In recent months,the stock of Shilchar Technologies has been to hell and back. It stood very strong in the initial market sell-off but when it gave way it continued to crumble,almost halving in the interim. Then just a week pre results stock started springing up. It opened and closed at UC on results day with 18k pending bids at UC and then the day post nos.,stock was locked at UC with 118k bids! I don’t recall seeing such a large pending bid queue on Shilchar ever. All this is a testament to how much they blew away expectations. To start with,the mgt itself had been guiding for 550 cr revs in FY25 which implied a Q4 similar to Q3 in terms of revenue. However,the company instead reported a ~60% qoq jump maxing out it’s capacity in Q4 itself. One must also note that mgt repeatedly understates peak capacity nos. A part of this would also have to do with the geographical & application distribution of their revenues. I remember back in FY23 they would keep insisting that 350 cr is their peak rev number,and yet they did 118 cr qtrly revenue with the same capacity. So it didn’t surprise me that their MVA realization at 7500 MVA and an annualized turnover of 930 cr comes to north of 12 lk/MVA rather than the assumed and stated 10 lk/MVA. It’s also instructive to note how mgt has repeatedly kept expectations low on the margins side. The EBITDA margins have been a slight concern for some smart investors since it’s always felt very toppish,being head and shoulders above peers. Company has stepped up it’s margins every few qtrs and sustained the new range. One must also note that Shilchar is the only listed Transformer co. that has been doing GMs of ~40% since 4-5 qtrs now. Mkts continue to love TRIL and give it a much better multiple inspite of repeated dilutions and much inferior return ratios. While to their credit,TARIL’s product mix has continued to improve I still feel the gulf b/w Shilchar & TRIL is too wide & quiet unfair.

I won’t be surprised if Shilchar does 850-900 cr revs in FY26 and ~30% EBITDA which implies a 250-70 cr EBITDA or an EPS of ~250+. So the stock after the recent thrashing and recovery is still available at 26-27x. TARIL with an expected PAT of 350-400 cr trades at 17k cr mktcap or at ~45x fwd.

Disc.: Invested. Views are biased,reduced my position in recent months.

21 Likes

I feel Shilchar was started getting the same valuations once Shilchar lists on NSE too and FII and DII buying picks up

1 Like

As per the management in concall, trade receivables are due to “LCs” (probably line of credit). Customers can either pay upfront (within 30 days) or after 180 days with interest. Since the company doesn’t need cash urgently, they prefer the 180-day option and earn interest.

Disc: invested.

5 Likes

Not Line of Credit but Letter of Credit. It is a very common instrument used in Trade Finance.

Letter of Credit Explained

6 Likes

Would you have deeper insights into why GMs for Shilchar are much higher than, say TARIL? During the concall, management said in terms of pricing, they might just 1-2% more premium over their competitors for what they say is better service and better product (?) that they offer. Their ROCE is also way more than TARIL’s and that has got to be driven by OPMs since there isn’t too much of a difference in the asset turn ratio.

So then what is it that drives their better GMs and OPMs? Operational efficiency? What is it that they do to give them consistently better margins?

Or is it simply their product mix that gives them better margins - I know TARIL is more into power transformers and higher kv transformers, furnace transformers, etc while Shilchar is more into distribution and renewables transformers.

4 Likes

It is because of the variance (variability of supply of electricity from solar and windmills that we need to put in these transforms in distribution too. coal plant 10 gw can operate at that capacity if you have coal all year long (24 hrs a day). 10 GW of solar’s output is not in your hand, anyways it won’t operate at night

1 Like

Had a couple of queries that I’ve clarified with the person handling Shilchar Investors Relations over call

In Q4 the domestic business had shot up but they don’t see any concern with exports as of now with any preponing of orders from clients in US as well. My query was regarding the drastic mix change as well as growth delta. Plus US business is a part of business. They would’ve have already charted a mitigation plan plus demand worldwide is huge.

Also had a query to them regarding exports to other countries & Europe etc to which I got the response that some new accounts have been added as well in Africa etc. One key thing is that domestic demand is huge, validated by Taril also.

On the capex side my query was what would be the timeline to scale up to which the person responded it would take 4-6 quarters but when I countered that last time it took less, he still maintained it’ll take a year. Not convinced but looks more like it’ll be the reality. He told that drawings etc are in progress along with equipment’s requirement to put up facility

My final question was on max capacity utilisation & whether there was any difference in output in case domestic business gets heavy as in they did 230 cr in Q4 to which he replied there’s absolutely no difference whether it’s exports or domestic but capacity utilisation can go up from assumed 100% which is actually fair as happens in capital equipment industry.

