Tata motor price vs Dvr ratio fluctuates between 1.4 and 2.2 leaving out extremes the ratios are reverting to mean

The extremes offer arbitrage oppurtunity which smart investors utilise to earn less risky returns.

3 Likes

A Tata Motor DVR has 10% voting right as compared to an ordinary Tata Motor share. 1:1 (1 voting right per share.) 1:10 (1 voting right for every 10 shares held.)

Hence Tata Motor DVR trades at discount vs Tata Motors Share …

1 Like

Thanks. May I know how you calculated this ratio.

So, suppose if its reverting to mean which comes to 1.8, Either tata motors stock to rise up to 460 from 425 (CMP DVR 2551.8=460) or Tata motors DVR should correct up to 236 (CMP Tata motors = 425 = 2361.8). But which direction is it going to happen is my question? I sold my DVR shares today and bought TATA motors assuming it will go up to 460 levels. Lets see how it plays out. Would be a good learning.

Yes, that I understood it will trade at a discount always, but question was with respect to the correlation between the two. If price is rising both should rise, if price is falling both should fall up to same extent. Any discrepancy in this should create arbitrage opportunity as mentioned by @hkgupta in above comment.

I am a long term investor, though I exited in between and traded part of it…In the last 5 years.

What I noticed , if you believe that the stock should do well…The DVR goes up higher % than main tata motors. Opposite is true for correction. (Please see above post and few others posts above it)

Since DVR had better returns I’m short term , it is difficult to predict. But I think it should improve now, though still UK business still unpredictable and so many moving parts . But I believe under Chandra this juggernaut is turning slowly. So I am betting on the Chandra to turn it…For good considering this is one stock Tata Sons increased stake heavily in recent years.

Thank you @hkgupta. That’s an interesting take.

Do you keep a ratio tracker on long term or is there a way for me to see this on long run, to see if my thesis holds water…if yes, would you share…My thesis was in bear phase…Ratio widens and bull phase it narrows.

If there is a dividend of let’s say inr 2, both classes get similar dividends… So, a higher yield on the DVR shares (dvr shares get 5 percent extra dividend than the normal shares)

If there is a spin off or a demerger, both classes get the same number of proportionate shares.

Example. If the cv business or Tata motors finance business is spun off, theoretically, the value of the dvr shares will be the same as the normal shares.

It is long running arbitrage position

Since Tata motors is future traded when motor/dvr ratio moved beyond 2.15

I sold x no motor and bought 2x dvr. In anticipation of reversion to mean

I added more positions as ratio went up

Today it has comedown to 1.66

So squared up 25 % position

Shall be out of trade by the time ratio reaches 1.5

This is no suggestion to trade

Pls carry out due diligence

4 Likes

So if the ratio moves towards 1.5, you dont do the reverse trade? i.e., buying tata motors and selling DVR ? Reversal to mean should work in both the ways.

Dvr is not in futures

1 Like

Given the news for Tata technologies IPO, can we do mathematical modelling of what will Tamo shareholders get?

Anyone tracking current numbers of JLR and any views on it??

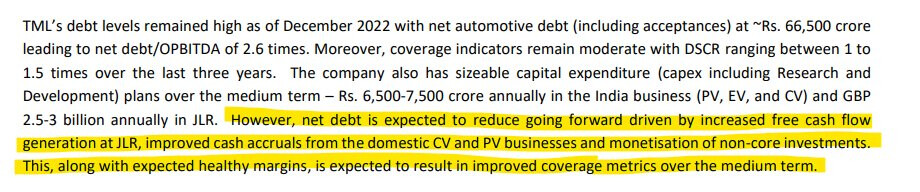

One of the best ways to identify a cyclical uptrend is the reduction in debt levels across the industry and improvement in ratings.

Look at how tata steel de-leveraged during Covid. Capex cycles are closely linked.

disc: we are invested & biased and this is not a reco

Ujjawal

Founder & CIO - WealthCulture

1 Like

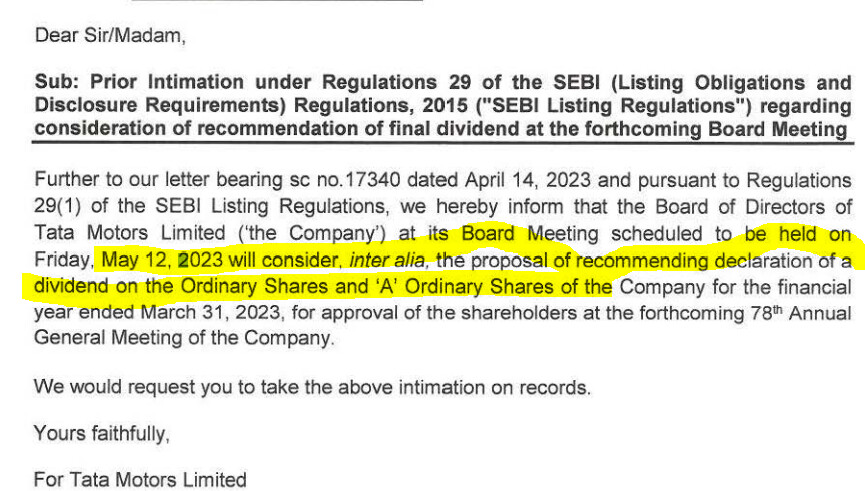

Tata Motors to conisider dividend as an agenda item on May 12th’s board meeting!

AJ

Disclosure: Remain invested.

4 Likes

Tata Motors weighs dividend after Dec quarter turnaround | Mint A report too in Livemint.

My thesis on tata motors for the next 1-1.5 year are the following -

Assumptions :

- The business will be in steady state for a while and margins can only improve.

- JLR has a very high order book of 152000 Vehicle and JLR is producing 2600 per week. So the JLR revenue has constant visibility till 58 weeks ( i.e entire 2024. This is also what the management is saying )

- They had a cumulative loss of 57 K Cr till now. so that loss will be offset with the profit that is generated hence I am considering a PBT instead of PAT of 4784 per Quarter. I am also considering the other income to be consistent. the forward PE for 2024 hence looks like (184715/(4784 *4)) = 9.65 .

So even if sales does not grow, debt reduction does not take place or margins don’t improve, the MCAP has the potential to double in the next 1 year. In FY 24 they will come out with large EVs which will have better margins ( Harrier and safari EV) . The PE of M&M is 20 . Also, I also assume we are not at the edge of a auto downcycle globally and in India for the next 1 year.

Disclaimer : 20% of PF and extremely Biased

9 Likes

2 Likes

Hello,

I’ve recently started reading the value chain of auto manufacturing. There are many good companies which caters to metal specialty engineering(I’m using this word broadly which can cover body building using different alloys, powertrain module, wiring and harness different things) which are listed in India. Does anybody know if there’s any company which manufactures infotainment ECU and display’s for OEM’s in india?

PS: I’m aware of DIS manufacturers such as Minda and Pricol. I’m aware of the the SW providers such as KPIT, Tata elxi and few others

2 Likes