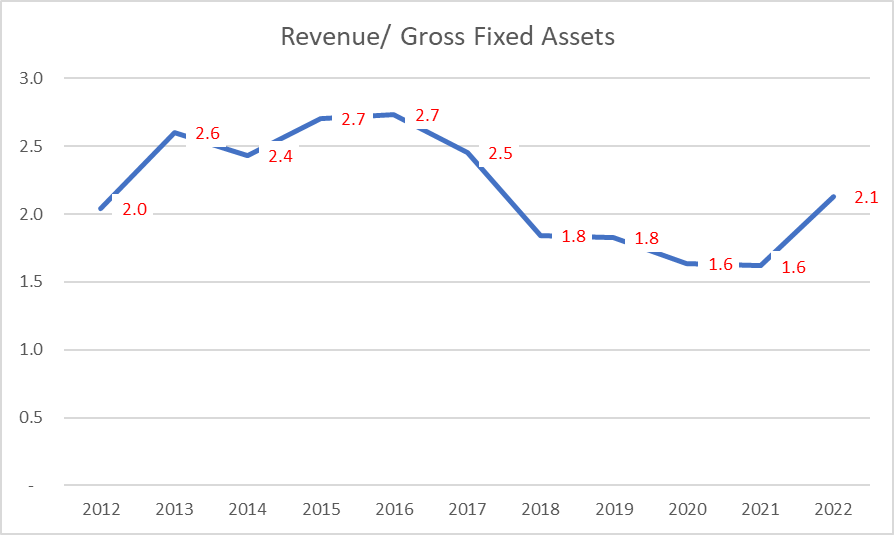

One thing I am unable to understand is that if you look at historical Revenue/ Gross Fixed Assets, they have ranged in the range of 1.8 on the low (ignore COVID years) and 2.7 on the high. The current Gross Block is INR 310 crs. Planned capex over next couple of years is INR 40 crs. That takes the Gross Block to INR 350 crs. If I apply the peak Rev/ GFA of 2.7 to this, the revenue potential from this asset base is INR 945 crs only. However, the management says that they can reach a revenue of INR 2000 crs with this Gross Block of INR 350 crs. That implies an Rev/GFA of 5.7. This looks way high relative to it’s own history as well as relative to the peer-set. What am I missing?

6 Likes

The 40 cr is to automate the entire production especially the lamination part on their various products.This will enable the company to reduce the time taken to produce, store and pack the products significantly.So they should be able to produce much more on the same asset base leading to operating leverage kicking in. You can think of it as improvement in manufacturing technology hence the earlier Rev/GFA does not apply. I have experience working in this industry hence can understand this change. One can youtube videos of automated laminated plants and semi-automated ones the speed of production will be quite evident .

On the point of peers, I believe greenlam also announced it will be doubling its capacity using similar technological advancements. Quite a few prominent investors bought more share of it after their announcement.

5 Likes

The operating leverage is to the extend that asset turns will be 5.7 times. This is very unusual for any industry. I think we should find comparable peer in Europe and compare asset turns.

Disclosure - Not Invested.

1 Like

You are right having revenue/Gross fixed asset is high will try and find a suitable company in a developed country .

Just to point out we were talking about revenue to gross fixed asset.

Asset turnover will include investments in working capital and inventory such which will increase the overall asset base by a lot if the sales go to 2000 cr. Doubt the overall Asset turnover will go above 3 ever sustainably .

3 Likes

Stylam Industries Q3 results highlights -

One of the fastest growing companies in high end decorative laminates and allied products category

