Waaree Group Begins 300 MW Electrolyser Manufacturing In Gujarat To Boost India’s Green Hydrogen Mission.

2 Likes

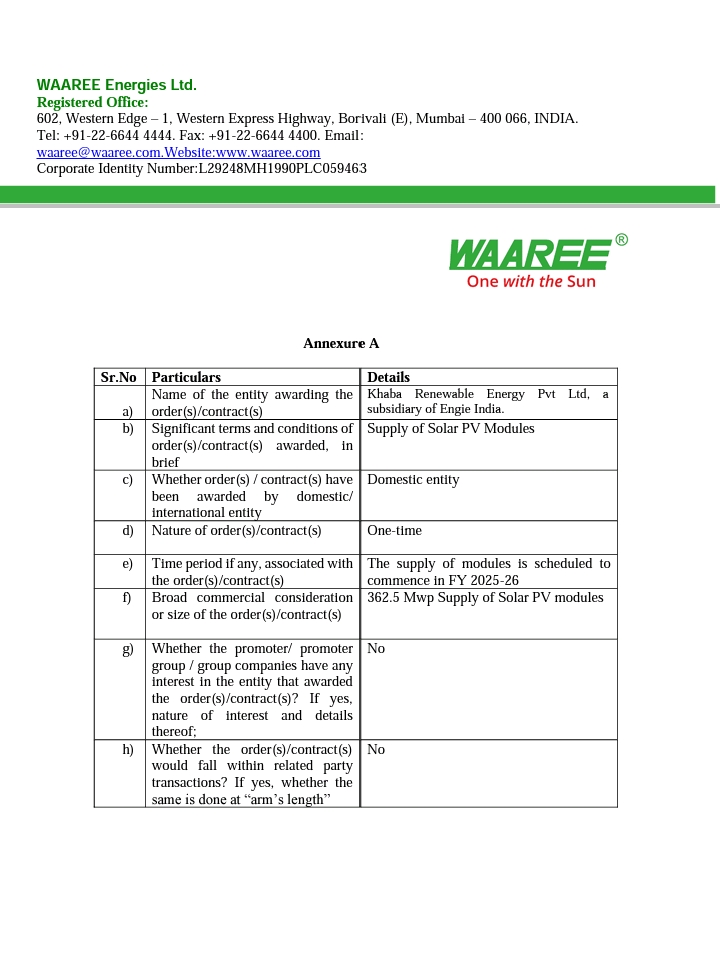

An order for the supply of solar modules for 362.5 MWp has been awarded by Khaba Renewable Energy to the company.