All in all management is conservative but I really do feel that 800 cr will be easily achievable with 850 a possible reality & they might come up with more capacity by FY27 Q1 or Q2 beginning, which really puts 4-6 quarters required to expand into perspective, because even if they announce in a couple of months now there are monsoons ahead which delayed the execution last year.

Disc: Invested & biased

16 Likes

If somebody has insights into these questions, it would help us understand the company a little better.

Shilchar makes specialised transformers mainly for the renewable energy sector, and a large chunk of their products are exported. These transformers are customised to handle the problems specific of renewables—like variable wind loads, tight voltage regulation, and low noise and heat losses. Because of this niche focus and engineering complexity, they can charge a premium.

On the other hand, TRIL operates in the mass, commoditised segment. Most of their orders come from government and PSUs through tenders, which are extremely price competitive and leave little room for margin.

In short:

• Shilchar = Specialisation + high gross margins

• TRIL = Commoditised + low margins + volume play

P.S. If you’re looking for a global equivalent to TRIL, it’s JSHP from China—a volume-focused, cost-efficient transformer giant.

Disc: Invested, but partially exited

8 Likes

Shilchar’s transformers are not used for civic projects outside India, if you see it’s top overseas customer is Baker Hughes in the USA and they import Shilchar’s transformers for Industrial applications. So Shilchar’s market it more or less immune to whatever Trump decides to do with America’s renewable energy sector. But the tariffs and related things could affect their exports significantly.

4 Likes

Right, but how do we understand it in the context of this:

“During the concall, management said in terms of pricing, they might just 1-2% more premium over their competitors for what they say is better service and better product (?) that they offer. Their ROCE is also way more than TARIL’s and that has got to be driven by OPMs since there isn’t too much of a difference in the asset turn ratio.”

2 Likes

For Shilchar and other transformer + transmission players, to get a better understanding, watch this

3 Likes

Amazing export performance by Shilchar in the first two month of Q1FY26. Export numbers up more than 2x YoY in dollar terms. This quarter could be at par with Q4FY25 in terms of exports performance if this trend continues in June as well.

15 Likes

how to track export data of shilchar?

Volza gives data. Exim as well.

1 Like

I think it’s not allowed to share proprietary/paid data here on the forum. But they have been doing good this quarter so far.

4 Likes

Shilchar’s Q1 FY26 Export numbers are out. Their total Export value is around ₹88 cr, slightly down QoQ compared to ₹95cr in Q4 FY25, but significantly up YoY compared to ₹43cr in Q1 FY25. The numbers are really good considering the fact that historically Shilchar has almost always had a 20% drop in Export value between Last year’s Q4 and current year’s Q1. But this time around it is just 10% drop between the two quarters.

Just sharing for everyone’s refference, please DYOR before taking any investment decisions.

13 Likes

They explicitly guided for domestic growth to outpace the exports growth this year. So with that kind of export data, definitely gives comfort.

11 Likes

Shilchar Annual Report 25 is here

Some highlights:

Product Portfolio

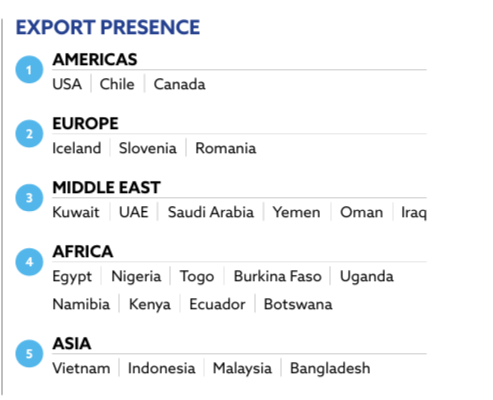

Export Presence

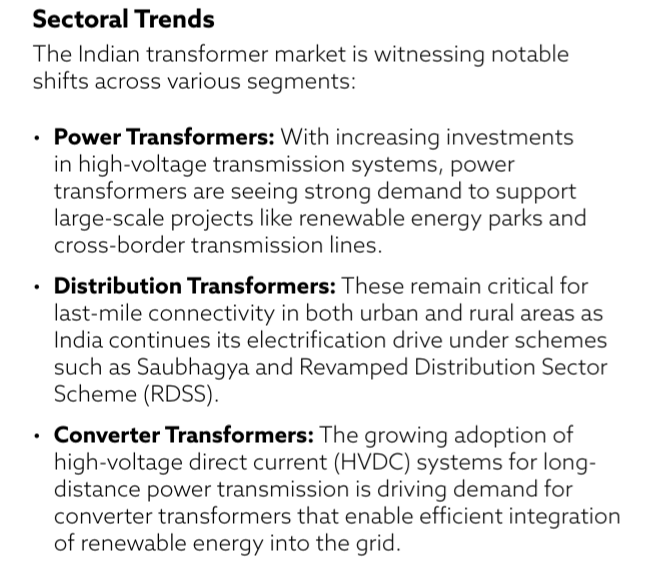

Sectoral Trend

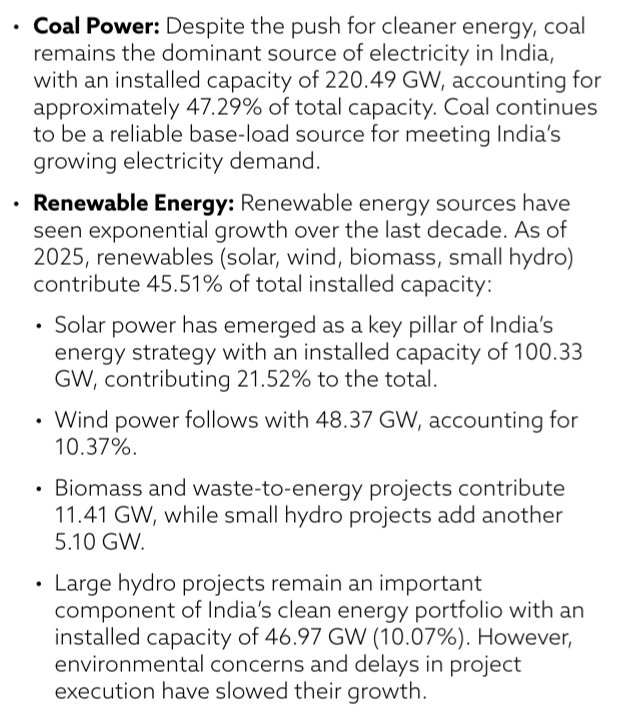

Capacity Contribution of Coal is still at 47%

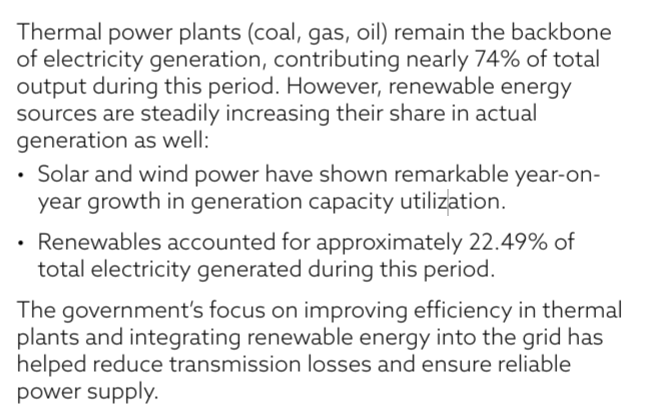

Thermal Generation is still at 74%, long way to go

Key Challenges to track

10 Likes

Im bit concerned/ confused about increasing receivables for Silchar. They increased from 94 to 229 Cr. Management says it’s due to LCs, but in my analysis, maths doesn’t add up.

Trade receivables in FY25: 229.72 crore

- Assumed LC interest rate (MCLR + 2%)*: 11%

- Expected 180-day interest income: 229.72 × 0.055 = 12.64 crore

- Actual interest income reported: 3.118 crore

- Of this, ~0.894 crore likely from bank deposits (29.8 crore @ 3%)

- Implied interest income from receivables: 2.224 crore (~17.6% of expected)

Therefore, this Indicates ~82% of receivables are not interest-earning

Note, (*) Receivables are classified as “unsecured,” so i think mclr+2% should be the interest rate.

Also, On page 125, provision rose from 1.01 crore to just 1.03 crore, despite receivables increasing from 94 to 229 Cr. They have reduced the weighted average loss rate (0.66% to 0.26%).

(Now it may be that since some receivables are in USD & they might yield low interest rates but gains due to dollar appreciation may show in forex currency translation, but I hope we get some clarity from management)

Disclosure: previously invested, partially exited. Posted, purely for educational and discussion purposes, and should not be construed as investment advice

8 Likes