Thank you nirvana_laha. for breaking down the co-lending math so beautifully. And I do think it is wonderful. Beyond the asset light model, I also think it is a potent method for a small NBFC with a limited amount of credit supply to meet a larger demand for credit.

But my main concern, as Focused_Investor stated so much better than me, is about the cross-selling by the banks, fintechs, other nbfcs who sign up for it with UGRO. While UGRO will be the client facing entity, IIRC, the management had said that the details of the client will be shared with their co-lending partners.

From what I understand, the reason for the high yield from MSME lending is that the uncertainty in their credit worthiness. And say this is priced at 12%. UGRO is sifting through the MSME universe with their tripod model to understand the clients actual creditworthiness. And let’s assume that comes up to 10%. Isn’t this arbitrage what gives UGRO their true edge?

But once a clients’ true creditworthiness has been revealed, the uncertainty is no longer there, making them eligible for loans at a lower rate. As a co-lending partner, I get access to this information for every loan I take up with UGRO.

And if I am a fintech/bank/nbfc who has a lower cost of funds and has co-lended with UGRO for a few years, what is stopping me from creating a database of these clients and their credit behavior over these cycles, and then approaching them directly with loans at a lower rate?

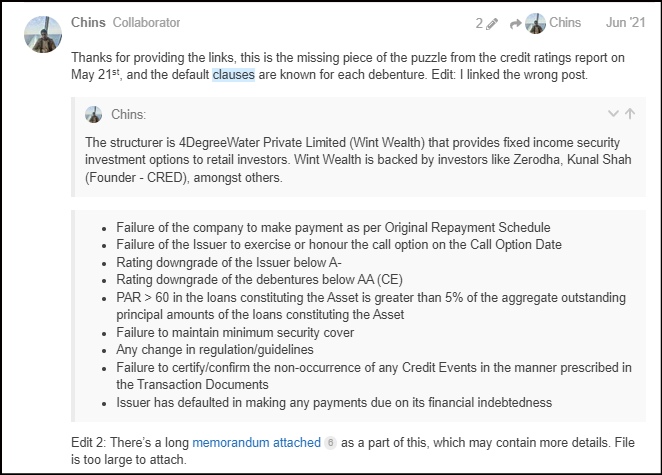

We in our family were holding some debentures of UGRO Capital, where in 33% were redeemed & we did received redemption amount along with monthly interest on 12th August. However in one account the amount was again credited yesterday 15th August. One of my friend also received twice. Looking at major lapse on companies part , i tried to call them on telephone no 022 48918686, which is mentioned on BSE site as well as on companies letter head submitted in recent announcements. However its a invalid no. Even on their website contact no 02241821600 is given but after hold music it gets disconnected. Then we write to company today morning, but till now nothing moves. This is just for information to everyone interested in this company.

Even they are spending outrageous sums on new hiring. Someone I know is into recruiting, he told me that these guys are offering more commissions by themselves to such recruiting firms without they even asking for it.

His comments around the HR team of Ugro was also that these guys are not professionals and does not know how things works in real world.

