Thanks for this insight Gaurav, Yes, you are right that the receivable is less than 180 days old. (From what i can figure out, 40% is denominated in USD) I have just one clarification to ask: If LCs are contractually interest bearing, shouldn’t interest income be accrued over time?

1 Like

Excellent results for Q1 with YOY revenue up by more than 47% & EPS up by more than 72%.

Disc: invested & no reco

3 Likes

Personally have followed Wood Mackenzie reports very closely since last 3+ years to see the evolving trends shaping the industry. So far, he has been mostly correct with his prognosis.

Here comes the most recent one:

Some key pointers:

- Wood Mackenzie estimates that, power transformers and distribution transformers are currently in a supply deficit of 30% and 6%, respectively, based on annual supply and demand estimates.

- The US relies on a single domestic supplier of GOES, AK Steel, forcing many original equipment manufacturers (OEMs) to source raw GOES or semi-finished transformer cores abroad.

- Copper windings, meanwhile, have emerged as another potential bottleneck to transformer production, due to their highly technical manufacturing process and niche specifications, and the US government’s 50% copper tariffs likely to worsen the issue.

- The domestic sector is also cautious about expanding capacity due to uncertainties surrounding the sustainability of US demand growth, especially as the “One Big Beautiful Bill” is expected to reduce clean energy investment.

- Many of the largest transformer OEMs have announced capacity expansions since 2023 to address the shortage in the Norther American market – some US$1.8 billion to date. However, the rate of demand growth will require even more investment to rebalance the market.

Disc:

Invested, no trasaction in past 6 months

14 Likes

Anyone aware when Shilchar will do their concall or they are not gonna do it??

There wouldn’t be quarterly concalls. They have moved to half yearly concalls now

3 Likes

AGM notes

- India emerging as one of the fastest growing power markets in the world;

12.3 GW of new capacity addition to the national grid, from Renewable energy in Q1 FY26. Of which solar contributed 10.5 GW - Confident of achieving the guided revenue for full year.

- 77% capacity utilization. Phase 2 of capex – Likely to share an update in 4 to 6 weeks.

- Working on the detailed plan on getting into higher kv transformers. Haven’t taken a final call. Might make an announcement by Sept end or so

- Continue to see strong demand from renewables sector in the domestic market

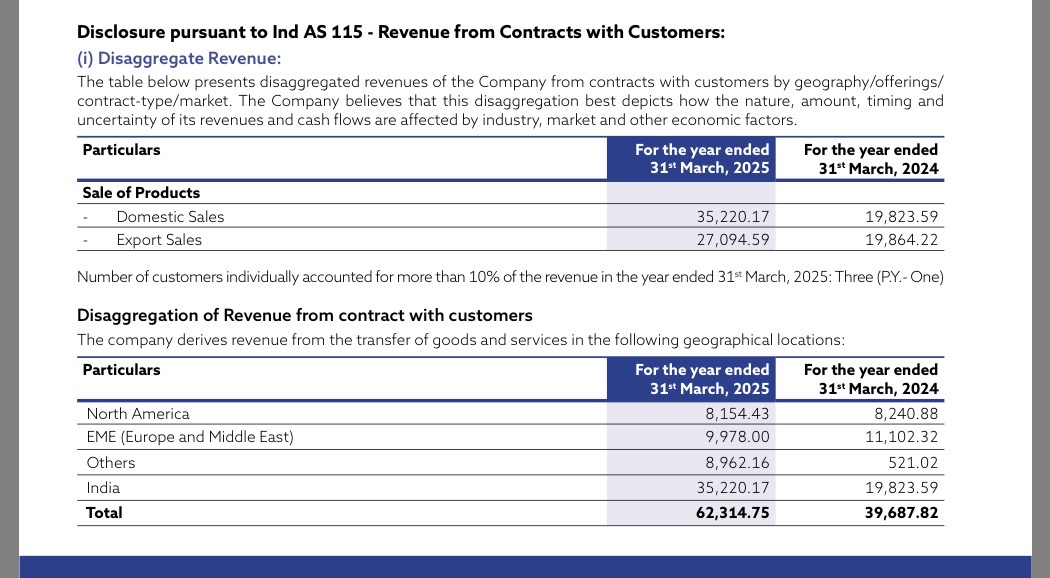

- Roughly 20% revenue from North America. Expecting a similar % contribution for this year FY 26 also.

- Risk mitigation in terms of realigning of geographies for exports, considering the buzz on tariffs?

o Likely to have a clearer picture within a month or so. Will evaluate then.

o On track to achieve the guided revenue for full year, even if there is some slight realigning of geographies that needs to be done as part of risk mitigation. - Continuing to see long lead times and shortages for transformers in export markets. More on this, in this Mercom article.

- NSE listing - Post receiving shareholders’ approval – will apply for the same. Process takes roughly 2-3 months’ time.

