The current CEO/MD Mr. Bharat Vageria is more down to earth and nose-to-the-ground compared to his predecessor (and co-founder) who was very flashy. Current management takes all questions in the con-call seriously and answers them properly even if questions are repeats/answers are available in the PPT.

While the overall growth numbers in the last few quarters speak for themselves:

Company has tendency to get into niche areas whose growth/TAM is difficult for outsiders/investors to understand - I haven’t been able to understand even by asking questions in multiple recent conf-calls about how big the oxygen cylinder opportunity is and if it’s rewarding enough for management attention.

If it is for ambulances, are there a handful of businesses that equip an ambulance with oxygen cylinders and may be convinced of their efficacy ?

Not sure how big a sport is mountain-climbing in India for a Rs.4000+ cr revenue company to concentrate as a business vertical.

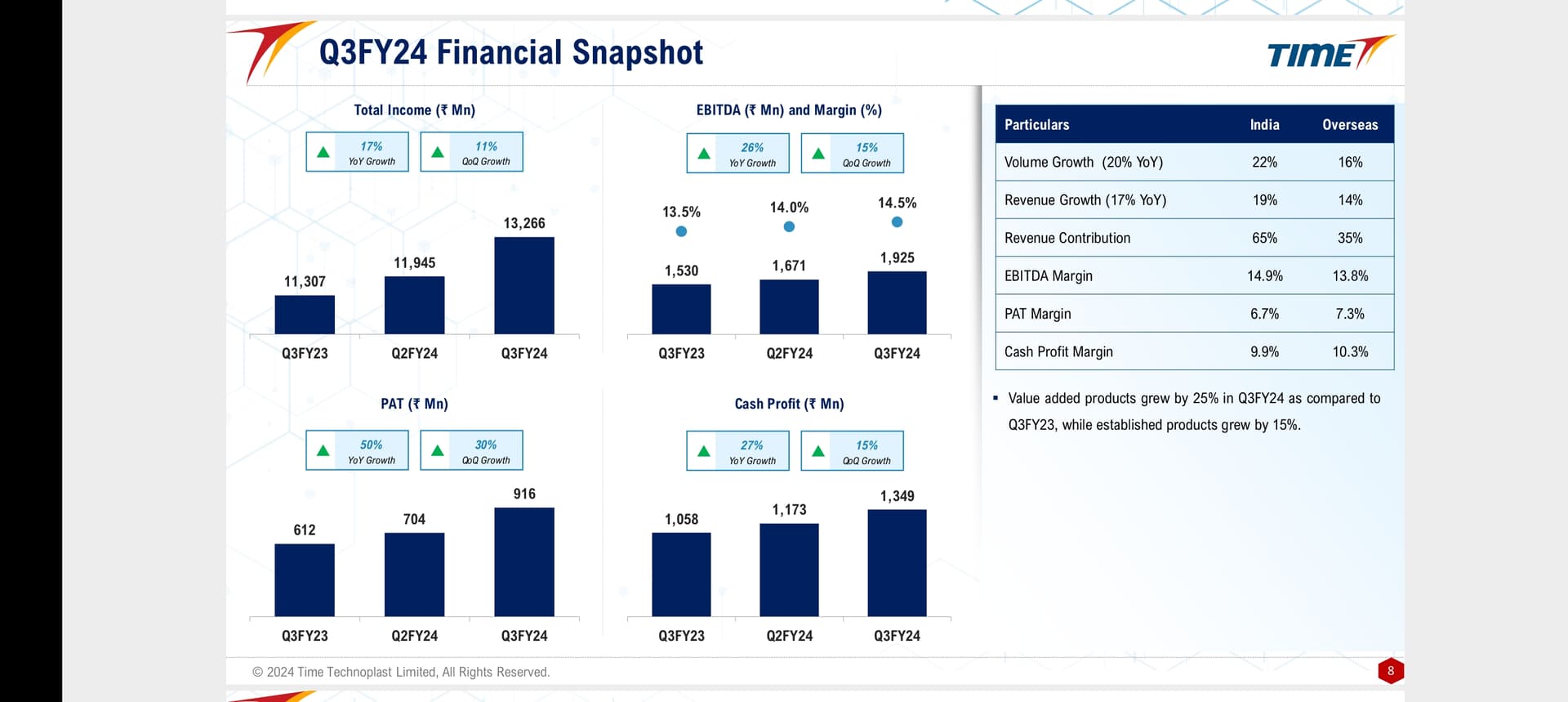

Overseas manufacturing (~34% TTM revenue) is mostly regular legacy products (with very little composite/value-add) but still has almost same EBITDA % as India manufacturing, and better PAT %. It also grew revenue at ~24% last year and ~13-14% this quarter.

