About Waaree Energies Ltd -

Incorporated in December 1990, Waaree Energies Limited is an Indian manufacturer of solar PV modules with an aggregate installed capacity of 12 GW.

Key Points

Market Leadership

Waaree Energies is India’s largest manufacturer and exporter of solar modules. As of FY24, it holds a 21% share of the domestic market for solar modules and a 44% share in India’s solar module exports. Its installed capacity surged from 2GW in FY21 to 13.3GW by FY24.

Product Portfolio

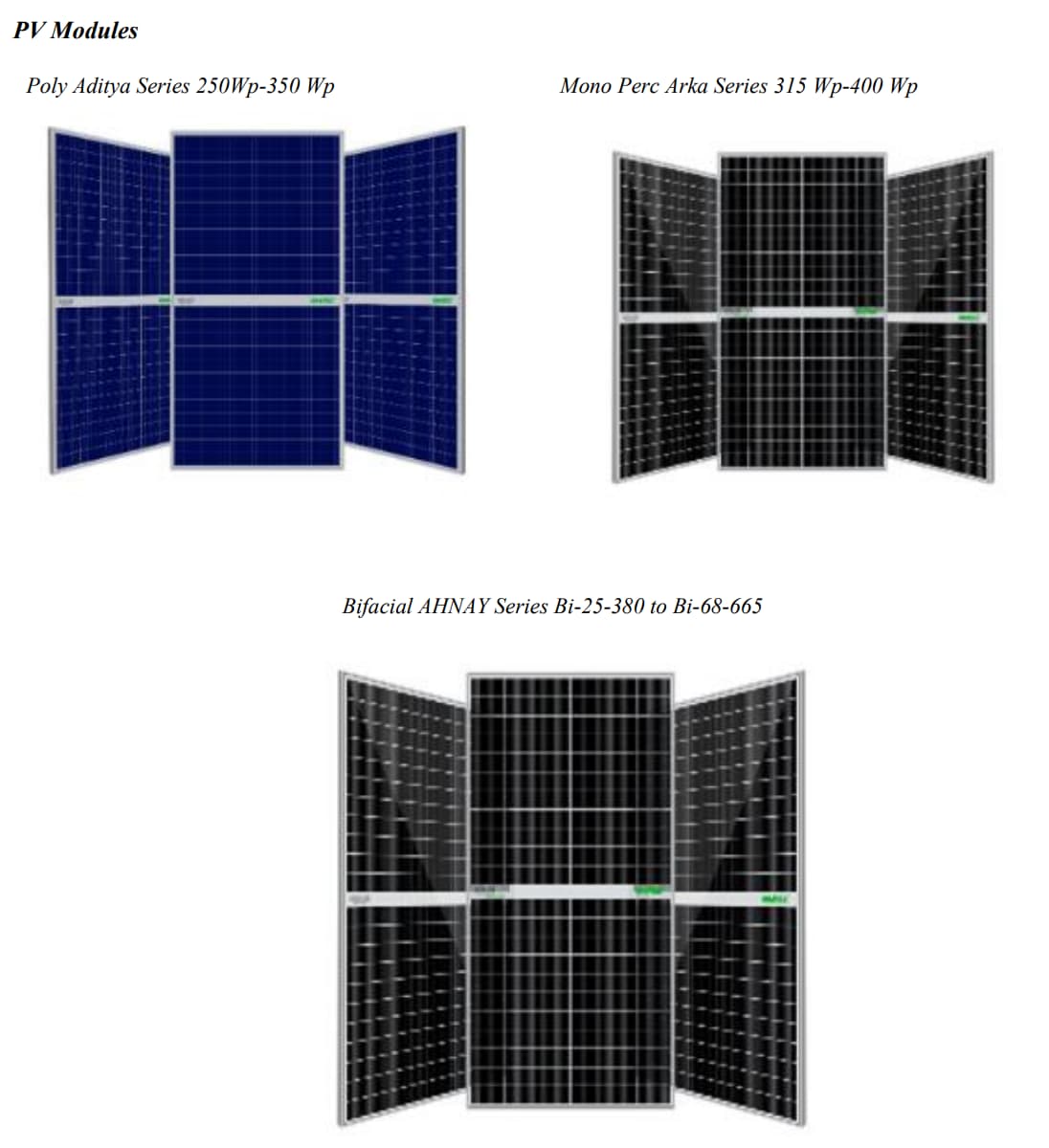

The solar PV modules are manufactured using multicrystalline, monocrystalline, and advanced technologies like Tunnel Oxide Passivated Contact (TOPCon), which minimizes energy loss and boosts efficiency.

