MoM was flat. A bit surprising there

AT 11.3% Compounded Half yearly

Why Co- Lending can do wonders for small NBFCs like Ugro capital?

Answers lies in lending interest rates calculation:

Suppose Ugro capital is having cost of capital of 11% and to earn 4% NIM they have to lend at 15% and above for higher NIM. Now customers who borrows at 15% and higher rate are obviously of Not excellent credit profile in general and there is always risk of NPA for Ugro capital

Now suppose if Ugro is Co-lending with say SBI at 50-50 lending ratio, so SBI is having cost of capital say 5 to 6% and decides to lend at 10% considering same NIM of 4 to 5%. in this case lending interest rate would be 12.5% which is average of Ugro and SBI lending rate.

That means Ugro can lend to quality customers at 12.5% having very good credit profile and low risk of NPA with 4% NIM even though its cost of capital is 11%. Isn’t it the boon for Ugro?

Here is the article where Ugro MD is saying that they are able to lend even at even 8.5% due to co-lending and their 50% books would be from co- lending and books will be around 9000 cr at 2023 end. This is a massive growth with quality.

Now, for such massive growth, Raising funds at low cost is not possible for small NBFCs because of which they are raising funds at around 11 to 11.5%. It seems logical as they can maintain good NIM even at this cost of capital.

Remaining 50% book quality need to be tracked closely if they are able to maintain NPA below 2-3%, massive growth with re rating can be seen

Please correct me if i am wrong but,

i do not think that is how the co lending works. interest rate depends upon the riskiness of the customers. co-lending does not bring down the overall risk. So i did not understand what you mean when you say interest rate would be 12.5% and how UGRO will get to lend to good customers.

In co-lending typically 20% of exposure is assumed by NBFC and rest by Banks. The reason banks would get into this is because ‘potentially’ NBFC has superior underwriting standards and collection efficiency than the Bank. Now, low cost of funds of the banks should not make major difference to the interest rate charged because of high risk. A very simplified example - 5% cost of fund + 5% NIM + 10% default risk → 20% yield.

Typically, NPAs are much higher in MSME - upwards of 10%. Similarly yield is also very high - upwards of 20%.

I did not fully understand the following,

U-Gro lends anywhere between Rs 1 lakh to Rs 3 crore at rates that range between 8.5% and 18% basis the risk profile of customer. At, 8.5% the lender is able to lend because it has partnered with Bank of Baroda for co-lending. If it were to lend on its own books, the cost of capital would be 10.5%. “We are still being able to lend to customer below our cost of capital because there is a partner attached to that,” Nath said.

Even for BOB to lend at 8.5%, the borrower should be a large corporate, not MSME. And in such instances UGRO should only earn fees income because they cant finance below their own cost of capital.

Why don’t you write to their IR/ or to the company directly? They will respond as Ugro is active there since they are creating awareness in the public markets on their business model (they need a fund raise in a yr or 2  )

)

I am sharing what I know/ understand - Ugro earns a fee on the 80% contribution of the banks. Plus on a wtd avg basis (80% of bank’s lending rate + 20% on Ugro’s) interest rate to the borrower becomes much lower. The 8.5% example would be for exceptional cases and would be be top notch customers (very good rating). Their median lending rate might be more towards 14/15%plus atleast in my view ( haven’t checked this). The fee on the 20% helps in getting some NIM for Ugro

Sign in to your accountlayouts/15/onedrive.aspx?id=%2Fpersonal%2Ffibac_ficci_com%2FDocuments%2FFIBAC%202021%20Video%2F3.%20FIBAC%202021%20-%20SME%20Finance-%20Can%20co-lending%20unlock%20SME%20finance%20%20How%20can%20co-lending%20be%20a%20mainstream%20channel%20for%20credit_.mp4&parent=%2Fpersonal%2Ffibac_ficci_com%2FDocuments%2FFIBAC%202021%20Video&s=09

Great discussion on co-lending model and future prospects:

Ugro MD is saying that next year, their disbursement would be around 3500 to 4000 cr through co lending only. So total AUM could be around 5000 to 6000 cr in all. Apart from that as the partnership matures, Acceleration could be much faster going forward. So one can Assume, what could be the growth rate in this space in next 3 to 5 years.