First company in India to introduce PU+Lacquer coating process for laminates

Operate Asia’s largest laminate manufacturing plant

Added facilities for lamination of MDF boards

Aprox 66 pc of revenues from exports

Current laminate capacity at 14.3 million sheets/year

Q3 financials -

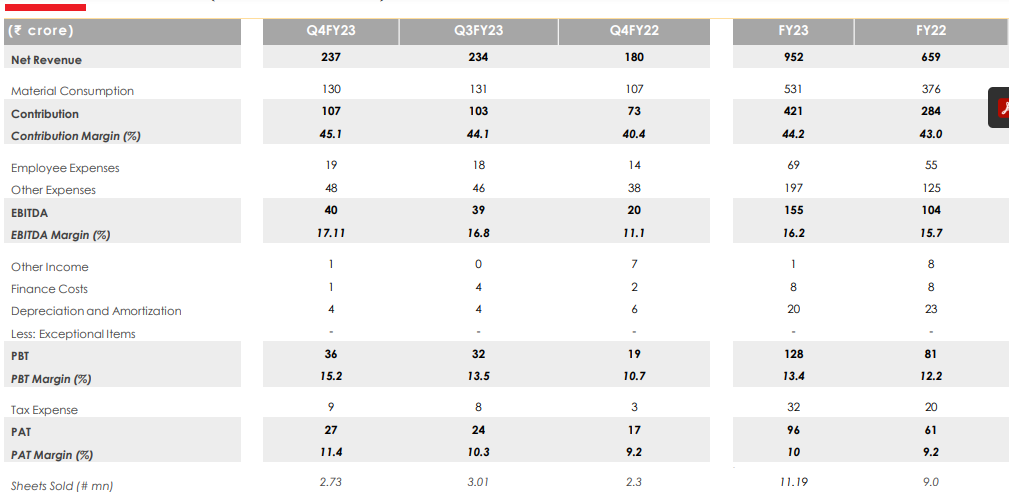

Sales - 234 cr vs 177 cr

EBITDA - 39 vs 33 cr, Margins at 17 pc vs 19 pc

PAT - 24 vs 16 cr, Margins at 10 vs 9 pc

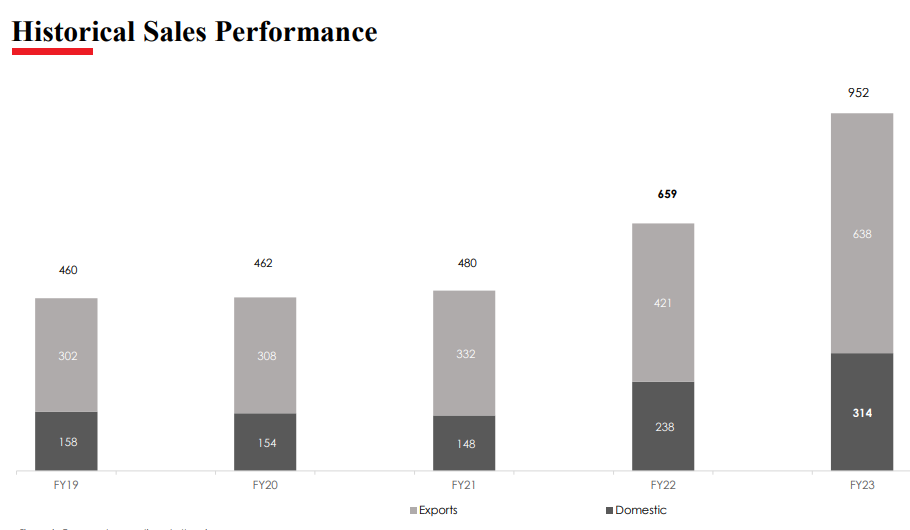

Last 5 yrs sales data -

338 vs 460 vs 462 vs 480 vs 660 cr ( no major dips despite COVID disruptions )

