Hi , I have been following your stock market journey since last 6 months and am in awe of your capacity to read and track wildly different industries and your knowledge base. Just wanted your opinion on a stock screening idea . I have been thinking of tracking the portfolios of what small caps mfs are buying in India from value research and then doing my on due diligence(aka reading concalls , annual reports and vp threads) . what are your thoughts on this process. I know this is a little bit of a cop out but do want to know what are the cons of this process . I know the pros are that evidence of institutional support , and high probability of dd by more experienced fund manager with better resources and time then me . Also any other stock screening ideas would also be appreciated . Thanks

Hi Harsh What is your view on Shree Ganesh Remedies on their recent performance. Are increasing your allocation

I have made a few changes to the model portfolio:

-

Initiated 1% position in Sharat Industries. I plan to play the shrimp sector via the market leader Avanti, where I already own 4% position and a smaller co like Sharat which can benefit disproportionately with revival in the industry. Sharat is currently operating at 50% utilization and has reported good quarterly results (flat sales, 32% EBITDA growth, 64% EPS growth). Management has been guiding for 15-20% sales growth, 20-25% EBITDA growth, and 25-30% PAT growth over next 3-4 years. By FY26, they want to reach 9-11% EBITDA margin by improving their capacity utilization. If this turns out to be the case, their FY26 revenues can be around 500 cr. and they can potentially report 20-25 cr. PAT. Their current market cap of 137 cr. offers a very good risk reward.

-

Reduced position size in NESCO (from 4% to 2%), Ajanta Pharma (from 4% to 2%), Sundaram Finance (from 2% to 1%). This transaction is largely to make space for new companies in the portfolio, and reallocation to other bets, where I feel risk reward is better. Ajanta has been one of my favorite businesses, however they have been topping out around 6.5x sales, where they are currently trading. Nesco is not so expensive, so my quantum of selling has been much more measured here. Sundaram has doubled since I bought, and are now trading at higher end of their valuation band, hence taking money off table.

-

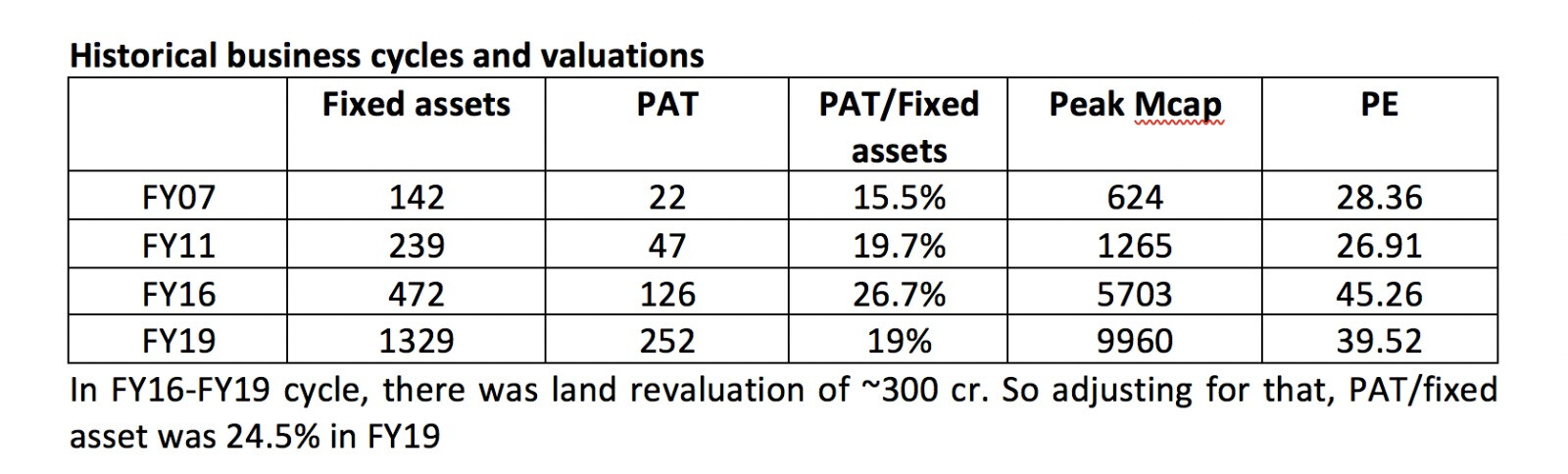

Increased position size in Aegis Logistics from 2% to 4%. I have been amazed at how Aegis has grown over time. Its rare to find a small cap which has grown profits by 10x+ in 10 years, while maintaining 20-40% dividend payout without equity dilution.

