I would like to boil down the two pictures according to a few “themes”.

Theme 1: The secret sauce of success: Operating Leverage

As @Parul highlighted amply,- operating leverage can attract a virtuous cycle. But what really is Operating Leverage.

Increasing Operating Leverage is really at its heart making your operations leaner. A business that continues to drive operating leverage is essentially not waiting for the proverbial winds to change, but adjusting the sails of its ship.

Driving operating leverage essentially implies, cutting costs, explicitly or implicitly. Explicit cutting cost implies the usual that we understand - reducing superfluous costs. But implicit cost cutting is far more powerful than explicit ones. Implicit “cost cutting” implies driving down costs of production via improvements in the process.

Results abound in the markets where we keep seeing operating leverage get rewarded beneficially.

How it plays out for Axtel: Take a look at the improving fixed asset turnover. The 5-year average was 4.35x and the current one is 7x. For a manufacturing business like this, it plays into the “idea” of Op.Lev very well.

Why?

While the yearly depreciation amount remains the “same”, the sales keeps on increasing - thus improving the profitability of the company.

While the “levers” behind driving operating leverage can be myriad and various, it all can be boiled down to a few essentials - you raise your prices (thus improving margins), or you improve your production workflow (thus improving asset turns), you employ technology (thus automating the process) or de-centralize (de-centralization, that is letting people drive the ops has shown to be extremely beneficial in early recognition of risks and cutting wasteful expenditure).

So how has Axtel been driving its OL?

It has improved its Fixed Asset Turnover, consistently improved its gross margins and most importantly reduced its cash conversion cycle to below 0

Theme 2: Opportunity Size and Structural Sectoral Advantage

Opportunity Size and Structural Advantage are best exploited for an investor when they work in tandem. When that happens, a “flywheel” is created.

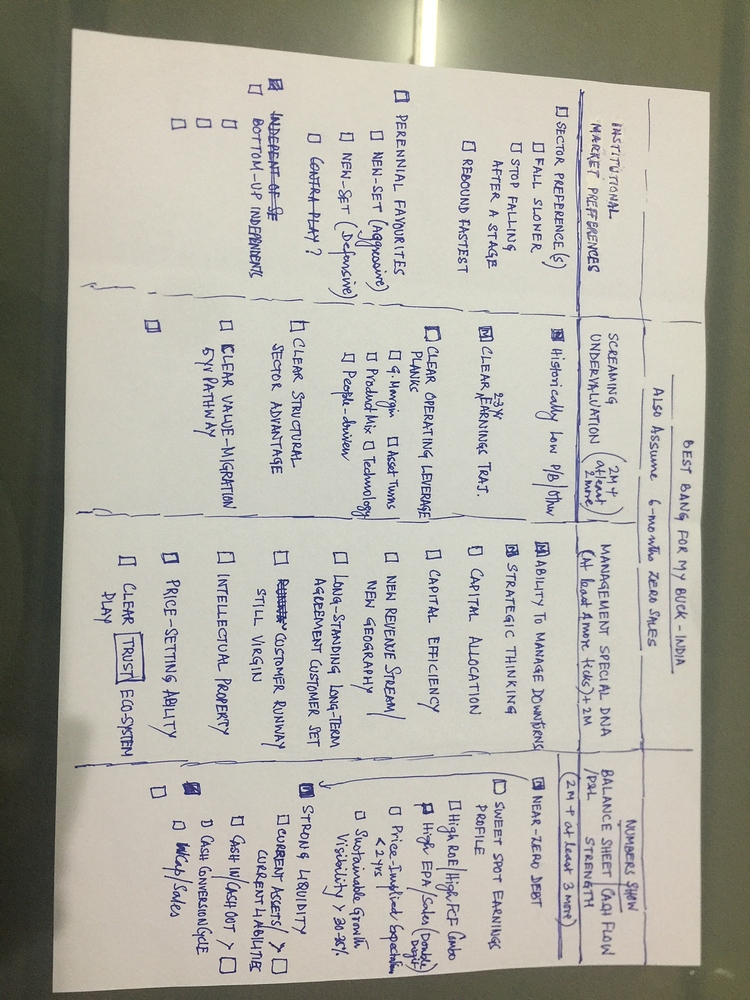

Large opportunity size helps in delivering sustainable growth - highlighted by Donald’s Best Bang for the Buck picture in the “Numbers Show” section (4th column, last subpoint in Sweet Spot Earnings Profile) and Structural Advantage of the business helps in “keeping” the benefits of growth.