Last 9M sales at - 716 cr

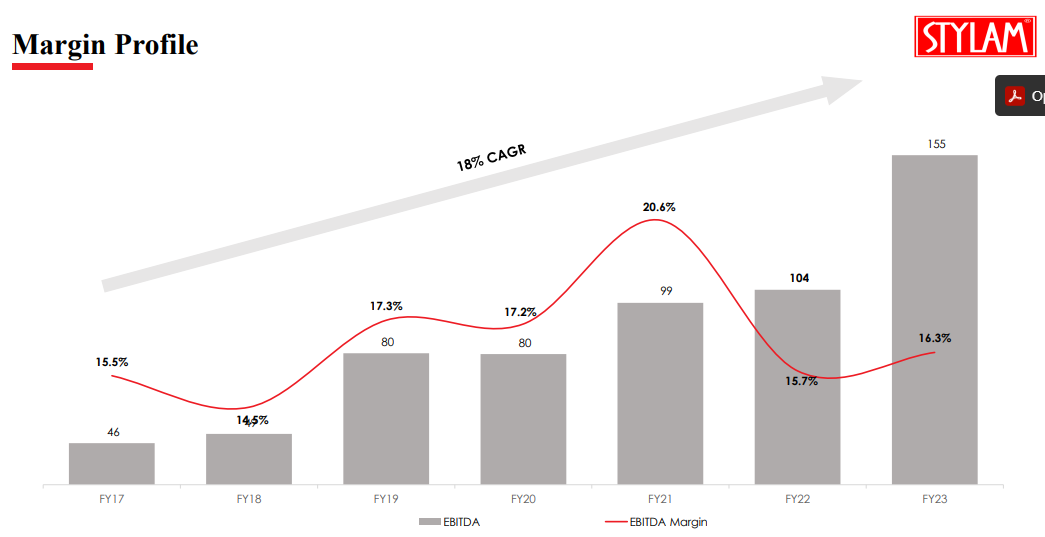

Last 5 yrs EBITDA margins -

14 pc vs 17 pc vs 17 pc vs 21 pc vs 16 pc vs 16 pc ( for last 9 months )

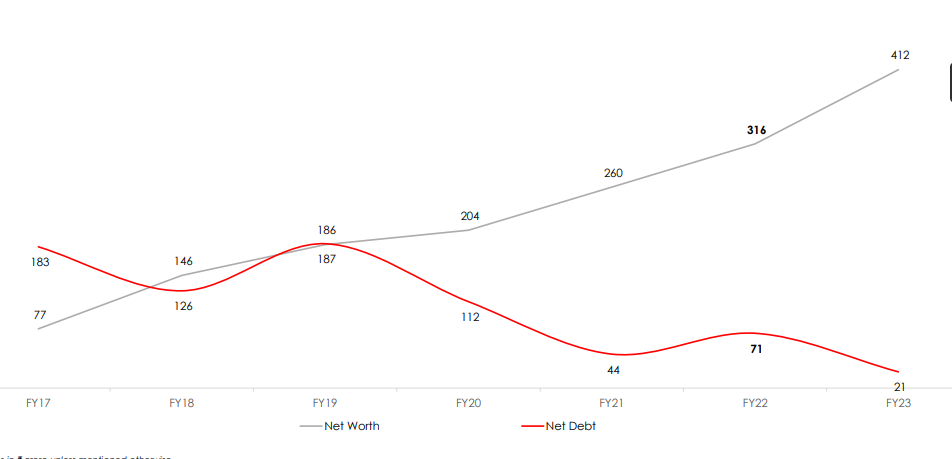

Debt down at 71 cr vs 183 cr in Mar 18

India’s first company to set up manufacturing facility for Solid Acrylic surfaces - a higher margin product

Q3 sales were lesser by 2-3 pc due logistics issues faced for supplies to Russia, Uzbekistan

Company clocking 80-82 cr sales in India for last 3 Qtrs

Hopeful of clocking 325-350 cr domestic sales by Mar 23

Acrylic panels clocked 7-8 cr of domestic sales. Its an import substitute, new product. Company hopeful that this number should grow manifold in medium to long term

Margins likely to improve in Q4 due reduced RM prices

Hopeful of getting to 20 pc + EBITDA margins by Q1 FY 24 due reduced RM prices

Current capacity utilisation at 80 pc. Maint, Automation and Modernisation capex planned for Rs 30-40 cr ( @ 10 cr/year for next 3-4 yrs ). Should improve capacities by 30 - 40 pc

Depreciation and Interest expenses reduced in Q3 due reduction in debt and completion of depreciation of some assets

60 pc of exports are branded sales. Rest are to OEMs like Thyssenkrupp who use company’s products in their elevators

Company seeing growth in exports despite economic slowdown due Mkt share gains and greater acceptability of Made in India products

Confident of clocking 15-20 pc toppling growth next year as well !!!

Hopeful of selling Rs 14-15 cr of Acrylic panels in Q4 vs Rs 7-8 cr in Q3

Company’s Acrylic boards have a sale potential of Rs 300-400 cr in next 2-3 yrs. This yr sales are likely to be around 30-32 cr. The growth in this segment can be huge

Expect Q4 to be better than Q3

Disc: holding, biased.

Company’s shares are also held by Sunil Singhania in his Small Cap PMS portfolio

7 Likes

good q4 results.

yoy growth of 27% in revenues

yoy growth of 61% in PAT.

