Promoter has been selling recently. About 3% stake sold in open markets in October after the quarterly result freeze window opened.

1 Like

Alchemy Capital picks 0.78% stake in power and distribution transformers maker Shilchar Technologies

4 Likes

Just an estimate

Assuming market will give a PE of 35-40 at max to Shilchar till new capacity kicks in.

We should see sidewise movement in Shilchar for next 1 year atleast.

Lets see how things pan out

Another round of selling by promoter, ~100 Cr cashed out.

Guys listen to concall, Its a cyclical sector. People who stuck at the top may not able to see profits for 3-4 years.

2 Likes

How is it cyclical? There is a severe shortage of transformers for the forseeable future, right? (I haven’t listened to the concall yet)

4 Likes

I believe a lot of questions above were on the cards, given that now the suspense over capex is over.

The last time promotor sold he sold almost 3 months before announcing previous capex. This time he’s again sold not at peak Euphoria but when stock is already beaten from its highs post rights.

There is a good possibility that rerating might not be very easy which is looking the case for a majority of small caps. But then a lot of funds will also try to enter.

What we might be losing sight of is that this same facility was built to take production capacity upto 30000 MVA & now where is any player indicating towards supply gut or subdued demand as of now.

It’ll all boil down to return expectations as well as horizon & valuations one is comfortable with.

The best time to sell in hindsight was a few months back & the best time to bet heavily in foresight might be a few quarters away.

There are many names available with better earnings & growth visibility for FY27 now, hence everyone has plenty to choose from even in this sector or otherwise as well.

Disc: Biased, invested & have trimmed over last few months. No recommendation

4 Likes

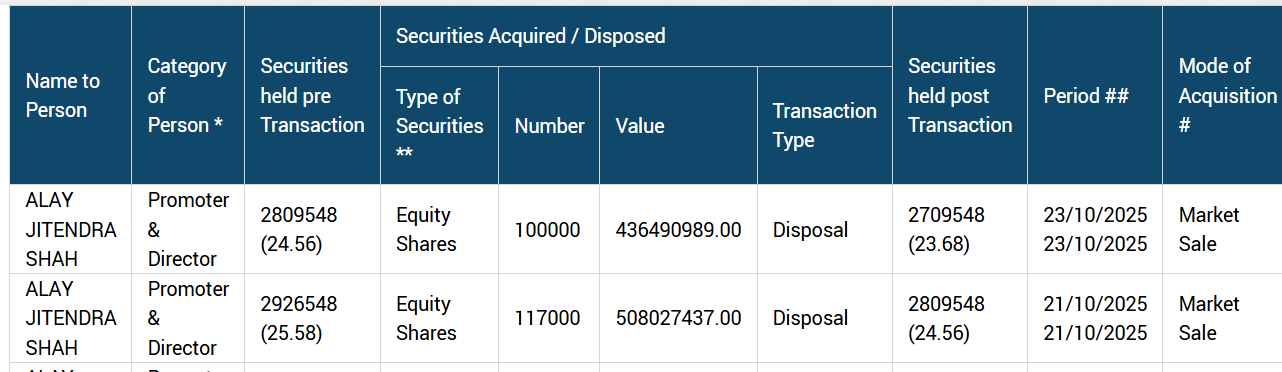

To contextualize this ‘promoter selling’ –

- 1,17,000 sold on 21st Oct.

- 1,00,000 sold on 23rd Oct

The avg weekly delivery volume for last 2 weeks, is around 72,000 shares. Despite such huge quantity of selling on 2 days, the share price has hardly budged. Which means that some Institutional buying is likely to have happened on these 2 days, else the share price would have reacted / dropped sharply.

Alchemy Capital, run by Hiren Ved (a reputed Fund Manager) was the buyer on 21st Oct, they bought 90,000 shares.

Similarly some other institutional buying may have happened on 23rd too, which we will come to know later.