Only point to track is Asset quality. If they are able to manage NPA well, sky is the limit for the company.

I think we need to look at Ugro much more than a mere NBFC. going by the initial strategy, it has positioned itself as a Tech platform for remote due diligence.

Look deeper and u realize that the Ambition is much deeper ! For e.g. It tied up with WINT WEALTH, a start-up on consumer debt to raise retail debt at about 8-9%…so eventually, a combination of a Retail debt platform (A la Wint wealth) and a platform to lend(Ugro) could completely sidestep the banks!!

Disruption !!

Sorry, but this is the wrong interpretation of Ugro’s goals.

If you listen to management speak, investing in Ugro is a bet on co-lending being adopted in India. They’re not looking to side step banks, but argue that it’s far easier for NBFCs to achieve their NIMs through a co-lending model, than it is to play the balancing game between lending rates and cost of funds.

Is a wonderful panel discussion on co-lending between a public sector bank, private sector bank, and an NBFC looking to adopt it. While everyone acknowledges that co lending is a win win for banks, NBFCs, and the customer, Mr. Nath also outlines the challenges to co-lending being adopted, namely the differences between NBFC norms and PSU norms. For Ugro to scale successfully, they need to sell to people like Mr. Rajkiran Rai, and agree on a product.

Mr. Nath is confident that co-lending uptake will be higher in 2022 and 2023. They’ve already onboarded SBI, and I think the key to this thesis is monitoring how the relationship with SBI pans out, after the 500 Cr. of disbursals are completed. Will there be a renewal for a longer duration than 4 months? Will they provide more funds? We will also get more clarity on the blended lending rates, and how they came to an agreement on policy. (Hopefully on Feb 9th’s concall)

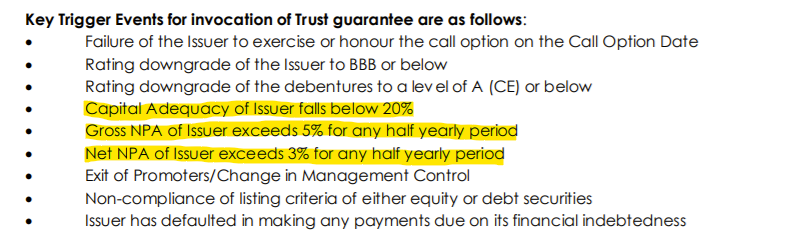

On this point, while NPAs are obviously important to investors, Ugro has several internal checks that should keep NPAs in line. For example, a vast number of their NCDs have an automatic break clause should the net/gross NPA exceed a certain %.

(Ratings report, September 2021)

–

Invested, transactions in the last 30 days

Fair point. However, you need to take a long look at their tie-up with WintWealth. I have invested through one such offering and the experience was educative, to say the least ! Clearly, the path ahead is much more than co-lending with Banks. It’s a bit like DtoC on both sides! People who lend money and one’s who consume…

I liked your unbiased and balanced way of looking at business you hold. I have not delved deeply into either Ugro or any other NBFC since a long long time (I think ever since ILFS crisis)…but I do agree with you that coexistence is the way forward…and certainly Banks are here to stay…otherwise why would a strong going capital first under VV transform to an IDFC first? Although if you ask old shareholders of capital first…they must have had a joy ride under the pureplay digital focused NBFC but the far sighted promoter saw sustainability in being a Bank…

Can you pls let us know how would Revenue & Profits sharing happen in colending and how would the risks of NPAs divided between the interested parties?

Also, distribution of responsibilities …are they standard or would vary from product to product and people/institutions involved? Any insight into how are they divided currently in case of Ugro?

