I was on the concall. Got a chance to interact with management, and had my questions answered.

Amidst all the good things, there is an elephant in the room that needs addressing.

Starting with the good:

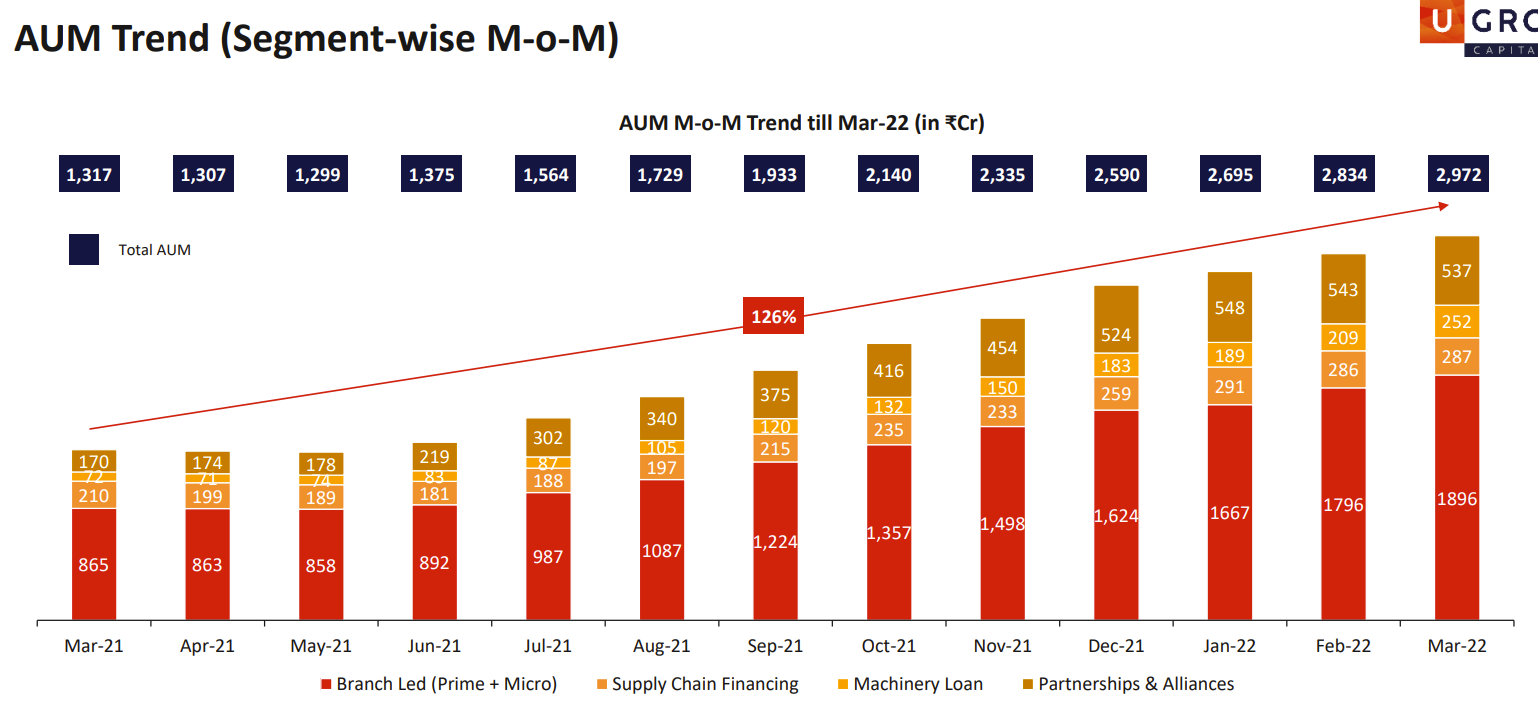

- Disbursals are at 3000 Cr. as of FY22.

- PAT has risen significantly, is up 292% YoY.

