Time technoplast (it’s a well run company operationally, except for lagging profits):

Please do comment/ highlight, if you as a reader find the analysis lacking/ wrong.

Estd. in 1989 and employing c.3,600; it is a polymer product marketer/ manufacturer making multiple products like bin, drum, containers can etc. I found this report on google and the analyst summarises the company’s operations nicely.

http://www.hdfcsec.com/Share-Market-Research/Research-Details/StockReports/3018654

Below is my observation around the company:

Although, every analyst report talks about industrial packaging, lifestyle and other segments; the actual ones disclosed in annual report are polymer (earlier in 2011 yielding 15 odd percent EBIT, now three year average is 10.2%) and the other one being composite, consistently yielding c.9.7%. That said, Time doesn’t define the two segments anywhere in terms of product lines, business or any parameter!!

Their primary business is industrial packaging from which it derives three quarters of its revenues. In terms of geography, it derives c.two third of this industrial business domestically and remaining third is from overseas. In the segment, its customer profile is primarily chemical companies, contributing more than half of the segment’s revenue and the other big chunk is fmcg. Both these business are expected to do good in terms of sales volumes (remember the high PEs of the two industries). In terms of geography, Time has now moved out from Korea, China and Poland; and now focusing only on high growth geographies, which is very good decision i think, especially for its volume growth story.0

The other key segment is infra (c15% of revenues), comprising of pipes, prefabs etc. If we continue to believe in the Indian infra story, I do not foresee any volume growth concerns here and thus increasing profitability. The pipes business grew by 15% in FY16. Battery business they are willing to sell.

The two other small businesses (5% each) are lifestyle (mats etc) and automotive components. The former might see some increasing competition (essentially commodity, limited specs) but its auto business might continue to flourish where spec requirement is high.

The other business is its composite cylinder; first I noticed its mention around some report of 2011 (yes 2011). The business over the years languished with company shifting its bases; now entire 700k/annum capacity in India. These cylinders are in different sizes, slightly (c.20%) more expensive than the regular ones; and given the kind of product it is, it requires a lot of approvals in each country. This business is finally now gaining traction with some volume visibility and approvals from c.25 countries. Although adoption by the markets is yet to be tested (trial quantities so far); but as a consumer if given an offer, I would like to have an explosion proof and more aesthetic cylinder; even at a few extra rs and just the Indian replacement demand is more than 20 mm a year. This business represents a huge opportunity, but only in a few years time, after the early adoption stage. The other competitor to them domestically is Supreme with 400k capacity.

Management: In terms of management, what I really like is that all of the executive directors have professional background, with some working in prominent companies of their time. All of them prior to forming Techno, were working in Prestige HM Polycontainers; and if you note from company’s website, they are performing the same functions now as back then in HM-polycontainers; one from finance, marketing and production!!! The other good thing I like is lack of equity dilution (in terms of new issues/ esops etc) over the years.

In terms of its shareholding: promoters hold c.58.5%; while DIs hold 8.7% and FIIs hold 19.5%. The amount of institutions shares has been around 30% for few years now.

Operational/ financial metrics:

• Revenue CAGR over last three years is 11.2% (noting FY16 flattish due to commodity prices (volume growth was 10%) and 14.2% over five years. With the company present in high growth geography, volume and thus revenue growth should remain elevated over the medium term, with a possibly good kicker coming from cylinders in two-three years time.

• EBITDA margins have remained relatively constant over three years (c.14%) but this should improve (reasons below) with increasing operational leverage with volume ramp-up.

• The Company has been good at cash flow generation and that is after deducting cash interest from operating cash flow. The company has consistently reduced its free cash flow deficit (CFO less cash interest, capex and dividends) over last five years; turning positive in FY15 and FY16 is expected to be no different.

• Working capital management has been very good with cash conversion cycle hovering around 95 days over past few years (increased in FY16 to 106, but lets wait for annual report). Lately, from my work experience I understand that business and competition intensity is increasing in India and a cost of this in domestic market has been increasing working capital cycle; which thankfully this company has avoided so far.

• In terms of asset turnover as well; Time has shown improvement increasing from 0.9 in FY13 to 1.04 in FY16.

• The only area it has lagged in is profitability, which along with increasing equity base has resulted in low ROE of c.10.5% over last few years.

• Liquidity of the Company looks fine and debt appears to be very manageable at 772 crs with current cash flow and growth outlook (AA- rating by crisil).

Key driver in growth going forward would be:

• Expected good volume growth of overseas units, which will mean better capacity utilization (FY16: 65%, of overseas units) and lower fixed costs/unit.

