Promoter SH is only 27.71%.

93% of promoter SH is pledged.

Any views on above?

Promoter SH is only 27.71%.

93% of promoter SH is pledged.

Any views on above?

A big Positive for Cell manufacturers like Websol & Premier. A big Negative for Module only players and EPC players.

If I understand correctly warrants have been converted to stock on 5th November(Correct me if I made wrong assesment here but quantity matches so…)

So in last 2 qaurters company made 65 cr profit and promoter group made 91.68 cr?

Please out mistakes in calculations if you spot any.

So here are my questions then :

1: This WEBSOL GREEN PROJECTS PRIVATE LIMITED can anyone help me with more details on this difficult to pin down as it is private.

2: Also how these 91 cr were used by it.

Thing which looks out of place to me is :

1: If credit line was secured from IREDA and pref raised why the need of pref warrants to get just ~15cr of captial infusion from promter

2: Why convert warrants now in bearish market when stock is expected to give stellar return based on demand and capex. They could keep it for atleast 4 qaurters.

Note: Not invested looking to take some position

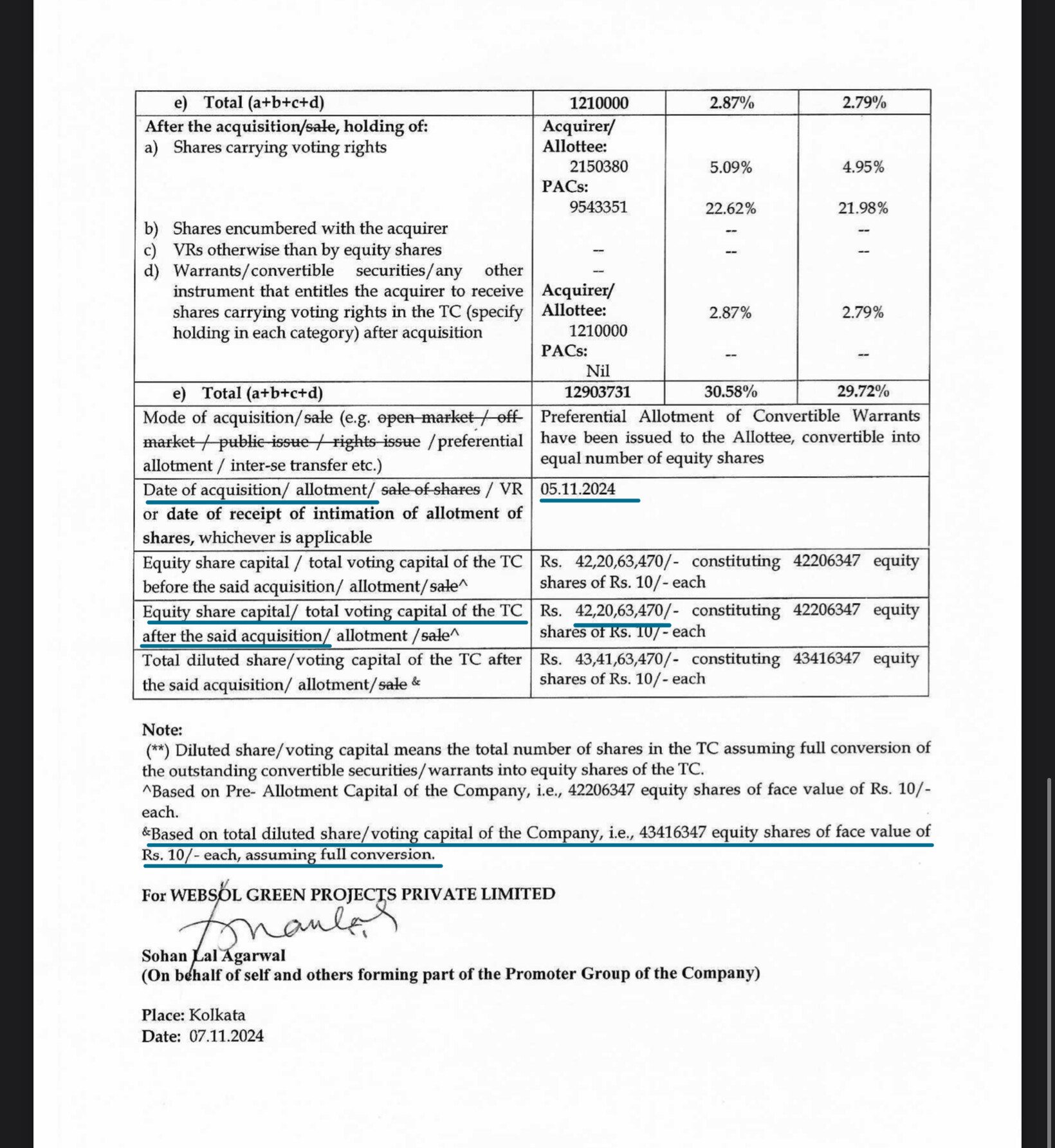

Websol Green energy is promoter group entity. They have been issued convertible warrants as a means to infuse capital by the promoters into Websol Energy ( Listed entity ) . The proposal for the same was announced to the exchanges on April 11 th ( The pricing of the warrants are also at Rs 530 due to the same ) . The subsequent price appreciation has favoured the promoters , but I think there is nothing illegal here.

The allotment of the warrants to promoter entity happened on 6th Nov. These have not been converted to equity shares yet.

Once full conversion happens the share capital will go up from c.42 cr to c. 43 cr.

Finally, Chinese Govt is showing a lot of interest in rolling back their existing incentives for solar industry which will increase their sale price if not much at least to some extent. So, the sale price difference between chinese and Indian cells, panels will narrow a bit. Positive.

