Feel they need to devise a strategy to establish a brand for the domestic mkt. Don’t think they have found much success yet, only once that happens i think mkt will give it a premium valuation.

Good part is they’re net debt zero now, new capex to come onstream by H2FY25.

1 Like

Japanese laminates major Aica Kogyo looks to pick stake in Stylam Industries. This news has lead to increase in share price recently. Any views for the purchase?

3 Likes

@rupaniamit since you track US real estate market closely (my assumption based on your work on Pokarna)

How do you see below product will impact Pokarna / Acrysil ?

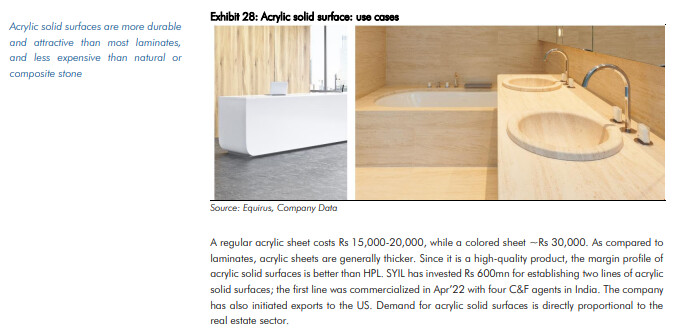

Note : This is a slide from Equirus - Stylam latest report.

- From the report I can see they make laminates for external cladding as well

About 7 years ago there was major incident in London

Government passed a law to replace all cladding (non fire resistant ) for all the apartments, there is some funding also allotted by the government. At this moment one cannot sell a property if the flat has cladding . If you have any insights about this subject please share your thoughts.

Many Thanks

2 Likes

Thank you for sharing this new product of Stylam.

Countertop material decision is driven by use-case and price difference between the alternatives.

Quartz really made its inroads and started replacing granite on a bigger scale when the designs of Quartz started matching and improving that of natural granite while the pricing difference also came to a level where user was ready to pay up for that upgrade. Long time ago price difference between granite and quartz was so huge that Quartz was considered a luxury countertop.

This acrylic solid surface product might find its applications in hotels (extended stays), rental properties, apartment complexes, hospitals, businesses, etc. I don’t think it can make inroads in residential houses which are mid grade and above.

One needs to dig through the price difference between laminate solid surface, acrylic solid surface, quartz, and granite to better understand the value migration and size of opportunity.

Once we understand the price difference (including final application project cost), only then we can have a view on what level of impact it can have on Pokarna, Acrysil type of businesses.

7 Likes

EBITDA margins contracting from peak of 20% and stagnant revenues. A worrying sign for profits and stock performance

1 Like

Thanks Anant for sharing. How do you see Promotor (Jagadish Gupta) and Director (Manav Gupta) offloading total of 5.5% stake last quarter. This is especially at a time where the outcomes of major expansion are at horizon?

Also, Manav Gupta’s (Director) holdings is disclosed under ‘Public’ and not ‘Promoters’. Any reason why?

And no exchange disclosures were made as well to the exchange regd the stake sale.

Request someone to explain the dispute within the promoter family. The management kept reiterating that domestic business is not growing due to internal issues and is looked after by his nephew manav gupta. Someone knows the details?

4 Likes

I am also eager whats the problem in management. last concall not sounds good .

2 Likes

STYLAM INDUSTRIES:

AICA KOGYO AIMS TO ACQUIRE A CONTROLLING STAKE (51% OR MORE) IN STYLAM INDUSTRIES.

Disc…invested

1 Like

Japan’s AICA Kogyo set to acquire 40% stake in Stylam for Rs 1,525 crore. There will be an open offer at INR 2300.