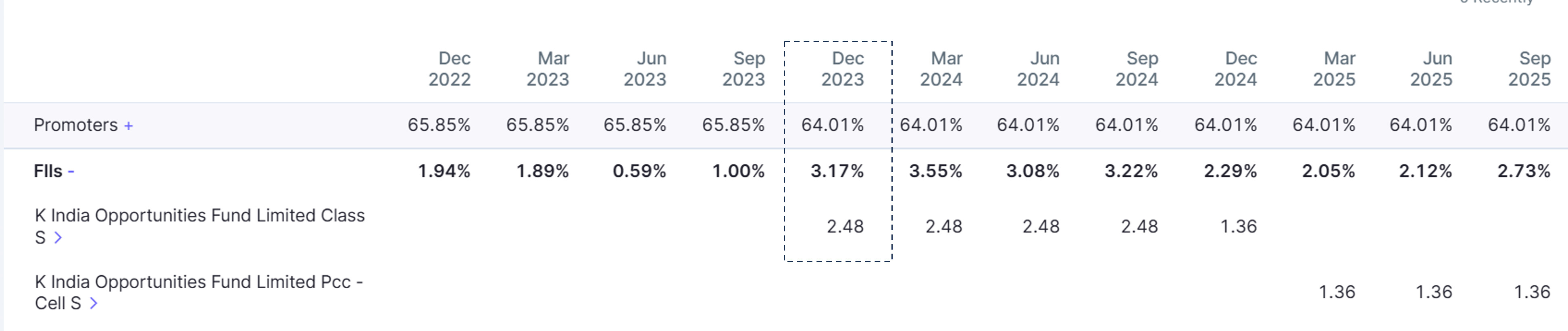

There was a round of promoter selling in Dec 2023 too, when a FII had entered the counter at the same time.

Cyclical stock yes, but the management mentioned during the call about, Govt thrust on 100% electrification and domestic renewable energy demand being strong tailwinds for the next few years.

7 Likes

Usually we grab some +ve information from the -ve things happening in any company.

If they want to sell shares to some institutions then they should go through block deal route rather than selling in open market. Moreover, there is no indication of selling share in the earnings call.

All players are having capex in pipeline and in 1-2 years available capacity would be on higher side. Demand jumps when country is having good capex cycle, all industries need transformers for new capex’s, but they may not need transformer for the same facility for next 10 years Avg. So, demand may not be much stronger going forward and valuations/margins may not withstands.

2 Likes

I have been invested in this one for a pretty long time and i booked profit on muhurat trading day. My two cents here:

1 - this is cyclical business and all companies in this sector are strugling - be it TARIL or Danish or Voltamp. It seems all got rated very well some time back and now some time for consolidation - time and price correction is being seen in all.

2. Shilchar management has delayed on their expansion plan for a very long time ~1 year was spent in coming out with a plan.

3. I could not join the con call, but went through the transcript and am bit surprised - it was Alay’s son who did most of the answering and his answers were not that strong and supportive - if you scan the transcript you will find - our customers are willing to pay us the premium, we are confident of meeting 750 cr revenue target, etc are there all over the place.

Reading at the transcript i got a feeling that the management now does not have much to speak - it is their normal business - business has peaked and may be will remain peaked for some time. Earlier the price rose sharply as there was both revenue growth and margin expansion - for the last few quaters margins has remained stagnant and revenue has grown at a flat 30% range. Also there is high possibility that they will reach peak revenue this year itself and next year there may not be any growth and in FY27 they are introducing new range of transformers which will again take some time to stabilize and accepted in the market and that will have an impact on the margins.

I may be wrong, but will be happy to sit on sidelines and track this one for next few quaters before taking a entry once again.

5 Likes

I agree most with the take on capex. Do feel that there’s somewhere some disconnect with how they have planned it. The biggest confusion is why they decided such a big capex last year & gave an indication that in a quarter details would be revealed which got pushed & now since they have announced the biggest mystery has been why not planned in phases as it would be brownfield.

Could be a case as wherein you pointed out that some sort of peak has reached in terms of margins & faster growth at such margins.

