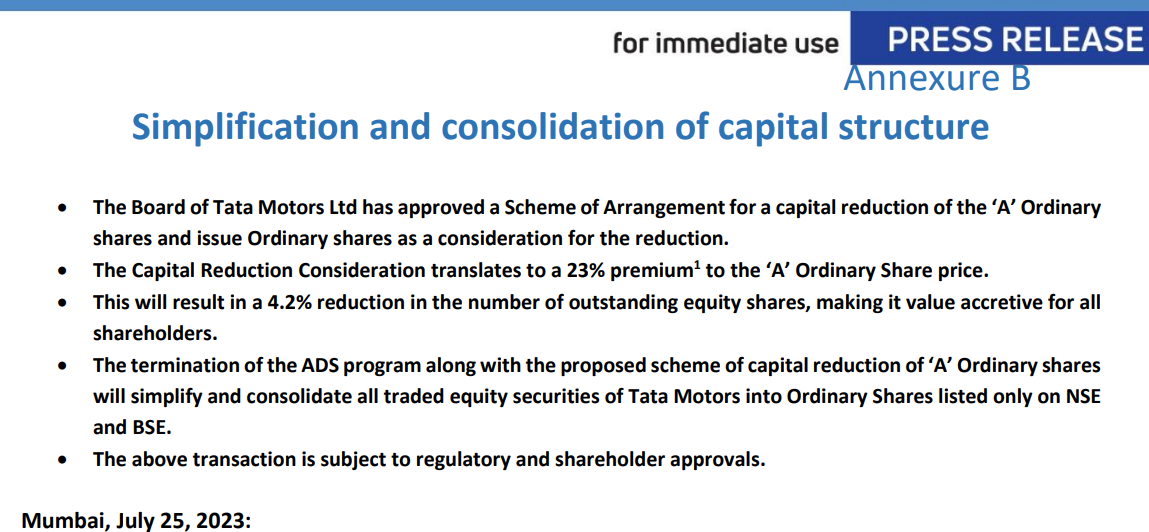

Looks like this handle will have a short remaining life. DVR holders to get 7 ordinary shares for every 10 shares held, roughly translating to 20% premium on currently traded price.

See the resolution here.

AJ

Disclosure: Remain invested in DVR and happy with this outcome. Views are biased.

8 Likes

Though it looks like a good windfall gain, but if one digs deeper it seems DVR shareholders are getting shortchanged.

In 2008 during Rights issue, when DVR was issued for the 1st time at 305; while Tata Motors shares were being issued at 340; so the differential then was only 10%; if we follow this ratio, DVR share holders should get 9 shares of Tata Motors for every 10 shares instead of only 7.

4 Likes

I didn know about that. Not something that you associate with a Tata Group company. For someone holding the shares from 2008 this is clearly unfavourable. Hope board relook into this and adjust the ratio appropriately.

AJ

2 Likes

Tsta motors is finally on path to grant divident… and once divident would have started the difference would have narrowed down to 10% [ max 20% ]. So as a dvr shareholder i am not happy with this. Expect ratio of atleast 8 or 9 … otherwise happy to remain as dvr shareholder

5 Likes

1 Like

Using this post to document my thesis for holding TaMO - DVR

(Other people have already written quality quantitative posts under this thread (eg: this one by @GourabPaul) - by repeating information I will pollute the thread and not add any value. Instead, I’ll write something that is not talked about a lot on this thread)

My reason: Value (even in this market).