1 Like

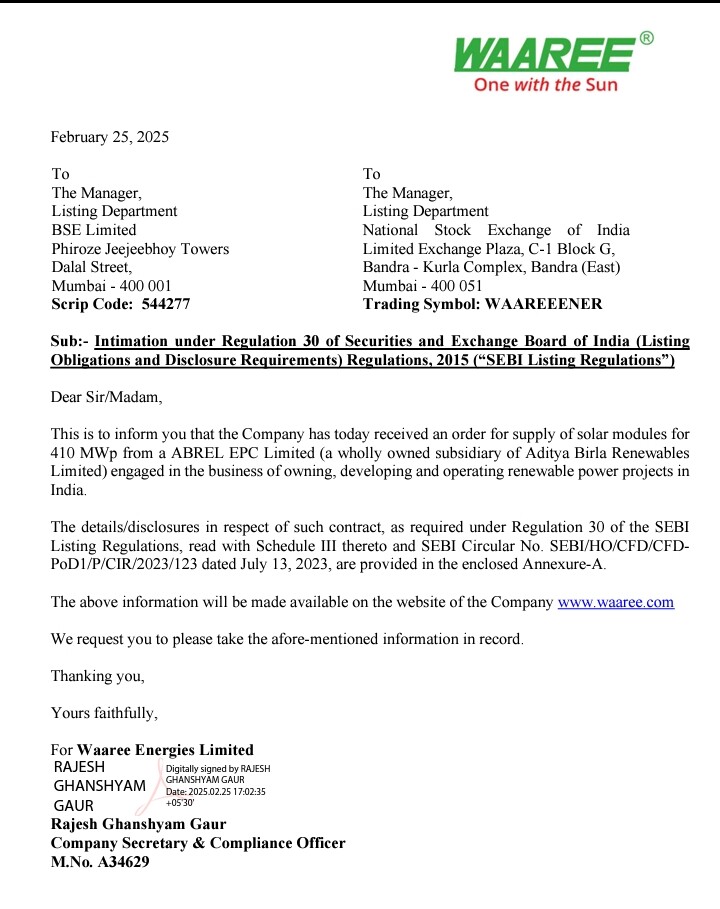

Company on 25-02-2025 received an order for supply of solar modules for 410 MWp from a ABREL EPC Limited (a wholly owned subsidiary of Aditya Birla Renewables Limited) engaged in the business of owning, developing and operating renewable power projects in India.

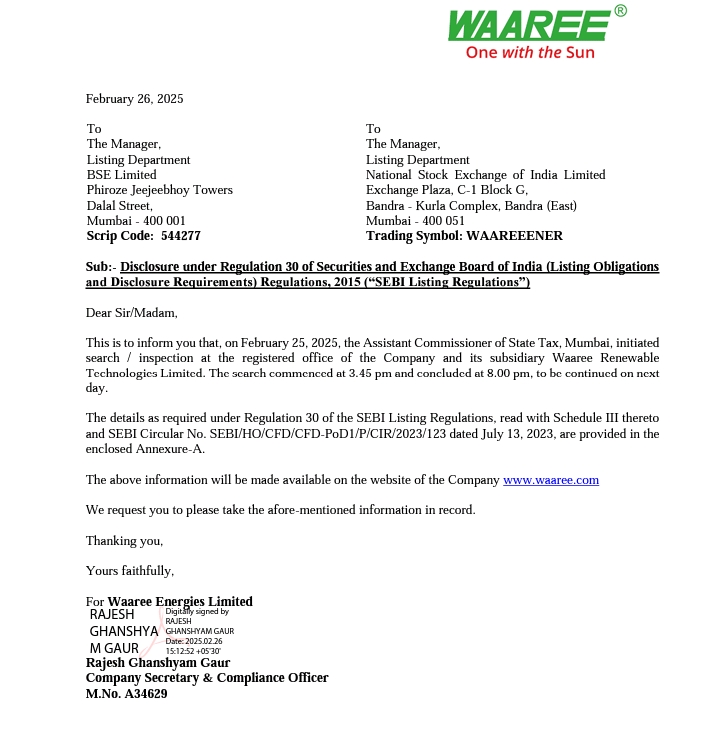

On February 25, 2025, the Assistant Commissioner of State Tax, Mumbai, initiated search / inspection at the registered office of the Company and its subsidiary Waaree Renewable Technologies Limited. The search commenced at 3.45 pm and concluded at 8.00 pm, to be continued on next day.

