Does anyone have any data on renewal of contracts or reviews from any corporates?

2 Likes

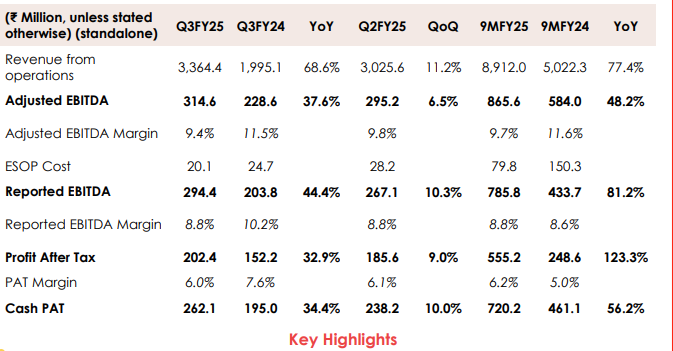

Q3 results (looks good at 1st glance)…came out, post-market, yesterday (7th Feb)

Investor presentation

Audio recording of the investor call

Disc : invested////not a buy/sell reco/not registered with SEBI

2 Likes

Zaggle

Mkting is a way to grow for Fintechs - it a necessary thing in businesses and short term market participants might want to position themselves in something else till the time these costs remain high.

As a stock holder i would look at 2 things :

- Will Mkting costs benefit

- Once mkting costs go away, will the topline remain

Topline increased ~70%

Market can reamain irrational. Do some homework wrt Customer stickiness - imo customer is sticky.

Zaggle takes money in advance (-ve receivables)

Valuations can run on its own. But always remember high valuations are not the lone reason to sell.

D: Still holding may trim/exit if the business thesis breaks.

14 Likes

Company needs to show better cash flow now. Infact, on margin, they mentioned in earlier call, 10% opm at Q4, FY25. Now they r talking in next 3 yrs and with no margin improvement visibility. That’s little disappointing

3 Likes

I think last year base line of margin where high… 10% approx… Margin not fall much qoq…but management not giving near term guidance on margins which is quite negative… Kab ayega operating leverage?? Management Giving guidance of 58-63 percentage on the base of fy24.(776). which is 1230 approx… On current margin pat will 70-80 cr…so its allready priced in and there is not much eps growth till next quarter, i think it made near term top in December… Biased… holding

8 Likes

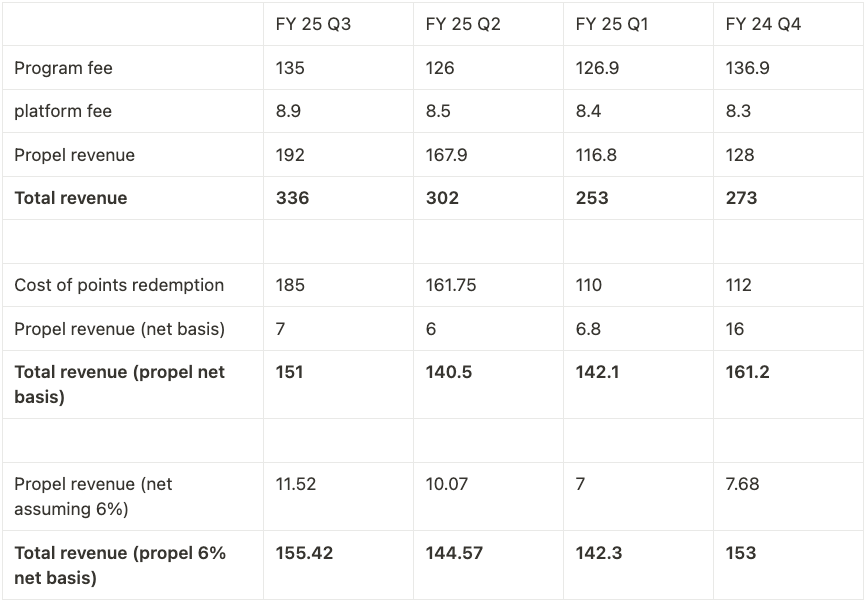

I was listening to their concall and everyone had more or less the same question whether the program fees would surpass the point fees business - Management dodged the question.

Points fee business is a 6% gross margin business essentially just a commodity business.

Lack of margin growth indicates that their program fees is not able to generate a lot of margin and also indicates that the cross selling prospects which the markets did think once are not playing out so well.