India manufacturing (legacy products) revenue is stagnating with probably ~100cr annual growth on a base of ~1850cr.

Even among value-added products (EBITDA 17-17.5%) the only growth driver is CNG products (cascades) with revenue doubling every year and expected to atleast double annually for next 2-3 years.

All non-CNG value-added products (~810+ cr FY23 revenue have been growing at 10% for the last 2-3 years), with LPG opportunity not panning out as expected. With the IOC order last year (repeated this year) LPG is running at ~90% realizable capacity of 1Million cylinders and company is not confident enough of both local/exports demand to expand LPG capacity.

Thankfully CNG cascade/cylinders demand is growing rapidly and auto-cylinders are probably a good optionality after next 2 years or so (from FY26). Tata motors have mentioned that 1 in 3 cars they sell would either be an EV or CNG fueled.

LPG remains a far away optionality but left to distributors like IOC. Hydrogen needs to cross the hype stage.

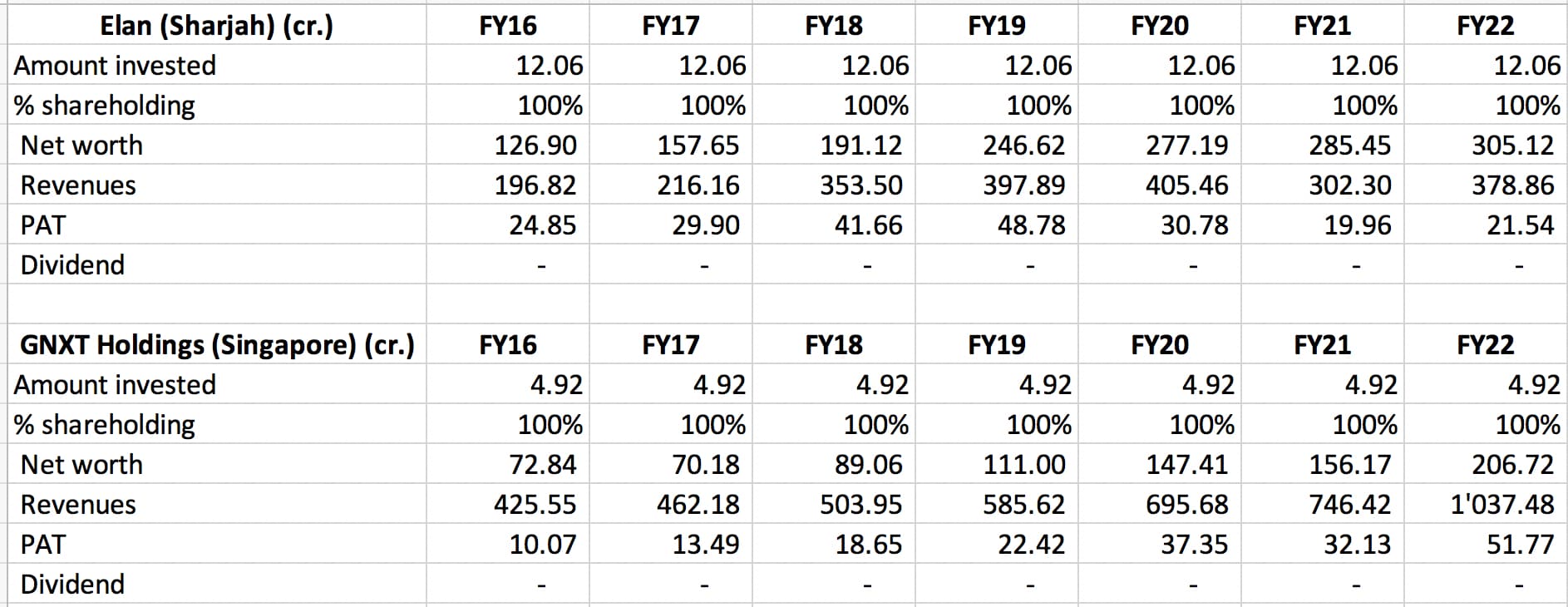

This is incorrect. Their overseas business is largely IBCs and composite cylinders and both are value added products. Excluding their US battery business, they have very good margins.

