Free cash flow still negative and debt is increasing.

It’s best to stay away from such companies at least until they start generating consistent fcfs.

It is actually one of my main filters before taking analysis of any company any further. If the business cannot generate free cash, then there’s something intrinsically wrong with the business model itself.

Dmart has negative FCF, because it puts back the cash generated into the business, taking no debt. So we have to know the reason why there is no free cash.

I am studying Websol Energy System Ltd. The company makes solar cells and is increasing its capacity by 7 times (from the current 250 MW to 1.8 GW) while upgrading its solar cell tech from multi-crystalline technology to Mono PERC and TOPCon. As per the annual report, 1200 MW capacity would come live by end of this year.

The company decided to take voluntary losses in Q1 by scraping the existing technology and replacing the legacy equipment with cutting-edge alternatives. The losses would continue for another quarter or so. Expected sharp rebound in 2023-24.

Not sure if it is part of the above capacity expansion plan but early this month, Websol announced JV with AMP Energy India, part of Amp Energy Group for 1.2GW capacity of solar cell manufacturing.

Disclaimer: Studying it and would appreciate any further thoughts. The company thread isn’t very active.

Solar module manufacturing industry in India has never been and is still not attractive from an investor’s perspective.

Most the technology required for manufacturing is always imported because there is no tech development which happens in India. Mono PERC as a technology is not very old, and now we have TopCon, additionally there will be many other in the development stage which will render the TonCon obsolete pretty soon.

Most raw materials required for module manufacturing are imported. The value chain is solar grade silicon ingots >>>wafers>>>cells>>>modules. At most we make cells in India from imported wafers and then module manufacturing is essentially an assembly work (with some automation/mechanization involved). There are many other materials required like glass, aluminum frames, junction box, connectors, soldering materials, EVA (front and back), backsheets, etc and host of chemicals, most of which (not all, but significant portion) is again imported, mostly from China.

The tech development in solar is rapid, meaning technology obsolescence is fast. This leads to significant CAPEX on a regular basis (leading to writing off of earlier investments).

The global price of solar module is driven mostly based on China’s price. Government may try to protect domestic manufacturers but its never going to be sufficient because India does not manufacture modules at scale. Moreover, many regard solar modules as commodity (for price negotiations) even though its not. And because of rapid tech development the fall in price of modules historically has been pretty high.

There is no technology advantage, no competitive advantage, no pricing power, for Indian manufacturers.

Just think about this, in the past decade and more, there is huge installation of solar projects in India, more than 80% of which used imported modules. Why, because the manufacturing scale was never there. Even currently, we dont have enough module capacity to meet the demand.

I personally think that it could only be a speculative bet and pure luck to make money, because fundamentally the economics are against module manufacturers. A company like Reliance Industries also bought a foreign module manufacturer and did not invest in building the business from scratch. Tatas also have had module manufacturing business for many years, but that has never scaled to meaningful capacities.

Look at historical performance of WebSol, Indosolar, Swelect, Surana from perspective of sales growth, profit growth, RoE/RoCE, networth improvement, etc.

Closing comment…chances of losing money in such stocks are much higher than making money.

Not invested, only sharing my personal opinion, not an investment advice.

Thanks, @Ketan_Chheda. This is exactly the kind of anti-thesis I was looking for.

I may go with a small allocation purely betting on the fact that India currently has a manufacturing capacity of 3GW of solar cells. The target is to increase it to 25 GW by April 2023. There is a union budget allocation of 19500 Cr PLI for this year. [source].

Some players will benefit just by the scale ambition. Hoping WebSolar to be one of those. What I am not sure about is how are they funding this.

Nature of the business is commodity, the OPM is pretty much reflection of that , where commodity play we need bigger volume, as supply side crisis will be over in a 6 months period so the commodity pricing will be over,

This is a 238Cr Market Cap company producing Aluminium customized products for end users in Defense, Railway, Automobile, Solar, Elect / Mech, Medical sector.

Thread was opened during March-2021 when it’s market Cap was half than today, Can not understand why Moderators decided to close the thread.

This company seem to be a good pick with these fundamental.

Sales growth 10%

RoCE 24%

PE 9

Dividend Yield 0.5%

Promoter has increased holding during April-May-June-2022

Has anyone looked at Krishana Poshchem

They make fertilisers. One of their group company Madha Bharat Agro Products expanded and with good results their share price increases 4X after expansion

The promoters are now doing the same with Krishana Poschem

The expansion has already completed and the new plant will go live in this quarter

The group recently also signed up with Jordan to ensure supply of phosphate at a good rate. This was done before the recent inflationary period so they have a good control over their raw materials

Their products being agricultural fertiliser are usually completely sold out as there is a constant shortage

You might like to look. This quarter most likely won’t be very brilliant but next quarter will give a good results and then subsequently as well their performance is likely to be good

If you have patience and want to accumulate now when impatient investors are selling in a years time this is likely to give a good return

There are so many good companies, why look at companies where promoters are selling

Look for instance Apcotex:

Their current plant is fully utilised. They have maintained better margins on that full utilisation so their customers don’t mind paying them to cover cost of inflation.