2 Likes

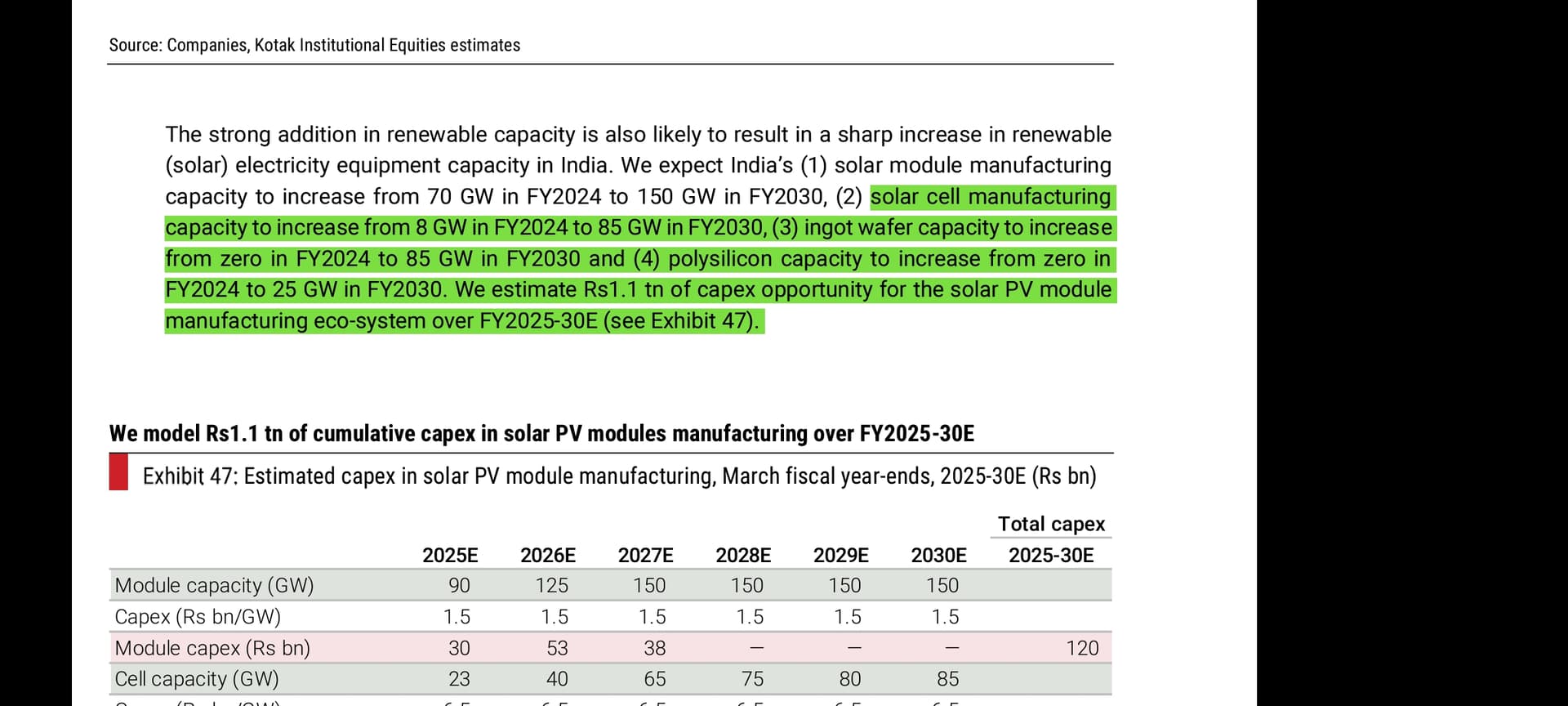

The brokerage projects a 30 percent revenue CAGR and 54 percent EBITDA CAGR for FY24–27, supported by a surge in module, cell, and wafer capacity. Waaree’s margins are expected to peak at 24 percent by FY28, before moderating due to rising competition and lower import tariffs.

The company is expanding into green hydrogen, electrolysers, lithium-ion cells, inverters, and battery energy storage systems (BESS) to diversify operations and sustain long-term growth. Nuvama likens the current phase of India’s renewable energy sector to the early IT boom of the 1990s, suggesting a multi-decadal opportunity.

Source ![]() NUVAMA

NUVAMA ![]()