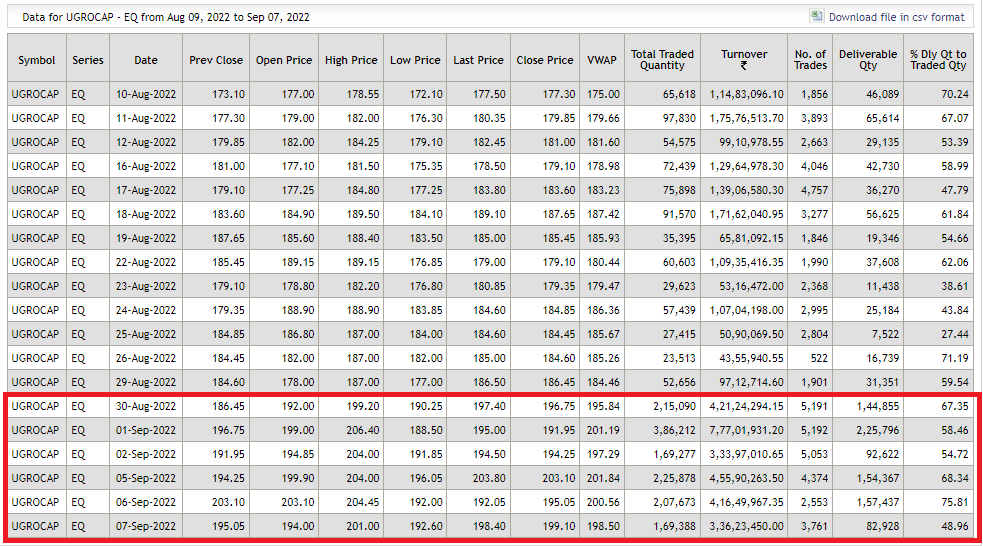

@Chins looks like accumulation is going on in Ugro as ‘Traded and Deliveries’ quantity is very high from 30 Aug. What is your view as volume of last 5-6 days are more than 4-5 times from normal days volume

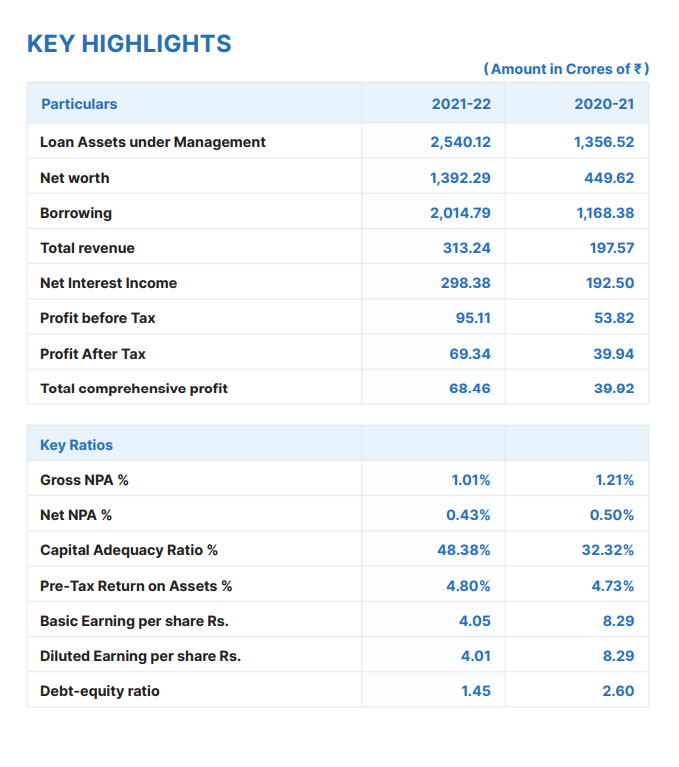

I have been looking into some other companies that function in the same space - MSME lending. Here’s a screenshot from an Avendus report from May this year.

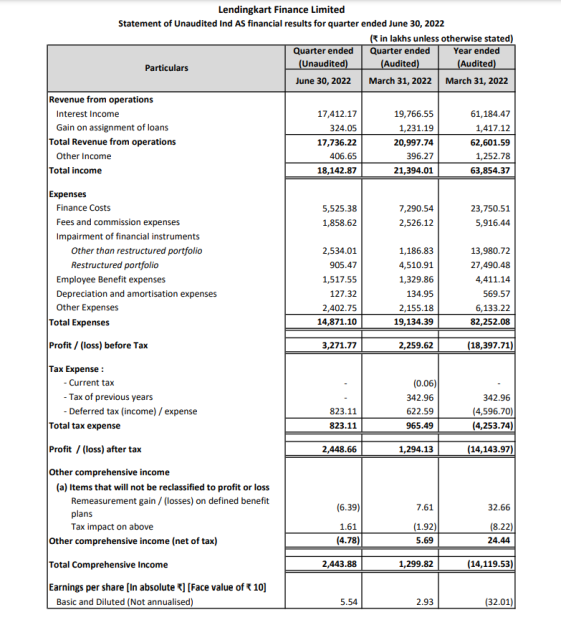

While the figures from the screenshot are dated now (we are above 4300cr AUM), think it will be worthwhile to track these and see how we compare. Oxyzo and Lendingkart are unicorns that plan on listing in 12-18 months. Lendingkart also happens to be one of Ugro’s digital lending partners. And Ugro are one of Oxyzo’s debt partners.