The Ministry has targeted internal firms by hiking the minimum capital ratio for investing in PV manufacturing projects, including silicon wafers and solar cells and modules. The new level is 30 percent, taking all parts of the solar chain to the same level as polysilicon, which was already at 30 percent.

The move is expected to deter new entrants as well as existing players from expanding ‘recklessly’, something many believe was done more in hope than a clear business plan in many cases.

If the price of wafers also increase, won’t it affect websol too ?

Hi,

Yes. It will affect Websol in the long run but not immediately as good margin is available in DCR market. At the same time, Chinese manufacturers have few hurdles to comprehend.

With the above scenario, Indian Module only players will find it difficult to pass on the price increase to buyers in India whereas Cell players/ fully backward integrated ones will enjoy the margins as the gap between Chinese and Indian Cells with help of DCR, ALMM List II would have become narrow which will pivot EPC, IPP and other buyers towards Make in India products.

2). US/EU export market of china is already affected due to regional policies. It is a boon for Indian manufacturers to get better margins there in future.

In any case, Indian Cell manufacturers will enjoy the dream run minimum till FY2028 due to scarcity of Make in India cells.

Sharing this without comment.

The US Commerce Department has announced a new round of tariffs on solar panel imports from four Southeast Asian countries.

The US tariffs will be imposed on solar panels from Malaysia, Cambodia, Vietnam, and Thailand. The Commerce Department calculated dumping duties of between 21.31% and 271.2% on solar cells from these countries. The duties will vary depending on the company. This is just preliminary. The final verdict will be delivered by May-June 2025.

Read more at: US Imposes New Tariffs On Solar Modules From Southeast Asia

I am pretty bullish on Websol Energy to be 3 to 8x in next 1.5 years from current price of 1250 - 1300.

What they do - manufacture Solar cells with current capacity of 600 MW and Solar module capacity of 600 MW. Solar cell line was partially operationalized in Q4’24. Module line was operationalized in Q2’25, no revenues have been booked in Q2 for modules.