3 Likes

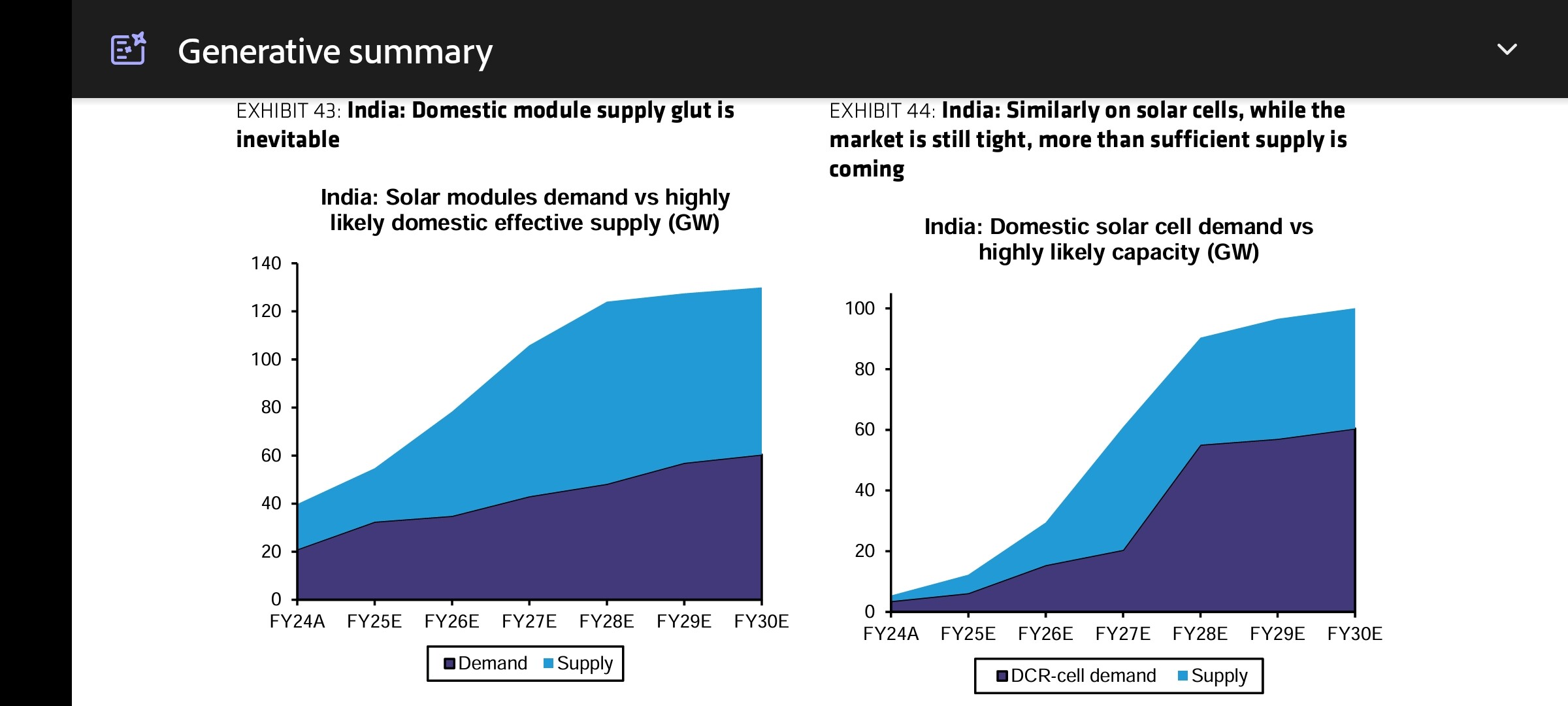

While reading this report they said modules will go into over supply in 2 years time in India. This point is ignored by most

2 Likes

also a rating upgrade by CARE on 19th march https://www.careratings.com/upload/CompanyFiles/PR/202503120353_Waaree_Energies_Limited.pdf