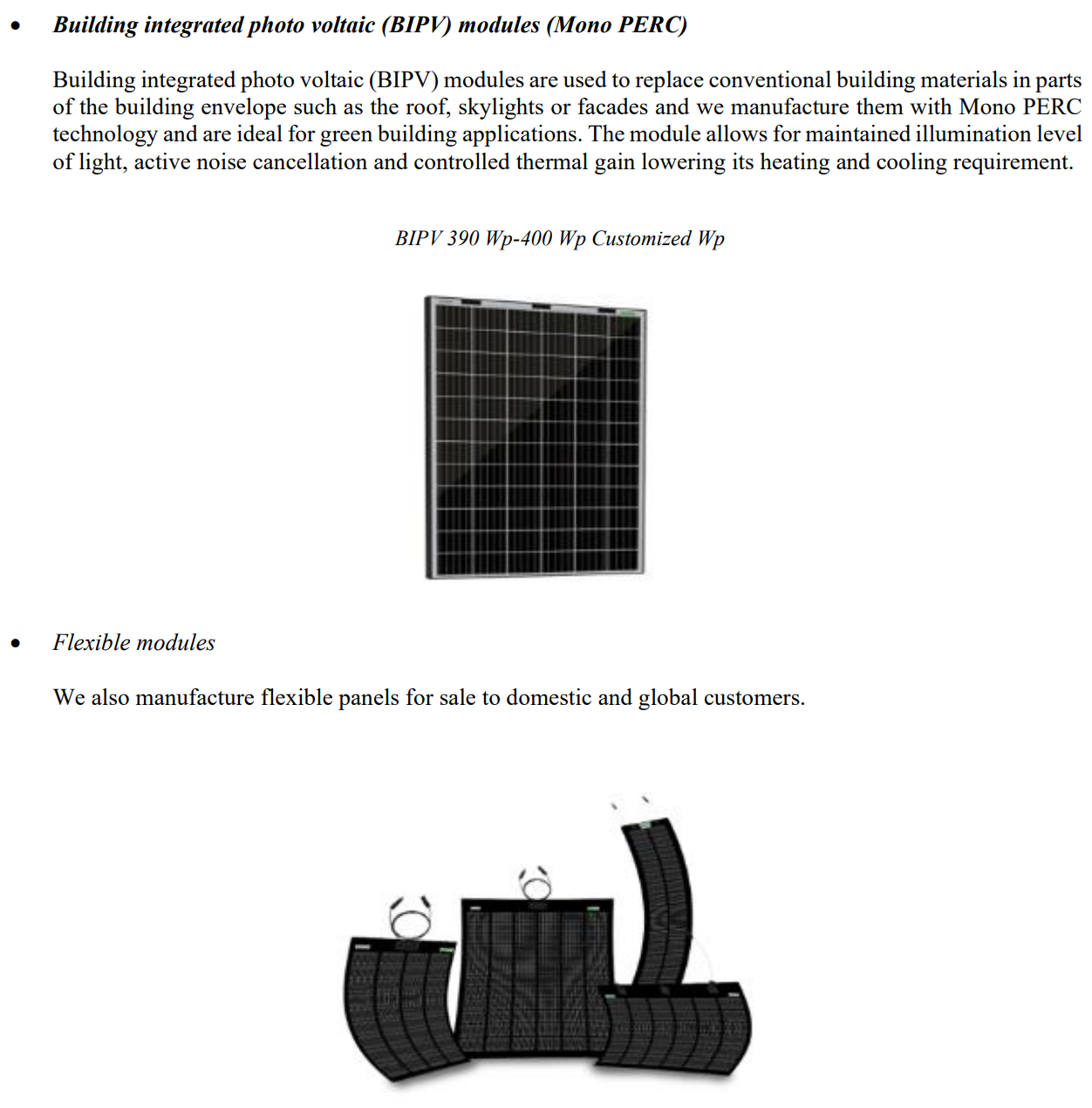

Its product range includes multicrystalline modules, monocrystalline modules, TOPCon modules, flexible modules, bifacial (Mono PERC) modules, and building integrated photovoltaic (BIPV) modules.