Net Profit:

Q2’24 = -55 Cr

Q3’24 = -59 Cr

Q1’25 = 23 Cr

Q2’25 = 42 Cr

they are doing pretty well in DCR cell sales. With current Cell & Module pricing, they are anticipated to have net profit of 55Cr+ per quarter.

So 600 MW cell + module line with 90%+ utilization is expected to give an yearly profit of 200-240 Cr.

Current Market cap = 5600 Cr.

So taking lower end of profits, Websol is currently trading at 1 year future PE of 28.

Waaree Energy & Premier Energy are its competitors. Waaree & Premier are trading at 80 & 240 PE respectively.

So Websol can easily trade at a PE greater than 80 in next 2-3 Quarters.

Icing on the cake : They are working to add 1 more line of 600 MW of Solar cell. Considering raw material price & final price of cells remaining constant, we can see ~100 cr worth of profits every quarter, which will be 400 Cr of profit annually,

Assuming PE for Solar industry cools down a bit, say comes to 70, we are looking at a market cap of 28000 cr, which will be 5X’er for sure.

They have plans to 2x the capacity of Solar cells from 1.2x to 2.4x in FY 26. They have talked about plans for backward integration for wafer and Inglot manufacturing, but I think they have not given a timeline for this.

I have taken more optimistic PE for Websol, we have example of Premier Energy which is currently trading at 240 PE. Considering Websol has good expansion plans, market may reward Websol with PE comparative to Premier Energy for next 6 to 18 months.

Disclaimer. Have been aggregating Websol since 1025, even bought some quantity today. As of now Websol is 26% of my direct equity portfolio. I intend to take it to 33% if it falls to 1150 or so. Have high conviction, so views would definitely be biased.

Websol currently develops cells using the Mono PERC technology and new capacity expansion also happening in similar direction.

Do they have plans to migrate to TOPCon as well in near terms or there is no need for next 2-3 years as current demand matches with their PERC technology.

Monoperc vs Topcon needs 4 more auxiliary components to shift from mono perc production to Topcon so unlike the perception that it will need a complete overhaul to shift from monoperc to Topcon…

As far as Websol is concerned I guess we will be in Topcon in the latter part of the expansion where we get into Greenfield expansion in new land…as long as we are expanding in Falta it will be mono perc…

Taking Future PE for Websol and current PE for Waaree and Premier doesn’t makes a sound comparison I think. ![]()

Take future PE for all companies will get u better figures.

I am sure, you would have read this point too in my message…

“Assuming PE for Solar industry cools down a bit, say comes to 70, we are looking at a market cap of 28000 cr, which will be 5X’er for sure.”

Future PE of Websol has been considered as toned down PE assuming premium will keep reducing as and when Solar cell capacity keeps increasing. Current PE of Waaree is 80+ & Premier Energy is 240+

One need to keep in mind all possible scenario’s that can happen.

The Indian solar sector significantly depends on government policies to drive growth, ensure demand, and support manufacturing.

The current state of India’s solar module manufacturing industry is characterized by rapid growth but faces challenges. As of mid-2024, India has a total manufacturing capacity of 77.2 GW for modules and 7.6 GW for cells. Domestic production has been spurred by policies like the reinstatement of the Approved List of Models and Manufacturers (ALMM) and the Production-Linked Incentive (PLI) scheme. These measures aim to reduce dependence on imports and promote local production .

Large manufacturers dominate, with the top 10 companies accounting for 58% of module capacity and all cell production. However, domestic production is still insufficient to meet the growing demand, leading to tight supply and elevated prices. The market also focuses on advanced technologies like monocrystalline PERC and TOPCon modules .

Despite increased capacity, Indian manufacturers face challenges such as inadequate cell production, reliance on imports for raw materials, and a volatile global market. Export contributions are declining, but domestic demand is expected to rise, ensuring manufacturers have a stable market. Operating margins are projected to stabilize at 12-14% as domestic competition intensifies .

The government plans to boost domestic capacity to 172 GW for modules and 80 GW for cells by 2026, but overcoming supply chain bottlenecks will be critical to meeting targets and ensuring timely project execution .

