Thoughts on results?

Heard the conference call recording post Q2. The biggest highlight of this quarter’s result is forex losses due to dollar strengthening vs euro.

During last 35-40 years(referring the chart below). Such a depreciation of euro against dollar have taken place only on two occasions. Around 1985 (Sharda did not exist then) and around 2002 (Sharda must be quite smaller back then)

Sharda’s business is facing quite a rare situation. The war between Russia and Ukraine along with interest rate hardening by US-Fed is likely to keep dollar stronger. Not withstanding what company has mentioned in the investor presentation and the impression they try to give during the investor conference, there are only few things that I think are happening to get forex situation normalized for Sharda

- The company wait for dollar to euro equation to normalize - less probable in near term

- Company re-negotiate with customers for better pricing - Thankfully they don’t have very long term contracts with customers(as mentioned during the last conf. by Mr. Bubna)

- Company increase the proportion of their revenue from NAFTA region. - again this would be gradual. But there are green shoot, for agro-chem as well as non-agro-chem they have shown more than 15% YoY revenue growth in NAFTA whereas For Europe, there have been 11% growth in Agrochem & 22% degrowth in Non-Agrochem segments.

There is slight increase in profitability in Q2 compared to Q1. But pre-Q1 level profitability seems to be few quarters away from now.

@harsh.beria93 Would appreciate your thoughts on - how do you see company’s trajectory for growth and profitability

5 Likes

Won’t they hedge forex like IT companies do? I’ll be surprised if they didn’t.

Based on management’s below mentioned comments during the concall. It implies that they are not in position to do the hedging at the point in time. I don’t believe they would be able to do it based on the narrative I heard on the call.

Options for hedging are very limited. They are not able to get clear views(about exchange rates). Vigilant to do hedging when there are clear view

IT companies are working with hedging for over past 15 years. I would be surprised if Sharda cropchem has any expertise on this. They have just started to think on hedging during last 3-4 months. I think, It will take time for them to figure it out

1 Like

Topline grew by 12%, gross margin pressure continued due to adverse movement of Euro vs USD. Management continue their guidance of 15-18% growth in revenue and EBITDA for FY23. Concall notes below.

FY23Q2 concall

- Guiding for 26-30% gross margins for FY23. Expect 15-18% growth in revenue and EBITDA for FY23

- Capex: 230 cr. in H1FY23

- Demand situation in Europe is good and has improved from last quarter

- Sourcing from multiple manufacturers in India and China. Don’t have long term agreements for sales or procurement. Everything is done on spot basis

- For Q2, volume (-) 23%, price (+) 34%

- For H1, volume (-) 13%, price (+) 36%

- Agchem quarterly volumes: 3mn vs 3.4mn in EU, 1.9mn vs 2.35mn in NAFTA, 0.6mn vs 1.4mn in LATAM, 0.75mn vs 1mn in ROW (overall volume declined by ~22.7%)

- Higher realizations are because of better product mix where company is benefitting from newer molecules that have higher realizations, even though blended volumes are lower because of older molecules whose volumes are high but realizations are low

- Gross margin breakup: EU (29% vs 33% last year), NAFTA (26% vs 28% last year), LATAM (24% vs 15% last year), ROW (30% vs 20% last year)

Changes made to counter forex issues

- Focusing more on NAFTA region (shown in increase in contribution to 40% of agchem sales which is almost same as EU). NAFTA + EU accounted for 81% of agchem sales in Q2FY23

- Sourcing more in Euro, not easy to simply change currency of procurement

- Improving hedging

- Passing on price increase to customers

Its good that most of these forex issues have happened in first half of the year, as Sharda gets most of its business during second half of the year (mostly in Q4).

About other points being made on hedging, I dont think it will be as beneficial as its being made out to be as Sharda’s core business is to play on currency differential. They buy products in USD and sell them after a few months in Euro, so a large part of their margins in captured in this differential. They will need to pay 3-6% on hedging and also will need to take a directional call on currency. Currently, they are getting the stick which can also get reversed in the future. Over longer periods, this is not what they should optimize for.