3 Likes

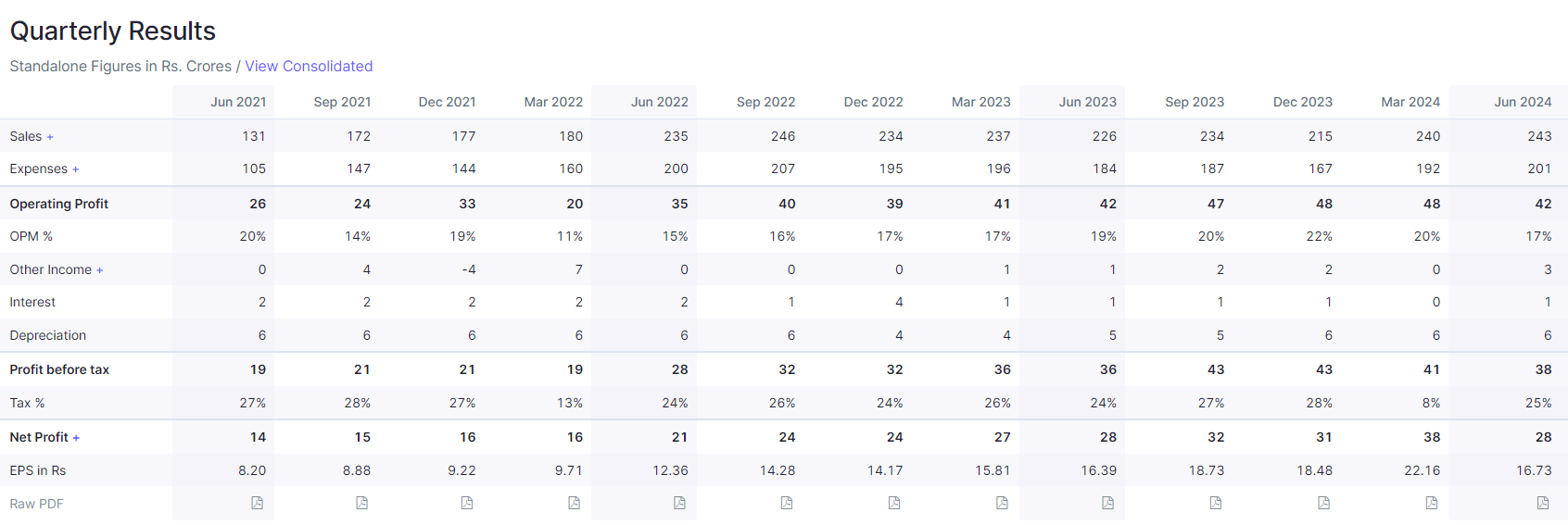

Rev - Quarter ended 31st December**, export turnover stood at Rs. 198 crores** compared to Rs. 185 crores in Quarter 3 of 2024 - 2025, registering a growth of 6.75%. Export amounting to approximately Rs. 617 crores against Rs. 543 crores in the corresponding nine-month period ended December 2024, reflecting a growth of 14%. Quarter ended 31st December domestic turnover increased to Rs. 72.89 crores from Rs. 68.97 crores in the corresponding year, reflecting a growth of 5.68%. Nine-month ended; domestic turnover rose to Rs. 229.5 crores compared to Rs. 217 crores in the corresponding period of the previous year, registering a growth of approximately 6%. Despite raw material cost pressure, our EBITDA margin improved to 20.51% for the quarter ended December 2025, compared to 18.07% in the corresponding quarter of the previous year. For the nine-month period ended December 2025, EBITDA margin stood at 19.51% against 18.72% in the corresponding period of the previous year.

Capex - Work on upcoming manufacturing facilities processing well and remain on track for commissioning by March 2026. Total planned investment for this project stood approximately Rs. 320 crores including GST, out of which approximately Rs. 227 crores has already been deployed.

Q on Ramp up New Plant Post Commisioning - if you talk about capacity-wise in laminates, in square meter, it will be around 10 to 12 million square meter a month, the capacity we would be having after the new plant comes in. Secondly domestic, as we said, it is a very huge market for each and every product. So, we are hoping in the next two years that we would be able to utilize 80% plus or 85% plus capacity of the new plant. Revenue wise, Rs. 1000 if we utilize all the 4 presses with full capacity and Rs. 700 crores would be the minimum.