Disc: Neither invested nor tracking any NBFC. However a wise man in the forum @nav_1996 had suggested me never to write off anything and hence I am unlearning the psyche of not looking back at sectors/companies I had shielded myself from. It helped me already in another sector/stock. Was attracted by colending and unbiased response of @Chins , hence may begin to track. Thanks

Thanks for the kind words ![]()

As a lot of your questions are those of fact, please refer to the following resources:

https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11376&Mode=0

Is the RBI circular that started the co-lending framework. The annexure contains information on revenue / profit sharing and examples of weighted averages of interest charged. There’s a more recent circular from 2020 that included housing finance, here’s SBI’s co-lending policy:

This is a nice talk Ugro’s management has given on co-lending, which explains a lot of what’s happening.

As a bonus, here’s a column written by Mr. Nath on the ILFS crisis, and an excellent read on Ugro shared higher up in this topic:

After understanding the basics of how co-lending works, one notices that almost every bank / NBFC has started to talk about co-lending in their exchange filings. Whether this is coincidence, or a sign of what’s to come is an investor’s call to make.

Axis:

Bank of India

Bank of Maharashtra:

Canara Bank:

CBI:

HDFC:

Chola:

Kotak Mahindra:

M&MFin:

SBI:

To my knowledge, the well known NBFCs are talking about implementing a model for co-lending and are working towards this. In contrast, this is Ugro’s singular focus, their platform and hiring has been focused towards building a working co-lending model.

If one were to read only one section of last quarter’s excellent concall, it would be this:

There’s a whole lot more to say, but this is honestly an execution game now.

Edit: The other side of the coin for co-lending:

https://indianexpress.com/article/explained/explained-co-lending-rbi-criticism-7670354/

Invested, transactions in the last 30 days.

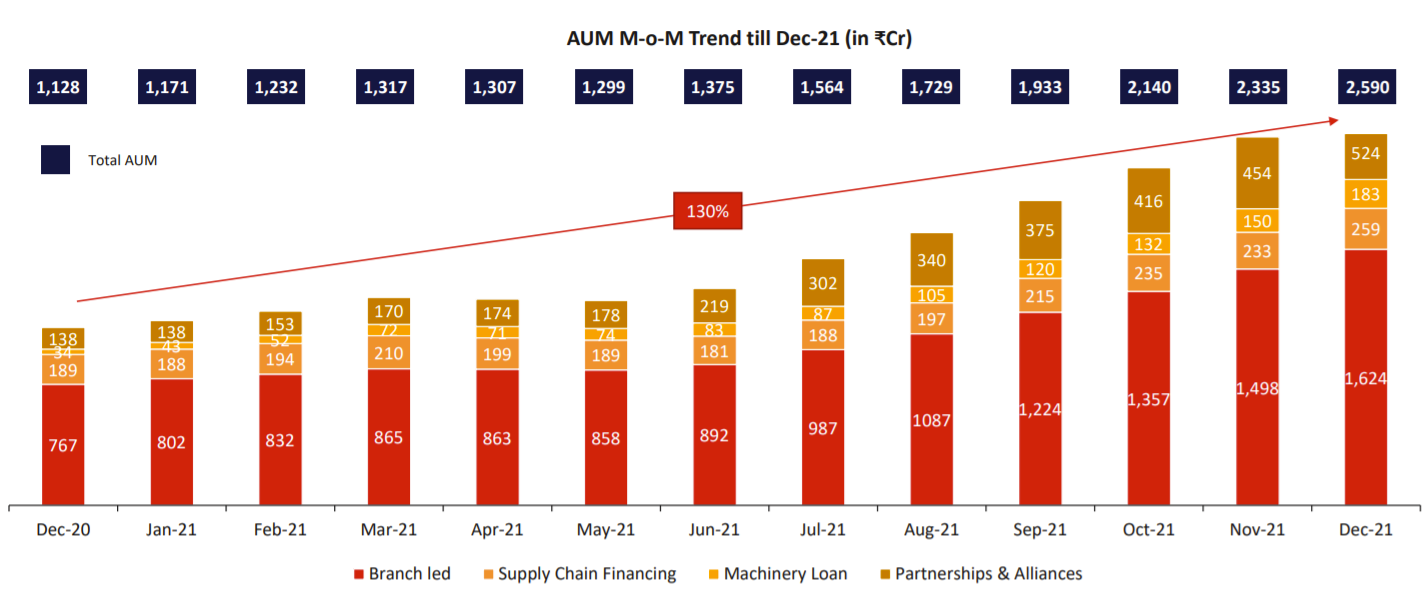

Updates for December:

- AUM has grown 130% YoY, 97% in 9 months, and 49.7% QoQ.

