Valid apprehension… but DCR component itself is a big market and they are the leader as backward integration on account of solar cell has been completed . Hope they can show good strength

3 Likes

Will the sale affect Waaree adversely?

2cd9b12a-285d-4217-b5b7-bddbfb108a88.pdf (861.3 KB)

Waaree energies bags order of 432MW module manufacturing from US Client

dd970ae5-18f3-4838-9b00-9a54df6fb478.pdf (1.0 MB)

1 Like

While Waaree Energies has announced a significant 452 MW solar module order through its US subsidiary, I remain cautious about such disclosures. Historically, companies have sometimes announced large orders to maintain investor sentiment, especially during periods of policy uncertainty such as US tariff changes. Since there is no regulatory penalty for order cancellations, these announcements should be viewed critically. In my opinion, the real credibility lies in the execution and revenue recognition of these contracts, rather than the order announcements themselves.

9 Likes

Is it mandatory for companies to disclose orders to exchanges or do they do it for building investor sentiment.

1 Like

They are supposed to submit any information that may significantly impact the share price as per the guidelines and thus exchange recommends to submit order inflows as well.

2 Likes

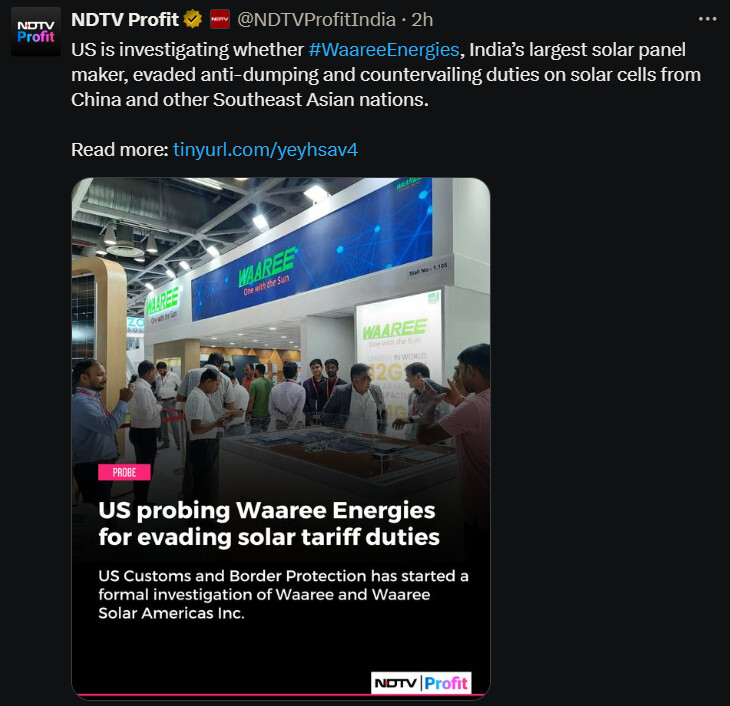

Anybody analysed the effect of anti-dumping measures on Waaree Energies?

2 Likes

@Vivek_Lodariya , what will be the effect of this legal battle on Waaree? Or its not that serious?

3 Likes

Waaree Energies Limited has acquired 64% equity stake in Kotsons Private Limited through a primary capital infusion of about Rs.192 crores , making Kotsons a subsidiary of Waaree Energies. The proceeds of this infusion will be utilized to further expand Kotsons’ manufacturing capacity, enabling it to meet the growing domestic and global demand for transformers.

As per the company, “The acquisition comes at a pivotal time for India’s power infrastructure sector. The country’s transformer market is expected to grow at a CAGR of 8–10%, reaching USD 5–6 billion by 2030, with demand expanding at 7.44% CAGR. This growth will be driven by emerging sectors such as green hydrogen, EV charging infrastructure, data centres, 5G rollout, and railways. By integrating Kotsons into its portfolio, Waaree not only gains a strong foothold in this expanding market but also strengthens its vertical integration, enabling greater control over technology, quality, and sustainability.”

15 Likes

Waaree Forever Energies Private Limited, has created three new smaller subsidiary companies. These new companies are Waaree Forever Energies Four Private Limited, Waaree Forever Energies Five Private Limited, and Waaree Forever Energies One Private Limited.

