i have extracted the trascript from this youtube video and summarized it via chatgpt:

Opening Remarks (Management)

- Speakers: Amit Bitankar (CEO), Sonal Srivastava (CFO), Abhishek Parikh (Group Head Finance), Rohit Wade (Investor Relations).

- Highlights:

- FY25 was a landmark year:

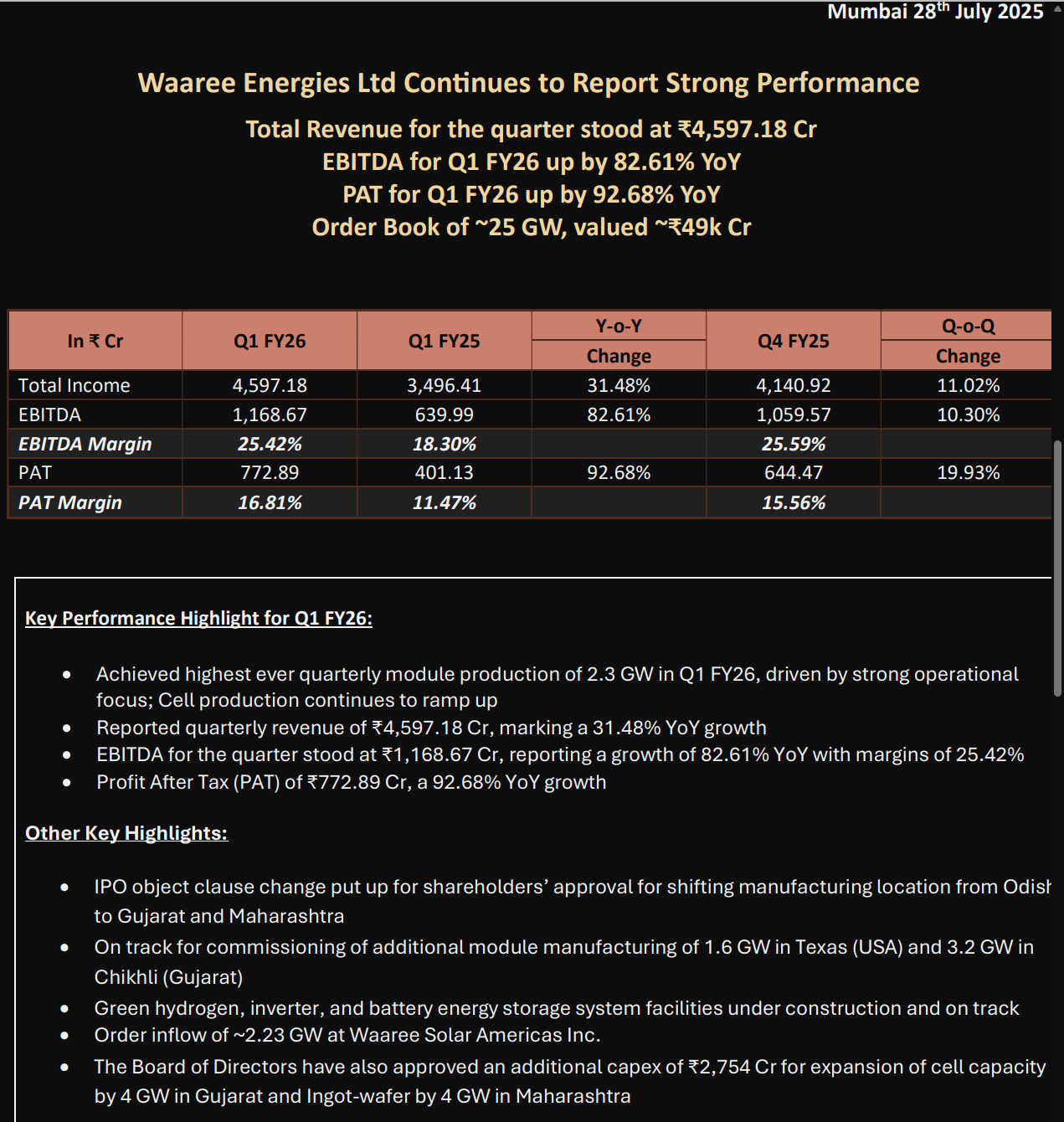

- Revenue: ₹14,846 crore (+27% YoY).

- EBITDA: ₹3,123 crore (+72.6% YoY), EBITDA margin improved to 21.04% from 15.56%.

- PAT: ₹1,928 crore (+51.3% YoY).

- Order book: Robust at ₹47,000 crore.

- Funds available: ₹15,550 crore.

- Module manufacturing capacity: Now at 15 GW — the largest in India.

- Cell factory: 5.4 GW commissioned.

- US operations: 1.6 GW manufacturing facility operational; IndoSolar acquisition posted ₹55 crore profit.

- IPO success: Strong investor participation.

- Recognitions:

- Tier 1 PV Module Supplier (BNEF).

- EcoVadis Gold Medal.

- CARE Ratings upgraded to A+ (long-term) and A1+ (short-term).

Strategic Initiatives

- Backward Integration:

- Targeting additional 4.8 GW by FY27.

