Q4 concall

Performance

India Beverages, as I mentioned, volume growth of 3%; revenue, 8%

India Foods, volume 8%, revenue 26%.

US Coffee, volume was negative 20% (due to price hike) overall revenue was up 6%

International, ex acquisitions, volume growth, 3% and revenue growth ex acquisitions of 6%.

Tata Coffee 14% volume and 16% revenue.

Overall, consolidated constant-currency growth of 12%; reported, 14%.

Update

India Business EBITDA margins expanded by 90 bps during the year despite inflation in salt.

Free cash flow conversion from EBITDA was close to 99% (OFC/EBITDA)

At the company level, the EBITDA margin contracted by 50bps in FY23, led by steep inflation in the International business

the target was to hit 4 million outlets by September of ’23. We are at 3.8 million as of March,

Alternate channels

Modern Trade FY23 revenue growth 21%

E-commerce FY23 revenue growth 32%

Tea Market share in volume terms we were down 50 bps, value we were down 113 bps.

During the year, we gained market share in salt,

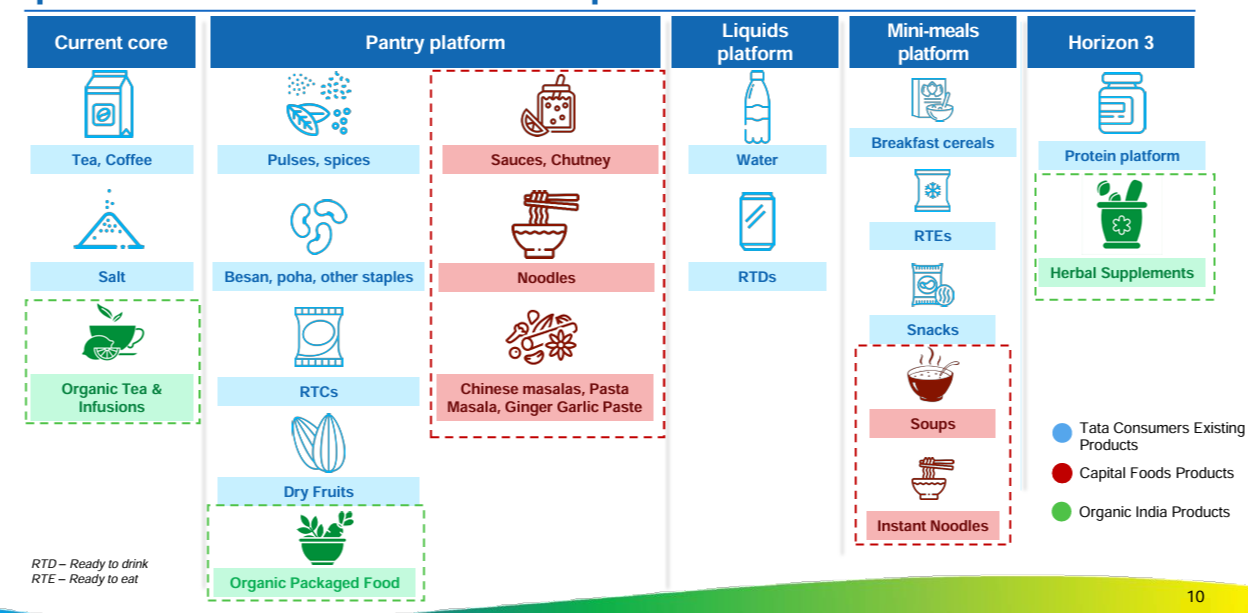

We have roughly doubled our launches compared to last year. And it’s not only foods and beverages, it is new categories including expanding Himalayan, and entering the protein space.

New engines of growth, moving beyond tea and salt, focus on Sampann, ready-to-drink, Soulfull, and the ready-to-eat, ready-to-cook portfolio.

Soulfull doubled in revenue last year.

Tata Sampann full-year growth being 29%.

RTE/RTC, we are slightly behind on our timelines, but now the international expansion, which is key on this business has picked up.

Starbucks, scaling rapidly tenth year. we crossed the INR1,000 crore mark. We added 71 stores, which is a record for Starbucks. We are now in 41 cities and 333 stores now nationally.

Salt volume growth of 8% and revenue growth of 26%, market share was 76%.

NourishCo, 80% revenue growth and Tata Copper is 2.2 times of its size.

Tata Coffee overall growth 11%

Q&A

International buz margin will come back to the historical level comming q1 or q2 due to increasing price and structural cost action

in Tea buz we are weaker in the South, stronger in the North

1.5 million direct distribution (outlets) as of now

total reach 3.8m target 4m by sep23

ebitda margin in starbugs

historical gross margin in salt buz between 32 to 37 % and we are more or less in the rage right noe

we do expect both tea and salt businesses to grow mid-single digits in volumes.

NourishCo side 3 year back presence in orissa andhra telengana and tamil nadu if u see now we are preset in 75 to 80% of the country

180 cr to 600 cr in three years targeting 4 digit revenue by 24 and focusing of expandig distribution

We expanded manufacturing footprint by 2x to 2.5x last year

So Starbucks according to Ind AS reporting, we are EBITDA positive and EBIT positive and statutory reporting according to that, the net PAT is negative.

rapidly expanding stores interest and depreciation front.

NourishCo we have two different distribution systems. One is the value and one is the premium end

The value portion is primarily the Tata Copper and Gluco Plus.

The premium end handles the Himalayan part of the portfolio, which is very specifically targeted to high-end on-premise accounts.

As crop goes up or down and prices go up or down we will keep moving our prices to make sure that, A, we are competitive; B, we are delivering margin; and C, we’re continuing to drive volume

growth and market share.

what would be the drivers of this margin improvement in indian business

EBIT margins would be driven primarily by volume growth while keeping costs under tight control

salt kind of margin improvement, if the RM Index goes down

Indian tea business

we are about 10% to 12% behind on distribution and also on market share (while comp to large comp)

we have to close this distribution gap by 10% increasing distribution

rural Tamilnadu.

Eastern UP

some parts of Maharashtra

by September