They have managed to reach PAT/fixed assets of 15-20% in good times. With current LPG expansion, their net block in 3 years will be around 5000 cr., which implies they can reach potential PAT of ~1000 cr (vs 510 cr. in FY23). I am reasonably confident of them achieving these nos, given their very good track record. Current valuation of 21x PE is towards the lower end of their traded band.

-

Increased position size in Propequity from 2% to 4%. This is largely due to stock doubling in quick time, rather than me adding to existing positions. They have been scaling very well, and plan to maintain sales growth of 30%+ in the near term. Their current revenue runrate is around 35 cr., and I feel they can reach 70-80 cr. sales in next 3-4 years. As this is a unique business model with very high margins and low capital requirement, I feel market will ascribe 10x+ Mcap/sales if they scale well, and I hope that they cross 1000 cr. Mcap in the next few years.

-

Reintroduced Chamanlal Setia at 2% position size. The numbers being reported by Chamanlal is worth noticing. For these kind of nos, I feel 8-9x PE is quite cheap. This being a cyclical space, I am closely tracking basmati prices as any sharp drawdown in that can bring down their earnings. I just hope that I am not buying at peak earnings!

Updated folio is below and cash stays at zero.

Core compounder (44%)

| Companies | Weightage |

|---|---|

| Aegis Logistics Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| HDFC Bank Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Gufic Biosciences | 4.00% |

| Godfrey Phillips | 4.00% |

| P.E. Analytics Ltd | 4.00% |

| Ajanta Pharmaceuticals Ltd. | 2.00% |

| NESCO Ltd. | 2.00% |

| I T C Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| LINCOLN PHARMACEUTICALS LTD. | 2.00% |

| Caplin Point Laboratories Ltd. | 2.00% |

| Aptus Value Housing Finance India Ltd. | 2.00% |

| Shree Ganesh Remedies Ltd - PP | 2.00% |

Cyclical (44%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 2.00% |

| Stylam Industries Limited | 2.00% |

| Ashiana Housing Ltd. | 2.00% |

| Ashok Leyland Ltd. | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

| Time Technoplast Ltd. | 2.00% |

| RACL Geartech Ltd | 2.00% |

| Manappuram Finance Ltd. | 2.00% |

| ANUH PHARMA LTD. | 2.00% |

| Dharmaj Crop Guard Ltd | 2.00% |

| MAYUR UNIQUOTERS LTD. | 2.00% |

| Godrej Agrovet Ltd. | 2.00% |

| Chaman Lal Setia Exp | 2.00% |

| KSE LTD. | 1.00% |

| Sundaram Finance Ltd. | 1.00% |

Turnaround (2%)

| Companies | Weightage |

|---|---|

| Punjab Chem. & Corp | 2.00% |

Deep value (10%)

| Companies | Weightage |

|---|---|

| Geekay Wires | 2.00% |

| Worth Peripherals Ltd | 2.00% |

| Sharat Industries | 1.00% |

| Jagran Prakashan Ltd. | 1.00% |

| D.B.Corp Ltd. | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

| Modison Metals | 1.00% |

| RKEC Projects | 1.00% |

I have never found a single good stock idea from a MF, instead I have seen a lot of MFs buying a stock I already own or track, which then increases its valuation. So, I am not the right person to answer this. On VP, there is no dearth of stock ideas.

Very good performance, I have increased allocation a bit, but not a lot. In hindsight, I should have taken larger bets on a number of pharma cos earlier this year (SGRL, Caplin, Anuh, Lincoln, Ajanta). But overall I am reasonably satisfied with my bunch of pharma cos, I will try to increase position in SGRL if there is a big dip.

Sales were reported at 1235 cr, less QoQ and YoY, still PAT at 192. Not an expert in reading figures, eager to understand.

Hi Harsh,

On Amararaja - Given Li Ion is a new game altogether where commericial viability is not established, neither who will become market leader is certain , what gives you confidence that Amara Raja will be successful?

As Amararaja will be investing more than 50% of its cash flows to Li ion batteries for many years to come, dont you think its a risky bet, in case it does not works out?

Please share your views.

Also if you can share some reference material to understand Li Ion battery value chain, it will be highly appreciated.