Q on Addl Capex Plans - But definitely other products, what we are talking, to multiple companies, which we were not able to do so for the past one year due to this family issue. There are two or three multiple plants which we have already studied and discussed. So, hopefully, we might be able to give some news in the next two, three months about our expansion plans.

Q on AKCL Partnership - With this Japan partnership, we will gain access to advanced technology used in the Japanese market as well as benefit from their strong export capabilities and dominant domestic presence in Japan. They will remain a strategic partner while we continue as promoter directors, and they have expressed full trust in our management. Their involvement will mainly be for major expansion decisions, while Manit took over last month and continue to manage the domestic business and operations. (Manav Exited who was Reason for Domestic flat rev)

Q on Change in Mgt Domestic Business - The domestic market was earlier handled by Manav for several years, so it may take one to two quarters to fully stabilize operations. We have already started restructuring by reducing excess manpower and strengthening the sales team, and we aim to achieve a top-three position in the domestic market over the next two to three years.

Q on Acquisition Happened - They have already bought Manav’s share (incl Pushpa & LAtha), which is 27%. And then comes the open offer of 26%. So, if 27% plus 26% comes to 53%, which they are obliged to buy. It depends whether they get that number of shares or number of percentage from the market or not. So, that is why it is minimum 40%. Their aim or agenda is just to take 40%. To be honest, we are not interested to even sell 1%. Yes, as per the clause, if anything happens, we might have to give them some percentage.

Q on Do Stylam Going to be Mfg House for AKCL - Stylam and Aica are separate companies and the Stylam brand will continue independently for the long term. They already have a plant in Rudrapur. Discussions on manufacturing or product sourcing have not yet taken place as Aica has not joined the board yet. Once they come on board, decisions regarding manufacturing or exports may be discussed.

Q on Conflict of Interest Between Both - First of all, they are not present in the western market at all. Europe, North America, they are not all present anywhere. Their major market is APAC region. Secondly, Aica itself is a very big brand name. It is a very old brand name. Stylam is actually nothing in front of Aica, to be honest. So, I think there is nothing, no conflict at all. It is just like two big brands getting together

Q on ADD on Solid Surface - Earlier, solid surface products were combined with laminates and due to internal family issues we could not actively sell them in the domestic market despite anti-dumping duty protection. Over the last one month, we have started managing solid surface as a separate product line under HPL (high Pressure Laminate). Going forward, we expect to report separate domestic and export sales for solid surfaces from the next quarter. Domestic is 12.31% and export is 21.35%, so total is 32.67% for Q3 acrylic solid surface. In only solid surfaces, number of sheets sold are 5574 and amount is Rs. 4.28 crores.

Q on EU & US Business - Firstly for Europe, the import value in Europe was 6.5%, which I think it will be 0% in the due course of time, whenever the agreement signs. And for US, it is right now 50%, as I was there in US last week. They have actually reordered us everything, and it will start manufacturing for them. So, they would be taking that duty in their cost.

Q on Stylam Laminates Vs MDF - we are not producing low-pressure. That is different, that is MDF. Low pressure is a different thing. We produce only high-pressure laminate, HPL.

Q on Fy 27 - . But next year we are definitely targeting Rs. 1500 crores to Rs. 1600 crores plus. Margins would definitely be better if you talk about the realization per sheet would increase because right now, we were selling just commodity items in the domestic market. So, the mix would change. Slowly and steadily as we would be targeting only on the value addition product.

My Take – Family dispute issue is behind, company to commission new plat in Mar 26. Aiming for 1500cr Rev for Fy 27, means an increase of 50%. They also discussed about acquisition of 2-3 plants. May come up with pref issue to promoters or AICA.

3 Likes

Let’s have a look at the macro factors across Feb-March 2026

-

Oil price increased the most in the last 4 years & barely any sign of de-escalation in the Middle-East war.

