Websol has placed itself better than most of the other companies in solar value chain except Premier energies. Premier has the advantage of scale and money coupled with latest TOPCon cell lines (one launched in 2024, other lines are underway).

Websol management is having 30+ years of experience and they managed to sense the future & also wanted to secure from China supply disruptions by announcing their plans of operating Ingot-wafer-Cell-Module line of 2.4 GW in future.

However, to attain self sufficiency, Websol needs to manufacture polysilicon, ingots and wafers in India. No Polysilicon producers in India till now. Only Adani Mundra is making Wafers, Ingots that too for self consumption.

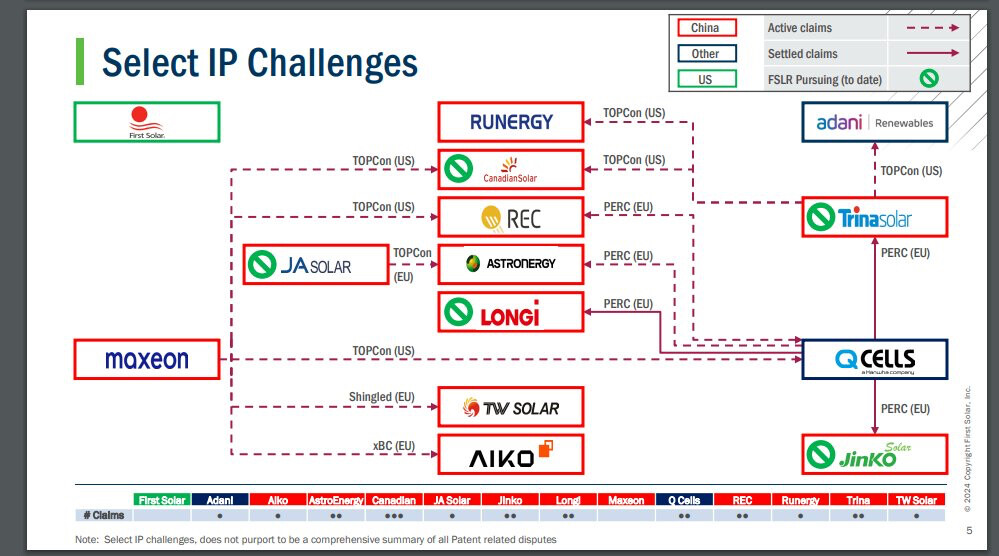

Polysilicon and Wafers can be manufactured in India but the technology and huge investment are the concerns. I came across in Internet that Trina solar is fighting with Adani for TOPCon technology related patent infringement in US.

https://static.trinasolar.com/us/resources/newsroom/US-International-Trade-Commission-Institutes-Investigation-of-Runergy-and-Adani

Most of the large global manufacturer fight with each other for patent infringements. Source. X tweet @Industrlpolicy dated 21-01-2025.

I am not saying that all Indian manufacturers will get the same kind of notices but patented technology is available with Chinese biggies so they have an upper hand in solar value chain manufacturing and supplying machineries to Indian Companies.

Again Websol is placed better as they source most of the machineries from Centrotherm, Germany. Wafers are imported from China but that is not the case with other biggies like Waaree, Adani, Premier & etc. Waaree and Adani are completely procuring machineries, technicians support, technology and raw materials like polysilicon and wafers from China.

Coming back to Websol, To achieve self sufficiency in India, Websol needs money, a lots of money to invest in backward integration (Assuming Centrotherm supports in technology patents but not sure). Capex for converting MonoPerc to TOPCon (not much), HJT needs to be added + production loss during the upgradation time. Hence, It will definitely take a long time to generate sufficient cashflow with the current pace of expansions unless a foreign/established Indian investor purchases a significant stake in the company and infuses huge money.

So to summarise the long story short, Websol is comparatively placed better than its Indian peers at least in Domestic demand context . I personally don’t see any threat for Websol up to FY2028 subject to sorting out funding arrangements. The valuation needs to be moderated at a FY26 Forward PE of 45.

Just my opinions. Invested from double digit price levels.