04/07/2024

PREFACE:

The company originally filed DRHP for a combo IPO of fresh equity issue worth Rs. 45 cr. and an offer for sale of 7800000 equity shares. According to the Lead Manager, SEBI returned this document saying that company has good earnings and is not in need of cash, hence opt for OFS route only. Based on this suggestion by the regulator, LM refiled the fresh DEHP in January 2024 with requisite size of offer and finally got approval for an OFS of Rs. 130.15 cr.as per final RHP. It is a debt free company as of now and is capable of meeting any fund needs from its internal accruals. Thus at the behest of regulator, the IPO was a fully secondary offer.

The IPO price was Rs 136 and it was listed on 10th June at NSE & BSE

ABOUT COMPANY:

Kronox Lab Sciences Ltd. (KLSL) is a manufacturer of high-purity speciality fine chemicals. It manufactures products compliant with reagents, pharmacopeia, and various food grade standards used in the pharmaceutical, nutraceutical, veterinary, food, biotech, chemical analysis and research, metallurgy, personal care and other specialty markets.

The company’s product groups include acetates, carbonates, chlorides, citrates, hypophosphates, nitrates, nitrites, phosphates, sulphates, and other ultra-pure fine chemicals.

KLSL manufactures High Purity Speciality Fine Chemicals for diversified end user industries. Its High Purity Speciality Fine Chemicals are used mainly as:

(i) Reacting agents and raw material in the manufacturing of Active Pharmaceutical Ingredients (APIs);

(ii) Excipients in pharmaceutical formulations;

(iii) Reagents for scientific research and laboratory testing;

(iv) Ingredients in nutraceuticals formulations;

(v) Process intermediates and fermenting agents in biotech applications;

(vi) Ingredients in agrochemical formulations; (vii) ingredients in personal care products;

(viii) Refining agents in metal refineries; and (ix) ingredients in animal health products, amongst others.

Company’s products are manufactured in accordance with industry standards like IP, BP, EP, JP, USP, FCC, LR, AR, GR and ACS in addition to custom manufacturing specifications, which differ from the industry standards, required by its customers in 10 mesh to 100 mesh.

Its range of more than 185 products spanning across the family of phosphate, sulphate, acetate, chloride, citrate, nitrates, nitrites, carbonate, EDTA derivatives, hydroxide, succinate, gluconate, among others are supplied to customers in India and more than 20 countries globally.

In addition to the manufacturing of products in accordance with various domestic and international standards, KLSL also undertakes custom manufacturing to achieve high levels of purity, as specified by the client, having different purity levels than the prescribed industry standards. Custom manufacturing requires deep domain knowledge, expertise and understanding of the characteristics of each chemical and its compounds, including decreasing the level of existing impurities and the processes to be deployed to reach the desired level of purity.

Manufacturing Facilities The company has 3 manufacturing facilities spread over 17,454 sq. meters, having an aggregate installed capacity of 7,242 TPA, which are situated at Vadodara in Gujarat, and is close to the seaports of Mundra, Kandla, Hazira and Nhava Sheva.

Expansion Co. intends to establish a new manufacturing unit at GIDC Dahej – II Industrial Estate and the company has acquired land measuring 20,471 sq. meters for it. In the new plant it plans to produce High Purity Speciality Fine Chemicals like acetate, adipate, ascorbate derivatives, aspartate derivatives, benzoate, citrate derivatives, EDTA derivatives, gluconate derivatives, glycinate derivatives, lactate, malate derivatives, orotate derivatives, propionate, sorbate derivatives and succinate.

User Industries

Pharma - 41%

Scientific Research & Laboratory Testing - 29%

Nutraceuticals - 25.5%

Others - 4.5%

Geographical Revenue Bifurcation

India - 68.5%

Exports - 26.5%

SEZ Sales - 5%

Merchant Exports - 1%

Exports USA is the leading export market contributing 80% of their export revenue; they have presence in 20 countries including, Argentina, Mexico, Australia, Egypt, Spain, Turkey, United Kingdom, Belgium, United Arab Emirates, China, etc.