-

Global freight rates are increasing due to sea-route disruptions & nobody has any idea when things will get back to normal.

-

All Indian laminate players (Greenlam, Century, etc.) stock prices are under correction because high oil prices increase input raw material prices & thus in the next 2 quarters (if not more) all these players will experience margin compression.

-

Amid all the negativity, one major laminate player, Stylam’s stock price didn’t correct at all, rather trading in a tight range of 2150–2250 across Jan–March 2026.

-

Stylam is a major laminate manufacturer that derives ~70% revenue from the export market (mostly EU & Middle East), so their customers are impacted, rising oil prices are putting pressure on raw material prices, sea-lane disruption is further worsening the situation which means the next at least 1–2 quarter results will come under pressure, STILL the stock price is not correcting!

-

Whenever any stock moves in such a tight range for months, either a sharp breakout on the upside or on the downside happens.

So let’s explore what can happen with Stylam.

Secret of No Correction - Open Offer

We discussed the tight range in stock price since the last 2–3 months, well that is mostly because of the “Open Offer” as follows -

-

Japanese laminate giant Aica Kogyo is acquiring a majority stake in Stylam. They already acquired ~27% stake from one promoter group & floated an “Open Offer” to acquire another up to ~26% stake, turning their stake anywhere between 40%–53% in Stylam.

-

The Open Offer (Aica will buy from existing shareholders) price is at Rs. 2250. The tender period closed on 5th March & settlement on 20th March 2026. That open offer price acted like an upward ceiling & coiled the price in a tight range. After 20th March 2026, the price is expected to break out either on the upside or on the downside.

What’s changing post 20th March 2026?

-

Stylam is no longer an Indian laminate manufacturer, rather they have turned into a manufacturing hub of an Asian giant, Aica Kogyo. The market may treat it as a Japanese MNC player & assign P.E accordingly over the longer run.

-

Stylam completed a massive expansion that can take their revenue 2X within the next 3-4 years. Considering macro headwinds, revenue growth may take longer than expected BUT if Aica Kogyo wishes it would be a cakewalk, because Stylam’s current revenue of ~1100cr is nothing in front of Aica’s global revenue of ~15,000cr (converted to INR). A small global manufacturing base shift of Aica can push Stylam’s revenue into different territories.

-

Stylam will get Japanese advanced patented technology, access to cheaper raw material sourcing, even access to low-interest debt. Aica Kogyo has a huge market share in the premium segment not only in the Japanese market but also across the Asia-Pacific region. So, there’s a massive synergy tailwind for Stylam, how much that will be reflected in financials is a different question.

-

Stylam already has best-in-class margins & one of the largest single-location manufacturing plants in Asia with an EU customer base. Post India–EU & India–US trade deal, benefits will be visible from 2027 onwards while India–EU zero tariff will remain effective.

-

Stylam’s domestic business was affected over the last 2–3 years because of a family rift. One promoter family permanently left the business by selling the full stake to Aica Kogyo, so now rifts are behind, entry of Japanese professionals may even scale domestic business to another level.

-

Finally, there’s a chance of scarcity premium due to free float squeeze post open offer.

Despite all positives, don’t forget the near-term red flags - rising crude oil prices, rising input material prices, rising freight rates, problems in the Middle East & EU which is Stylam’s major customer base which all combined can reasonably put pressure on the next at least 1–2 quarters financial results!

Disclosure - The above write-up is shared among our clients. We are SEBI Registered Research Analyst (Paul Asset) & investment manager of Alternative Investment Fund, 129 Wealth Fund. Over the last few weeks we have invested in Stylam & anticipating very strong accumulation is going on among few institutional investors.

5 Likes

Thanks for the detailed post Prasenjit, was useful!!