What do I mean by “keeping the benefits of growth”?

Think about the difference between the growth of companies like Lava mobile phones, Intex, Micromax and growth of companies like Coke and Pepsi.

While the first set grew at a much scorching pace, they failed to keep customers hooked to their product and thus they had to spend increasingly larger amounts for advertisement (Hugh Jackman ad, remember?) So when the demand slowed down just a bit, they were struck with slowing sales and high degree of amortized expenses.

Whereas coke, pepsi has a much more staid and slower growth rate, but there is a habit forming nature to their products. I have not seen one person switch from Coke to Pepsi (my brother might be an exception, since he drinks anything that has soda in it), and no one switching from these two to RC Cola (yes not even my brother).

Being able to keep the benefits of growth, ensures that we benefit from opportunity size.

Hence having a “structural advantage” ranks very high in the list and precedes a lot of other important aspects of the business.

How it plays out for Axtel

Take a look at its economic profit per unit of sales over the course of its last 10 years.

It has been all over the place 2010-2016 but tentatively moving up in the last 3 years.

EPA margin (EPA/Sales) is a great way to look and think about a company with regards to its structural advantage.

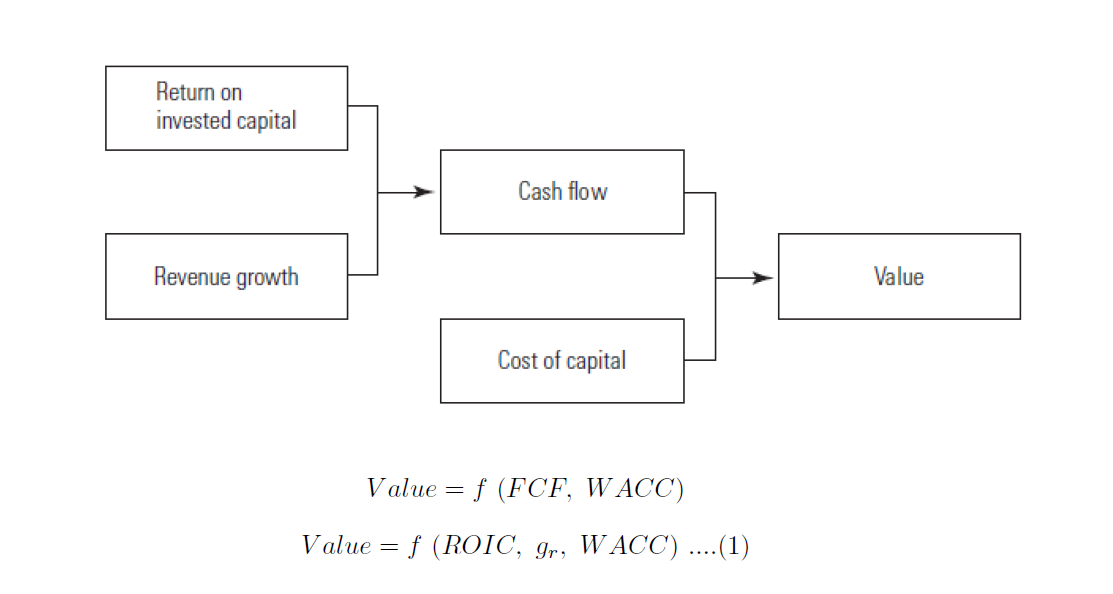

Economic Profit is a very simple concept : It tries to answer, what’s the “profit” earned by the business after its explicity (that you see on P&L statement) and implicit ( that you don’t see) costs are taken care of.

Implicit Costs like Opportunity Cost and Cost of taking a risk like this , are included in Cost of Equity for a Shareholder.

So Accounting Profit (that is reported) differs from Economic Profit as the latter takes care of the implicit cost of equity for a shareholder as well.

Now take a look at EPA/Sales trend of Axtel. Too early to say if Axtel is turning over a new leaf, but its wise to believe something is afoot.

And as for the opportunity size and room for growth is concerned - there is a lot of discretion involved into it usually. I can see, Donald has already calculated a 5 year average sustainable growth for the business. It’s 7.73%.

I don’t know without context of its competitors and without its sector if its high or low.

But as we saw in the example between Intex, Micromax and Coke- growth matters, but can you keep the fruits of the growth matters even more.

“Keeping the Fruits of the Growth” implies is there any economic profit left (ex growth)?

I realize the post has already stretched quite a bit.

But this was 2pence.

@Donald, if this is something that meets your approval, then I can add a few more observation points of mine.