While there are fundamental differences in the businesses - proportion of on-book: off-book, secured:unsecured, physical presence (number of branches + opex that goes along with it), etc - I think the listing of these businesses will definitely throw further spotlight on Ugro (if the market hasn’t caught up already) and could prove to be a rerating trigger. Inviting thoughts and analyses.

But for this to happen, we definitely need management to walk the talk and focus on profitability. No better time to plug this epic meme from @Chins (follow him on Twitter for more such gold).

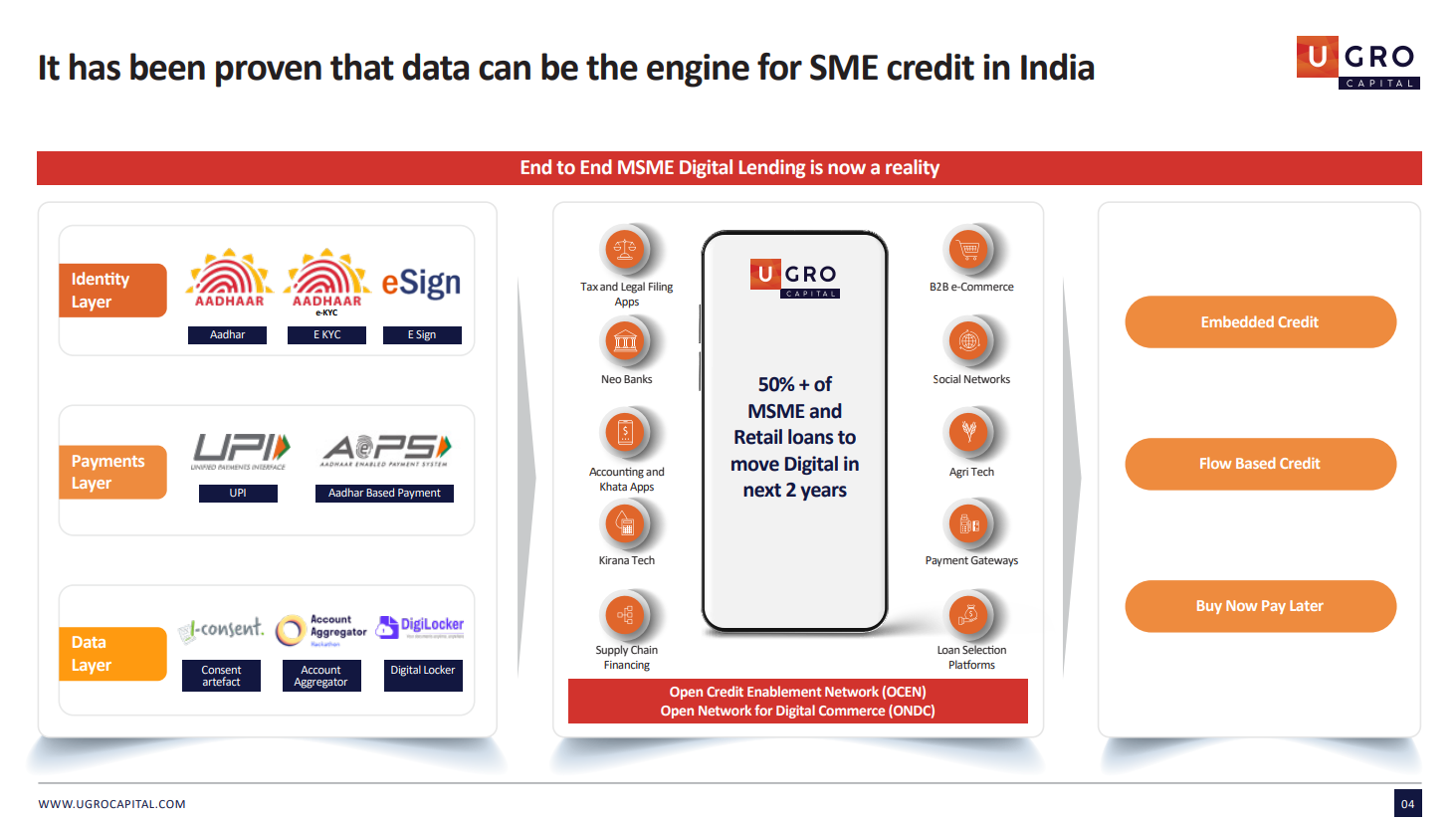

Like PSBs going live on AA earlier, these are all small steps towards the digitization of finance that will help enable access to credit. Ugro has been one of the pioneers in forseeing this and positioning themselves accordingly, evidenced by the fact that they were the first lender onboard GeM Sahay. Attaching a slide from their recent investor presentation.

If we don’t consider one off tax, Ugro has reported highest ever profit So next quarter results gonna All time great if asset quality remains stable…

ROE gonna expand from hereon with less dilution to equity as co lending gonna 30% plus…