Just take a glance at the amount of capital they invested and the kind of money they make in exports.

Another good set of results, with sales growing by 14% and EPS by 27%. In the past, management used to overguide and underdeliver and this has changed significantly since Mr. Bharat Vageria has taken over as CEO. Not only are they being more measured in their capex spends, but they have been judiciously paying down debt while focusing more on value added capex. There is a good possibility that they end up delivering 20% ROCEs in next couple of years. Concall notes below.

FY24Q1

Debt reduced by 32 cr. in Q1FY24

Capex: 44 cr. (18 cr. towards established products + 26 cr. towards value-added products)

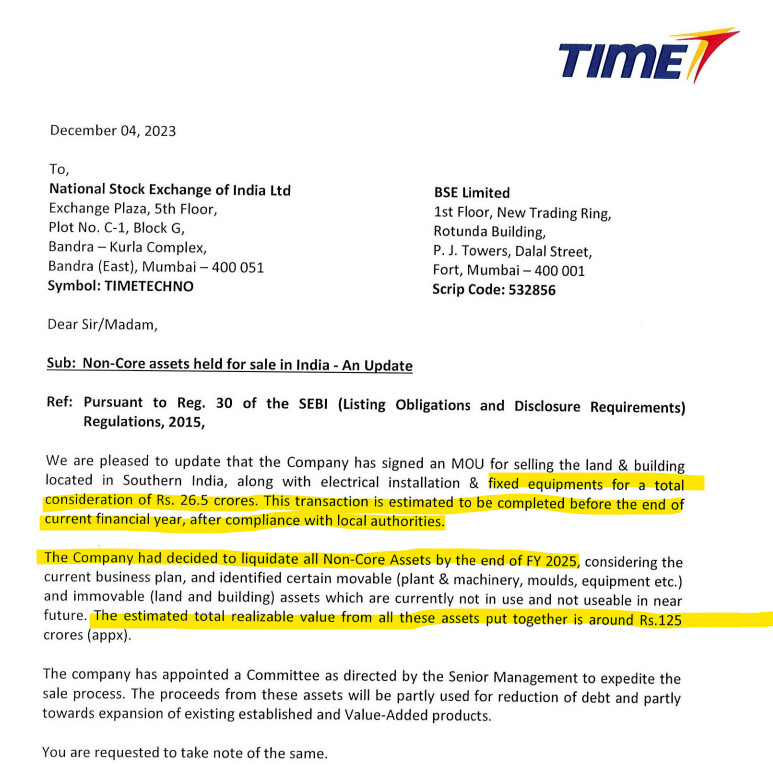

Divestment discussions are at an advanced stage, talking with multiple customers to sell different parts of business geographically

Expect 500 cr. of revenues in composite products in FY24

US has declined by 20%, but haven’t seen that kind of pressure in other export markets

Export breakup: 50% (South east Asia and Taiwan), 20% (USA), 30% (Middle East)

MOX film: have capacities to do 150-160 cr. revenues. Don’t plan to add capacity

Received PESO approval for manufacturing Carbon Fibre Reinforced Composite Cylinder (Type-III) for Medical Oxygen and Breathing air (first Indian company to get this)

Will submit hydrogen cylinder to PESO for approval in 2024

Disclosure: Invested (position size here, no transactions in last-30 days)

Time techno came out with good q2 fy 24 results with both topline and bottomline growth. Presentation attached.

Important update from presentation is “The Company is in advanced stages of discussion for 2 out of 3 geographies for the said consolidation cum restructuring of overseas business and

estimating to complete the transaction including receipt of proceeds in FY 2023-2024.”

If proceeds received from divestment are significant, then it could be a good trigger. Definitive timeline given for the corporate action. Concall on 16 th Nov will provide more details. disc: invested.

Company had given a deadline of end-Sep 2023 to complete the whole overseas sale for the last 8-9 months atleast, and clarified that 2/3 (US, SE Asia, SW Asia/Middle East) were in advanced discussions in last conference call. Looks like they need more time to close this. US business is going through headwinds, so one can speculate if selling US business is problematic.

