There was a very good recent article from Morning context on Amara Raja. I am sharing the key points below.

-

Galla’s political career: has been vocal in his opposition to the Narendra Modi-led government and has close connections with Andhra Pradesh opposition leader and TDP president N. Chandrababu Naidu. In July, The New Indian Express had reported that he now wants to quit active politics and will not contest in the general elections in 2024.

-

Amaron has managed to bag the top spot in the replacement battery

-

Next generation of business leaders came in (two nephews of Javadev Galla, Harshavardhana Gourineni and Vikramadithya Gourineni)

-

Harshavardhana, 35, has spent eight years at auto component maker Mangal Industries—he also served as the CEO of the group subsidiary.

-

Vikramadithya Gourineni, 32, has worked at Amara Raja Power Systems (power equipment and project developer) and Amara Raja Electronics (maker of power circuit boards). Tasked with “new energy” business. He has been allowed to take on more risks

-

International: Boost share of international sales from 13.3% in FY23 to 50% in next 5-7 years, plans to gain a foothold in the US and Latin America. Do contract manufacturing for Walmart and Amazon to manufacture private-label batteries for the US and other region

-

Investing Rs 400 crore to setup a recycling unit that will recover 150,000 tonnes of lead—this will help the company meet 30% of its requirement every year

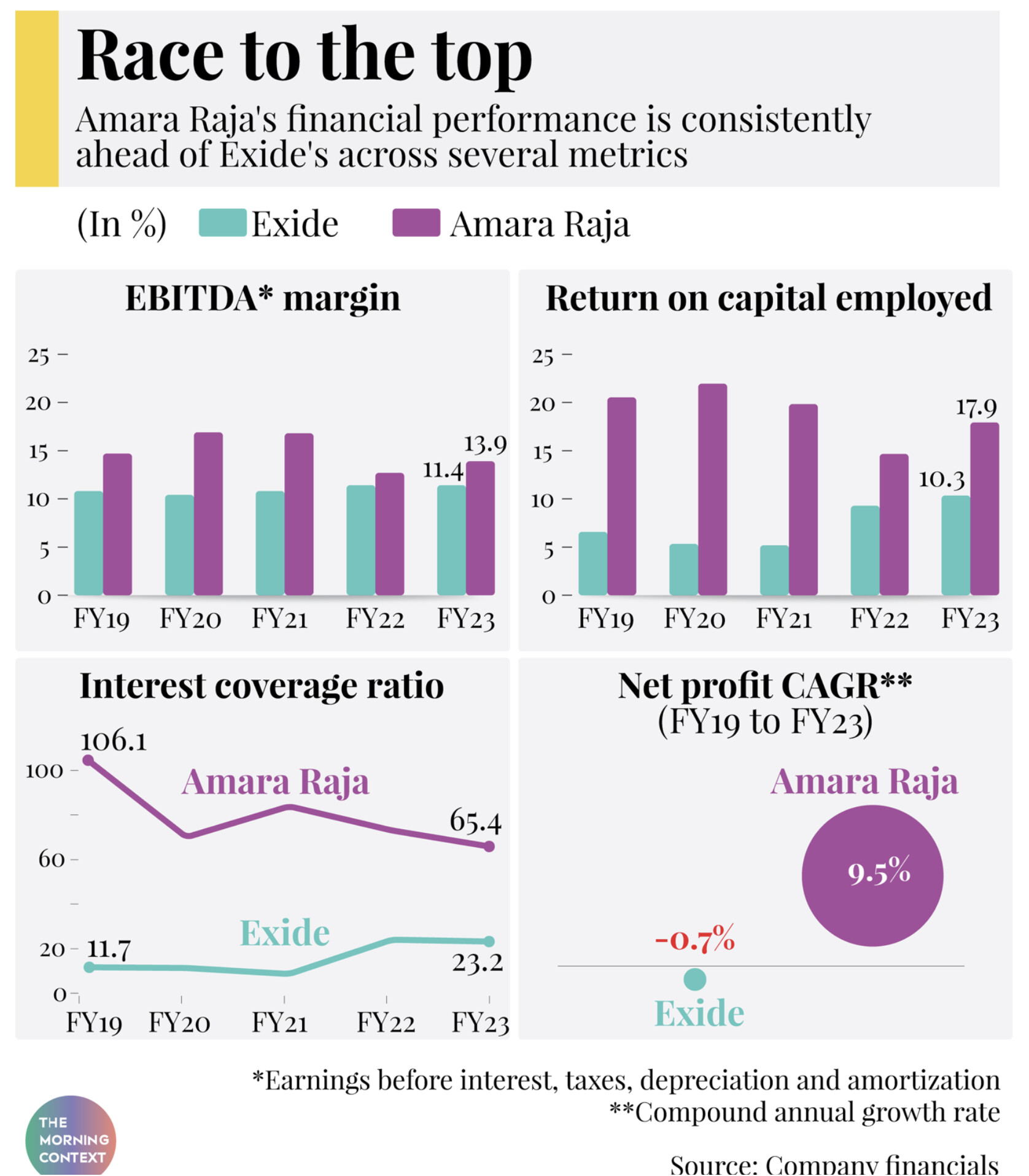

One key financial highlight between Amara and Exide (Amara scores higher on each possible metric)

Disclosure: Invested (position size here, no transactions in last-30 days)