Their raw materials are used by one of the largest latex gloves manufacturer. Glove manufacturing business is recession proof.

And Apcotex is now almost on the final few days or weeks of going live with a new plant.

The risks of failure of that extra capacity is very low

I said “likely”, one can’t be certain

However I don’t know what you mean, infer what ?

“Next qtr low” or “better following qtrs”

Both are likely due to so many factors: inflation pressures, expansion project not handled correctly, low demand, competitive price pressures, etc etc

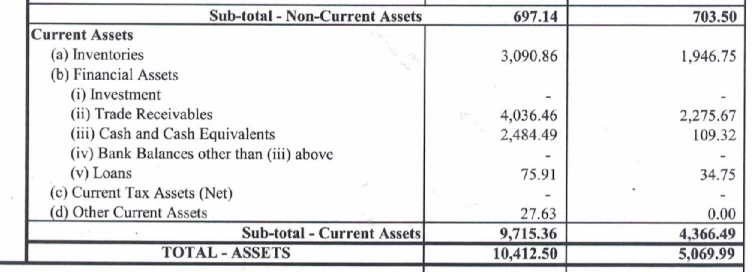

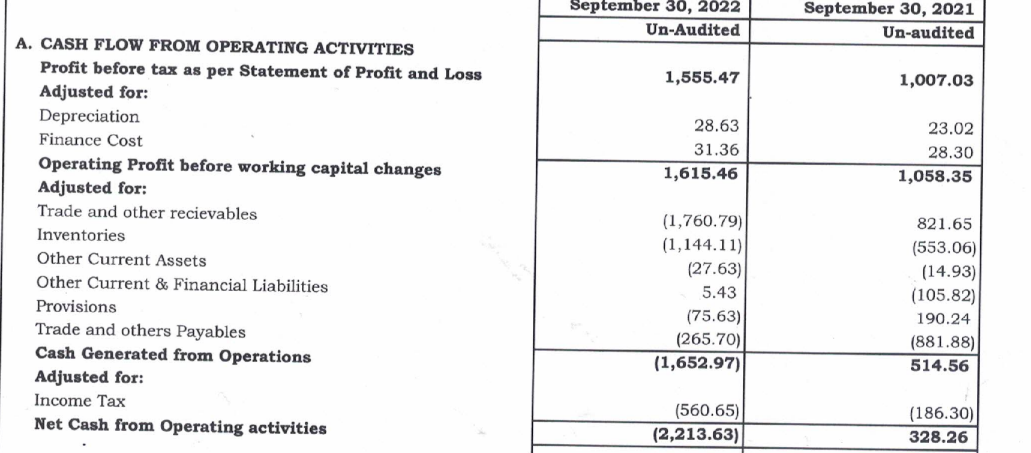

In the balance sheet as on 30-Sep-2022, there is sharp increase in CWIP and Borrowing.

Is this the reason or something else, that even after July-Aug-Sept-22 result which is improved YoY, the stock price is sliding. Down 10% since result announced.

I bought just before result announcement [observing improved RSI] based on technical, and now sitting on 10% loss.

I had a loss of 30% on globus spirits after I first brought it and then it went on to deliver multiples of my buy price.

If you are a technical buyer generally you should be able to avoid the 10% draw down.

Its near impossible to have a 10% drawdown if trading technically if the amount you are investing is low as you shld have and respect a stop loss.

However I trade fundamentally as I dont live in India and keeping technical trading screens open during trading hours is difficult

I do trade technicals in US and on s&p futures

I trade only flag patterns breakout with a stop loss. Apcotex had a failed breakout with volume on 23rd september but no follow through.

The promoters have been buying a lot of quantity as if you look at their last investor presentation, the expansion is not talked about a lot neither they talk about their demand. Those things are mentioned in the concall.

I suspect they want to either underpromise/overdeliver or maybe accumulate a bit more when the expansion initial hurdles are ironed out

On technicals its still within the flag pattern. At this stage the risk is it might break down which if it does, then it will lose another 5 to 10% however if you pick now, with a 5% stop loss the risks are very low

Ofcourse all stocks move in line with markets. If the index is down, most will give some but generally during the july selloff I was invested in Timken that didnt break the flag although was nearly about to but fresh money kept arriving into it as as soon as the indices turned it rallied

I think for me 30% drawdown for 3x return is fair game, nothing can go up in a straight line. My partner gets worried when its down 30% but I have asked her to not look at where I am investing just worry about running the home and giving me time off. Win-win

Apolgies for the long post.

Ps: the increase in WIP and borrowing is in line with my expectations of what should happen during expansion stage. I’d be worried there was no change in WIP or cost of capital. I actually had made a screen once to see growth in CWIP and inventory but all of it takes time to drill into which I dont have.