You mentioned that Open Offer price acted like an upward ceiling, and the price is expected to break out post 20th only.. could you explain this.. i would have thought downside was protected and since open offer closed on 5th March. price if it has to go down should have gone down post 5th itself.

disclosure: I am holding few shares and looking at the Japanese management’s entry have been thinking of increasing stake, but was waiting for some correction in the counter.

This is how FIIs & DIIs accumulate shares. Since the open offer price is 2250, they will never bid higher or even close to that 2250 mark until settlement happens. They know macro headwinds and know that retailers must panic in broader market fall and attempt to sell shares that are either still in profit or have corrected less. They are patiently sitting with a bucket, accumulating whatever supply comes into the market without raising the ceiling. The long lower wick candles you can see in the charts across March are proof that smart money is absorbing all the panic supply from retailers. The best part is such prolonged smart money accumulation don’t attempt to capture short term upside rather pre-empt some long term upside.

However, even FIIs/DIIs don’t have unlimited cash. At a certain stage, they will complete their allocation, and after that, if heavy supply pressure comes from another institution (like MF redemption pressure from investors), then ultimately the downside support will be breached. That’s why I mentioned clearly that there will either be a violent upside breakout or a violent downside breakdown, nothing in between.

The point is to see whether demand exhaustion happens first or supply exhaustion happens first - even the institutions are eagerly watching for that and positioning themselves based on current clues.

P.S. - I may not be able to reply any further queries or other members’ questions, as I too have limitations on what I can write in a public forum.

2 Likes

The tendering period is till 31st March, right?

As per latest update, the open offer tendering period is delayed. So now 3 situation emerge for Stylam -

- Another month long tight price consolidation in 2140-2240 zone until Open Offer concludes.

- Decisive upside breakout if float squeeze & massive supply contraction happens.

- Decisive downside breakdown if somehow Aica Open Offer got cancelled or face some massive hurdle.

This is going to be an interesting case study that is offering so many lessons to investors.

Study this interesting case, while the Middle-East war, rising oil prices, and rising sea freight rates caused a massive correction in the Indian small-cap space, every laminate player bled. Every company dependent on crude oil-linked RM or exposed to sea route-linked Middle-East & EU exports faced massive price correction. Then how Stylam stock price is completely detached from everything, despite the business fundamentals being directly linked with crude oil prices, the Middle-East & EU

Indeed. They have shown robustness in comparison to Century Ply and Green Lam.

Think we can attribute it to the classic 2 of the forces defined by Porter.

- Competitive Rivalry - Leads exports to over 80 countries, so the tariff impact is only limited.

- Bargaining Power - The rise in crude oil prices as well as tariffs was shifted to the end customer due to the nature of the product being world-class. Hence, their margins aren’t impacted.

Corporate Restructuring & Shareholder Alignment

The Exit of Manav Gupta & Strategic Entry of Aica Kogyo

Historically, Stylam’s domestic business was severely bottlenecked by internal family disputes. A major operational and ownership clean-up was executed in early 2026, completely transforming the governance structure.

The Domestic Bottleneck Resolved

The domestic market was previously managed by Manav Gupta. Due to a multi-year family rift, domestic operations remained un-systematic, and high-margin products like acrylic solid surfaces were neglected despite anti-dumping duty protections. In February 2026, Manav Gupta, along with Pushpa Gupta and Dipti Gupta, exited the company completely, selling their entire 27.12% stake to Japanese strategic partner Aica Kogyo at ₹2,250 per share.

Shareholders’ Agreement (SHA) Mechanics & Open Offer Results

Aica Kogyo launched an Open Offer to acquire an additional 26.00% stake from the public at ₹2,250 per share. The post-offer advertisement filed on May 19, 2026, reveals the following structural outcome:

-

Shares Tendered: Public shareholders tendered only 4,66,116 shares (2.75% of voting capital) due to the market price trading significantly above the offer price of ₹2,250.

-

Aica’s Current Stake: Post-offer, Aica holds 50,62,984 shares (29.87% of voting capital).

