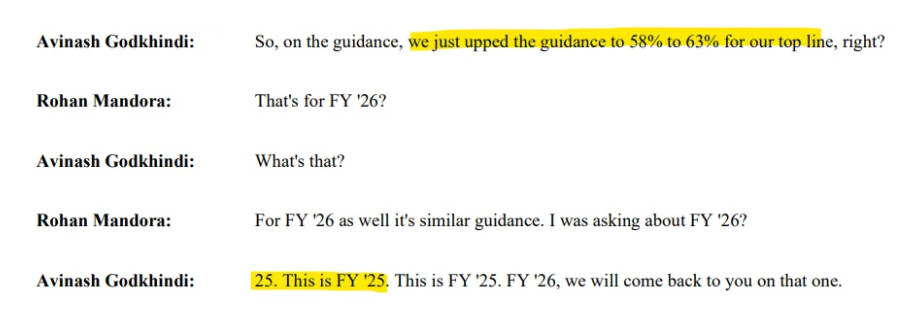

- Management guides for a 63% revenue growth for FY25 which amounts to ~₹1265 crs for the full year. Assumming a TTM PAT margin of 6.5%, that would amount to FY5 PAT of ~₹82 crs. If we take a high 40% PAT growth in FY26 and FY27 that would impute forward PEs of 40x and 29x at the current market cap of ~₹4600 crs.

The keywords in the above are a) 40% revenue growth rate b) margins remaining constant (although mgt guided for a 1 - 1.5% increase in EBITDA margins)

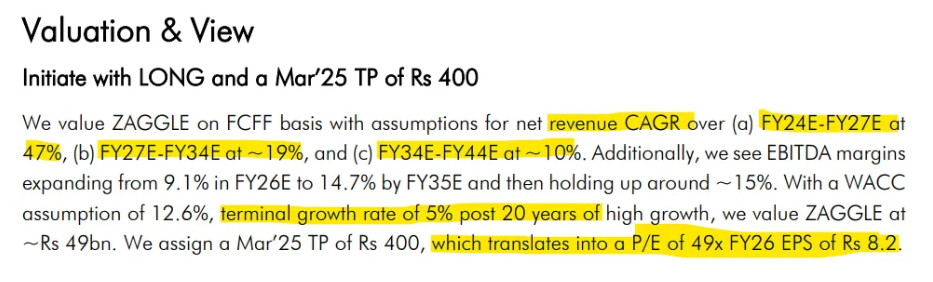

- Equirus performed a DCF this time around last year, with the below assumption and came up with est. market cap of ~5400 crs as of FY26. The important thing to notice here is the revenue assumtions made to arrive at the valuations. ~19% growth rate from FY27E -FY34E plus a terminal growth rate of 5% seems a bit aggressive.

- Zaggle presently operates at a TTM price-to-sales of ~4.1x which is seems to be close but less than comparable companies. Such companies include IT companies with a sub-₹10,000 crore market cap with a sales growth of 30% or more over the last 3 years.

Feel free to read my entire theis on the Co here: Zaggle Prepaid: A high growth play on Corporate spendtech

8 Likes

Yes there is tremendous stickiness due to the network effect. Once on-boarded, customer exit seems difficult.

4 Likes

Zaggle Stock Analysis: What led To The Sharp Decline In Return Ratios | Know Your Company

4 Likes

Channel partner deal for 3 years with Grand Thornton where Grand Thornton will offer Zaggle spend management platform to its corporate clients and large enterprises.

1 Like

Every other day the company is announcing these deals. So many well established companies dont resort to this . Why ?

isn’t it good for investors?