Disc: Invested

15 Likes

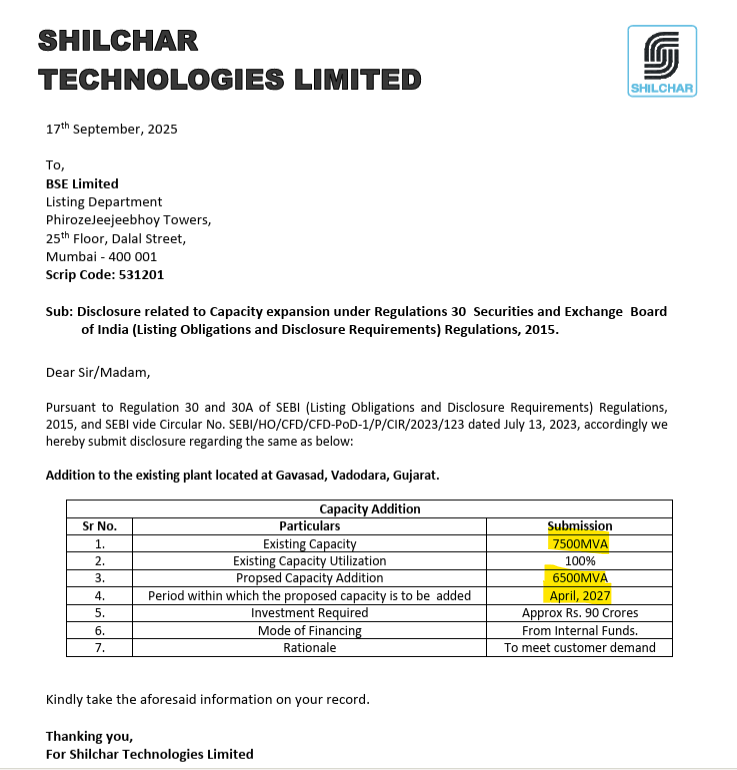

- Finally, capex announced.

- Almost double current capacity

- This also gives confidence, US tariff volatility wont have much impact

18 Likes

On first glance a very well thought out plan on almost doubling. The most important question that’ll get answered in H1 concall would be how this capex would come on stream.

Whether it’ll get commissioned in phases or it’ll be one time in April 2027, exactly the way last one played out. Now these are temporary scenarios & they are actually known to surprise with their numbers from existing capacity too.

But it’ll be good if some part can get commissioned by Q2 of FY27 so that in FY28 that capacity can be taken to 100% utilisation with rest coming in FY28 beginning.

But all in all getting it commissioned means that by FY29 they’ll reach peak capacity with a revenue capability upwards of 1500 crores. Not bad for a company that could soon be making a PAT closer to if not more than its FY23 topline(with no debt/ equity dilution as of now)

Disc: Invested, Biased & had sold some holding over last 2 months

They are conservative but they’ve also proved that they are terrific with their planning & have literally played this on front foot.

8 Likes

Most likely the whole capacity will be taken live altogether by April 2027, and this date could get pushed as well based on the past execution of capex. But that’s fine, the management does it prudently, and has always taken a very calculated approach. The only thing that needs to be known is that whether they will be expanding into existing range of transformers or they will they start manufacturing more high capacity ones, which the management has hinted that they are interested in doing. Because the per MVA realisation, and margins could change drastically with new category of products. So if someone has some clarity on that, or can get in touch with the IR team to get a clarification it would really help.

On the Exports side, they are doing really good YoY, in almost all months they have been outgrowing their YoY numbers, which is a good thing. MoM or QoQ could be fluctuating, but YoY there’s almost always growth.

3 Likes

What is the source of exports figures that you typically refer to? Does it also help drill down to the exports to the US ? (per the mgmt. discussion during the AGM, the exports to the US is ~22%)

Yes exports specifically to US can be tracked. Over a financial year it is around 22%, but accross months it keeps changing.

1 Like

On an annual basis it is around 20%

Can you redirect me to the source(s)?

Any thoughts how this affects the company

The U.S. is now expected to add almost 250 gigawatts of renewable energy capacity between 2025 and 2030, down from the IEA’s previous forecast of 500 GW. The revision reflects policy changes such as the earlier phase-out of federal tax credits, new import restrictions, the suspension of new offshore wind leasing, and restricting the permitting of onshore wind and solar projects on federal land. To note, tax credits had been the main driver of renewables growth in the U.S. since their introduction in 1992

4 Likes

Intimation about conference call/Investor Meet on 18th October, 2025 2.30 p.m. Registration details available

1 Like

Shilchar Investor presentation.

fc14e3cc-ff62-456b-8b4c-cdba9fd1e25d (1).pdf (4.4 MB)

Amazing results, decent uptick QoQ despite slow exports, which means they have scaled in domestic markets and are still able to maintain PAT Margins. Looking forward to the conference call.

2 Likes

The concall addressed one of the most important questions which is regarding new capacity expansion. The entire capacity would come up in April 2027 only, hence next year could be a little lukewarm as to what we are used to. The FY26 nos have been pegged to 750 cr now with an estimate that FY27 would be 900 cr from existing capacity only. FY28 beginning new capacity would start getting utilised.

Edit- FY27 would be between 850-900 cr since management gave two numbers during the call

Disc: Biased & no reco

10 Likes