Amit

How has your portfolio being performing? Do you track against Nifty/Smallcap/MFs?

@harsh.beria93 Hello Harsh, Even I could not find any reference to Pneumatic nails in their AR. Also, it is a high margin product and Geekay seems much ahead of Maiden forging in its production I am wondering why would company deny the product line in their AGM and does not capture in their AR. Any insights/inputs highly appreciated

Hi Harsh, what is your opinion about paper companies like JK Paper, and West Coast paper mills? They appear to be cheap and I was wondering if I am missing something.

I like Satia Industries too at these valuations.

Please dont look at sales figure as its driven by gas sourcing business, which doesn’t drive profitability. You can go through the Aegis thread to understand key business drivers.

Lithium ion is a fast evolving space where its hard to foresee how future will play out. My bet on Amara is largely on their core business of lead acid batteries, which is going to be a major profit driver for the foreseeable future, and management’s focused intent on building their lithium ion business without bloating their balance sheet by outrageous capex spends. Just to give an example of this, Amara already does 100 cr.+ quarterly sales in the new business segment (FY23 sales was 250 cr.), and its profitable. At this rate of growth, in a couple of years this new business segment will contribute >10% to their overall sales, and will be decently profitable. And in terms of valuations, its very cheap.

It has done decently, YTD folio is up ~45% with deep value bets being up ~96%. I share the portfolio performance at the end of a year, and plan to continue doing that.

AR23 wasn’t very informative, but the previous ARs provided good insights on their product segments. Also, management talked about these things at the AGM, I still need to digitize my notes. Once I get time, I will share it on Geekay thread. You can see the product level breakup until FY22 below.

Once we are close to peak earnings in cyclicals, PEs start to look very low, but my observation in cyclicals has been that earnings collapse during a downcycle. In my understanding, the paper downcycle started earlier this year, with paper imports putting a cap on realizations. Also, paper cos had a huge tailwind in 2021-23 due to lower imports. I generally get interested when PB for paper cos fall below 1x, currently thats not the case for majority of paper cos.

Have you heared about this

https://x.com/Tijori1/status/1728254980929495372?s=20

Hello Raj

Nothing really right or wrong about any approach in selecting stocks … Idea should be to avoid landmines and even if you make mistakes they should be small mistakes …

all the best

Malolan

One of the questions which I have got repeatedly over the last 3.5 years of this thread is why I adopt a very diversified portfolio approach.

My thoughts

The key to successful investing extends beyond the sheer quantity of companies in your portfolio; rather, it hinges on the quality of your judgment in selecting investments. Without a sufficient number of decisions, it is impossible to discern whether the outcomes were a manifestation of luck or a testament to skill.

When one invests in small companies, the spectrum of potential outcomes widens significantly. In such a landscape, diversifying one’s portfolio across a broad range of bets emerges as a prudent strategy. This is an acknowledgment that individual investments may yield varying results, with some exceeding expectations while others may fall short.

Anyone interested in this, please look at the link below where Rajeev Thakkar shares his thoughts on small and midcap investing (time stamp: 13875).

Also, please note I am unwilling to engage in further dialogue about this.

The event was great (Was present there physically.) One this which i wasn’t able to digest was on why they don’t have investment in the Infrastructure … When there are good companies like L&T…!

Can you please share your thoughts on this @harsh.beria93

Coal india , Power Grid , is into infra or not?

Coal india as per them was a pure commodity play.

Power Grid was their “Power” theme based stock with the logic that Powergrid has business of transmission of power irrespective of hydropower or any elec.

My understanding of Parag Parikh MF house is that, they like to invest in companies which are simple to understand, with positive consistent cashflows and very low debt.

Since L&T has L&T Finance as one of its subsidiary, they will always have high Debt/Equity ratio at consolidated level. L&T is not simple business to understand with presence in Infra, construction/real estate, Metro, Finance and IT. That could be one of the reasons why there is no L&T.

Till 2021, there ROE at consolidated level was below 14 which was not comparable with some other businesses / large caps.

This is based on my understanding of Parag Parikh investment philosophy.

Hi Harsh,

This Thread is a gold mine to learn a lot from you.

I’ve seen Gufic in your portfolio for a while. What is the rationale behind this.

Thank You

Every investor has their own pecularity and style, they are free to do what they feel is right.

You can read more below.

Hi Harsh, What’s your view on PI with news of rainbow? Your study in agro is excellent. Thanks