-

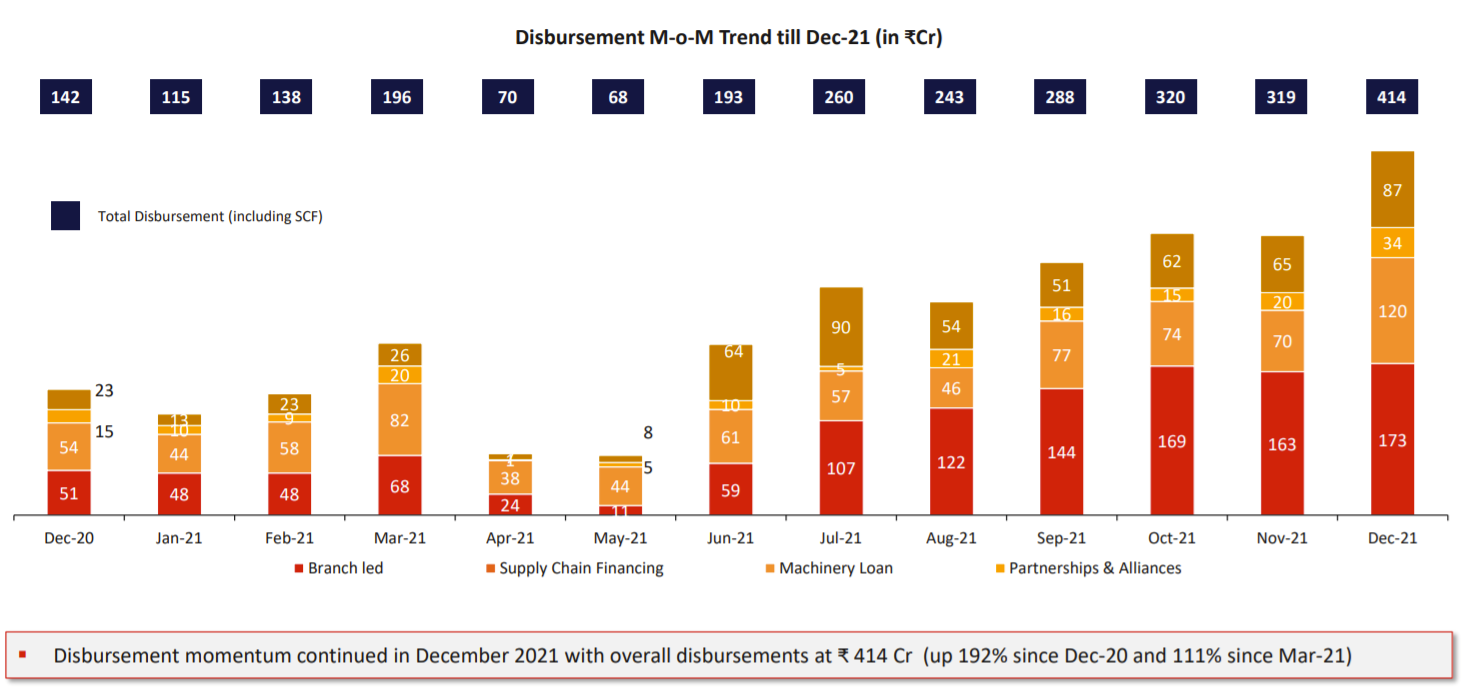

At the end of Q2FY22, disbursements were 288 Cr. On the concall, management told investors to expect monthly disbursements of 500-600 Cr. by the end of Q4FY22. We’re now at 414 Cr. in Q3FY22, well on track.

-

Expect Partnerships & Alliances to see the largest growth in FY23.

-

Collection efficiencies / bounce rates have steadily improved from the second wave of covid.