Management has delivered upto now on all guidance, so even if they achieve 75% of future guidance, it’s book value can increase 3x in next three years…

Mr. Nath has talked about how their TAT times are fast and how that’s great for their customers but does anyone know what KPIs they (if at all) have to actually measure how satisfied they are with UGRO, with the app? What is the percentage of their repeat customers?

Is the process easier after you have a credit history with UGRO? Lesser meetings? Even faster TAT? Especially once a collateral has been vetted once?

Also since UGRO is able to see credit histories of their customers, do they follow up if they see that a former customer of theirs has chosen to go with someone else for loan to understand why?

The space is getting competitive so won’t customer experience be key for UGRO’s success? Esp if they want to hang onto their quality customers?

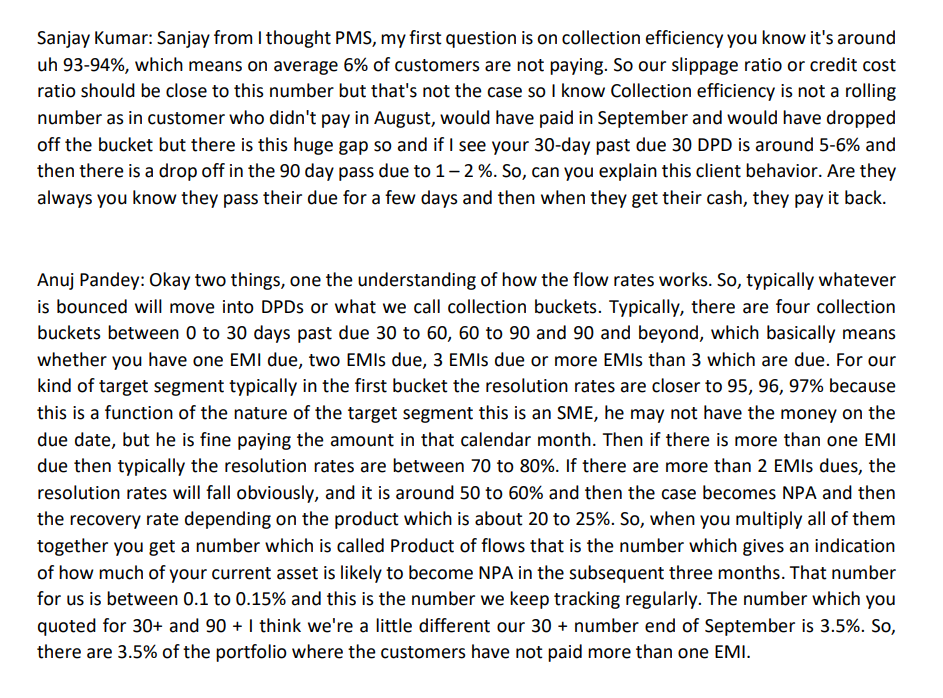

Below is the extract fom conference call regarding collection efficiency which some boarder asked earlier:

Wane D’Mello: Okay, thank you. And one last question is just for the sake of investors like how do you

guys define collection efficiency so we are at 94%. So, you know what comprises the rest of the 6%?

Anuj Pandey: So, we define connection efficiency by current collection divided by current demand.