These new companies were formed in September 2025 and have no business or earnings yet because they are newly started. The main purpose of these new companies is to develop and manage specific power projects under an Independent Power Producer (IPP) model. Waaree Forever Energies Private Limited fully owns these new companies.

4 Likes

Has anybody found anything in their balance sheet which tars or exonerates them?

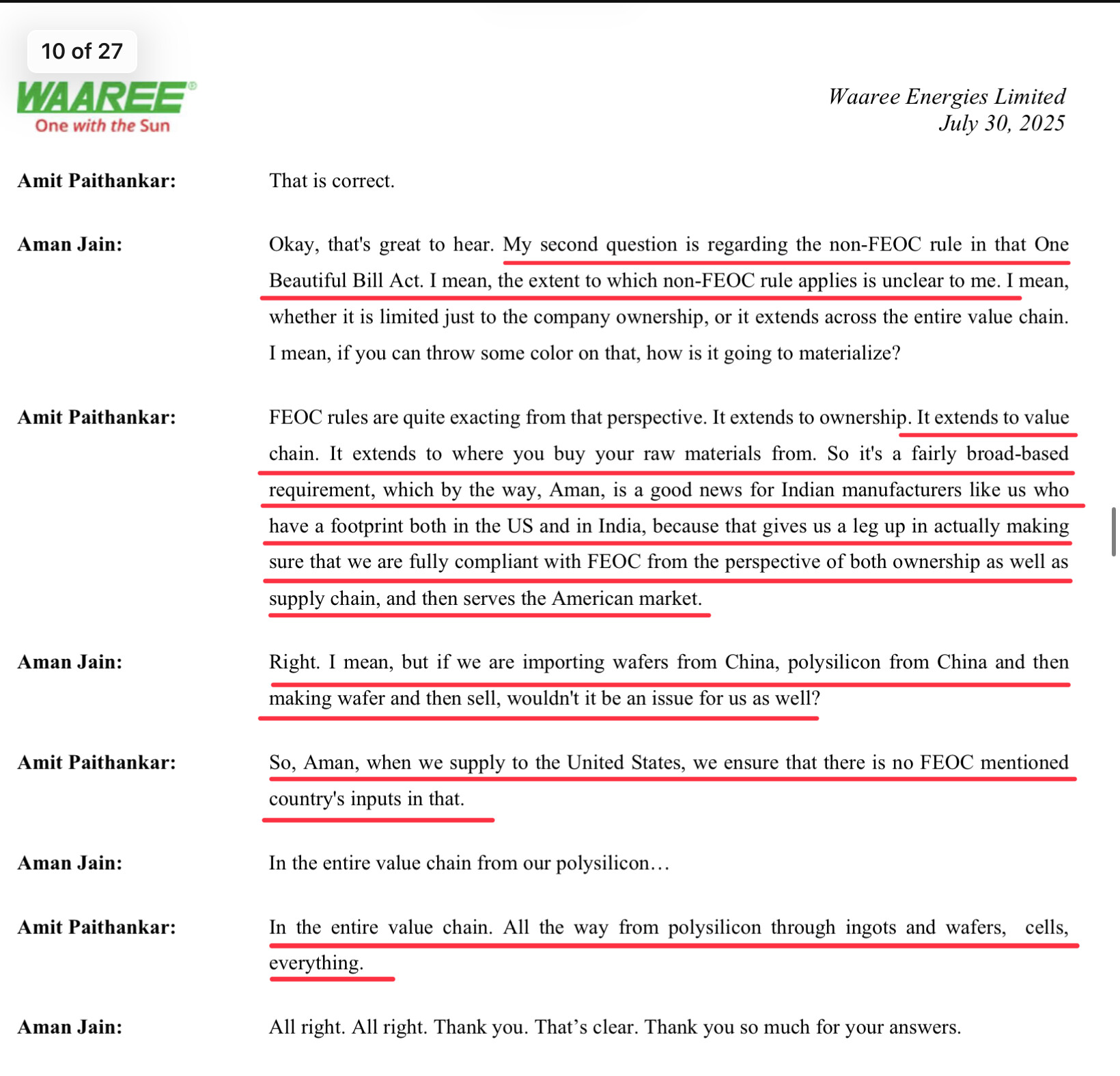

This was the management response in the last investor call . But I am not sure how they can source Polysilicon, Ingot and wafer from non China sources even if cell is some how sourced from non China sources. However Mr. Paithnakar is categoric in his statement.