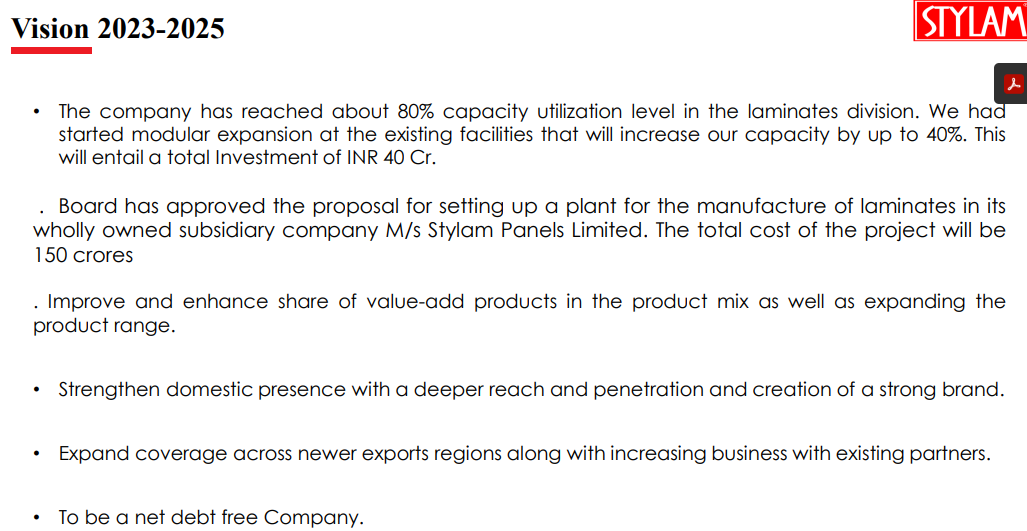

company plans to invest 150 cr in a laminate manufacturing capacity.

growth visibility in domestic seems to be very strong.

Disc- Invested

3 Likes

Notes from Q4 Concall. The line wasn’t very clear, so there may be some inaccuracies in my notes, please go by transcript when its released.

Q4 FY23 Concall

-

Acrylic solid surfaces

- Q4 revenue 9Cr, says EBITDA breakeven already (Doubtful about this)

- April turnover 4Cr

- Exports possible

- Going to participate in an exhibition in Germany

- Have filed for anti-dumping duty on acrylic SS imports

- Quality on par with Korean imports

- Exports to Israel, Philippines etc.

- Peak revenue capacity is 400Cr - 500Cr

- FY24 revenues next year should be > 50Cr definitely (Otherwise plant should be closed down)

- Margins maybe similar to laminates

-

Laminate exports

- No challenges in global demand outlook

- Current capacity utilisation is 75-80%

Employees – 8 to 9 only, no offices, no marketing needed (How are they selling 60% branded in export markets then? Who/what is driving the brand?) - Domestic market – 150 sales people; Don’t see much manpower addition in domestic sales biz

- New Capex plan announced

- Existing land

- Going for new value-added products – new sizes etc

- Focused mostly on export markets

- 150Cr expenditure within this year (99%) – targets to start operations by March FY24

- Entering High pressure Laminates – turnover will be 500Cr at max utilisation

- Same location as existing integrated plant

- Says capex will happen via internal accruals (How? CFO is 66Cr and cash on books is 27Cr)

- Margins should be better than existing laminates biz (Less competition)

-

Existing laminates capacity - After existing plant 40% expansion total revenue capacity will be 1200-1300Cr

- 20Cr already spent, 20Cr will be spent further in FY24

- Stylam is growing in South India faster (40-45% YoY growth in South India)

- Revenue growth for next 2 years – targeting 20-25% growth every year; Margins will improve as sales scale up

- Says 100-150bps overall margin expansion should happen YoY in FY24

- Q4 domestic vol – 12L, export 15L

- FY23 domestic vol – 45L, export 56L

- 150 member domestic sales team (What was the no last year?)

Disc: Invested

12 Likes

Building on Nirvana’s post, here are my notes from their call. Company continues their strong growth trajectory with sales growing by 32% and EPS by 63% in this quarter. Management seemed very confident of delivering 20%+ growth going forward.

