the text that you have highlighted " with identified buyer" . will you please help me understand, what are you trying to indicate ?

They are about to complete the transaction with potential buyer subject to due diligence

Company came up with decent nos, sales and profitability reached FY19 levels. Management is confident of growing sales @15% past 4000 cr. in FY23. Concall notes below

FY23Q1

- Expect 15% revenue growth in FY23 and should cross 4000 cr.

- Capex was 48.5 cr. (34 cr. for value added + 14.5 cr. for existing products which is mostly maintenance in nature)

- 60-70% of LPG cylinder capacity is booked by IOCL. Q1 revenues were muted for LPG due to floods in certain regions. The division is running at 90% capacity utilization

- Composite cylinders (LPG + CNG) should exceed 350 cr. in FY23 (planning for sales of 950’000 LPG cylinders + 225 cascades)

- Current cascade capacity is 20/month which should increase to 25/month in next-6 months. This capacity addition will cost ~130 cr.

- Based on current LPG capacity (~1mn cylinders out of theoretical capacity of 1.4mn), can do sales of 230-240 cr. (realizations of 2300-2400). Expansion of 1mn cylinders (~90 cr. cost) is only planned and will execute it as they get better order visibility

- Have slowed down CNG cascade order booking as they are running as full capacity

- Complete benefit of additional LPG + CNG cascade capacity will reflect in FY24

- Expansion for CNG on-board will happen in next phase after the current capex of CNG cascade. Focus will be more towards passenger cars as that is a high value segment

Disclosure: Invested (position size here, bought shares in last-30 days)

Q1FY23 CONCALL NOTES:

• Expecting to cross Four thousand crores in revenue in FY.

• Why is growth lower QOQ? – From the last 15-20 years, revenues have followed the following pattern – 20-22% revenue of full FY in June, 25% in Q2, 25-27% in Q3 and 30% in Q4. So, that’s why the drop in revenue.

• COMPOSITE PRODUCTS (CNG + LPG): Very Robust demand for the composite products. 230cr of Sales in FY22. Expecting minimum 350cr in sales from composite products (Very conservative estimate).

550cr Order Book currently for CNG cascades + LPG cylinders. Full capacity booked. Going slow in order intake because of capacity constraints.

New capacities to come by end of FY23 – CNG Cascades expansion ongoing. Current capacity – 150cr, Order Book – 250cr. 125cr Capex, 400cr revenues possible on 125cr capex.

LPG Cylinders 1 million cylinders expansion (current capacity – 1 million) will be done based on expected order flow from other OMC’s.

• WHY THE RESTRUCTURING OF OVERSEAS BUSINESS? WHY NOW? – There’s too much opportunity in India for composite products. Need to invest in Capacities to fullfill current and upcoming demand.

Also, Value-added products have 20% Ebidta margins vs 13% for the overseas business and lower working capital requirements. Both of these factors will help in achieving the 19-20% ROCE goal set by management in the next three years.

Targeting 1000cr revenues from composite products itself in 2-3 years’ time.

• 50-60% of proceeds from restructuring will go towards debt repayment, 200-250cr for value-added products capex and remaining will be given as a special dividend or buyback to the shareholders.

• Company will continue to hold minority interest in the overseas operations. Management and personnel will continue to be the same.

• Will look to consolidate product mix and operations of Indian business as well.

• Currently in talks with 3- Wheeler companies for trial of Li-Ion batteries.

• Raw material prices are softening.

• Company has 1-month pricing mechanism for 50% of customers and 3-month pricing mechanism for 40% of customers. Thus, all the volatility of raw materials is passed on to the end customer, but with a little lag.

• Competition – 3 companies in TYPE-IV Cylinders. All of them are importing. TTPL is the only company to manufacture in India. Government preference for Made in India products.

Disclosure: Invested (Biggest holding of portfolio)

@harsh.beria93 @pranavpallod12 thank you for the notes. I felt mgmt’s response was weak and not convincing for these 3 questions:

- While they’ve been talking of 18-22% EBITDA for value-added products for the last 2-3 years, the highest has been 17%+ (lower than the low-end). This is supposed to be the driver for next 3-4 years atleast. Either they could have explained what’s stopping from attaining this EBITDA range or guide to more attainable range.

- There hasn’t been any revenue growth from FY19 Q1 to FY23 Q1 (comparing just quarters).

- Supreme without current capacity (and from what Time Techno mgmt says without owning technology) has aggressively bid for and got a larger LPG contract vs Time Techno from IOCL(Indane). What’s stopping Time Techno being a bit more aggressive. Are they being safe and waiting for orders to add more capacity by anticipating that more orders from IOCL may not come soon ? This is inspite of them claiming to be kings of Type-IV LPG cylinders (in India and exporting) for last several years. I wouldn’t have felt bad if Time Techno had got say 55% of the IOCL contract and Supreme 45% , and not the way it happened.