Manufacturing Facilities

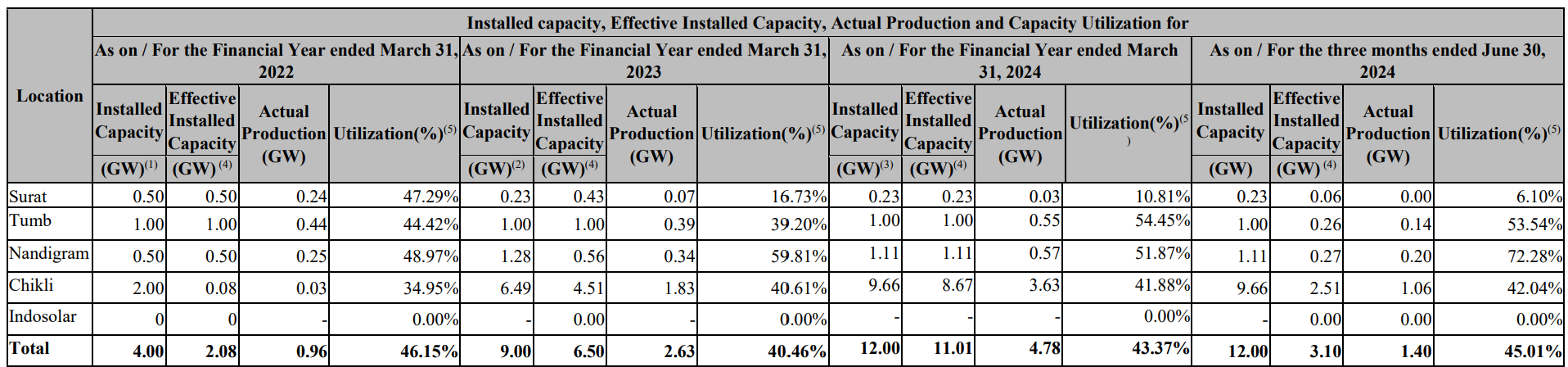

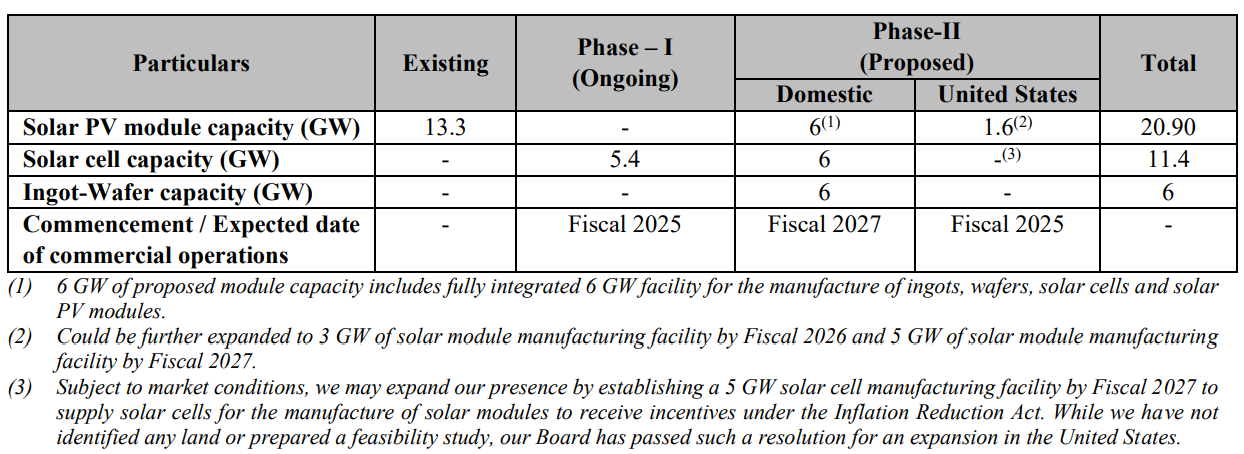

Waaree Renewables operates 5 manufacturing facilities in India. These are in Gujarat (Surat, Tumb, Nandigram, and Chikhli) and Uttar Pradesh (Indosolar Facility, Noida). With a total installed capacity of 12 GW as of June 2024, the company is expanding its facilities to 20.9 GW by 2027, including backward integration into solar cells, ingot, and wafer production.

Plant A: Located in Chikhli, Gujarat, this plant is the largest, with a capacity of 9.66 GW, producing both monocrystalline and multi-crystalline modules.

** Trading Business**

The company engages in the trading of solar components, including inverters, batteries, and solar water pumps, sourced from global suppliers.