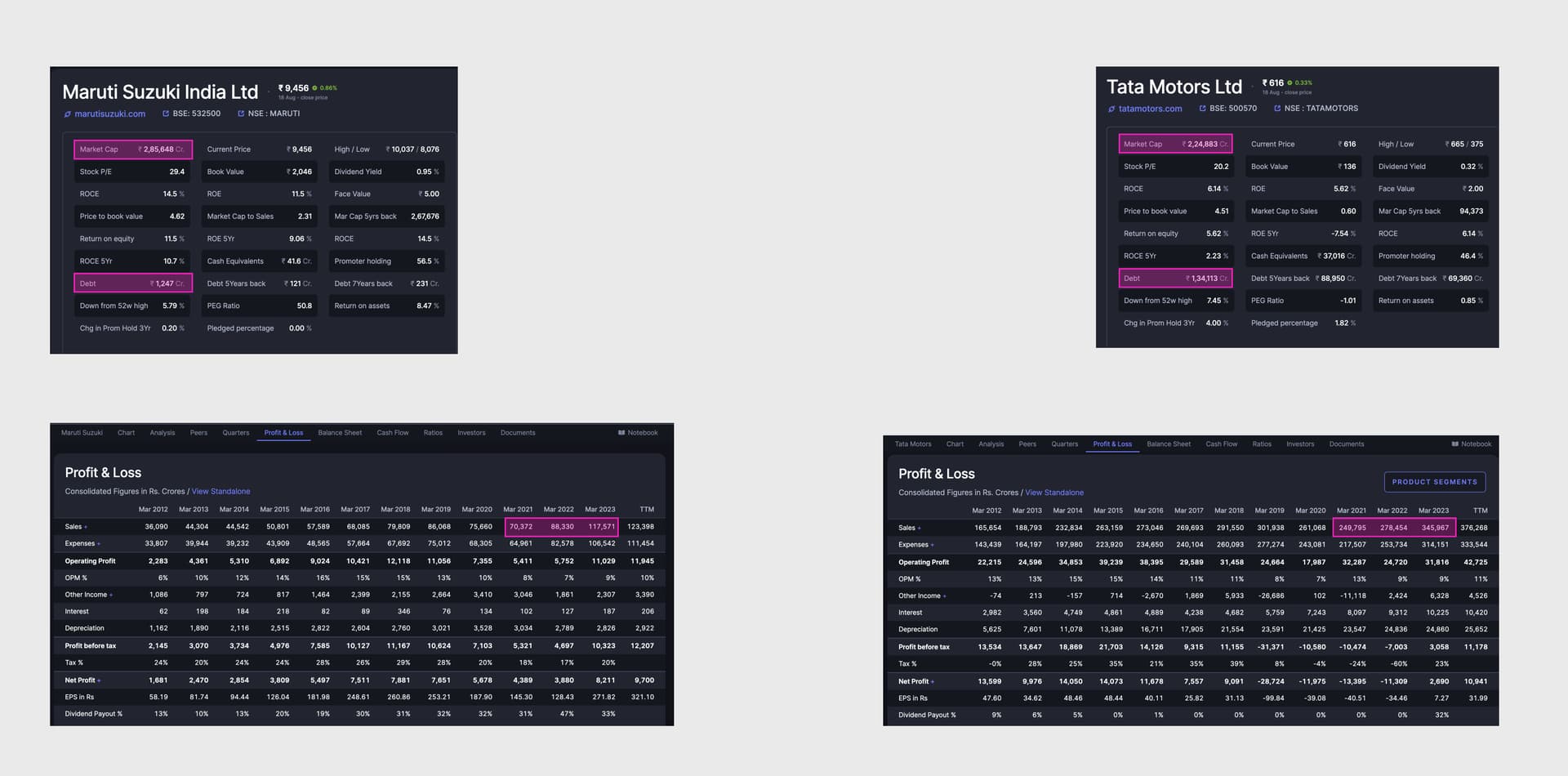

a) TaMo does more than 2x sales as Maruti but has a lower Market cap (+20k for DVR). It does more sales every year than it’s Mcap.

b) Imo, if the debt were to go off, the real numbers would surprise everyone. Can the debt go off? I believe they are doing the right things and the trajectory is in the right direction (again, not going to repeat quantitative information since there is enough of it in this thread).

Risks:

1. Hydrogen-powered v/s EVs: If somehow Hydrogen vehicle scales up, I believe that government would prefer/push Hydrogen over EVs (especially how China’s dominance in the EV value chain is). I am unsure how long can I hold TaMo <I’ll use this space to expand more as I find hard evidences (or) frame my mind>

2. Is another pricing war coming?: There are new manufacturers coming up (and most likely more will come up for EVs) which could eventually cause a margin erosion. Be it pricing wars in telecom or making the world’s cheapest car, the group’s history of failing at “good ideas” is not unknown. So once again, I have doubts about how long I will hold TaMo.

5 Likes

Nice observation.

Being in the industry for some time, I can negate hydrogen at the time being. The infrastructure is just not there yet. There are some fundamental questions which is yet to be clarified.

If OEMS were developing hydrogen passenger vehicles we would have seen software’s / Hardwires being build for the same. They would have gone through 6-7 years of validation cycle before being commercially viable.

As for competition, yes they would come and probably take away some market share, but what tata motors is doing by selling low cost EV , setting up the charging infrastructure, building EV components in Tata Autocomp is approach this as an ecosystem problem. I recently bought a Tiago EV and the main reason was the availability of charging infrastructure. No company is doing that at scale.