Typically, in other Financial Services Industry a lot of people give collection efficiency by dividing the total

collection by current due, if we do that, our connection efficiency would be closer to 99%. So, this rest 6%

is what flows into what we call buckets. The first bucket is called bucket X, typically in that bucket X our

resolution rates are around 97-98%.

Firstly, I want to thank the Vpers for building a formidable thread full of varied opinions. I have read it from top to bottom and also gone over the recent annual reports. I think I am clear on the Colending model and the hunger in the SME sector for loans.

I have some exposure to SQ, SOFI and UPST. I use AI/ML in my job and also teach it regularly. here are some of my comments/questions to the learned folks and would love to hear back.

Basically this is sub prime lending. so is UPST, sub prime lending is prone to fat tail black Swan risks. In the case of UGRO, one can envision scenarios, recessionary scenarios which may precipitate a large set of simultaneous defaults across multiple seemingly unrelated sectors. AI ML models and pretty much any academic data analysis will be blind to fat tail events. UGRO says their model has passed two covid waves, which is some reassurance, but that is not yet the spectrum of all market cycles. UPST ticker is down considerably. Basically, in the current high interest env, banks are choosing not to Co-lend with UPST.

THIS TAIL RISK WILL NEVER GO AWAY WITH UGRO. The bigger the AUM, more scary will the the fat tail blow ups.

Scalability - at low AUM base, company can be very choosy and maintain asset quality. However as AUM grows, company will be very tempted to relax lending criteria which may lead to higher NPA. Only time will tell if they can build up AUM while preserving asset quality. The underlying requirement is that there are enough good quality SMEs out there that have to be tapped. Again, only time will tell.

COMPETITION. The kind of data driven models UGRO AR talks about doesn’t seem too hard to replicate by other NBFCs or banks or similar startups. Is the TAM large enuf for multiple players? Cross selling or cannibalism by Colending partners was also brought up, but only be an issue down the line.

CG risk etc. Learned posters brought up religare issues. While PE punters also goof up big time (softbank, anyone?) they will definitely vhet known risks. I think this monster in the closet may be the least scary of all.

On the positive side, if this happens to be the decade of the blossoming of the Indian SMEs and if UGRO scoring system is truly working, a multibagger s enario will result. As the tail wind is decadal, a staggered investment with possible occasional downsizing steps thrown in may be the way to go.

DISCLOSURE - Studying, not taken a stand/position yet.

I am a bit of a dunce,rants are not recommendations! Do your own DD

Hi I have one question regarding Ugro.

They are growing the loan book very fast.the npa ratio is constant with highly growing loan book.that means absolute npa is increasing at a fast pace. so if loan growth slows down will the npa generation slow down? The only thing bothers me about ugro is that the loan book is unseasoned and can the npa profile be as it is today? I think that’s what market also concerns about. Haven’t studied the business in details just saw few quarterly presentations.