1 Like

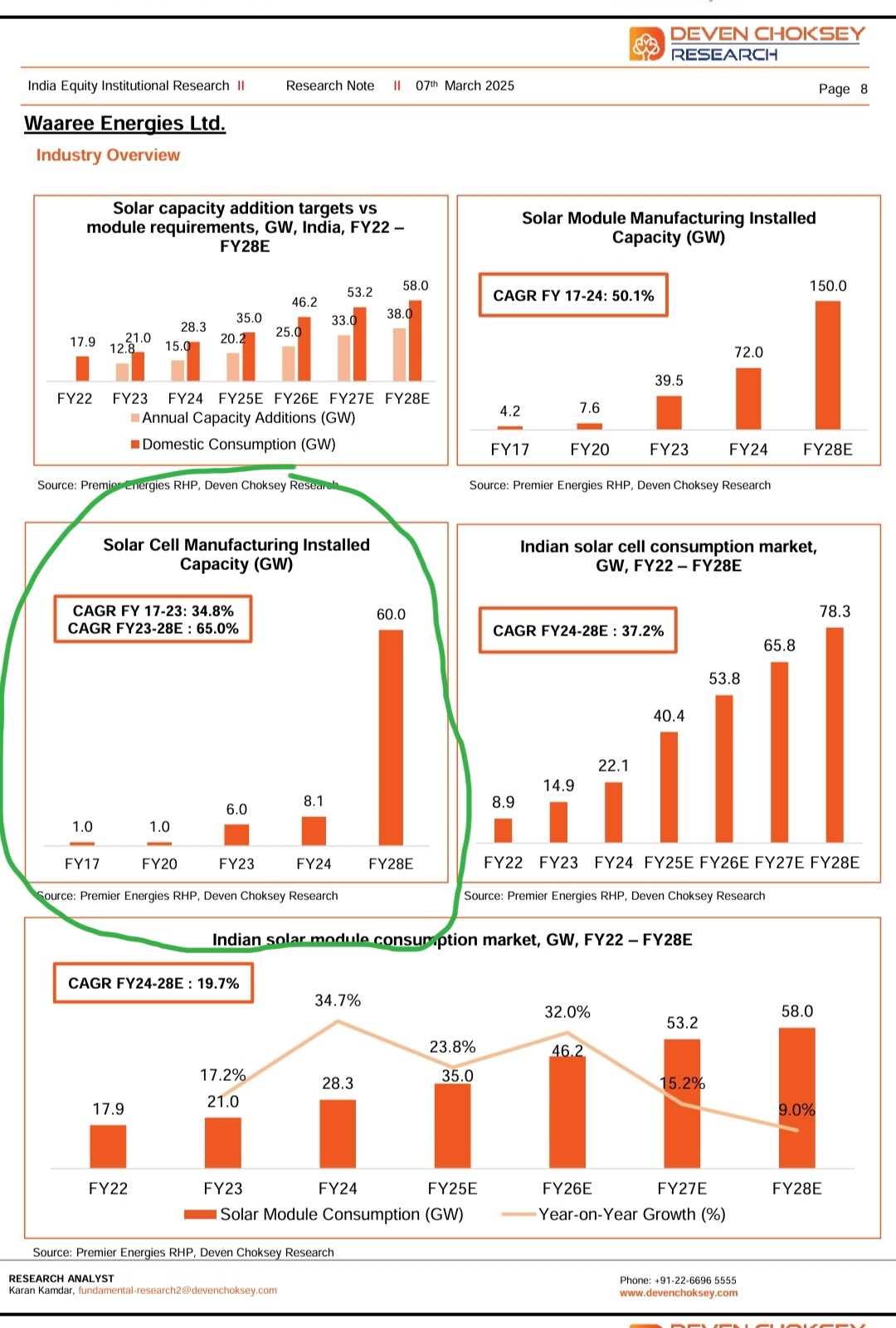

DRChoksey_Note_on_Waaree_Energies_Ltd_Boosting_growth_with_expansion.pdf (513.8 KB)

Great insights ![]()

![]()

1 Like

So even in FY28, domestic demand would outpace planned installed cell capacity by 30%+ and usually all of planned expansion projects would not get commissioned at actual planned date would not get commissioned at the planned time. So if 20% projects see a delay, we will see 50GW cell capacity in India, vs demand at 78 GW. That would be a deficit of 45%.

Disclaimer - not invested in Waaree Energy but in other cell manufacturing companies.

4 Likes

The discussion on solar energy from 51.10 minute in the interview.

3 Likes

This over supply is definitely coming but assume it is creating more pressure on smaller players who are eventually graduating to become tooling / outsourcing agents for players like Waaree.

Surprisingly waaree still is unable to supply sufficiently in domestic market and works primarily on taking advances against most of the orders.