Also, another company that I have recently discovered is Divgi Torqtransfer. They sell the EV gearbox for both Tata and Mahindra. It is also an interesting company

Disc : Holding both.

9 Likes

Hi @GourabPaul Divgi appears to be an interesting business with very few competitors in their business. Their order book, financials, previous execution everything looks good but valuation is on the higher side. If you’ve studied this company, what’s your take w.r.t valuation?

Disclosure: I’ve a invested a very small quantity in Divgi for tracking purpose.

3 Likes

Tata Motors released the vehicle sales performance

JLR : https://www.bseindia.com/xml-data/corpfiling/AttachLive/7ef4f7b7-1877-4ad7-825e-d45f920851fa.pdf

Domestic Business: https://www.bseindia.com/xml-data/corpfiling/AttachHis/11c2c596-664d-4e41-9cbe-c05b355323d1.pdf

Though the PV domestic sales was a bit low, I believe it was because of their facelift variants of Nexon and other models. They are coming out with facelift versions, which are feature loaded and extremely well priced in my opinion.

What is exceptional is their JLR business which has sold 106561 vehicles (including china , Cherry JLR) and they have an order book of 168000 vehicles ( Q1FY24 - 185000 vehicles). They are able to produce 5000 vehicles per week , and had 2 week of planned shutdown this quarter at the plant.

Hi @Hemanth1121 ,

Yes Divgi I feel is a great business, but its fairly valued in my opinion. The strengths of the business

- EV Gearbox supplier for both Tata and M&M

- Virtual monopoly in the 4x4 space due to their torq converter portfolio

Current capacity can give them around 500-600 Cr of sales

Other drivers will be EV gearbox of 3 Wheelers. I will try to write more on the company and the product soon

Disc: Tata Motors is almost 22% of my PF and i am heavily biased.

9 Likes

Can someone guide if dvr shareholders will get Tata technology rights as is being considered for Tata motor shares

Individuals and Hindu Undivided Family (HUFs), who are equity shareholders of promoter Tata Motors as on the date of the filing of the Red Herring Prospectus with the Registrar of Companies (RoC), will be considered eligible for the initial public offering (IPO), Tata Technologies said in an addendum to its draft red herring prospectus (DRHP) filed with Sebi.

Read more at:

Technically speaking, DVR shares are restricted only with voting rights. Further detailed explanations can be given by experts on the subject.

1 Like

Any idea whether DVR shareholders will also get some shares of Tata Technologies?

Tata Motors to sell 9.9% stake in Tata Technologies for Rs 1,614 crore.

TPG Rise Climate SF Pte. Ltd will buy for 9.0% and Ratan Tata Endowment Foundation will acquire the balance 0.9% stake in Tata Technologies Limited.

Tata Motors currently has 74.69 percent stake in Tata Technologies Limited. The current transaction is made valuing TTL at INR 16,300 Cr (~US$ 2.0 billion).

Note that the share price of Tata Motors was up 4% today.

See the press release here.

AJ

Disclosure: Remain invested in DVR. Views are biased.

1 Like

16300 crore is the valuation based on March 31st. As of today the market cap of Tata Motors is 2,44,314 crores, so Tata Technologies valued approximate 6.7% of Tata Motors as per this. Am I correct? if we know what Tata Motors’s market cap as of March 31st we may get more accurate. Do we need to add Tata Motors DVR Market cap and other country listing also to see what tata Motors is worth as of March 31st and as of today? Experts, please clarify.

Disc: I am invested in Tata Motors DVR and biased.

Will Dvr shareholders be also eligible for Tata Technologies IPO. Can anyone please throw some light on it. Thanks

Hello Everyone,

I have a quick question for you. Let me know if this is practical.

The conversion ratio of 7 ordinary share for every 10 DVR is clearly not in the best interest of DVR holders and at a significant discount to origal issue price(which was at a discount of 10% from the then ordinary share price).

Is there a way the DVR share holders can raise protest against the current conversion ratio and get a better deal?

I believe the non-promoter, non-institutional share holders are a really small minority and voting against the motion will not have any impact on the overall results.

AJ

Disclosure: Remain invested.

1 Like

Tata’s are supposed to be minority friendly group and if enough noise can be raised in the media on the same, i am sure they would relent, afterall what is being asked is not really unfair!

On oneside if you see the shareholding is skewed towards large institutions

But retail shareholders absolute count has more than doubled in the last 3 years, thereby benefitting more small investors!

Stories can be formed! ![]()

1 Like