If they can crack LPG market this company can triple its sales… and price can reach 500… CNG cylinder market is very small compared to LPG. but it takes a lot to get the PSU oil marketing companies to move… in so many years they have managed to get one order from IOCL!

I think after IOCL it will happen sooner than later…

5 Likes

Company is going to show best ever results in q3 and q4 FY 23. They should expand composite capacity faster and launch composite for cars.

2 big triggers

- composite cylinder for cars

- composite cylinders for LPG - they need to get larger orders from IOC and also other OMCs.

6 Likes

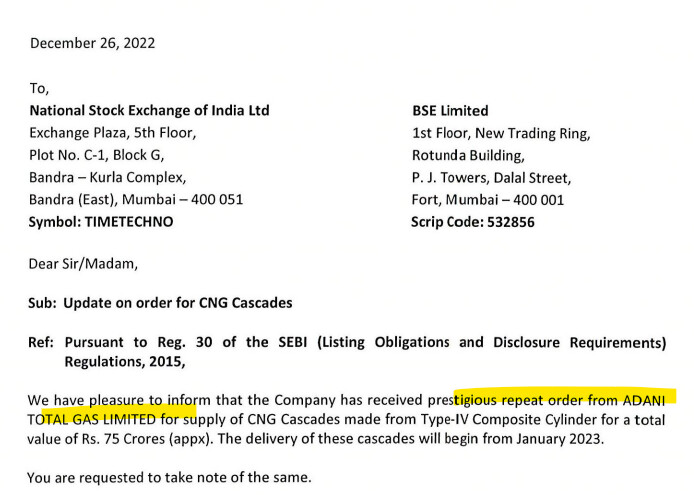

Received New Single Largest Order for Type - IV CNG Cascades and Expansion Status

Company has received order from Maharashtra Natural Gas Limited for supply of CNG Cascades made from Type - IV Composite Cylinders, for a total value of INR 134 Crores (approx.) to be supplied within one year period.

In order to meet growing demand for Type - IV Composite Cylinders for CNG Cascades, Management is undertaking capex in a phased manner:

Phase - I (FY 2022-23)

The Company is increasing the manufacturing capacity by 300 cascades (18,000 cylinders) in FY 2023 with a capital outlay of INR 55 Crores.

With the above expansion, the total cascade manufacturing capacity will increase from 180 to 480 cascades (28,800 cylinders) by March 2023.

Phase - II (FY 2023-24)

Under Phase-II, Management has already undertaken expansion program to increase the capacity by further 600 cascades (36,000 cylinders) and the same will be completed in Q4 FY 2024 with an outflow of INR 125 Crores. Total cascade manufacturing capacity after completion of Phase-II will be 1,080 cascades (64,800 cylinders) per year from March 2024.

2 Likes

Time Techno came with very good results when compared with other packaging cos. Sales grew by 20% and EPS by 14%. Company is on track of exceeding 350 cr. in composite CNG and LPG cylinders in FY23 and can do 500+ cr. in FY24. Concall notes below.

FY23Q3

- Received 134 cr. order for CNG cascade from Maharashtra Natural Gas Limited

- Divestment will be announced in 3 months, process is a bit delayed as International business did very well in 2022 and valuations will be driven by CY22 nos (& not on CY21 nos)

- CNG cascade expansion: FY22 capacity was 180 cascades (10’800 cylinders). By March 2023, capacity should increase to 480 cascades (@55 cr. capex; 18.33 lakhs/cascade). This should further expand to 1080 cascades (64’800 cylinders) by March 2024 (@125 cr. capex; 20.83 lakhs/cascade)

- Pipes and Mox film business have grown slower in FY23 vs other businesses. Pipe business has revived with cooling off PVC prices

- CAPEX: 169 cr. in 9M, includes 53 cr. towards capacity expansion, re-engineering automation for established product + 116 cr. towards value-added product

- Expect 1200 cr.+ revenues in Q4FY23 and 15% growth in FY24 (established products should grow at 10-12%, and value added at 25%+)

- IOCL has renewed their LPG cylinder order

- CNG + LPG revenues will be over 500 cr. in FY24 due to limited capacity

- In a normalized scenario, working capital for established products is 110 days and is 70 days for value added products

- Have applied to PESO for approval of oxygen cylinders

Disclosure: Invested (position size here, no transactions in last-30 days)

12 Likes

Wonder why valuation of company is so low inspite of very good numbers.

Low debt and good credit rating.

Demand more than supply in high margin composite business.

3 Likes

https://www.bseindia.com/xml-data/corpfiling/AttachLive/e7dbc79f-b2d5-46c0-8f11-19f3352567c1.pdf

Q4 results out.

1 Like

I used to sell Time’s technoplast Duro Turf door mat and rolls in 2010 - 2014.

Company was pioneer in this field and they were the first one to enter this market.

This segment has grown very fast since then but duro turf has not been able to maintain that growth rate or leadership position.

Market is now flooded with Chinese imports and other Indian companies Turf which offer similar products at far cheaper rate.

I guess, it is not a priority division for the company.

Also, I just visited their website and at bottom it still shows year 2017.

2 Likes

100% Pledge released. Sales have increased by 18% annually, Margins stable. Receivable and inventory days have also marginally improved.

Decent results by the Company.