5 Likes

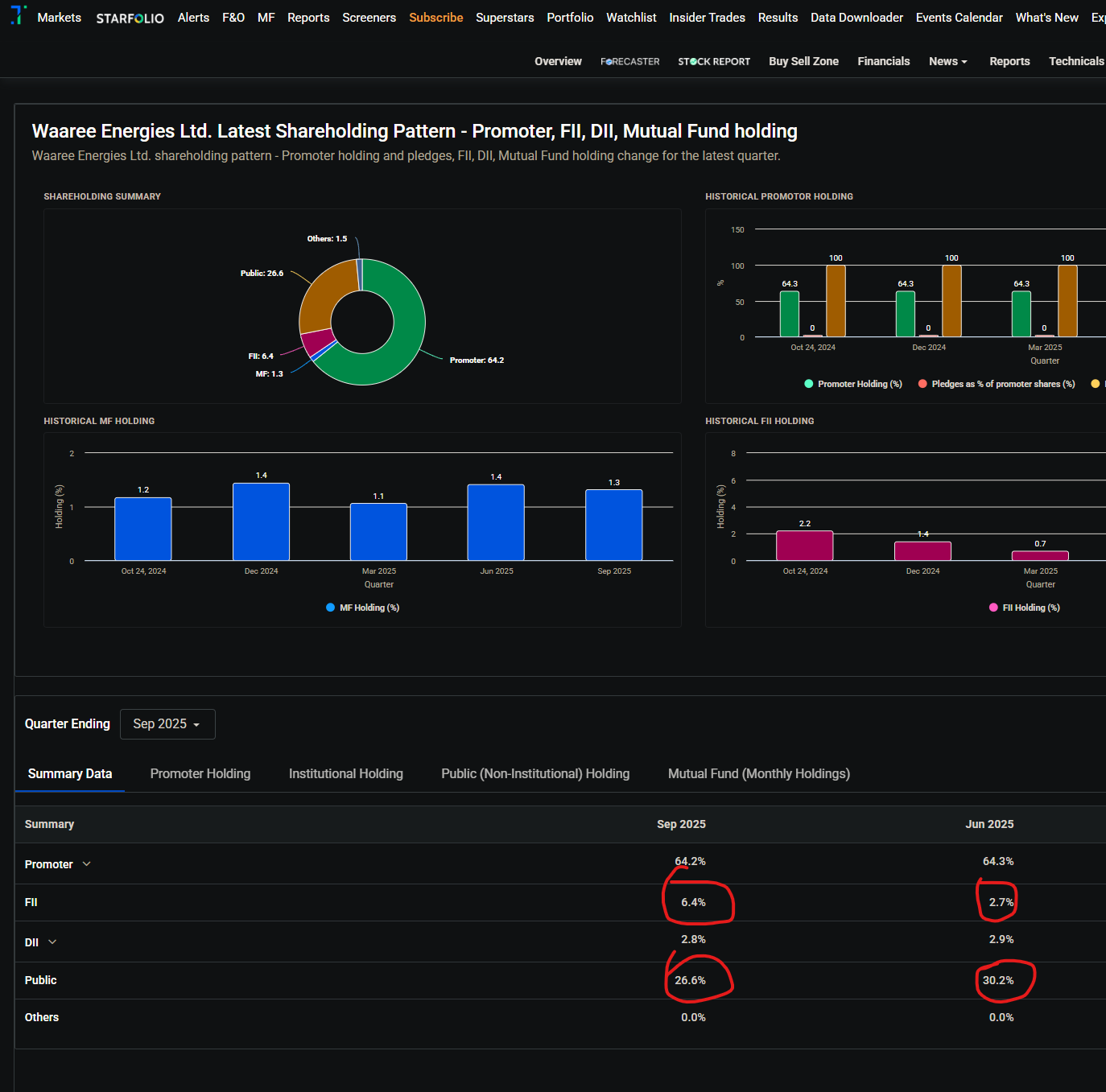

in a quarter dominated by FII selling across the market, i see significant increase in FII holding alongwith decrease in Public holding incase of Waree Energies, should be good signs (Disc : Invested heavily)