FY23Q4 concall

- Targeting 20-25% sales growth, margins will improve with scale

- Existing laminate capacity can gives 1200-1300 cr. revenues (including capex of 40 cr. out of which 20 cr. was spent and remainder will be sent in FY24)

- Approved proposal for setting up a plant to manufacture laminates for 150 cr. in wholly owned subsidiary company (Stylam Panels Limited). Can contribute 500 cr. to revenues (mostly for exports). These will be higher margins

- Quarterly exports are showing a declining trend (from 169 cr. in Q1 to 151 cr. in Q4) because of reduction in ocean freight component, there is no volume decline

-

Acrylic:

o 4 cr.+ revenues in last month, 9 cr. in Q4FY23. Next quarter acrylic sales will show a step jump

o Should be able to reach 50 cr. in FY24

o Installed new machine last quarter

o Capacity is for 400-500 cr.

o Margins maybe similar to laminates - Laminate: 75-80% utilization

- Have not seen much impact of recession in sales in Europe (especially in high value add laminate)

- US contribution is currently 4-5%

- Marketing: domestic 150 sales personnel (no need for further addition) + export 8-9 personnel

- Growing faster in South India (40-45% growth)

- Margin should expand by 1-1.5% in FY24

Disclosure: Invested (position size here, no transactions in last-30 days)

14 Likes

Really, difficult to digest that their 60% branded business with just 7-8 employees.

Anyone in laminate business can throw more light about their actual business.

