The takeaway from this article gives us another KPI for Ugro:

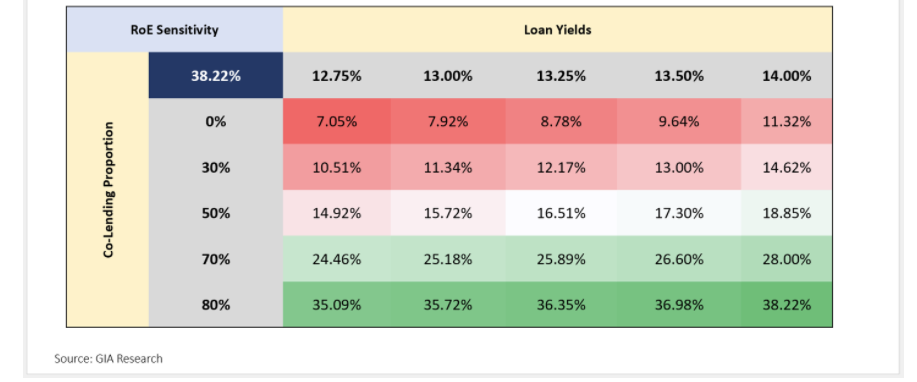

For their targets of 18.8% RoE, at the current loan yield of 15.7%, they need ~30% of their AUM to come from co-lending. (Depending on assumptions made about leverage and loan yields) Let’s ask how their loan book has evolved in the last 15 months.

| Date | AUM(Cr.) | Co-Lending % |

|---|---|---|

| 30/09/2020 | 979 | 14.40% |

| 31/10/2020 | 1024 | 13.18% |

| 30/11/2020 | 1072 | 12.13% |

| 31/12/2020 | 1128 | 12.23% |

| 31/01/2021 | 1171 | 11.78% |

| 28/02/2021 | 1231 | 12.43% |

| 31/03/2021 | 1317 | 12.91% |

| 30/04/2021 | 1307 | 13.31% |

| 31/05/2021 | 1299 | 13.70% |

| 30/06/2021 | 1375 | 15.93% |

| 31/07/2021 | 1564 | 19.31% |

| 31/08/2021 | 1729 | 19.66% |

| 30/09/2021 | 1932 | 19.31% |

| 31/10/2021 | 2140 | 19.44% |

| 30/11/2021 | 2335 | 19.44% |

| 31/12/2021 | 2590 | 20.23% |

-

Mr. Nath tells us that 50% of the disbursements in FY23 are expected to be through co-lending. This needs to play out for the thesis to remain intact. The bear case is them falling short of the target AUM, falling short of the 30% mark, and needing higher % of book to be under co-lending should the loan yields drop to sub 15%.

-

My assumption is 100% of the partnership channel is co-lending from banks. In reality, it’s blended with their co-lending partnerships with fintechs like Kinara. Therefore, depending on how much % the banks actually take up (my guess is >80%), the % of book under co-lending correspondingly needs to be higher.

D: Invested.