CNG Cascades - 225 crores order book for next 6-8 months - ~170+ crores revenue possible in next 2 quarters for FY24. No other competition, but noises from BHEL-Indraprasta Gas MoU to develop CNG Cascades esp for hydrogen applications. Indraprasta Gas is a Time Techno customer.

LPG - going on BAU mode with IOC repeat order (~7.6L) utilizing most realizable capacity of 1M. They made ~231 cr in FY22, ~190 cr in FY23 and may be clock ~200+ cr in FY24. Looks like IOC order is high volume but less profitable as company hasn’t increased LPG capacity in last few years. Supreme Industries has got similar order from IOC, but not sure if Supreme competes with Time Techno by supplying to other PSU/private LPG companies

IBC - Expanding big time - company has IBC capacity directly and through subsidiaries both in India and all over the world (Type-4 LPG and CNG Cascade capacities are only in India as far as I know). Pyramid Technoplast which recently IPOd is a direct competitor here, and also expanding capacity judiciously.

FY24 remaining order book of 200 cr for pipes - these are good top line numbers, but this is less profitable and probably more working capital intensive too… cash flow might also take longer if this is related to govt contracts.

Overall a lot better than expected Q2 results, hopefully will lead to 650-675 crores FY24 EBITDA.

Management is clearly executing well on value-added products revenue/profitability… fingers crossed on their 17% EBITDA goal within 3 years… the goal was for 17% including overseas business, but will be easier to achieve with just India business.

Discl: Invested since 2018, added more till 2022, big part of portfolio.

I am pleasantly surprised that Time Technoplast has gotten into a very good growth patch, with improvement in margins and continued growth in sales. Sales grew by 16.6% and EPS by 41% this quarter. They are close to finalizing the international divestment deal. Concall notes below.

FY24Q2

FY24 revenues should cross 5000 cr. (H1:H2 revenue mix is 45:55)

Debt reduced by 2 cr. in Q2FY24

Capex: 55 cr. (22 cr. towards established products + 33 cr. towards value-added products)

CNG cascade: order book of 225 cr.

FY24 expected ROCE: 15.5% and 1.5% improvement each year

18-22% margins in composite cylinders

Seeing 15%+ growth in IBCs. GNX brand from Time Technoplast has been well established globally and is their main competitive advantage, as overseas customers ask for GNX IBCs for chemical shipments

Target divestment of 100 cr. of non-core assets and no non-core assets by FY25

Overseas divestment: valuation of ~1000 cr., will be selling 80%. Will be finished in FY24

I am also adding my notes from their AGM held earlier.

AGM23 notes

LPG Composite cylinders: Added new countries like Taiwan, Ghana, Nigeria, Bermuda, St. Lucia, Romania, Burundi and Australia. Applied for approval to supply LPG cylinders to the USA

CNG cascade cylinder order book: 250 cr.

Introduction of Multi-Layer Technology for Industrial Packaging products (Drums, Jerry cans and IBCs) for use of Post Consumer Recycled (PCR) material in the middle layer of the product and use of PCR material to manufacture IBC Components are few steps in that direction. To encourage reuse of IBC, innovative business models such as cross bottling, collection, rebottling and reuse is now the new norm

Overseas divestment: offering businesses on the basis of 3 regions, i.e. USA, South East Asia (including Taiwan) and MENA Region. Due diligence including legal process is on for two out of three regions and is expected to be completed any time soon

FY24 capex: ~200 cr.

Disclosure: Invested (position size here, no transactions in last-30 days)

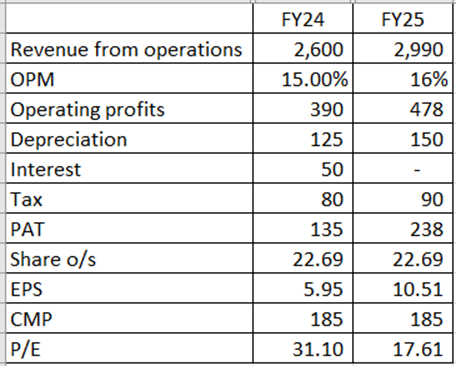

I don’t think “P/E of 16.5 X and an EV / EBIDTA of 7.7 X” is the right way to look at it. Since the company has already announced its plans to exit the overseas businesses, these investments should be looked upon as Assets Held For Sale. And so Time Technoplast should be valued on Standalone earnings, plus some value added for continuing subsidiaries such as TPL Plastech and the battery business.