-

The 40% Minimum Commitment Clause: Under the SHA, Aica has a contractual right and obligation to hold a minimum of 40.00% stake. To bridge the 10.13% shortfall, the remaining promoters (Jagdish Gupta, Saru Gupta, and Nidhi Gupta) will dilute their holdings to Aica in a secondary transaction (Second Closing under SPA 2).

-

Promoter Intent: Promoters explicitly stated in the May 2026 call: “Our aim is not to sell even 1% more than what is contractually required. The dilution is strictly to satisfy the 40% SHA clause.”

Operational Roles & Management Continuity

The transition is structured to preserve operational agility while absorbing global best practices:

-

Manit Gupta took over as Whole-Time Director in February 2026, actively restructuring the domestic sales team, cutting excess manpower, and streamlining dealer policies.

-

Aica Kogyo operates strictly as a strategic partner with board representation (one seat filled in February 2026). They do not interfere in day-to-day operations, which continue to be led by promoter directors Jagdish and Manit Gupta.

Capacity Expansion & Asset Productivity

Greenfield Plant-3: Imminent Commissioning & Revenue Potential

The construction of Greenfield Plant-3 at Manak Tabra (Panchkula, Haryana) represents a massive capacity inflection point. After repeated delays, commissioning is now imminent.

Timeline & Regulatory Delays

Commissioning Date: End-June to Mid-July 2026. Trials and machine testing commenced in May 2026.

The Delay Reason: A Supreme Court observation required seeking Environmental Clearance (EC) from MoEF, Delhi because no Corporate Environmental Responsibility (CER) framework was active in Haryana at that time. This regulatory hurdle added a 3-month delay (shifting commissioning from March to June/July).

Capex & Financing Edge

Total Capex Incurred: ₹334 Crores (up from initial estimates of ₹300-320 Cr due to GST and regulatory compliance).

Day 1 Profitability: Management asserted that the plant will be profitable from Day 1 because:

-

It is funded entirely through internal accruals (zero term debt, zero interest drag).

-

70-80% of fixed overheads and employee hiring have already been absorbed in recent quarterly P&Ls.

-

Incremental manpower required is limited to only 150 workers.

Forward-Looking Income Statement

FY27 Projections: Management Guidance vs. Forensic Stress-Test

We present a side-by-side comparison of the Management Guidance Case and our Forensic Analyst Stress-Test Case. Projections factor in a maximum of a 1-quarter operational lag for Plant-3.

| Metric (INR Crores) | FY26 Actuals | FY27 Management Guidance Case | FY27 Forensic Analyst Stress-Test Case | Forensic Variance & Assumptions |

|---|---|---|---|---|

| Net Revenue | ₹1,091 Cr | ₹1,300 - ₹1,350 Cr | ₹1,210 Cr | Stress-test assumes a 1-quarter delay in domestic dealer stabilization and a slower ramp-up of Plant-3 (contributing ₹180 Cr vs. guided ₹250 Cr). |

| EBITDA | ₹220 Cr | ₹286 - ₹324 Cr | ₹242 Cr | Stress-test factors in a 3-month pass-through lag for crude-linked raw materials and initial sub-optimal capacity utilization at Plant-3. |

| EBITDA Margin % | 20.1% | 22.0% - 24.0% | 20.0% | Management expects margin expansion via operating leverage and value-added compacts. Stress-test assumes margin dilution from raw material cost pass-throughs. |

| Depreciation | ₹21 Cr | ₹32 Cr | ₹32 Cr | Reflects the capitalization of the ₹334 Cr Greenfield Plant-3 in Q2 FY27. |

| Interest Expense | -₹5 Cr (Net Credit) | ₹4 Cr | ₹4 Cr | Assumes minor working capital interest; term debt interest remains zero. |

| Profit Before Tax (PBT) | ₹203 Cr | ₹265 Cr | ₹216 Cr | Conservative stress-test PBT margin of 17.8% vs. guided 19.6%. |

| Tax Rate % | 26.0% | 26.0% | 26.0% | Standard corporate tax rate applied. |

| Net Profit (PAT) | ₹150 Cr | ₹196 Cr | ₹160 Cr | Stress-test PAT growth of 6.7% YoY vs. guided 30.6% YoY. |