2 Likes

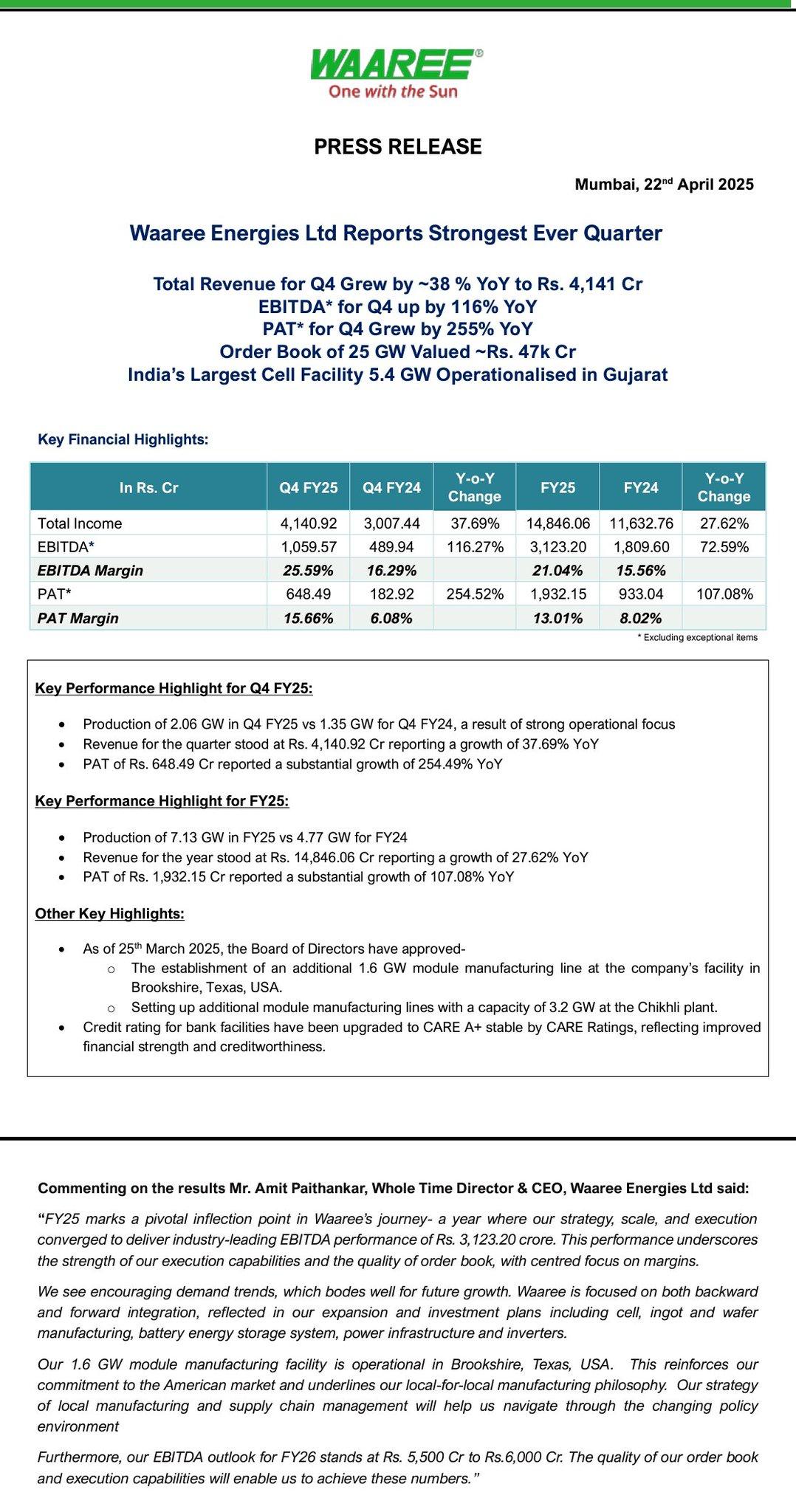

waaree energies posted blockbuster q4 fy25 result

- pat grew by 255% yoy

- total revenue grew by 38% yoy

- ebitda up by 116% yoy

- ebitda margin expanded to 26% from 16%

- gave ebitda guidance of rs 5500-6000 cr for fy26

- order book at 25 gw valued at 47k crores

- india’s largest facility 5.4 gw operational in gujarat

- new 1.6 gw module manufacutring line operational in brookshire, texas

- bank rating upgraded to care a+

disc: invested pre-ipo at the lowest level

2 Likes

A great news article regarding the south east asian tariffs on solar panels in the US,Waaree is going to be beneficiary even though the tariff rates are even 40%,people would still buy and waaree has major exports to US.

3 Likes

Yeah, that’s a big deal. Even with the 40% tariffs, demand in the US is strong enough that buyers will still import and Waaree’s in a great spot to benefit. Their supply chain’s solid, and they already have a foothold in the US market, so this could really boost their export numbers

Uploading the conference call with ppt, no need to listed to the audio & the ppt in 2 different screens now

4 Likes