-

Branches have increased from 9 in March 2021 to 34 in July, to 75 in December 2021, with 34 new branches opened in the last two months. Should expect to see disbursals per branch go up as operations start running in full flow in these new branches.

If we calculate the target AUM of 20,000 which Mr Nath is aiming for, we can see that is around 75% CAGR AUM growth every year. Current CAGR First 13 Months’ CAGR growth is 130% as given in the presentation. Considering the fact that the base is too small in the early stages of growth, 130% is in line with the management target. In other words, AUM’s CAGR growth might not touch or shoot above 120% from next year.

Waiting for #Q3FY22.

Was nice to see Ugro and Shachindra get many a mention in @Rakesh_Arora’s latest note on co-lending. Hopefully someday all conversations around co-lending will have at least a passing mention of them with the kind of strides they are making in the space.

Disclosure: Invested

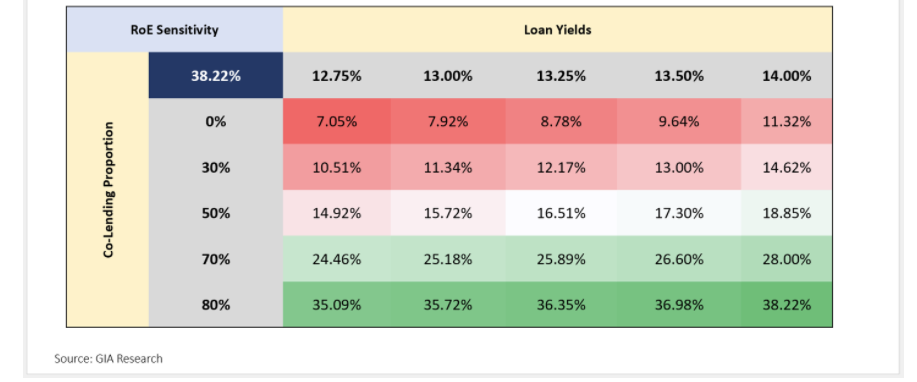

The takeaway from this article gives us another KPI for Ugro:

For their targets of 18.8% RoE, at the current loan yield of 15.7%, they need ~30% of their AUM to come from co-lending. (Depending on assumptions made about leverage and loan yields) Let’s ask how their loan book has evolved in the last 15 months.

| Date | AUM(Cr.) | Co-Lending % |

|---|---|---|

| 30/09/2020 | 979 | 14.40% |

| 31/10/2020 | 1024 | 13.18% |

| 30/11/2020 | 1072 | 12.13% |

| 31/12/2020 | 1128 | 12.23% |

| 31/01/2021 | 1171 | 11.78% |

| 28/02/2021 | 1231 | 12.43% |

| 31/03/2021 | 1317 | 12.91% |

| 30/04/2021 | 1307 | 13.31% |

| 31/05/2021 | 1299 | 13.70% |

| 30/06/2021 | 1375 | 15.93% |

| 31/07/2021 | 1564 | 19.31% |

| 31/08/2021 | 1729 | 19.66% |

| 30/09/2021 | 1932 | 19.31% |

| 31/10/2021 | 2140 | 19.44% |

| 30/11/2021 | 2335 | 19.44% |

| 31/12/2021 | 2590 | 20.23% |

-

Mr. Nath tells us that 50% of the disbursements in FY23 are expected to be through co-lending. This needs to play out for the thesis to remain intact. The bear case is them falling short of the target AUM, falling short of the 30% mark, and needing higher % of book to be under co-lending should the loan yields drop to sub 15%.

-

My assumption is 100% of the partnership channel is co-lending from banks. In reality, it’s blended with their co-lending partnerships with fintechs like Kinara. Therefore, depending on how much % the banks actually take up (my guess is >80%), the % of book under co-lending correspondingly needs to be higher.

D: Invested.

We have exciting new news! In a panel discussion around the impact of the recently announced Budget on the MSME sector, Shachindra confirmed that 9 more banks will be co-lending with Ugro after SBI, BoB and the rest.

Timestamp: at around the 5:15 mark

Disclosure: Invested