Disclaimer - invested and kinda scared

7 Likes

latest buying by Zaggle was in this company

Synergy should play out

Also gives them new customer base to may be cross sell in future

Yes bank and others are also there with Mobilewaretech

7 Likes

The key issue here seems to be the lack of an increase in program fees and platform fees, rather than an expansion of margins. Looking at Propel revenue on a net basis provides a clearer perspective. While Propel’s margins have declined even if they were to recover to 6%, as you noted, the overall impact would remain relatively limited. Revenue has essentially been flat over the year.

P.S.: I’m relatively new to investing and ValuePickr, so please bear with me in case I make any silly mistakes. I appreciate any guidance or corrections!

4 Likes

Only one suggestion, do compare YoY rather than taking Q4 2024 numbers. If you would observe, there is usually a noticeable jump from December to March through the years. You would then see a big jump YoY in prigram fees… Also if you would go that route, Program fees are much better QoQ and yet everybody was celebrating last quarter’s results and disappotinted with current quarters results

7 Likes

Margins have been the same at the 9% levels for FY23, FY24 and 9MFY25.

Company is growing topline at 50% plus and should continue growing at that pace given client wins almost every week

Profits have doubled in 9MFY25 YoY.

Stop jumping around on quarterly fluctuations. They are running a businesses, not an excel file where you drag the formula.

So instead of nit picking one needs to ask did markets overpay to start with.

33 Likes

Pros:

◇Company’s Topline is growing by 50%,Guidance upped to 63%

◇Margins are stable and in the range that company promised. (9-10%)

◇TAM is growing day by day due to management’s approach to tap into untapped profit pools. (Zoyer (BROAM) fleet management, etc)

◇5 acquisitions in pipeline from QIP proceeds. These would add to Topline over time.

◇ Management is humble and growth oriented.

Cons:

◇ Low Margin Business (propel)

◇ Equity Dilution over the years.

I believe the market is in Heavily panicked mode and that added to the freefall of company (25% in 3 days)

Disc : invested and Looking to add more if possible but skeptical.

11 Likes

Just want to remind here that profit growth matters as well.

For most SAAS or software product companies profit grows at much higher rate than revenue (eg: Rategain technologies) because of operating leverage.

But if you look at zaggle especially in last 2 quarters ( because we now have reasonably high base) the PBT growth is slower than revenue growth.

In December quarter Revenue grew by 70% YOY while PBT grew by 28%.

Add to this dilution.

EPS growth for last quarter is 20% YOY.

Now the question is, do you want to invest in a company at 60 PE that grows at 20%

Discl:Not invested

7 Likes

This is a great point that I’ve been repeating over multiple posts in the thread. As someone who had built a SaaS product, this is one of the few areas where I can make some confident assertions.

Actual SaaS companies are probably the best example of “operational leverage” playing out. SaaS companies only have two costs (actually, most big ticket SaaS companies have sales teams which has its own slightly more complex unit economics but I’ll ignore it for now to keep the analysis simple)

- Labour - Software developers to build the product, maintain it, add new features etc.

- Server costs - Usually paid to some cloud service provider such as AWS, Azure etc. No one manages their own servers anymore.

Now the labour cost is the same whether you have 10, 10,000, 1 million customers. It isn’t something like manufacturing or services where labour usually scales linearly with customers. So you get pure operational leverage, there are very few examples in the world of this where you have a true fixed cost and every additional customer just pretty much goes straight to your profit line item.

Server costs usually increase linearly but servers costs are very, very cheap. You can see this reflected in gross margins of SaaS companies, server costs are usually <10% giving these companies gross margins of 90%+.

So you have

- One very, very high fixed cost - Software developers are expensive, not just in terms of high salaries, but they also need significant ESOPs to entice them to join and stay.

- One very, very small relative to fixed costs variable cost - The server costs are too negligible with the exception of special situations (AI is a good example where server costs are high - both to train and inference its models)

However, Zaggle’s subscription revenues are so low that this operational leverage does not play out. Instead their revenues are dominated by card processing fees (a large part of which they give back in cashbacks) and voucher reselling (where one was initially seeing some operational leverage play out as they increased the volume of vouchers purchased getting better wholesale discounts but now appears to have reached max margins).

@rookie_investor_1 Point is correct IMHO. Zaggle should be valued on earnings rather than sales AS there is no operational leverage here so there is no reason to expect any (significant) margin expansion. EPS growth is the sole metric that Zaggle should be valued on.

8 Likes

Zaggle is essentially a Fintech company at the core. They might term themselves as SaaS just to attract better valuations. It’s a bit funny how everyone will try to justify it as a SaaS at ATH but with 45% correction, it suddenly isn’t.