** Revenue Bifurcation - Product wise**

- Solar PV Modules: 78%

- Solar EPC Services: 15%

- Energy Storage Systems & Others: 7%

Revenue Bifurcation

- Export Sales: 57.64%

- Direct Sales to Utilities and Enterprises: 30.05%

- Retail Sales: 10.15%

- Other Income: 0.8%

International Business

The company exports solar PV modules to markets including the United States, Canada, Italy, Hong Kong, Turkey, and Vietnam. The U.S. is their largest export market, accounting for 57% of export sale

New International Manufacturing Facility

Waaree is setting up a 1.6GW solar PV module manufacturing facility in Houston, Texas, to cater to demand in the United States. This facility is expected to be operational by the end of FY25, with plans to expand capacity to 5GW by FY27

Focus on Backward Integration

Waaree Energies is working towards reducing its dependency on imported solar cells by establishing domestic manufacturing capabilities.

Waaree is setting up a fully integrated 6 GW facility in Odisha for the production of ingots, wafers, solar cells, and solar PV modules. This facility is expected to commence commercial operations by FY27

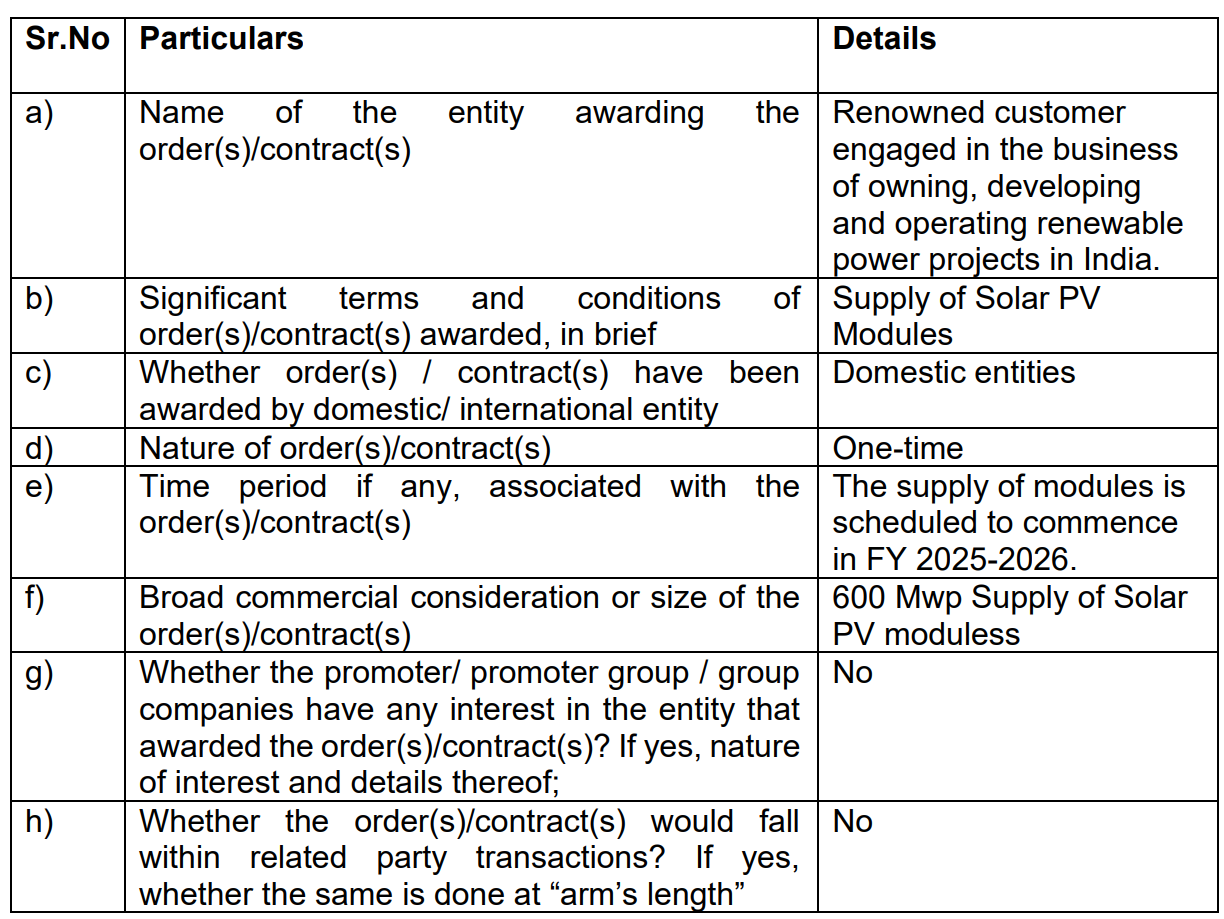

Order Book

As of June 30, 2024, Waaree Energies Limited boasts a substantial 16.6 GW order book for solar PV modules, including domestic, export, and franchisee orders.