Overall ok quarter, I feel debt, restructuring and the land sales is taking a lot of mgmt attention, and they’re being very careful after mindless expansion and lack of fiscal prudence in the last several years. Invested since 2019 and adding.

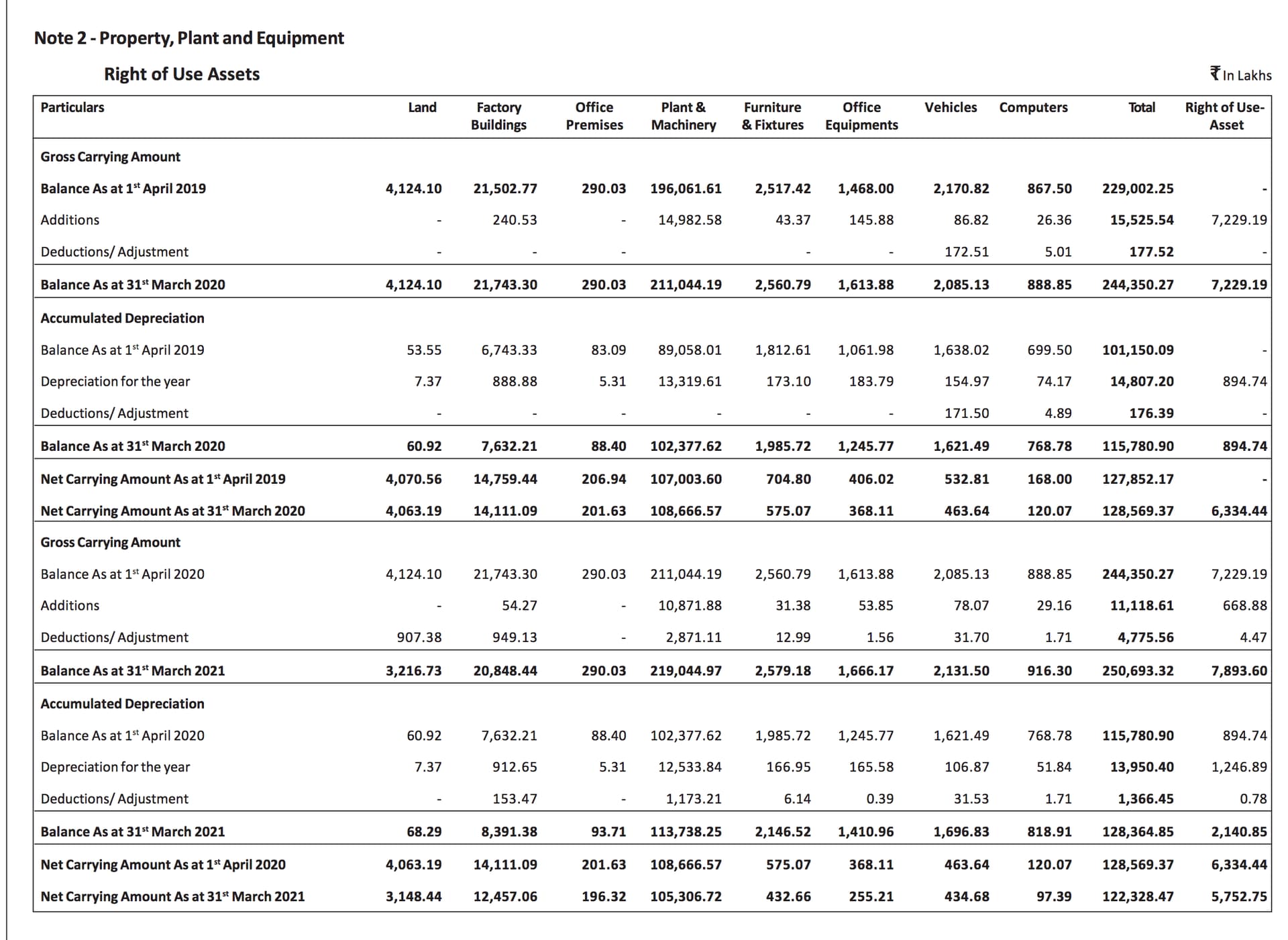

Sales of the Company has increased from Rs 2755 Cr (FY 2016-17) to Rs 3650 Cr ( 2021-22) whereas CAPEX incurred during the same period was 212 Cr, 244 Cr, 231 Cr, 138 Cr, 102 Cr ,179 Cr.

In-spite of significant CAPEX done by the Company there is no significant improvement in Sales. With this kind of CAPEX (Rs 1106 Cr during last 5 to 6 years) expenditure , the Company should have build up significant capacities. Can any body advise comparative capacities of the Company as on 31/03/2016 & 31/03/2022.

Where are the CAPEX expenses going ???