If you look at employee cost as a % of revenue they do have some operating leverage similar to a true SaaS company in their favour but probably it’s not reflecting in bottom line as they might be spending a reasonable amount in acquiring those customers.

Only way for them to increase their margins is to scale up their subscription based SaaS platforms like Save, CEMS, and Zoyer.

They don’t have network effects in any of these platforms, only moat might be switching cost.

There’s nothing changed in their business suddenly this quarter and they have delivered on their guidance so far and not overpromised historically or decreased their guidance for the future so I don’t think it makes sense to associate the price drawdown with their low margin Propel business or anything they said in the concall. It’s purely due to high valuations and broader market correction.

17 Likes

I might be oversimpliyfing a bit but your conclusion seems a bit contradictory to your argument.

Whatever you’ve said about operating leverage for SaaS companies seems to be correct.

As Zaggle adds more customers, it should add to the bottomline without significant increase to the cost. Their fleet management solution for example, it doesn’t really matter if they have 2 or 100 customers, the costs won’t vary much . What am I missing here ?

3 Likes

Yes, if Zaggle is able to generate considerable subscription revenues in future (whether from fleet management or anything else), then operational leverage will kick in.

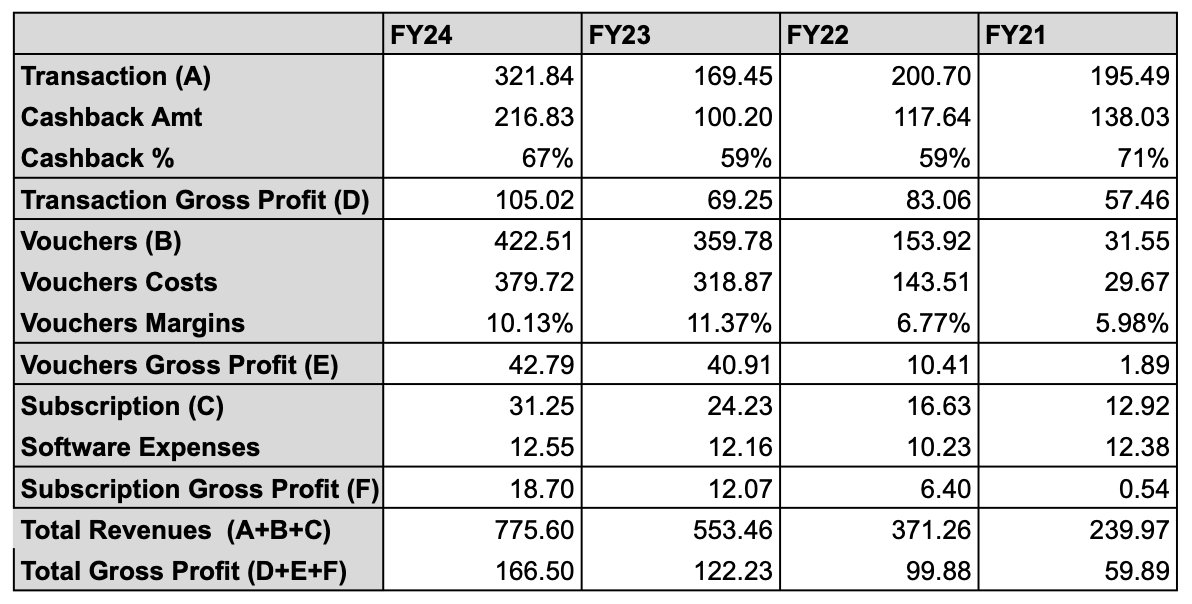

Right now, we are seeing the reverse happen. Reproducing financials that I posted above

In FY21, gross revenues of subscriptions were 12.92cr while of vouchers and transactions combined were 227.04cr. So already a very small portion 5% of total gross.

In FY24, gross revenues of subscriptions were 31.25cr while of vouchers and transactions were 744.35cr. So it went further down to 4% of total gross.

You can actually see the leverage play out under subscription revenues in the table. Their software expenses costs are pretty much fixed from FY21-FY24 while their subscription grows from 12.92cr to 31.25cr.

This is the beauty of the operational leverage of SaaS businesses ![]() .

.

On the other hand, you can see costs (cashbacks & voucher costs) scale with transaction and voucher revenues.

There was some initial operational leverage kicking into play in voucher as margins went from 6% to 10% but 10-12% is probably the max margins they can get from voucher business (given that retailers such as Shoppers etc. have 20-30% margins themselves so there is only so much wholesale discount they can give)

But you are correct in that if they can get huge subscription revenues from fleet management (or even their acquisitions) and make subscriptions a large part of their revenues, then operational leverage will kick in.