- 6 GW integrated wafer-cell-module factory in development.

- Battery storage (3.5 GW) and green hydrogen (300 MW electrolyzer) facilities scheduled by 2027.

- Forward Integration:

- Expanding into power infrastructure — 17.57 GW in development.

- EPC business (V Renewable Tech) under execution: 3.2 GW.

- 3 GW inverter facility by late FY26.

Sustainability Focus

- Committed to net-zero emissions:

- Scope 1 & 2 by 2030.

- Scope 3 by 2040.

- Achieved environmental product declarations for modules.

- Aiming for lowest carbon footprint in the industry.

Financial Guidance for FY26

- EBITDA projected: ₹5,500–6,000 crore.

- Confidence backed by order book strength, integration across value chain, and execution capabilities.

Analyst Q&A — Key Highlights

1. DCR (Domestic Content Requirement) Strategy:

- 5.4 GW cell plant running.

- Strong DCR order build-up, especially in retail segment (~1.5 GW anticipated).

- Margins expected to benefit.

2. US Business and Tariffs:

- 17–20% of revenue from US exports.

- Managing tariff uncertainties through flexible production in India and US facilities.

- Current US tariff on Indian imports: 14% (with risk of an additional 26%).

3. Order Book Details:

- 45% India, 55% Overseas (mostly US).

- Orders secured with advances.

- EPC order book (~3.2 GW) included in the total.

4. Capacity Utilization (CUF):

- Varies from 60% to 90%.

- Focused on maximizing EBITDA rather than only volume growth.

5. Future Revenue Mix:

- FY26: Still mostly manufacturing and EPC.

- New segments (batteries, green hydrogen) expected to contribute from FY27.

6. Margin and Cost Management:

- Raw material cost optimization is key.

- Gross margins have improved even with stable module realizations (~21 cents/Watt).

7. Retail Business Contribution:

- Around 23–25% of revenue.

8. Financial Health:

- Customer advances at ₹4,000–4,400 crore.

- No major exceptional income included in EBITDA guidance.

In Short:

Waaree Energies reported a record FY25, delivered strong growth across all fronts, successfully expanded capacities, strategically integrated backward and forward, and gave a confident FY26 growth outlook while proactively managing risks like US tariffs.

5 Likes

means 7.13 GW production generated respective Revenue

how long order book take to realize into revenue

Saw a recent notification of internal transfer of Promoter shares within family from Juniors to Seniors. Not sure how to take it. Generally it should happen the opposite way right?

1 Like

I’m currently holding the stock at an average price of ₹2,478. The recent concall seemed quite positive — the management sounded confident, guiding for an EBITDA of ₹5,500–6,000 Cr. However, despite this upbeat outlook, there hasn’t been any meaningful positive price action.

Would appreciate thoughts from fellow members — how should one interpret this? Is the market still skeptical or is it just a matter of patience?

4 Likes

It’s just a matter of patience.. company is going great guns .. I had a discusson with the management and they are confident enough ..

Enhanced capacity on account of solar cell will definitely increase top line ..

There is huge demand in DCR solar panel because of subsidy and now that company has started solar cell production as backward integration coupled with tail wind in the sector market will definitely react positively

7 Likes

Anybody compared the two Waarees, Renewable and Energies? Would be so grateful for your views.

In simple analogy Renewable is a EPC company and energies is a tech company do PV panels,BESS and Hydrogen energy (Recently bought another transformer company).

6 Likes

Waaree Energies Factory visit

Cell Manufacturing Capacity

-

A single production line can manufacture 6,800 cells per hour, resulting in 163,200 cells per day and 53.85 million cells annually (based on 330 operational days).

-

The company will operate three lines: one PERC and two TopCon, bringing the total annual cell manufacturing capacity to 161.56 million (16.1 crore) cells.

-

All plants, including the Noida facility, operate at over 75% utilization.

-

Maintenance shutdowns for cell manufacturing are planned for two days annually.

Technology & Maintenance

-

Chinese and Thai technicians oversee the assembly of new technology and machinery, while Indian technical teams manage operations post-installation.

-

The company maintains a stock of critical spare parts to address emergencies efficiently.

Competitive Landscape

-

Management acknowledges the presence of multiple players in the industry and anticipates new entrants.

-

Previously, competition was in a smaller market with lower gigawatt capacity, but now they are competing on a larger scale against bigger players.

-

No significant oversupply concerns are foreseen in India, mainly due to China’s market dynamics.

USA Subsidiary vs. Waaree India Business

-

Both the USA subsidiary and Waaree India will manufacture solar modules.

-

However, they will not compete against each other, as both will be local players with a strategic focus on their respective markets.

-

The Indian business benefits from cost advantages, whereas the USA subsidiary will gain an edge through local manufacturing incentives.

Cell Procurement & Government Schemes

- Imported cells from China cannot be used for government schemes.

- Currently, they source cells at a higher price from external suppliers, but costs will decrease once their in-house cell production becomes operational.

Cell Plant Infrastructure

The company’s cell manufacturing capacity currently supports only one-third of its module production needs

10 Likes

Waaree Energies -released All in one solar Kit.