Quarterly Revenue & EBITDA Trajectory (Forensic Stress-Test Case)

| Metric (INR Crores) | Q1 FY27 (Proj) | Q2 FY27 (Proj) | Q3 FY27 (Proj) | Q4 FY27 (Proj) | FY27 Total (Stress-Test) |

|---|---|---|---|---|---|

| Net Revenue | ₹285 Cr | ₹295 Cr | ₹310 Cr | ₹320 Cr | ₹1,210 Cr |

| EBITDA | ₹57 Cr | ₹59 Cr | ₹62 Cr | ₹64 Cr | ₹242 Cr |

| EBITDA Margin % | 20.0% | 20.0% | 20.0% | 20.0% | 20.0% |

Operating Leverage & Margin Dilution Math

EBITDA Margin Drivers & Raw Material Sensitivities

Stylam’s EBITDA margins are highly sensitive to crude oil derivatives (Phenol, Melamine) and ocean freight rates. However, the company possesses structural buffers that insulate its absolute cash flows.

The EBITDA Margin Dilution Math (Critical Investor Concept)

When raw material costs escalate, Stylam passes on the absolute cost increase to its customers. For example, if raw material costs rise by ₹10 and revenue is increased by ₹10, absolute EBITDA cash flow remains identical, protecting investor capital. However, because both the numerator (EBITDA) remains flat while the denominator (Revenue) increases, the headline EBITDA margin % mathematically dilutes. Investors must focus on absolute EBITDA growth rather than headline margin contraction during inflationary cycles.

Key Margin Buffers & Mitigants

-

Forward Bookings: Stylam maintains a 5 to 6-month stock of Phenol and Melamine booked under old contracts, delaying the impact of Middle East war-linked cost spikes by at least two quarters.

-

FOB Pricing Structure: 75% of revenues are exports, and contracts are priced on a Free-on-Board (FOB) basis. Ocean freight volatility is borne entirely by the customer, insulating Stylam from shipping spikes.

-

FX Tailwinds: With the Euro trading at ₹112 and the USD near ₹96, Stylam derives a 3% to 5% net profitability buffer from favorable exchange rates, offsetting raw material inflation.

-

Operating Leverage: Greenfield Plant-3 requires zero extra fixed overheads or salary expenses (70-80% already absorbed). Manit Gupta highlighted: “We can generate ₹300-400 Cr of incremental turnover with almost zero extra fixed opex, dramatically expanding operating margins as utilization scales.”

Value-Added Growth Engines

The Acrylics Turnaround & Patented Japanese Tech Launch

Beyond commodity laminates, Stylam is leveraging its partnership with Aica Kogyo to trigger two high-margin product catalysts.

1. Acrylics Segment Turnaround

FY26 Performance: ₹15 Crores revenue (acknowledged as an underperformer due to family disputes and lack of domestic focus).

FY27 Target: ₹50 to ₹70 Crores.

The Aica Synergy: Aica Kogyo is a massive global buyer of acrylic solid surfaces, currently importing large volumes from DuPont (Europe/USA). Aica’s senior leadership visited Stylam’s facility in May 2026 to qualify and transition their global sourcing to Stylam, creating a massive, high-margin import-substitution pipeline.

2. Patented Japanese HPL Technology

The Catalyst: Under the Shareholders’ Agreement, Aica Kogyo is transferring advanced, patented Japanese technology in High-Pressure Laminates (HPL) to Stylam.

Timeline: Commercial launch in India is scheduled within 2 to 3 months (Q2 FY27).

Strategic Moat: This technology will allow Stylam to manufacture premium, high-barrier products that are currently unavailable in the Indian domestic market, driving brand premiumization and dealer enthusiasm.

6 Likes