Disc…invested

2 Likes

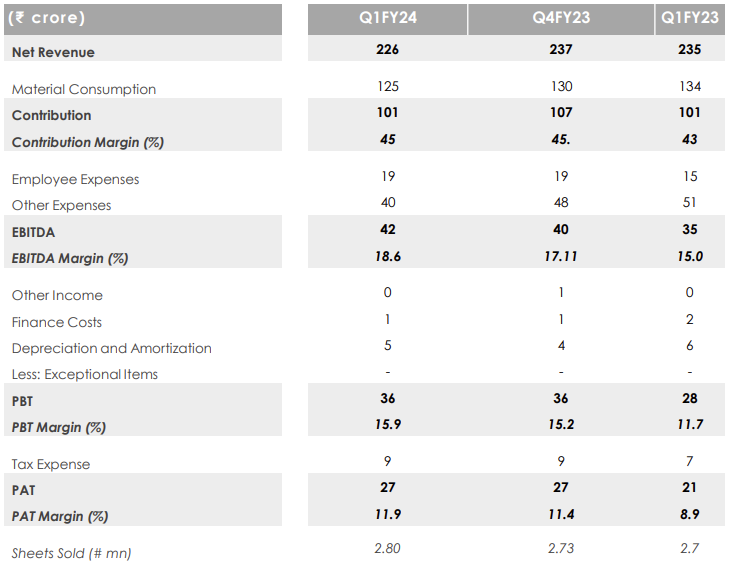

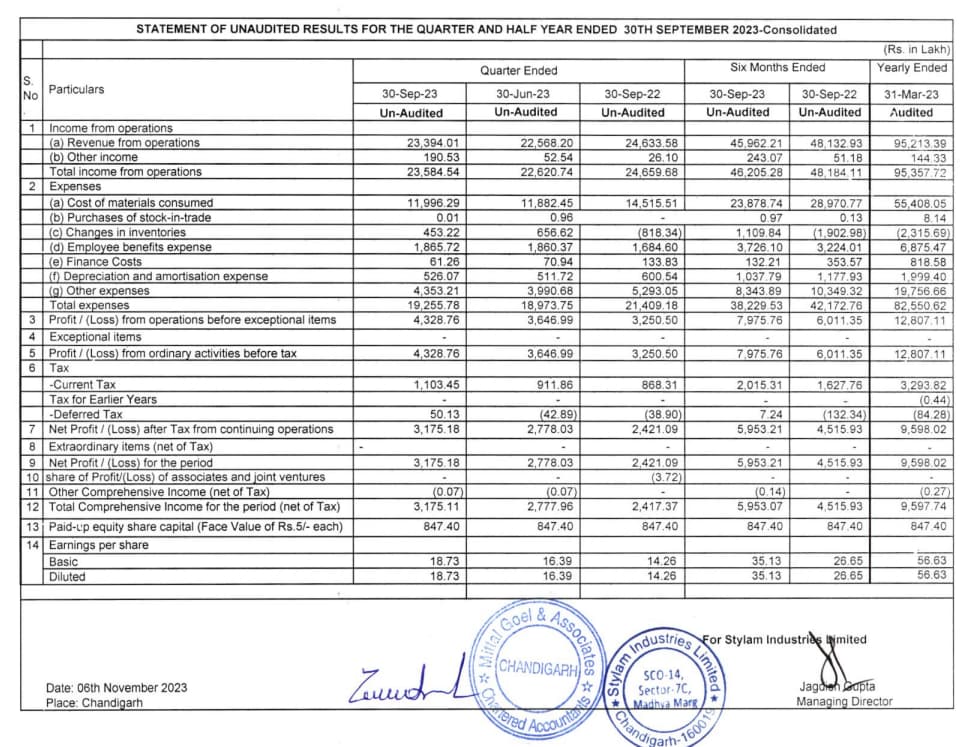

Stylam clocked sales of INR 226 crore in Q1F24 quarter, with slightly decline of -3.96% YoY .Sales decline during the quarter was primarily by exports, which were INR 149 crore (-11.83 % YoY decline). although domestic sales witnessed significant uptick, clocking sales of INR 77 crore (16.7 % YoY).

The Company sold 2.8 million laminate sheets during the first quarter of Q1FY24 (vs. 2.7 million in Q1FY23; a 4 % YoY growth). Per sheet realizations vary based on the product mix during the period. Contribution margin has remained stagnant same as previous quarter and now stands at 44.69 % for Q1FY24 (vs. 45.1% in Q4FY23). Further, EBITDA for the quarter stood at INR 42 crore. In terms of margins, it stood at 18.51% (vs. 17.11 % in Q4FY23 and 15.03% in Q1FY23).

30% YoY PAT growth on margin expansion

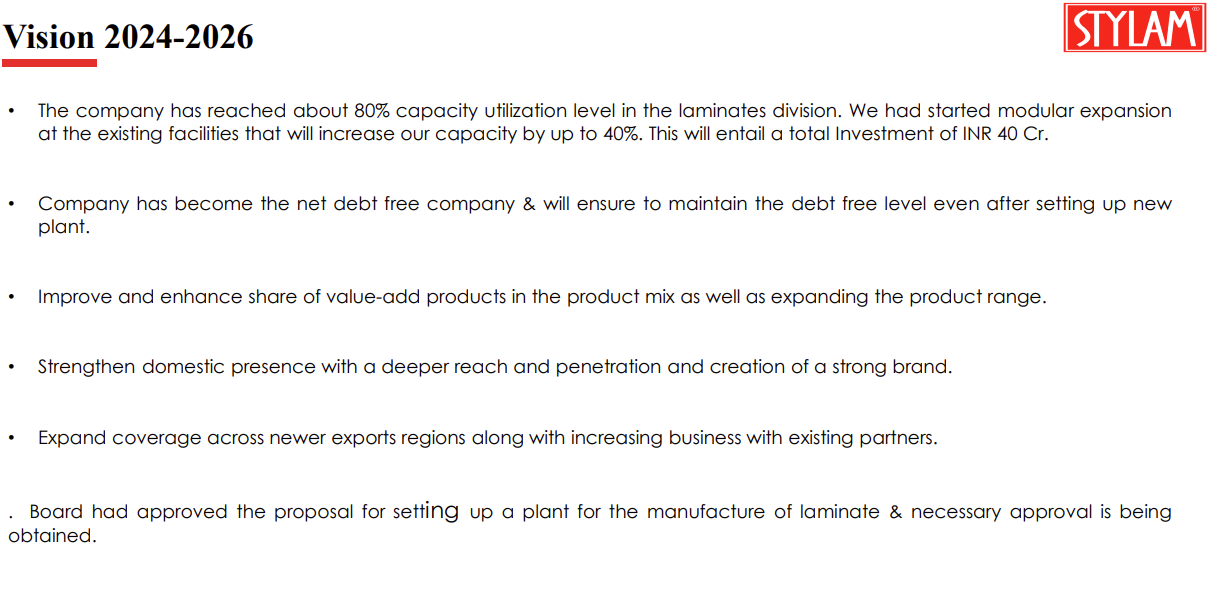

Stylam has improved its working capital despite adversities; the cycle stands at 92 days for the first quarter (vs. 93 days for Q4FY23). Net debt stood at INR (-)27 crore as on 30th June 2023. Net worth stands at INR 440 crore.

