The other Points are NOT worth much debate (for me) - since the terrain has been laid out well before by others. Request everyone at VP to get really focused on 2 things from here on:

A. Have we created the Ammunition? (Else one would NOT be able to sleep well/vital for ENERGETIC response). I would reckon anything less than 30-40% Cash is sub-optimal. If sitting ON Higher Cash that could be due a) Absence of Core/Satellite Portfolio structure b) Need for complete rejig of Portfolio (brought on by excesses of last 2-3 years?) c) Zero Clutter mindset - Ready for Positive Action

B. Do we have CLARITY on what to buy? Choices create CONFUSION - that’s a Life-Fact. Plethora of Delicious Choices can make us really really confused - unless we are in the category of always know what we want to buy - which certainly won’t get us the maximum bang for the buck, but is a good enough response, in current context.

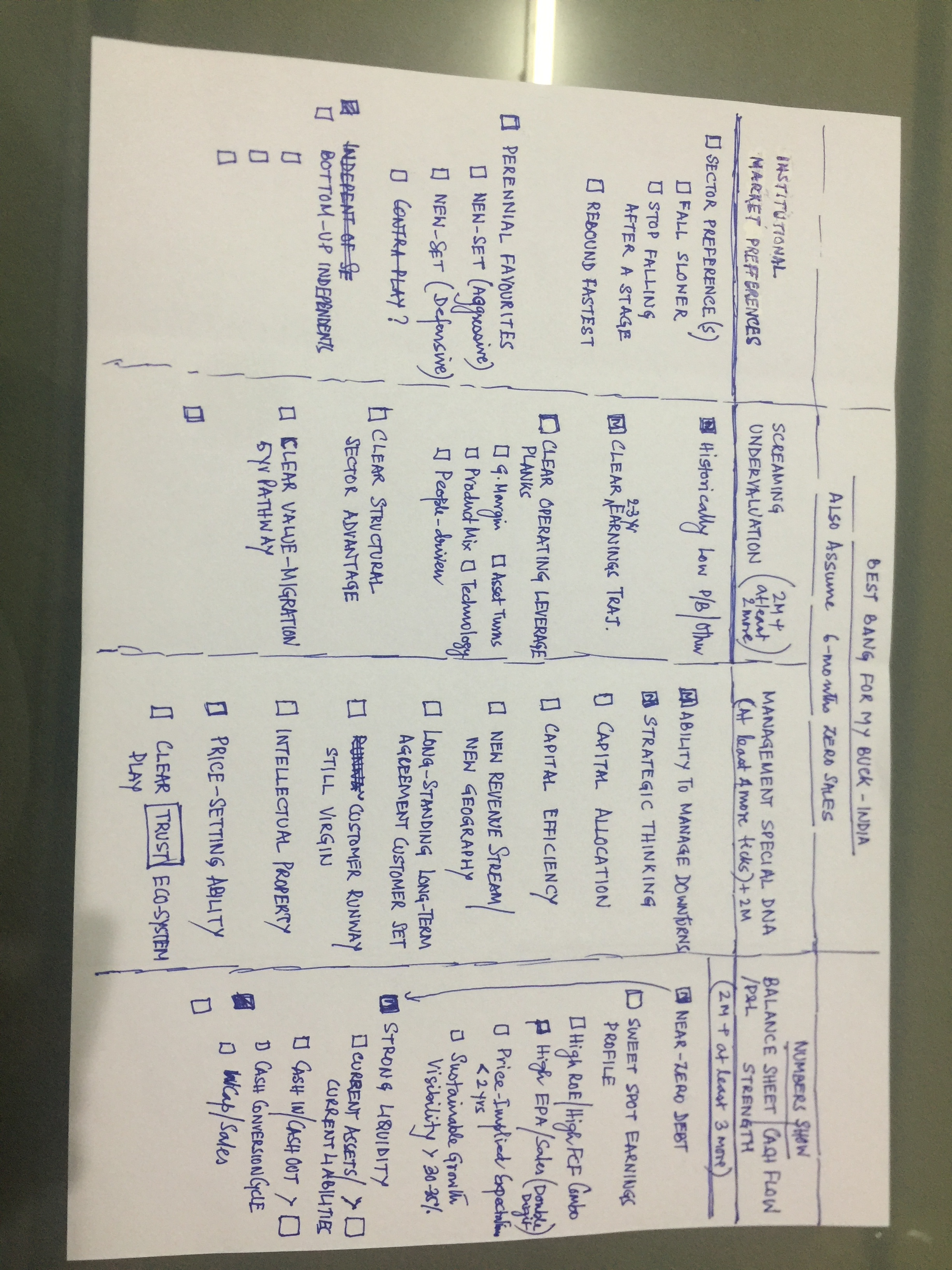

To help us all get fixated on this immediately, I am releasing a just-started-on Opportunity Map (probably not fit for public consumption at this stage) on a hunch that this might just be the ‘something’ that galvanises us into Action Mode on mapping the huge Buy Opportunity …coming soon!

Let’s refine this incrementally. Calling for inputs from Senior VP Members. This is once again just a starting Opportunity Map. Am seeking outside help - especially Mr D & Mr M - to help refine this. Don’t even know if this meets their standards ![]()