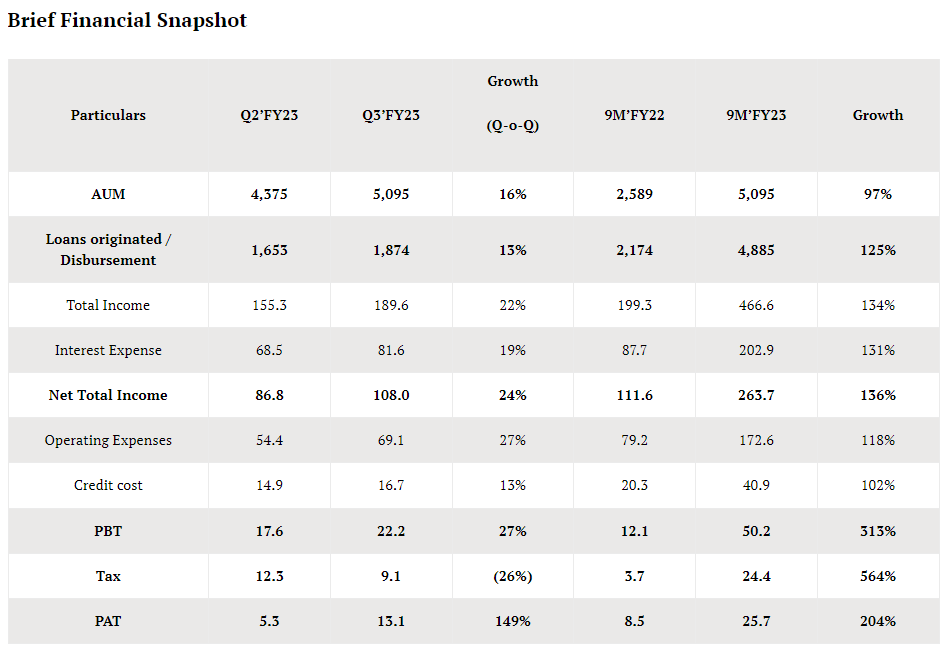

INR 4,886 Cr of Gross Loans originated in 9M’FY23 (up 125% compared to 9M’FY22) and INR 1,874 Cr of Gross Loans originated in Q3’FY23 (up 78% YoY and 13% QoQ).

Total Income stood at INR 189.6 Cr for Q3’FY23 (up 123% YoY and 22% QoQ) and INR 466.6 Cr for 9M’FY23 (up 134% compared to 9M’FY22)

Net Total Income stood at INR 108.0 Cr for Q3’FY23 (up 131% YoY and 24% QoQ) and INR 263.7 Cr for 9M’FY23 (up 136% compared 9M’FY22)

PBT increased to INR 22.2 Cr in Q3’FY23 (up 338% YoY and 27% QoQ) and INR 50.2 Cr in 9M’FY23 (up 313% compared to 9M’FY22)

GNPA / NNPA as on Dec’22 stood at 1.7% /1.1% (as a % of Total AUM)

Over 38,000 customers as on December 2022

98 branches (as on Dec’22)

b)Liability and Liquidity Position

Total lender count stood at 67 as on December 2022

Total Debt stood at INR 2,885 Cr as on December 2022, and overall debt to equity ratio was 3x

Healthy capital position with CRAR of 21.54% (as on December 2022)

Is the high debt a cause for concern OR is this expected for a novel company like UGRO who is growing very fast?

Is the high debt a cause for concern OR is this expected for a novel company like UGRO who is growing very fast?

Debt isn’t high for Ugro. For banks and NBFCs, 2.85x D/E is not high leverage. Don’t evaluate banking or NBFC companies from the POV of manufacturing or other sectoral companies.

Description of the Security Commercial Paper

Listed/Unlisted Listed

Allotment Date 19-04-2023

Redemption Date 28-03-2024

Tenure of the security 344 Days

Face Value per Security (Rs.) 5,00,000/-

Issue Price per Security (Rs.) 4,59,906.50

Issue value (Rs.) 9,19,81,300/-

ISIN INE583D14220

Redemption value (Rs.) 10,00,00,000/-

Name of IPA Yes Bank Limited, Mumbai

Issued in favour of The Greater Bombay Co-Operative Bank Limited

Thanks everyone who has shared their inputs so far, it has been very informative.

Came across this new item related to RBI keenly watching Co-lending practices, especially of organizations without an established track record. It doesn’t cast any apprehensions on Ugro directly, but something for us to keep in mind.

Raised 340 Cr. of equity. New investors are onboard for a tenure of 5-8 years.

Launched a much awaited product where they provide working capital loans for very short tenures, often charging interest for as little as a few days.

There was a lot of drama following the switch from Acuite to Crisil. Acuite promptly downgraded Ugro’s rating, leading to a clause breach in one of their MLDs. Incidentally, VP had discussed these clauses during the early days of the thread, two years ago:

They have scaled their off-book AUM from 475 Cr. at the end of FY22 to 2400 Cr. at the end of FY23.

There is currently an overhang in the stock, where DBZ Cyprus (one of the large investors) have been constantly selling. Shareholding has gone down from 20% last year to now below 1% in my estimate.

Q4FY23 results should see around 30 Cr. of PBT, but we expect a tax issue of around 7 Cr. (from the same issue in Q2) relating to old deferred tax. FY24 should be completely free of any abnormal tax, and they’re expecting around 200-220 Cr. of PBT in FY24.