Investor presentation:

3 Likes

Another good set of results, with sales and EPS growing by 15%. Company has scaled their composite CNG and LPG cylinders to 345 cr. and are now hoping to cross 500 cr. in FY24. Concall notes below

FY23Q4

- Sales: 4289 cr. (2831 cr. domestic + 1458 cr. overseas). Targeting 15% growth in FY24

- Capex: 223 cr. (87 cr. towards established products + 137 cr. towards value-added products)

- CNG cascade capacity of 480 cascades (28’800 cylinders; 300 cr. potential sales & 90% utilization) has come onstream and is fully sold out (current order book of 260 cr.). Phase II expansion will be fungible between hydrogen and CNG cylinders

- Divestment of overseas assets will finalize by September 2023, currently looking at alternate options as well (like selling assets in different geographical markets to different customers)

- ROCE will be 15-16% in FY24 and exceed 20% in 3-years (without taking divestments into account)

- Overseas split: Asia (50%), Middle East (34%), USA (16%)

- Rate of interest is 9.25% (blended with overseas). Has increased by 1.5%

Disclosure: Invested (position size here, no transactions in last-30 days)

11 Likes

Thank you for the notes - I think they’re being conservative with CNG cascade peak revenue possible. 180 cascades capacity = ~150 cr revenue in FY23; with 480 cascades capacity at full utilization ~400cr revenue should be possible, though current order book is 260 cr.

What I’m worried about is 2 years back during their analyst day, LPG was touted to be the biggest growth driver, while CNG Cascades was considered a relative optionality. There doesn’t seem to be much movement with Indane after the initial + repeat order of ~7L cylinders. There are ~29 cr gas connections = 58 cr cylinders. 25% conversion is ~14.5 crore cylinders, which is about 100x current Type-IV LPG cylinder manufacturing capacity in India (Time Techno = 1M, Supreme = 0.5M).

3 Likes

Agree… LPG is bigger opportunity - superior product as safer and lighter. can be very useful in rural areas/ last mile connectivity where cylinders will always be used…

Somehow they are not able to grow that business.

Main problem is with the higher cost associated with composite cylinder. Who will bear this cost … Customer or Oil Marketing Companies.

Customers - Those who opt for composite cylinder needs to make the additional deposit for it.

Q4- FY 23 Concall Notes

~Q4 % Increase YoY

Revenue-15% (India-10%, Over- 26 )

Volume-12% (India-8%, Over-22)

EBITDA- 21%

PAT-15%

~ Revenue Split

India-66%, Export-34%

~ CNG Cascade/Cylinder-

Order Book-260 Cr

Current Annual Capacity- 480 which could generate 300 Cr Revenue.

Expansion phase-II-600 no by Dec’23

•125 Cr Capex required which will be funded through internal accrual.

•Fungible between CNG & Hydrogen

Capacity after phase-II -1080,which could generate 800 Cr,assuming 90% utilisation.

Oppertunity of onboard Vehicles to unlock yet

No other Indian manufacturer

Some players import & assemble

In the next 5 years Composite can become 2000-2500 Cr revenue

~ LPG

Capacity-1.4 million

Capex not planned this year.

Can be taken next year depending on feedback from other Oil Marketing player.

~Re-structuring

Timeline- Sep’23

To be based on 2022 year no.

Each 3 continent business to sell seperately.

Objective of Restructuring in intact as earlier ( Debt, Capex & Share holder)

~ ROCE Guidance

13.5/16/19/20+% by FY 23/24/25/26 respectively.

Earlier guidance given is intact.

Following factor to help that

•More contributions Value added,

•Reduction in Working Capital

•Margin expansion

~ Value added % of Total sale-

23/25/30/35% by FY 23/24/26/28

~100% Promoter Share is pledge free

5 Likes

Hi forum members, really enlightening to see the conversation especially the track kept by @harsh.beria93 . I am a very new investor in time technoplast. Bought it a month ago. The company claims that it is the largest manufacturer of large size plastic drums. However, I did not find any report to corroborate this. Further in a lot of exports website and Indiamart, Time’s discovery is pretty low. Would be great if any supporting evidence is there??

1 Like

The significance of this for TTPL is twofolds -:

-

Continued high demand for type iv cascades as gas network keeps on increasing

-

Secondly, more importantly, they’ll be launching CNG TYPE IV CYLINDERS for Automotive application once Cng cylinders capacity expansion is completed this FY , both for OEM’s and Replacement/ aftermarket segments.

They have been focusing on cascades till now because of capacity limitations… once expanded capacity comes in, then Cng automotive application becomes another big, medium term/Long term growth driver.

I think that’s why they’re so keen on restructuring and selling majority stake in overseas business and investing it in india CNG operations… because the growth opportunity does seem quite attractive

7 Likes

Read second point of above comment… also go through concall notes posted above

2 Likes

Time techno maintained its track record of posting decent results and whatever management talks about in concall seems to be playing out in results.

For q1 fy 24, sales improved to 1080 crores from 945 crores in q1 fy 23. 14% growth.

EBIDTA improved to 148 cr from 124 cr. 19 % growth.

EBIDTA margin improved to 13.7% from 13.1%

PAT improved to 56 crores from 44 crores . 26% growth.

Debt reduced 31 cr q on q.

Divestment of overseas subsidiaries. Management talks about being in advanced talks for sale of overseas subsidiaries in two geographies.

Managament talked about 15% revenue growth and consistent improvement in margins going ahead. As per q1 fy 24 results, company seems to be headed in the right direction.

Sale of subsidiaries would be a big trigger as it will help in reducing debt significantly. Another would be some progress on sales of Hydrogen cylinders. As of now composite cylinders comprise of CNG, LPG, and Oxygen cylinders.

Company has a market cap of 3000 crores and a debt of around 900 crores . EV comes to around 3900 crores. TTM sales at 4400 crores. A lot of management talk focusses on debt reduction and improvement of return ratios.

Attached GMMA weekly chart shows a clearer picture with important resistances crossed and important resistances expected ahead in dotted blue lines. disc: invested. not a recommendation.

Technically, the stock price crossed an important 4 year high of 126 and has been consolidating above that level in a range of 130-142 for 4-5 weeks now. Previous all time high was at 232 in Jan 2018.

17 Likes