• Above is true for Indian business as well but the volume growth is lacking its overseas operations; although was at good 10% yoy in FY16 and capacity utilization at 85%

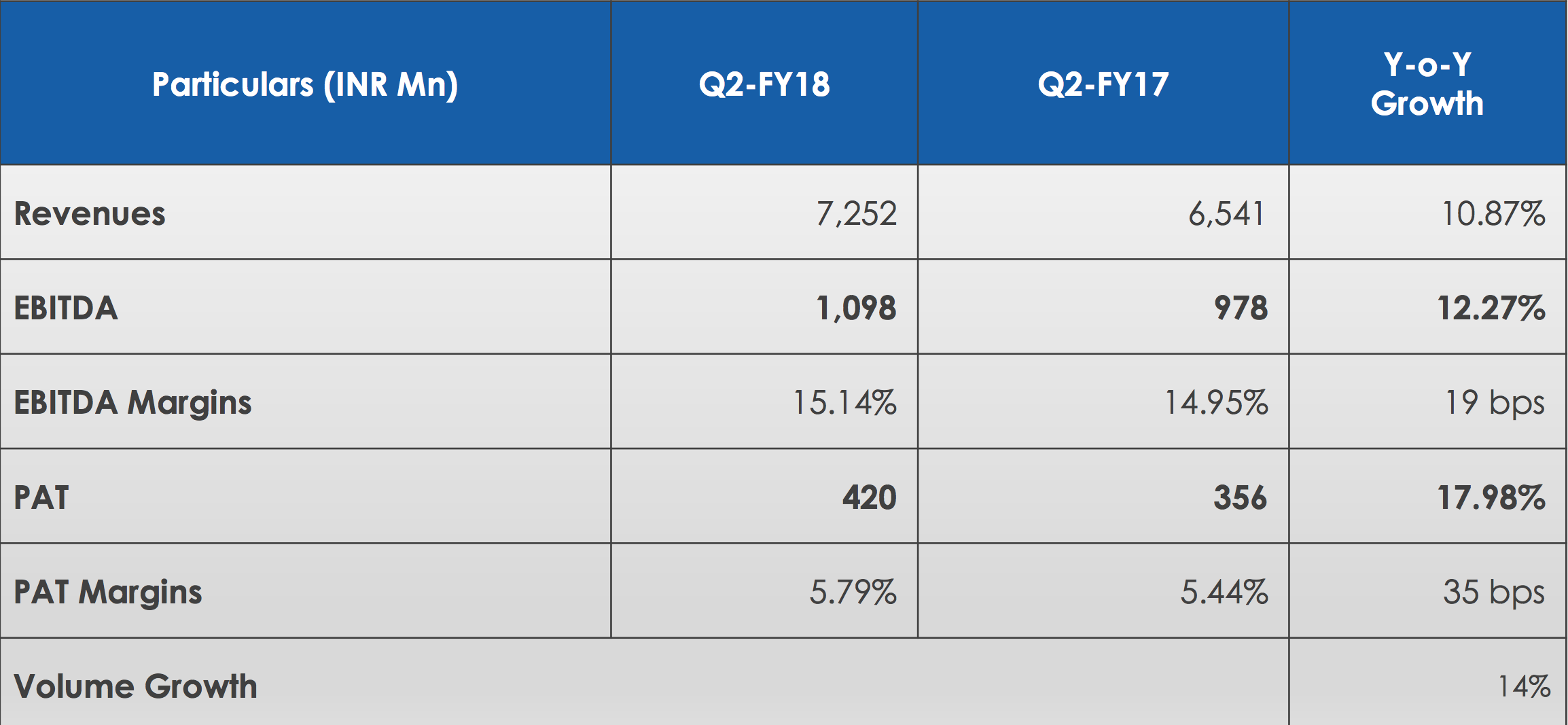

• FY16, they discontinued certain business, because of which results were not comparable; accounting for which FY16 revenue, EBITDA and PAT would have grown 5.1%, 6.9% and 8.7% yoy.

- Increasing focus on growth from internal accruals, which should improve balance sheet, and limit interest outgo.

- Possible improvement in incremental margins in the industry itself, with demand getting picked up.

Quote from the concall on future growth ”Anil Jain- So I would close on the note that we have set out targets for ourselves FY-2021 the turnover of this company and the profits et cetera will be double of what we have done in FY’15-FY’16 and our ROCE should be in excess of 20%.” This appears to me a manageable target and during the call he also mentioned of keeping the debt max at current levels and fund the future growth from internal cash. This also looks believable with good cash flow generation and tight working capital control so far; which if happens would be a double bonanza for equity investors with growth and same debt levels; a significant jump to EPS.

The Company is currently trading at a trailing PE of 12 in mid 60s; lower than its peers on relative valuation multiple, with good operational record, making me think its slightly undervalued and might get rerated in the medium term with hopefully better results. Also, the stock has seen remarkable upward momentum in short term, and may be its prudent to wait for some time to settle down before adding positions(but just my view).

Disclosure: I am invested in the stock at an average price point of INR50.6/ share (c.5% of my portfolio), invested over last two months.