Using Standalone earnings, a crude back-of-the-envelope calculation for FY24 suggests Time Technoplast may make something like Rs.2600 crore revenues and Rs.135 crore PAT, which gives an EPS of Rs.5.95 and a P/E of around 31 X. Benchmark P/E range for this group can be considered as 16 – 22 X based on where peer group companies trade.

The bigger jump in TTL’s numbers will come in FY25 when - if all goes as per plan – margins will improve further, debt can come down to zero or near zero and EPS can breach Rs. 10 plus. At this level, current P/E comes to 18 X which is in line with the sector benchmark.

Hi, Not doubting your numbers but if you look at FY24 company should be making around 5000 crs of revenue now overseas is 1/3rd of this so that should give 3.3K crs of revenue for Indian business. Thanks!

Thanks for your feedback, so let me clarify. My numbers are purely of TTL standalone entity, excluding TPL Plastech and battery business. If we add these, they would come closer to what you are saying. When management says India business, they are including all these.

I think TPL Plastech being a listed entity, it should be valued separately giving some holding company discount. TTL does not have full control over TPL Plastech’s cash flows. I prefer not to consolidate in such instances. Battery business can be consolidated, but it is a small one in the overall scheme of things.

And my main point is not the numbers forecast but the methodology - how the current valuation should be looked at. Looking at the current consolidated numbers and saying “P/E of 16.5 X and an EV / EBIDTA of 7.7 X” is not the right way. That is the point I was making.

Thanks! As I am holding this company since long time(& holding it from lower level) and I am trying probe what would be right valuation for this business as revenue quality is also improving due mix from value added products are on rise. I think reasonable PE should be b/w 15-20 but if you see it’s real competitor Pyramid, it has got rich valuation compared TT but it has also better return ration (which I am expecting in future for TT, if they continue on this path).

Likely scenario after completion of restructuring and aftereffects :

FY26 or 27

Sales

4000

OPM

15%

Operating Profit

600

Other Income

3

Depreciation

112

Interest

1

Profit before tax

490

Tax

26%

Net profit

362.6

1.80%

Maintenance capex

72

Owners earnings

402.6

While this is not going to be exact, but it is showing us an approximate picture,

Interest expenses will go down close to zero as company will pay off entire debt, so interest expenses of nearly 100cr will go to zero and entire amount of this money will flow towards bottom line through tax expenses.

Depreciation will reduce proportionately to sale of foreign assets, so that amount will also flow towards bottom line.

As share of value added product will rise, margins are going to increase, while I have used 15% , potential is over & above that.

This company is struggling for growth capital from many years and main reason for that was demand of maintenance capex from the established products or commodity products, company was generating around 200 to 250cr owners earnings in recent years and out of it around 100 to 120cr were maintenance capex requirements for the next year. Again much of the remaining money was going into working capital, so they only had a growth capital of less than 100cr from internal generation every year.

Now this scenario going to change, with the owners earning of 400cr in FY26 or 27, much of this money will flow towards growth capex as maintenance capex requirements will reduce and NFAT is going to increase and working capital requirement will reduce, so company can grow much faster in future from internal accruals.

My average buy price is Rs38.xx, so if they pay dividend of 10-12% of net profit as they are doing since many years, my dividend yield will be around 4.5%

ROE & ROCE are going to improve substantially.

As company will be able to grow from the internal accruals in the future, with share of value added products increasing constantly, will be net debt free, with higher ROCE and future perception of market participants towards high growth LPG, CNG & Hydrogen cylinder business this company can trade at any PE from 20 to 50, I don’t know.

I bought this business in 2019 & 20 at Rs38 mainly because it was exceptionally cheap at future PE of 2, I had no intentions to hold it above 150 but with passing year story constantly evolved positively. promoters started acting rationally, they tried to repair their past sin’s, and their composite cylinder business is too good to have. With its fast growth capability after restructuring at current price it may be trading at 5yr forward PE of 6 who knows.

I sold some quantity at 135 and I regret my decision, I still hold substantial quantity and do not intent to sell it anytime soon. because market is all about future, and as business is getting better & stronger with each passing year I don’t see much possibility to losing money.

Risks: Restructuring doesn’t go as planned, Promoters again start acting irrationally which is rare possibility.

Note: Not a SEBI registered analyst, do your due diligence before buying, only sharing my thought on business and I may be biased. I can be wrong and can change my mind anytime.