Capacities for that year should be available from the annual reports, can also be cross-checked with the gross/net block and depreciation. Some of these may also be maintenance capex which will happen every year (not sure of quantum, will be available from the presentations and ARs).

Of the top of my head I can think of:

- The LPG line (1.4m capacity but only 1M throughput)

- All CNG related capex

- Atleast half the US expansion if not full

There were irregular if no conf calls in 2018 till 20-21, improved a lot with regular conf calls in last 2 years with an additional 3 year plan detailed call in June 2021.

A 3-4 years promoters pledge of shares to hold on to some land in Mumbai (and build a business center) was released recently, with an imminent announcement promised about selling that land.

I feel the mgmt is course-correcting and doing a lot of things right now - not getting distracted by land for office HQ and trying to disposing it off, conservative with debt, looking for partners/equity in only lower profitable overseas investments, investing mostly in only higher profit areas etc., they’re willing to sell off the battery unit too (only 20-30% utilized) which surprisingly has a 100cr order book for FY23.

As per management 1 Million LPG capacity cost around Rs 85 Cr and they have spend Rs 1106 Cr during last 5 -6 years. My observation is that inspite of spending Rs 1106 Cr in CAPEX, substantial capacities have not been build up. Last year also they have spend around Rs 179 Cr in CAPEX and still there was no increase in LPG capacity because of which they did not bidded for LPG tender.

This can be treated as a “red flag”. Capex is regularly used by companies to divert money as per seen in few of my bad investee companies like Talwalkars and Manpasand Beverages.

Not saying there is necessarily fraud over here but any company, doing regular large capex without commensurate increase in capacity, calls for deep dive analysis for sure.

Disclosure - in watchlist

You need to refer to last 5 years presentations as to where the capex had been spent

This company was into multiple product lines and so many geographies , that it had too many mouths to feed …

Refer to this old 2020 presentation you will understand complexity

Now for first time they are prioritising … Hope they might to better job in allocating capital

It seems Company is capitalising its Expenses to show improved EBDITA margins. This may also be the reason of higher amount under CAPEX without any meaningful capacity addition and also resulting in higher deprecation amount every year.

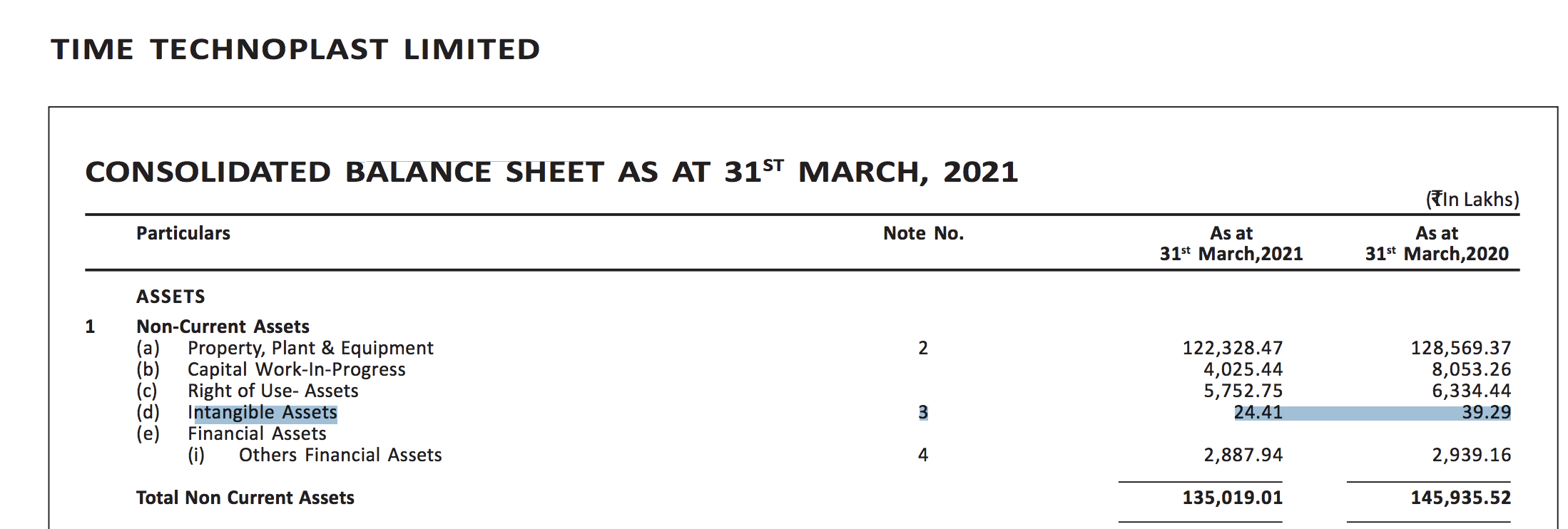

Whats the rationale behind this statement? A casual glance at the balance sheet shows there are no revenue expenditure items in non-current assets.