Clients

In FY23, Co. served 566 Customers in India and 33 International customers.

Top 1 Customer - ** 9% of FY24 revenue

Top 10 Customers - ** 57% of FY24 revenue

IPO Details

Co. raised 4,321 Crs through the IPO and got listed on Oct 28, 2024.

The fresh issue of 3600 Crs will be utilized for:

A) Financing the CAPEX of establishing the Odisha Plant.

B) General corporate purposes.

| Narration | Jan-00 | Jan-00 | Jan-00 | Jan-00 | Jan-00 | Mar-20 | Mar-21 | Mar-22 | Mar-23 | Mar-24 | Trailing | Best Case | Worst Case |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Sales | - | - | - | - | - | 1,995.78 | 1,952.78 | 2,854.27 | 6,750.87 | 11,397.61 | 6,737.19 | 20,521.10 | 16,034.93 |

| Expenses | - | - | - | - | - | 1,903.01 | 1,867.93 | 2,748.32 | 5,915.06 | 9,822.80 | 5,717.12 | 17,414.02 | 14,303.52 |

| Operating Profit | - | - | - | - | - | 92.77 | 84.85 | 105.95 | 835.81 | 1,574.81 | 1,020.07 | 3,107.08 | 1,731.42 |

| Other Income | - | - | - | - | - | 25.01 | 44.65 | 96.58 | 87.74 | 576.11 | 174.22 | - | - |

| Depreciation | - | - | - | - | - | 27.13 | 28.54 | 43.27 | 164.13 | 276.81 | 132.64 | 132.64 | 132.64 |

| Interest | - | - | - | - | - | 33.71 | 29.66 | 40.88 | 82.27 | 139.91 | 73.77 | 73.77 | 73.77 |

| Profit before tax | - | - | - | - | - | 56.94 | 71.30 | 118.38 | 677.15 | 1,734.20 | 987.88 | 2,900.67 | 1,525.01 |

| Tax | - | - | - | - | - | 17.92 | 23.79 | 38.72 | 176.88 | 459.82 | 248.50 | 25% | 25% |

| Net profit | - | - | - | - | - | 41.71 | 48.51 | 75.64 | 482.76 | 1,237.18 | 730.17 | 2,171.01 | 1,141.39 |

| EPS | - | - | - | - | - | 2.12 | 2.46 | 3.84 | 24.49 | 62.77 | 25.42 | 75.57 | 39.73 |

| Price to earning | 131.73 | 131.73 | 131.73 | ||||||||||

| Price | - | - | - | - | - | - | - | - | - | - | 3,348.15 | 9,955.02 | 5,233.79 |

| RATIOS: | |||||||||||||

| Dividend Payout | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | |||

| OPM | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 4.65% | 4.35% | 3.71% | 12.38% | 13.82% | 15.14% | ||

| TRENDS: | 10 YEARS | 7 YEARS | 5 YEARS | 3 YEARS | RECENT | BEST | WORST | ||||||

| Sales Growth | 80.05% | 68.83% | 80.05% | 68.83% | |||||||||

| OPM | 10.80% | 10.80% | 10.80% | 11.98% | 15.14% | 15.14% | 10.80% | ||||||

| Price to Earning | 131.73 | 131.73 | 131.73 | 131.73 | 131.73 | 131.73 | 131.73 | ||||||

| Source - Screener |

Risks

- Policy and Regulatory Changes: Shifts in government incentives or tariffs for renewable energy could impact revenue and profitability.

- Intense Competition: A crowded market with many local and international players could lead to price pressures and margin compression.

- Supply Chain Disruptions: Reliance on raw materials and imported components exposes Waaree to risks from supply shortages and price volatility.

- Technology and Innovation Risks: Rapid advancements in solar technology require continuous investment; falling behind could reduce competitiveness.

- Financial Dependence on Subsidies: Changes or reductions in government subsidies and incentives could reduce demand for solar projects, affecting Waaree’s growth.

A closer look -

Products and offerings

Manufacturing Facilities

Utilization

Expansion plans

Disclosure - Invested