“With Waaree Radiance, we’re initiating a nationwide movement aligned with PM Surya Ghar to bring solar energy to every Indian rooftop,” said Mr. Nilesh Malani, Chief Marketing Officer, Waaree Energies Limited. “Our goal is to educate, inspire, and engage homeowners who are ready to take charge of their energy future. By simplifying the solar adoption journey and delivering it through an integrated brand experience, Waaree Radiance is truly illuminating homes, minds, and possibilities.”

Running from July 21, 2025, the campaign will span key cities across Gujarat, Maharashtra, Rajasthan, Uttar Pradesh, Kerala, Tamil Nadu, Madhya Pradesh, Andhra Pradesh and Telangana, aiming to build widespread awareness and adoption. In addition to its technical simplicity, Waaree Radiance supports customers with online warranty registration, Waaree’s trusted nationwide support network, and availability through over 400 Waaree franchises across India—ensuring that help is always close to home.

8 Likes

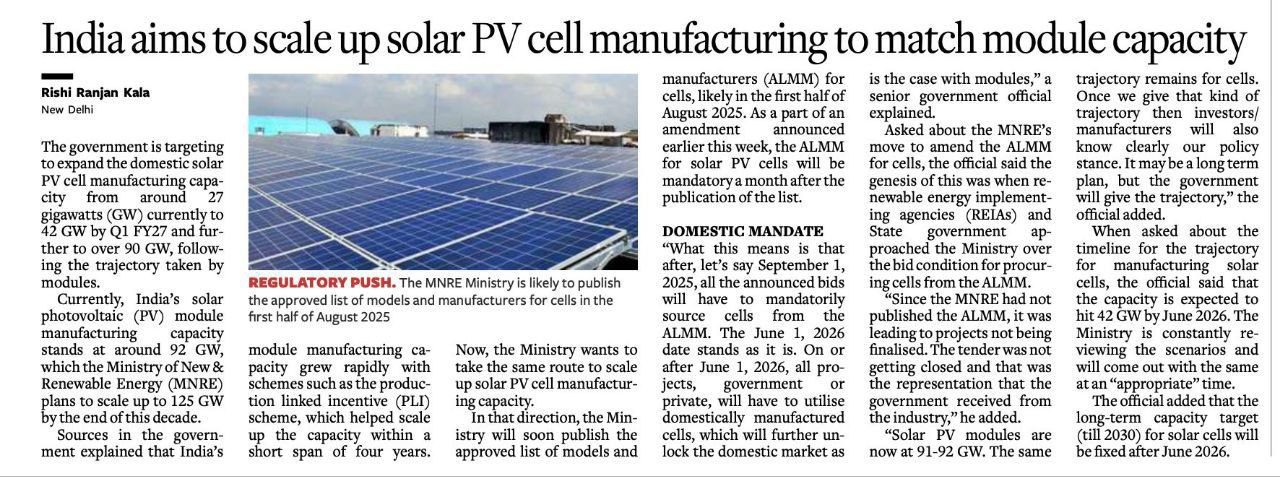

This ALMM will help waaree and on top of it aggressive ramp of cells capacity to match modules

2 Likes

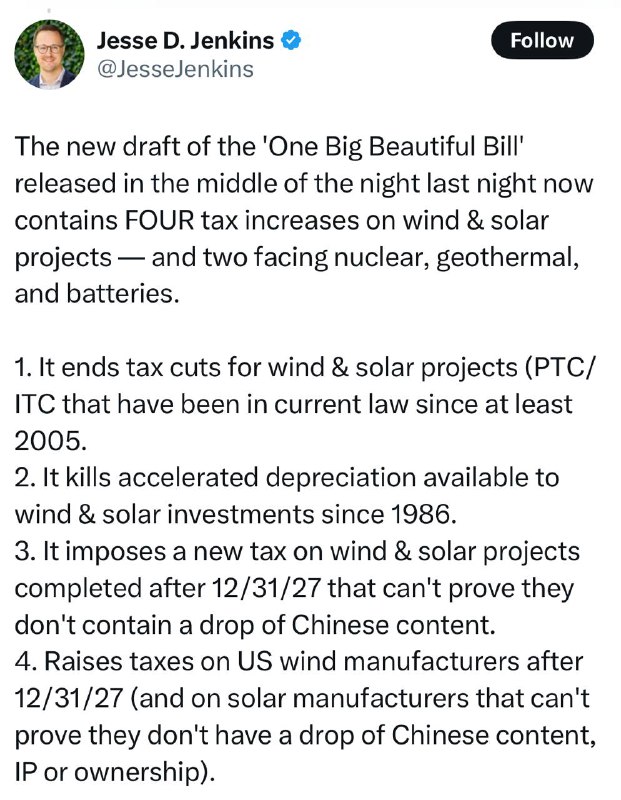

This company is doing everything right. But with China slashing solar panel rates, if I am right, China is almost 40-50% cheaper than India. What chance would Waaree have globally without govt intervention?

3 Likes

Transcript of Analyst /Institutional Investors Meeting on Financial Results for the Quarter ended June 30, 2025

1 Like