Some players already expecting oversupply by the end of fy27-28.

China provides an excellent example of how large solar module manufacturers have outperformed smaller ones in a matured and highly competitive market. “I might be completely wrong, but I’m sharing some insights.”

Here’s how the factors to the Chinese solar industry:

Economies of Scale

China’s large manufacturers like LONGi Green Energy, Jinko Solar, and Trina Solar produce solar modules on an enormous scale, enabling them to dominate the market:

• LONGi’s Leadership: In 2023, LONGi was the largest solar module supplier globally, leveraging massive production capacities and cost efficiency.

• Lower Costs: These companies achieve economies of scale by sourcing polysilicon, wafers, and other materials at low costs due to bulk purchases and in-house production.

Smaller manufacturers struggle because they cannot match the price advantages or efficiencies of these giants.

Technological Advantages

• R&D Investment: LONGi invests heavily in R&D to develop high-efficiency monocrystalline modules like bifacial panels. This has allowed it to differentiate its products and capture premium segments.

• Smaller Players: Smaller companies lack resources for significant R&D, forcing them to compete on price alone, which is unsustainable.

Financial Strength

• Access to Capital: Chinese giants benefit from state-backed financing and favorable government policies, allowing them to expand production, invest in new technologies, and weather global supply chain disruptions.

• Market Downturns: During periods of oversupply or price wars (e.g., 2017 and 2018), large players survived due to better liquidity, while many smaller companies exited the market.

Global Reach

• Companies like Jinko Solar and Trina Solar export modules to over 100 countries, diversifying their revenue streams and reducing dependency on China’s domestic market.

• Smaller players often rely on local markets, leaving them vulnerable to domestic policy changes or price competition.

Vertical Integration

• Chinese giants have integrated operations across the solar value chain, from polysilicon production to module assembly.

• For instance, LONGi produces its own wafers, ensuring cost control and consistent quality.

• Smaller companies depend on third-party suppliers, making them vulnerable to price fluctuations and supply shortages.

Brand Reputation and Trust

• Buyers in the global market prefer large Chinese manufacturers due to their established brand reputation, quality assurances, and long-term warranties.

• Smaller companies struggle to gain the same level of trust, especially in international markets.

Price Wars and Market Consolidation

• China’s solar market has experienced intense price wars. Large manufacturers like LONGi and Jinko Solar managed to sustain operations with razor-thin margins, while smaller competitors couldn’t survive.

• Over the past decade, market consolidation has reduced the number of small manufacturers, with large companies capturing the majority of the market share.

Government Support

• The Chinese government’s policies, like subsidies, export incentives, and favorable loans, have favored larger manufacturers with the capacity to scale.

• Smaller manufacturers have not benefited equally and have often been squeezed out of the market.

Outcome in China

• Dominance of Large Players: By 2024, companies like LONGi, Jinko Solar, and Trina Solar have captured over 60% of the global solar module market.

• Decline of Small Players: Smaller Chinese manufacturers either exited the market or shifted to niche or less profitable segments due to the inability to compete on cost and scale.

Large manufacturers in India, like Adani Solar, Waaree Energies, and Tata Power Solar, can leverage their scale and resources.

In conclusion, the Chinese solar market illustrates how large manufacturers dominate through scale, innovation, and integration, leaving smaller players struggling to compete in a mature market. This trend is likely to replicate in other regions as solar markets develop further.

Hear what Waree has to say

ALCM coming from 1st June,2026

The interesting point to note from MNRE circular is" ALMM List-1 (module companies) should use cells from ALMM List-2 ( cell companies) post June 2026". Otherwise they will be removed from ALMM List-1.

Solar cell companies will be in driving seat and they should get their due valuation.

It is like all Govt projects will use modules made of Indian solar cells. A big support from Govt. for Solar cell companies. If Websol implements their plan of 2.4 GW Cells by 2027 then ALMM list-2 will help them to sustain their earnings.