9 Likes

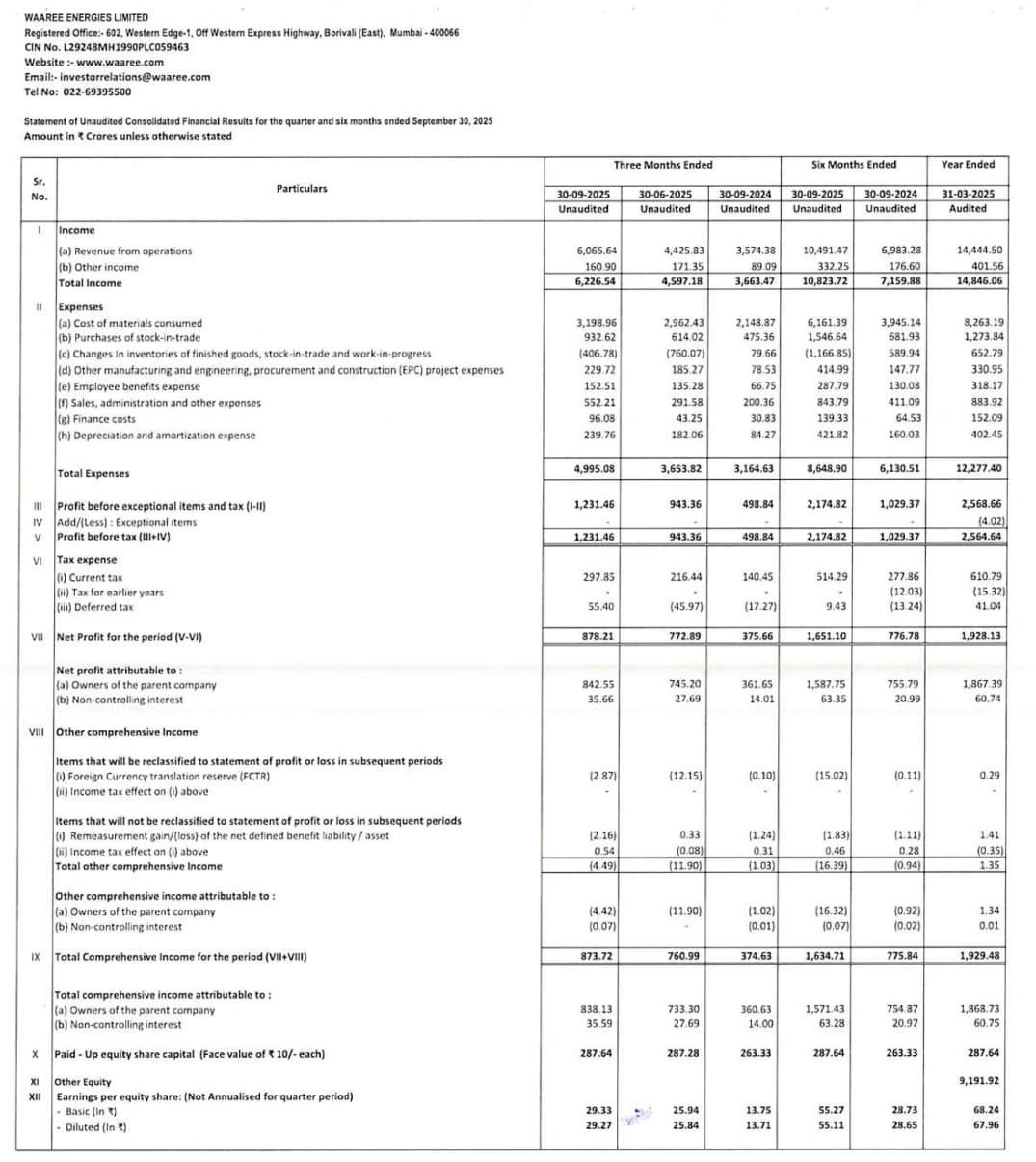

Concall Q2FY26 - Overall a set of good results. However that said, below is something to be monitored further, though management is mentioning as “The supply chain is configured to be fully compliant with US laws (like FEOC) and to attract the lowest possible tariffs.”