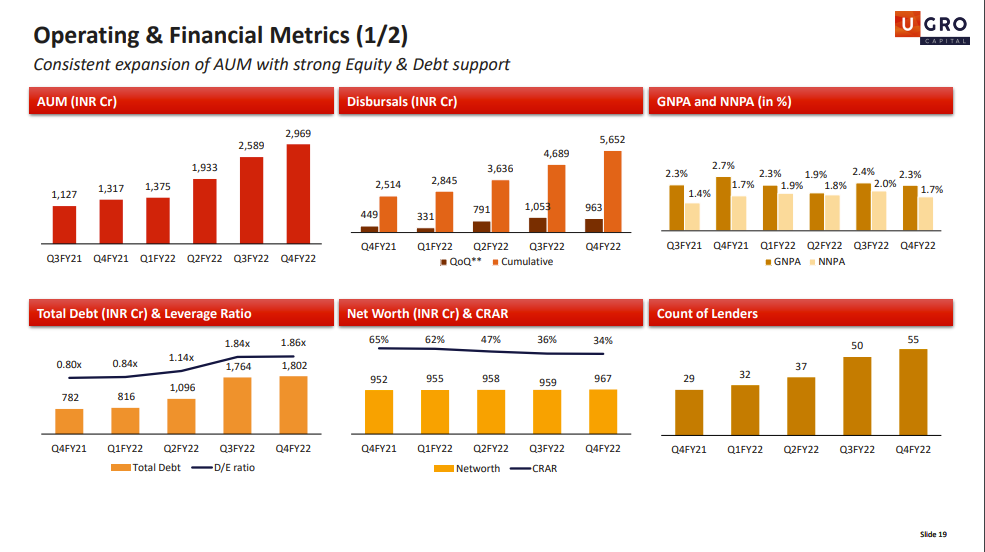

- NPAs are down, from 2.7% GNPA to 2.3% GNPA.

- Branches up to 91 as of FY22.

- New co-lending partnerships, 16 active discussions with 6 private banks, 5 PSUs, 5 NBFCs, 2 SFBs.

- Co-lending is 16% of the book at the end of FY22.

Now, here’s what they see as the year ahead:

While none of this is new, one can read between the lines to make an observation:

-

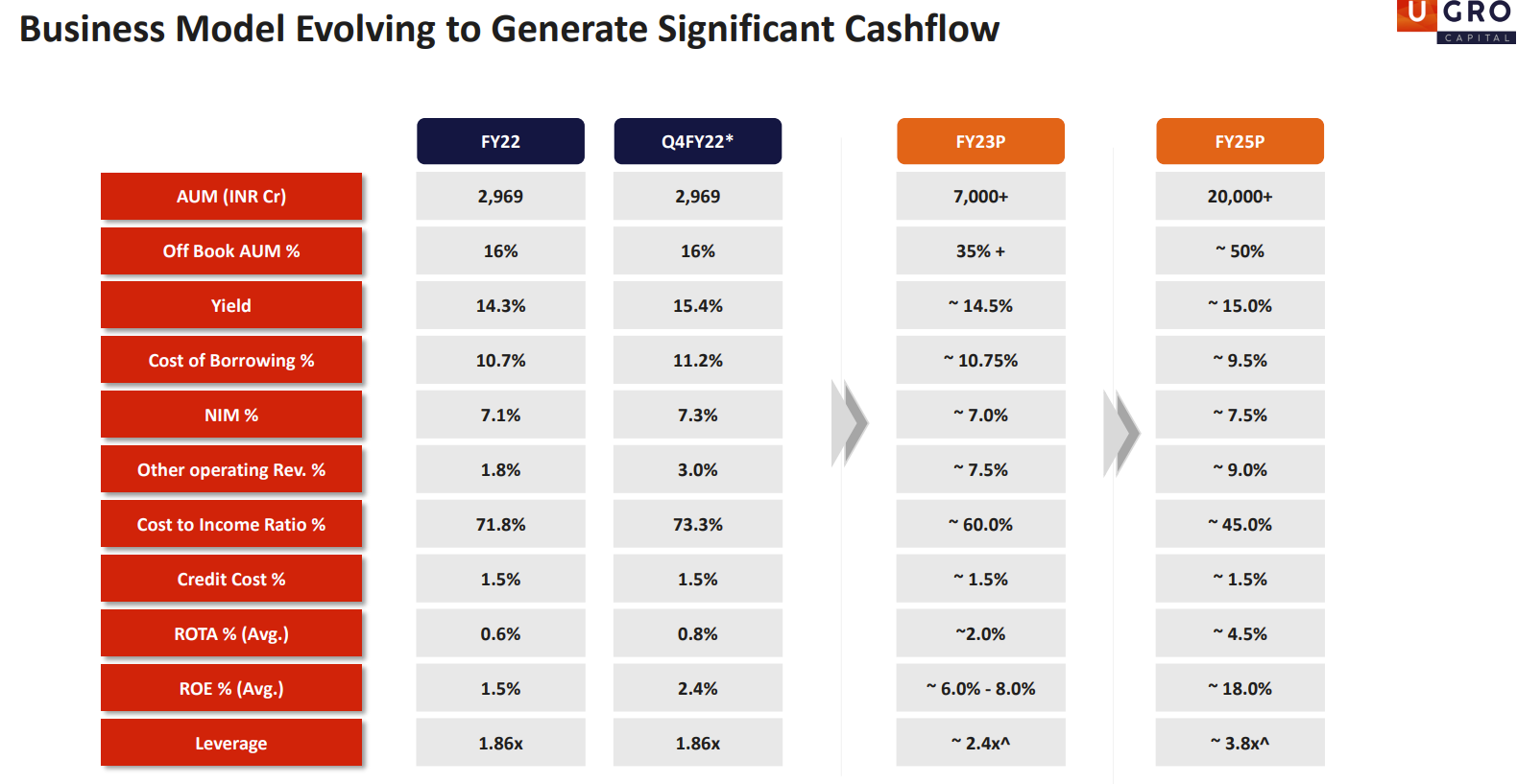

They see OpEx reducing from 73% in Q4FY22 to 60% in FY22. In the concall, Mr. Nath addressed this to say that the existing branch framework (OpEx) is sufficient to meet FY23 disbursal targets. Therefore, they’re stopping branch expansion for a year and allowing PAT to catch up. What this means is that a reduction in OpEx, and a subsequent increase in AUM should drive the PAT up very significantly from the 6 Cr. that we see in Q4.

-

Concall + presentation have a nice new explanation of their ML model. They’ve included a Proof of Concept in the presentation (Usually PoCs are much more detailed and technical. This is just a slide in an investor presentation, and actually explaining PoC would take pages and pages. I was happy with answers to my questions on this).

Elephant in the room

Ugro needs a fundraise to successfully scale AUM past 10,000 Cr. In the board meeting, they’ve obtained permission to do a QIP up to the tune of 500 Cr. (or half their market cap!!!)

Now here’s the elephant. A QIP this large is currently half the market cap. Investors from ADV, Samena, NewQuest would not take kindly to a dilution at this share price. Ugro’s currently trading at book value, and roughly 10 rupees per share higher than they paid for it back in 2018. While the company has scaled successfully so far, these investors have little to show for it in terms of returns.

A QIP at the 52 week high of 220 would at the least be much easier to digest. Management needs to find a way to keep investors happy by doing the QIP at a higher price, but as we’ve seen in the last month, Mr. Market is in no mood to oblige.

If they don’t QIP / raise funds, there’s a limit on how large they can grow with a limit of 3.8x gearing, even with the additional benefit of co-lending allowing them to disburse 4x the amount of loans with the same equity base compared to traditional lending. If the AUM faces a bottleneck, Mr. Market will most definitely not reward shareholders.

In the concall, the reply was encouraging: that they can also raise funds through other means, and the eventual QIP isn’t set in stone as 500 Cr. This is just board permission to raise the amount if needed. I’ll be watching with interest how this plays out. However, it has no real bearing just yet, as they’re still at 34% CRAR.

@Malkd you’d mentioned being on the call, please do add your thoughts.

Disclosure: I’m (very) invested, biased.

I’ve not found much joy in writing updates to this thread due to my position size: found here. I feel hesitant to write, should my posts be coloured by bias.

I’ll be stepping back from this thread from now on.