If a company is capitalizing its revenue expenditure, it can done in 3 ways:

- By putting revenue expenditures as part of intangible assets

- By putting them under other financial assets

- By putting them under PPE & CWIP

1. Intangible assets: There’s barely any

2. Other financial assets: These are clearly explained as deposits to government or payments made to vendors.

3. PPE: All the items mentioned in this schedule corresponds to capital asset of a company.

In last 3 years, cumulative fixed asset purchases was ~427 cr. and cumulative depreciation was ~464 cr. In this time period, company achieved higher overall capacity (e.g. added LPG capacity). Thus, depreciation figure is actually in excess of maintenance capex, thereby penalizing net income. This is a common phenomena in a growing company, where depreciation figure may not actually represent true nature of maintenance capex.

If you need clarifications, let me know. I don’t see how company is capitalizing its expenses.

Disclosure: Invested (position size here, bought shares in last-30 days)

Read some of above post, many people are concerned about where did the amount spent over the years on capex is gone?

as per my knowledge this company’s business requires high maintenance capex in the range of 80-100cr every year, so most of that amount is gone into maintenance capex, nothing to worry about it.

Disc: Invested

TTPL

MARKET CAP 2300CR

RESTUCTURING OF OVERSEAS BUSINESS–(1/3)

Business is around 1200cr.

Valuation Deal around 2000cr.

Indian business (2/3)

Valuation must be 4000cr.

Cash deal of overseas business is around2000cr.

Rerating of comapny is on card. Market cap should be around 4000cr…

Video link is attached.

Disclosure holding 4% of PF

AR22 notes

- Value added products (21% contribution vs 20% in FY21): Composite IBCs (11% vs 10% in FY21), composite cylinders (6% same as FY21), MOX films or techpaulin (4% same as FY21)

- R&D team comprises of 30

- Time Techno is third largest manufacturer of IBCs globally

- Overseas business contributed 32% of sales (vs 31% in FY21). EBITDA margin for domestic operations was ~14.0% and for overseas operations was 13.7%

- Company is restructuring overseas business through strategic divestment, proceeds of which will be used for repayment of debt, capex for composite cylinders and for core Indian business

- Has manufacturing facilities at 31 locations across the globe (including 21 within India)

- Received single largest for Type-IV LPG Composite Cylinders to IOCL of 0.75 mn LPG cylinders to be supplied over 12-months

- CNG cascade order book is 250 cr.

- Total capex incurred was 185.7 cr. (vs 103.5 cr. in FY21). Capex for established products was 78.5 cr. (vs 67 cr. in FY21), and was 107.2 cr. (vs 36.5 cr. in FY21) for value added products

- Key raw material is PE granules (derivative products of oil and natural gas) which are largely imported

- KMP and director remuneration: 1.96 cr. (vs 1.64 cr. in FY21)

- Number of employees: 2’521 (vs 2’423 in FY21) (no increase in salary of employees or key managerial personnel)

- Statutory auditor fee: 40 lakhs (vs 45 lakhs in FY21)

- Number of shareholders: 73’356 (vs 37’672 in FY21), price (low): 60.2, price (high): 94.5

Disclosure: Invested (position size here, bought shares in last-30 days)

Good Q2 results. Margins a little down but sales on track. Margins will improve coming quarters with decline in crude prices.

Their strategy of improving product mix is working well. At expected EPS of 12 price should be 150.

Just an additional observation - the cash flow from operations has improved to ~175 Cr vs ~110 Cr last year on account of better management of working capital. Going forward the key monitorable has to be the debt reduction and finance cost.

Investor presentation - here

Q2 Results - here

As they have the pass through mechanism of raw material inflation, believe raw material reduction will also be passthrough to customers. Also the raw material they directly related to crude prices but the price is more to do with supply - demand.

Company came out with decent nos, with 12% YOY sales growth and flat PAT. Concall notes below.

FY23Q2

- Packaging product order book is monthly

- Growth was driven by overseas business (21% YOY vs 8% for India)

- Pipe business target is 200 cr.+ in FY23

- LPG cylinder: 80% domestic + 20% exports. In recent quarter, export mix increased to 40% due to higher rainfall resulting in changing demand schedule from IOCL. Running at 85% capacity utilization. No planned expansion until they get order from other OMCs

- Guiding for 1%+ improvement in EBITDA margins and 20%+ revenue growth in H2FY23

- Generally, H2 is 55% of business

- Expansion of Supreme Industries in LPG composite cylinders is because they don’t have enough capacity to service current order book. Even after their expansion, Time’s capacity will be higher

- CNG on-board cylinder marketing will start only after expansion is complete

Disclosure: Invested (position size here, bought shares in last-30 days)