Didn’t pay attention to who answered the queries during concall & thanks for bringing that up too. Was a little amazed that two numbers came up in Concall with emphasis on 750 cr, which by no means is a bad number but certainly putting guidance at lower spectrum.

Need to see what kind of numbers other players come up with. TARIL over past few quarters used to come all guns blazing & declare results almost in first or second week. They’ve still not announced the dates. Need to see how other players have fared & what’s their commentary.

Disc: Have trimmed holding over past 2-3 months. No recommendation. Not authorised

I think they emphasised on 750 for this year with a reason. If they said they will do 8500 - 850 this year which in all probability will happen, then they will not have a growth number to speak for next year - which will be again something around 850 - 875 cr unless their new capacity shows in phases

2 Likes

The discourse on this thread has stunned and surprised me in equal measure. Firstly,I see a lot of confusion regarding Shilchar’s rev nos in the coming years & on their peak revenue nos. So one must understand that the realization/MVA can vary widely depending on kV mix and whether it’s being sold in the domestic mkt OR US/export mkt. Also,the Shilchar mgt has always been conservative even while talking of it’s peak revenue. They seem to take 10 lk/MVA realization as standard.

So here’s the thing: Back till FY21 & 22,when co had a capacity of 4000 MVA they would maintain that their peak revs will be in the 350-400 cr range. Later they raised it to 400-425 cr. However,in Q3 of FY24 they did 118 cr revs which translates to 472 cr annualized..that’s a variance of 25-35% from the first number! This capacity went up by 75% so it would mean at full util this 7000 MVA capacity can bring in 800-820 cr revenue. But in Q4FY25 they did qtrly revs of 232 cr which means a revenue of 930 cr on annualized basis! Now in the recent concall even after doing 172 cr revs mgt is saying they are at 90-95% util which means peak revs won’t be more than 700-20 cr. And similarly,with new capacity they are saying they’ll be able to do 1400 cr revs. Thus,the web keeps getting more tangled. Invariably,the mgt will push this number up once the new capacity comes in. So my estimate is that the peak revs post capex will be 1800 cr or so.

The matter of promoter sale is more fascinating. People are quick to dismiss cap good cos as ‘cyclicals’ and ‘commodity’ so there is an inherent bias to look out for the exact time things will start going downhill. However,Shilchar is a total anomaly since it makes 60-70% RoE/RoCE and doesn’t need to raise money or infuse money. So the only way such a promoter can cash out is by selling it’s stock. And regarding the timing,anyone can go back and check that the last stake sale took place around 2 years ago. Stock is 2-3x from there.

So my expectations would be this: In fy26 they’ll do 750-800 cr revs and ~950 cr in FY27. Fy28 will be the major step-up year.

I have also been surprised to see how the stock of Shilchar has been treated over the last 12-15 months. 6 months back ppl tracking the sector were complaining that Shilchar is not aggressive enough and there’s no revenue visibility beyond this 7000 MVA capacity. TARIL was considered top of the league both for it’s aggression and size. However,Shilchar has been able to maintain it’s very high GMs and EBITDA margins while continuing to grow at 30-40%. It now trades at 27x ttm and 22-23x fy26. Unless,markets or people with deep pockets expect the margins of the industry to go into severe shock due to oversupply or something starting Fy27 only then are such valuations justified. Still TARIL now trades at a premium of 100% to Shilchar on a ttm basis. So mkts are suggesting that it’s ok if a co dilutes all shareholders to raise money but it’s not ok if a promoter who keeps growing via internal accruals decides to ‘cash out’ a little.

Disc.: Invested. Views are biased.

27 Likes

Hope the trailing video\tweet clears where should we bet on

3 Likes

NSE listing update.

1 Like

As per the recently released Nuvama IC report on VoltAmp, Shilchar’s average realisations are about INR 0.95 mn/MVA while for Voltamp, it’s almost INR 1.4 mn/MVA. That’s a big difference considering both serve similar categpries (<220 kVa class transformers)

4 Likes