Repeat Customers During the Fiscal Years 2023, 2022, and 2021, the company served 351, 316, and 283 customers, respectively. In the last 3 years the company served over 592 customers, with 141 (23.82%) placing repeat orders.

R&D Capabilities The company has established an in-house research, development, and testing (RDT) laboratory to develop and test products. During Fiscal Years 2023, 2022, and 2021, the company manufactured and sold 157, 156, and 159 products, respectively.

Customer concentration

Top 10 Customers - 50.5%

Top 20 Customers - 65%

KLSL’s blue-chip customer list included name like Sanofi, Divi’s, Mankind Pharma, Lupin, Dr. Reddy’s, Sun Pharma, Zydus to name a few.

Key Things to Note :

(1) Company is a small niche player in the segment since last 14 years.

(2) It has plans to expand capacities 3.5x times its current capacity.

(3) CAPEX planned over FY25-FY26 is worth ~60 cr. v/s current gross block of 36cr.

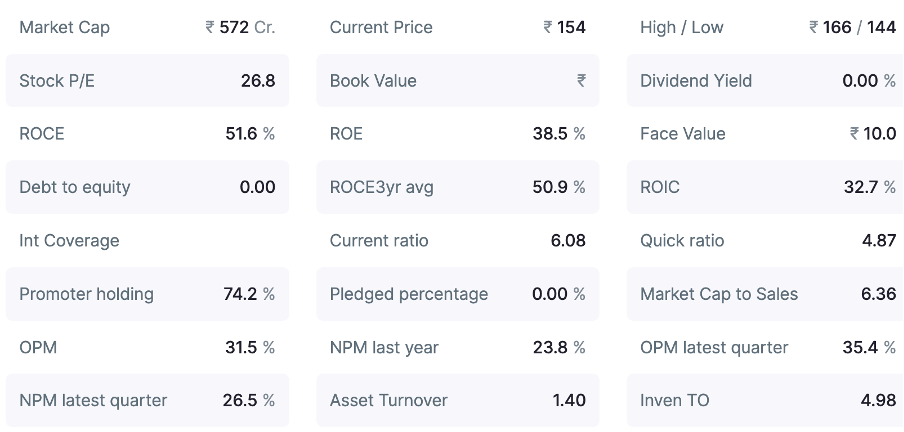

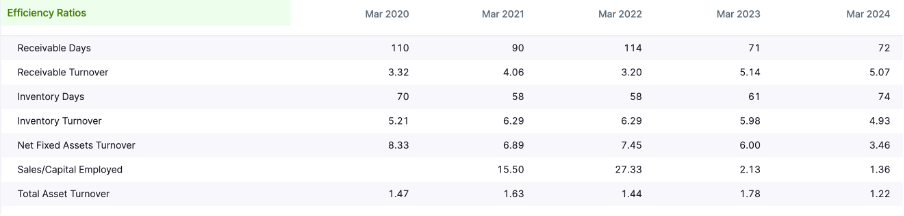

(4) EBITDA margins over last 5 years are 21% + each year.

(5) Consistently good positive Operating Cash Flow Generation with last 8 years average EBITDA to OCF conversion at 53.13 %.

(6) Exports currently contribute 26 % to total revenue.

(7) Exports are majorly to USA which signifies credible quality of its products.

Strengths of Kronox Lab Sciences

Client retention: Manufacturing niche specialty chemicals for clients requires a lengthy R&D (research and development) and audit process. This creates significant exit costs for clients. As a result, it becomes costly for them to switch suppliers, ensuring they stick with the company. Kronox maintains a sales record of over five years with almost one-third of its client base despite having no long-term contracts.

Weaknesses of Kronox Lab Sciences

Heavy reliance on pharma and biotechnology industries: Over 70 per cent of Kronox’s revenue was linked to the pharma and scientific research segments as of nine months ending December 2023. A slowdown in these industries can significantly impact the company’s financial performance.

Revenue concentration: Kronox caters to over 500 clients. However, its top 10 clients contribute nearly 45 per cent of total revenue. A walkout or reduced demand from even one key client can adversely affect the company’s financials.

======================================================

Compiled Notes from here & there