1 Like

Company saw further revival in margins along with muted sales. Sales declined by 4% because of 12% drop in exports, countered by 17% increase in domestic revenues. Management is guiding for further improvement in gross margins, export demand is currently a bit tepid. Concall notes below

FY24Q1

- Reduction in ocean freight will have ~20 cr. impact in FY24 (impacted by 6-7 cr. in Q1)

- Existing capacities can support 1500-1800 cr. revenues

- Domestic volume: 14.2 lakh sheets (growth of 42%). Has lower realization vs exports (was 475 vs 660 last year; my own computation and it maybe because of product mix).

- Export volume: 13.8 lakh sheets (decline of -19%). Realization increased from 994 in Q1FY23 to 1080

- Expects GM expansion next quarter onwards (because of reduction in prices of chemicals)

- Acrylic: 9.5 cr. in Q1 (no operating losses). FY23 revenues was 21 cr. (12 cr. domestic + 9 cr. exports). Has setup a second line. Expect 40-50 cr. contribution in FY24. At full utilization of the 2 lines, can do 350-400 cr. revenues (produce 6mm and 12mm thickness). Stronger in South India

- Laminate Capex: 125-150 cr., will finish in 10-12 months (have applied for government approvals, so can get delayed). Expect revenues of 400-600 cr. depending on product mix. With this capex, they can reach potential topline of 2000 cr.

- Export volumes will revive by expansion into North and South America

Disclosure: Invested (position size here, sold shares in last-30 days)

4 Likes

Source https://www.bseindia.com/xml-data/corpfiling/AttachLive/ed3a59d7-e6ba-40c4-807e-57f3587f5000.pdf

2 Likes

Stylam-update from credit rating 2023 and concall

STYLAM

1…Capex

A…40 cr@For modernization and automation of plant that will increase capacity @ 10-20%

B…Rs 125 crores to Rs. 150 crores.

=The company has reached about 80% capacity utilization level in the laminates division.

=Board had approved the proposal for setting up a plant for the manufacture of laminate & necessary approval is being obtained

=We have already started, architecture, land is already with us. We have applied for government

approval. We are quite hopeful that we will complete this project maximum within 10 months

to 12 months from now onwards.

2…We recently received a Certification from NSF International, USA for our Solid Acrylic Surface products

=NSF International, USA recognized and certified Stylam authorizing the

Company to bear the NSF mark.

3…Domestic business.

=We are growing, some slow growth is happening in major brand every

quarter there is increase in the sales.

= That we are doing, we don’t know about 3 years, but we are quite hopeful that things are going better in long run

4…Acrylic business

=Last year we did a total sale of Rs. 21 crores in full year.

= 9.52 crores Acrylic sales in Q1

=It will take longer time for significant revenue from acrylic segment.

Disc…invested

1 Like

Sorry what concall is this? Q2 results aren’t out yet right?

1 Like

Is company not having concall for Q2 this time ? Need to understand the guidance on sales growth as seems company has consistently underperformed on sales growth for last 2 Qs with respect to the initial guidance

The company gave guidance that growth will slow down due to macros but margins will improve due to commodity prices stabalizing. This is actually very much in line with the guidance.

4 Likes

Cant find the Product wise breakup and also the sales volume annually, which Century and Greenlam do give ?

Stylam came with lower sales (-8%) and improved margins leading to good growth in EPS (30%). They are facing headwinds in domestic markets and in Europe, and are very bullish on USA exports. Concall notes below.

FY24Q3

-

Lost 20 cr. sales due to Israel war. Shipments to Europe affected, not much impact on USA exports

-

Strong visibility with healthy enquiries for sourcing from global OEM (added many new OEM customers)

-

Greenlam has global offices and Stylam doesn’t have any global office

-

Expect US to become larger than Europe. Europe is currently very slow

-

Domestic laminate business is taking time to scale up fast due to stiff competition. Have been weak in domestic markets

-

Acrylic:

-

5.4 cr. in Q3; 20 cr. in 9MFY24 (11 cr. domestic + 9 cr. exports). Utilization level is <10%

-

Focus has been to sell under own Granex brand vs OEM sales which has delayed scaleup

-

Expect Government to impose antidumping duty on imports of acrylic surface from China, and this will be a huge boost for them (700-800 cr. annual imports)

-

-

Capex

- 150 cr. brownfield expansion is now increased 200-250 cr. (added one more production line from 3 to 4 now). Likely operational in 3QFY25. Revenue potential is 600 cr. (vs 500 cr. earlier) and expect a fast scale up as ~50% capacity is already booked from export customers

Disclosure: Invested (position size here, no transactions in last-30 days)

8 Likes