Regulatory Risk (US AD/CVD): This was a recurring theme in the analyst Q&A. The US has initiated an anti-dumping/countervailing duty (AD/CVD) investigation into solar cells from India and other countries. If significant duties are imposed, it could impact the profitability of exports from India. Management’s response was that the probe is in its early stages and they are confident they can navigate it due to their US manufacturing footprint and transparent pricing. However, this remains a key external risk to monitor.

Also the real progress on US exports Inventory pile-up needs to be monitored in upcoming months

6 Likes

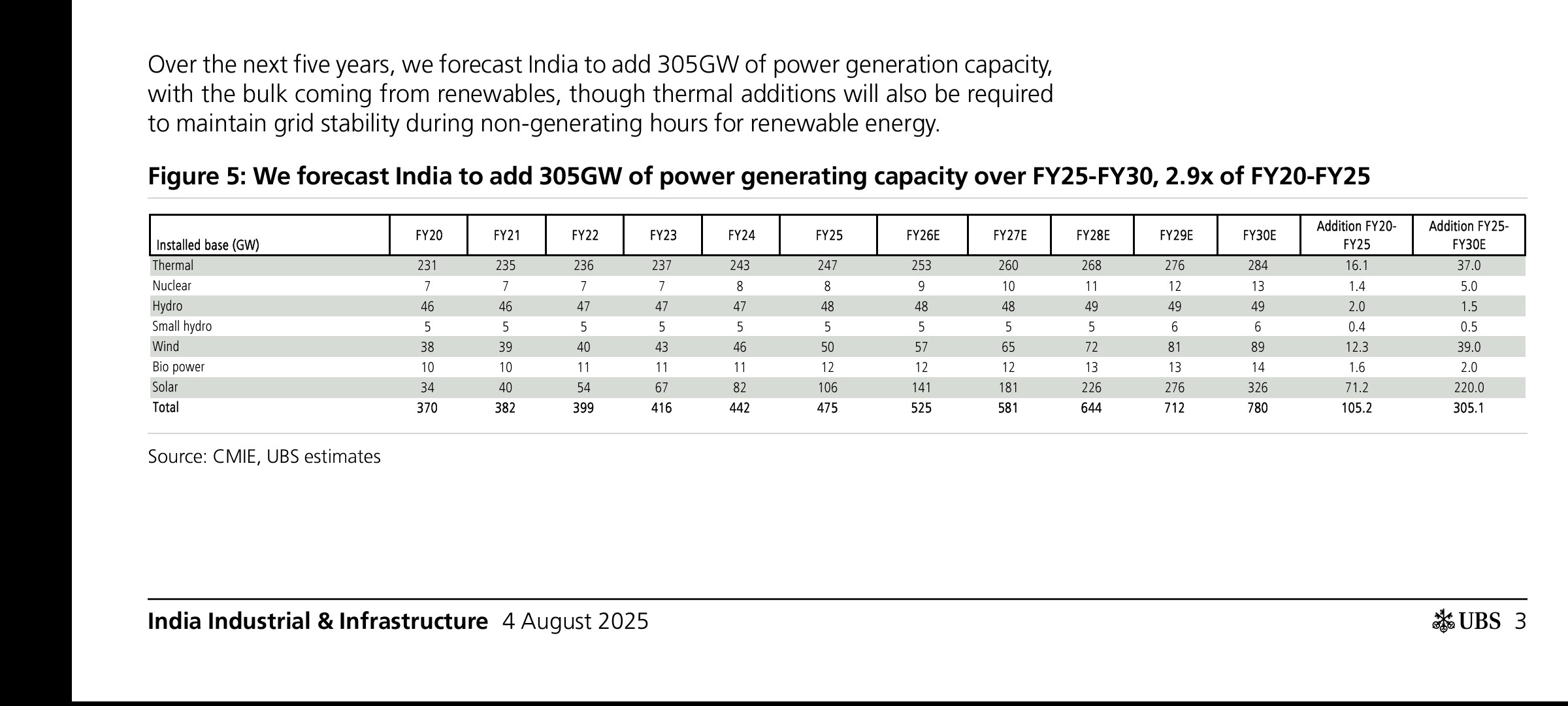

things look sorted till FY27, but we need to watch out for saturation after that: https://x.com/EquityInsightss/status/1980160633233617260

1 Like