I haven’t gone through the latest concall (transcript is not out yet) so I don’t know if they are scaling up their subscription revenues through new software such as fleet management and acquisitions in a big way but at least as things stand, I would not count on operational leverage.

6 Likes

ah ok , got your point but I partially disagree that there’s no operating leverage. The cashback % has remained more or less stable and the employee and server costs for acquiring a new customer is negligible as they already have the platform. For example profit from transactions is ~100 cr in FY 24. If they add 1000 more clients and the profit goes up to 200 cr, the employee and server costs remain the same, but Zaggle makes more money which I think is operating leverage.

I’m not very sure about how the vouchers business works but I think the same principle might work there too.

I get your point that the leverage is not as much as a pure SaaS company, where every penny after a threshold flows to the bottomline, but Zaggle, a fintech-SaaS hybrid does have operating leverage imho, though to a lesser extent.

4 Likes

Q3FY25 Concall Notes

Two Acquistion Targets in Advanced Stage

From reading between the lines, I prophesy they are

- Gift Card Provisioning - Most likely a software that allows merchants (e.g. Shoppers) to provision virtual gift cards. Revenue will most likely be subscription or some sort of volume based pricing.

- Payment System - Most likely a mobile wallet which has UPI payment and wallet-to-UPI integration. This is because MDR of 1.1% can be applied on wallet-to-UPI purchases and would be a good alternative for employees over prepaid cards given the popularity of UPI

Acquisitions will not be closed in Q4FY25, most likely sometime in FY26.

Three other acquisition targets, presumably not in advanced stages, also mentioned but no further details.

No Impact of New Tax Regime

New Tax Regime cuts out all the benefits but Zaggle’s users only the meal portion of the Old Tax Regime’s benefits and that makes up only 0.48% of the revenues of the processing fees revenues.

New Product Launches - BROME and Fleet

-

BROME - “Branch Recurring Operating Monthly Expense” - Signed up Blinkit and Zepto for it, not much detail but apparently for managing “store level expenses”. Revenue will come from processing fees of transactions and subscriptions but not clear which one will dominate. To be honest, I’m not sure of the difference between BROME and Zoyer.

-

Fleet - Signed up AGP City Gas, not much detail here either. I am guessing that they are issuing cards that fleet operators can be used at AGP City Gas stations. Remains to be seen if fleet operators find it useful. Not clear whether revenues are subscription or processing fees but I suspect the latter.

Hullabaloo about low margins of voucher business and overall low margins ![]()

Multiple callers asked about the margins, I think about half the questions were on margins. Basically, vouchers is a low margin business of 7-9% and most of voucher commissions are paid out in Q3 which is why margins even further constricted in Q3FY25.

Overall margin expansion will come from increased share of processing fees and subscription revenues in the future. EBITDA Margins were 15-16% in FY22 before launch of vouchers segment after which they reduced because it is a very low margin business.

Guidances

- 58-63% revenue growth guidance for FY25

- 9-10% EBITDA margin guidance for FY25

- No revenue guidance for FY26

- 10-11% EBITDA margin guidance for FY26

- 15-16% EBITDA margin guidance for “next four years” (I assume this means FY29)

- Processing fees and subscription revenues to grow faster than vouchers revenue in the future

- My Take: Processing fees has a good chance. Grew 110% YoY and even though lots has been flat for last four quarters, they seem to have signed up lots of customers.

- My Take: Extremely skeptical of subscription fee revenues growing faster than vouchers but they are starting from a very low base and with the right acquisitions, its plausible.

I think I have a good idea of the business now and their future plans. Will think about valuation of the business soon, especially now that its price has dropped significantly.

10 Likes

Promoter Bought 25000 shares (92 Lacs worth approx) after shares slump 20%+ in 2 days.

Definitely a good sign IMHO. He even confirmed he couldnt understand why zaggle price crashed after results on ndtv profit interview recently.

For those who are wondering why isnt the operating leverage of a SAAS biz kicking in yet… Well saas revenue was less than 10% of their business to begin with. They are basically a prepaid card issuer primarily which is a low margin business. They are the #1 at it. So what do you do next? You find other avenues to grow. Hence the Zoyer, fleet management, acquisitions etc. So due to any of these IF the Saas revenue as percentage of total revenue grows then surely margins will improve. In bear case, if saas doesnt grow and company still achieves its topline guidance, pat is gonna double by FY27. In Bull case , if margins grow and topline grows as promised its a double engine growth. Only time will tell.

Disc : invested.

9 Likes