Good update but again same mistake of July 2026 instead of 2025. management should sack the guy who is writing these letters.

Corrected now. ![]()

![]()

Can we expect the ttm eps to be around 40 for FY25 ? And around 60 for FY26 ?

Yes. 40 should be achievable assuming they start selling modules from Q4,FY25. Otherwise it may end up around 35 range.

On a conservative estimate, FY26 EPS should be close to 80 subject to sustaining current margins with 90% utilisation of both Cell & Module lines and also successful execution of another 600 MW Cell line.

So if everything goes according to the plan, we might be looking at say 3× cmp in the next 2 years ? Keeping 60 pe as target ?

Hi

That depends on the equity dilution plan that management would choose to raise funds for future expansion of backward integrated ingot- wafer- Cell- Module line and also EPC vertical.

However, 60 PE may not be sustainable in the long run. So, imv, a conservative PE of 45 may be given to RE companies with a moat. On this basis, doubling from current level is easily possible.

Keep it simple. Let’s say it achieves 2.4gcell and 550mw module in next 2 years by Fy27 as said in Annual Report and some time in next two years it conveys it’s ambitions 9f doubling it’s capacity…in next 2 3 years i see upwards of 25000 30000 mcap with 10mcap to sales valuation

True but if websol makes it to almm 2026 with peak solar being in 2035-2040, it looks like a safe bet right ?

Can any one please explain why websol OPM is so high compared to other solar panel manufacturing company?

One can follow this thread on X for websol updates

Expecting PAT of about 50 Cr.

Due to DCR vs Non DCR cells sales mix. DCR cells (Websol sell mostly DCR cells) have higher margins than non DCR cells. 15-20% difference in margins. mentioned in premier energies concall, you can read it for reference.

Can you please share the full PDF?

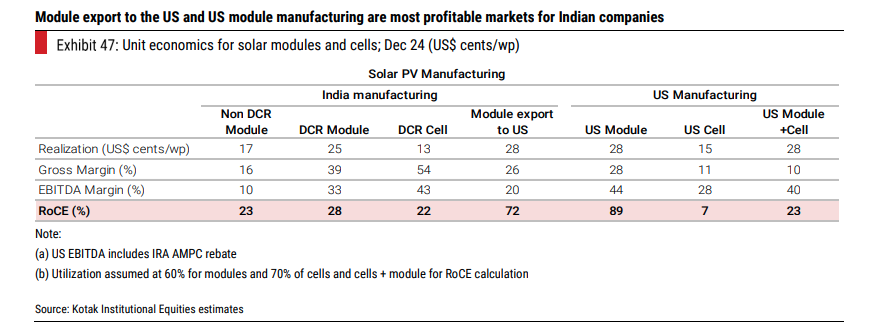

Renewable Energy- Kotak.pdf (4.8 MB)

Unbelievable the kind of journey this stock has covered! Life changing! Let’s hope this becomes 10GW cell manufacturing company in next 5 years

Receiving a lot of query from people who want to understand what’s happening in terms of technicals.

Reiterating the basics of wealth creation is that actual money is made only when your short term average is above your longer term average. So let’s 20ma is above 50ma and the moving averages trend upwards… That’s the time when wealth appreciates because the buyers are ready to pay up because of underlying growth and future value.

Coming back to websol, fundamentally like I said previously with current valuations if the company is able to become a 2.4 GW cell + 550mw module in next 2 years ! I see atleast 25000cr mcap.

Now technically, we have breached 20ma and last pivot low of 1620 and created a double top at 1865. So now we switch our focus to where we can bounce from…50ma 63ema range is 1480-1540

Below that we can revisit 100dema or 20 weekly ema which has been a very important support from last 18 months .and all long term drawdowns have been arrested there… This is 1300 1330 levels!

Below that the god support is at 1000 levels currently where 200dma resides! We shouldn’t be visiting that given the current triggers! But who knows? Never say Never right?

If it gets there, it will be time to sell the neighbours house and buy websol😂 Just kidding!

Hope this helps! Happy Makar Sakranti!

Disclaimer ~ I might or might not have any position in Websol and the levels are just for educational purpose! No buy sell advice!

That’s the reality going forward. China will command and control as they have solar manufacturing machinery capacity and processing technology patents.

What’s your inference of this with respect to WEBSOL?