Some thoughts through the last month of volatility.

-

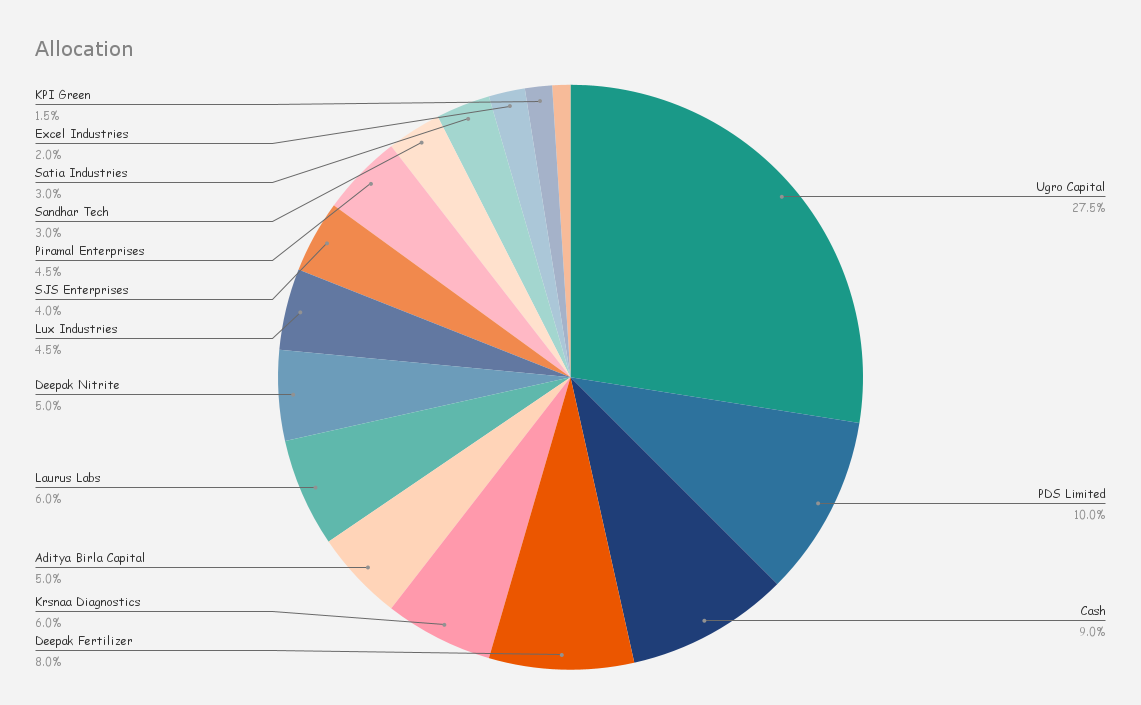

Post market volatility, other companies in my watchlist have corrected significantly and offer equally good risk/reward. I have brought weight in AB Capital back down again to neutral. I couldn’t have timed the correction happening (or the piece by the Morning Context), and the company has delivered an excellent FY22.

-

The correction has of course been painful in some names, and I have thought about whether I’ve made a mistake constructing a small/midcap heavy portfolio. However, I think I’d lose more sleep if I owned fewer shares of Ugro or PDS, than I’d lose in fear of a drawdown. I remain stock specific in my approach, and if all the hard work results in a portfolio that delivers strong earnings over my investment horizon, that’s all I have in my control.

With the exception of Laurus, I don’t think any of the companies in my portfolio are expensive, or have a lot of growth priced in. -

I have initiated a position in Satia Industries at a share price of 115. The thesis has been covered very well in @Rafi_Syed’s excellent thread as well as by @kalpesh4430 I realised that the Satia thesis shares a lot of similarities with that of Filatex, but is the better investment overall.

Both have large capex plans but Satia’s has come onstream already. Both have a pipeline with a high margin optionality, and Satia doesn’t have an overhang with the IT department, nor a history of issuing warrants. -

I’ve deployed around 6% in cash, will be deploying 1-2% every week going forward.

- I have invested in a farm. An intelligent young investor introduced me to KPI Green, and I’ve been encouraging said person to write a company thread here on the forum.

Being deliberately sparse with details, farm operates out of an 850 acre plot of land in Gujarat, and produces solar power here. They have two business segments, where they either produce power on site, and sell it over the grid, or they develop, operate and maintain captive power plants for companies like UPL, Larsen, Cadila, over long term contracts.

Thesis is of a high growth company (that has used debt to build capabilities), with 50% EBITDA margins, and slowly improving PAT margins over a longer term as the debt profile reduces. While the share price has run up significantly, valuations are quite reasonable. I have taken an initial postition, and will slowly scale as I understand the longevity of the business model.

I’m happy to invite comments and discuss further, but I encourage those reading to look over the company for themselves: KPI Green Energy Ltd financial results and price chart - Screener

Next week, I will write an overview of how all companies in my portfolio performed during Q4.