Their focus should be on getting more registrations, increasing customer base, and improving contribution from better markets (in terms of realization and working capital). They have done all this, their US + EU contribution was 80% of Q2 agchem sales which speaks a lot about business execution. Also, given the fact the biggest quarter is still sometime away, the full year nos can change significantly.

Disclosure: Invested (position size here, no transactions in last-30 days)

9 Likes

There was a recent interview with Sharda cropchem management who said that the currency losses they had faced in H1 are likely to reverse due to increasing Euro vs USD. If we look at Euro vs USD, Euro has recovered somewhat in the last 30 days.

More importantly, their nos are Q4 heavy. If Euro keeps on strengthening, not only will H1 losses reverse, but they will be benefitted from higher revenues in H2FY23. Lets see how future unfolds. Notes below.

- Euro is recovering against USD, H1 currency losses of 82 cr. are notional in nature and should reverse if Euro keeps on strengthening

- In constant currency, they had 20% growth in H1FY23

- Agchem sales are growing very well in Europe and USA

- Non-agchem products are doing better than agchem in terms of sales and margins

- Capex will be ~450 cr. in FY23 and will be maintained in 400-500 cr. in next 2-3 years

Disclosure: Invested (position size here, bought shares in last-30 days)

14 Likes

@harsh.beria93 - The Covid lockdown in China which is a primary supplier of the material for Sharda, can probably cause dent in the Sharda’s performance?

4 Likes

Looks quarter results are good and agchem has recovered well.

Sharda came with good set of results, with sales growing by 16% and EPS by 6%. Margin pressure due to Euro vs USD is reversing and company’s notional loss reduced significantly this quarter. The one positive thing about this Euro vs USD fiasco was that it happened in lean quarters for Sharda, and now that we are getting into the better part of year this trend is reversing. Additionally, company has done exceptionally well to pivot the business towards US. Concall notes below

FY23Q3 concall

- Expect 15-20% in sales and profitability in FY23

- Capex: 300 cr. in 9M FY23

- For Q3, volume (+) 9%, price & product mix change (+) 6.7%

- Gross margin breakup: EU (35.5%), NAFTA (28%), LATAM (24%), ROW (27%)

- Entered biocide segment for disinfectants

- Have gained significant market share globally in last few years

- Working capital will come down

- Quality and timely servicing is the reason behind very good performance in non-agrochemical business. Their belts mostly go into material handling (ports, mining, etc.).

- Suppliers quoted very high prices for sourcing in Euro. So company kept on sourcing in USD and are now benefitting from Euro strengthening

One of the reasons that can explain Sharda doing so well over years is due to their supply chain sourcing and execution. The only Indian agchem companies that make more money than Sharda are UPL and PI Industries within listed universe (excluding MNCs). And all this growth has come from internal resources, without debt and consistent dividends, which have grown in line with business growth. Even during COVID year, their sales grew which is a testament to their execution. I have been surprised how good they actually are in terms of execution. And I keep on wondering why they trade at these multiples.

Disclosure: Invested (position size here, no transactions in last-30 days)

16 Likes

Was checking the monthly charts of the company for all periods on Chartink, this is what the chart looks like

and I checked to see if the equity base increased during the same period for reasons of corporate actions

The price chart does not look very impressive over the last 7/8 year period. Wanted to know your thoughts on it and what might change going forward.

Probably because of their cash flow?

EUR has appreciated vs. USD and almost back to FY22 end levels of 1.1, would that benefit financials through reversal of unrealised FX losses? Also, what’s the outlook on the company especially with reopening of Chinese economy post lockdown, which is the biggest market of its raw material sourcing (can RM cost come down and gross margin to improve)?

Has anything changed fundamentally as stock has seen decent correction?

@harsh.beria93 - Appreciate your expert opinion on how do you see prospects going forward and pls help me understand your investment thesis on Sharda at current valuations?

1 Like

Selling pressure continued today and infact stock had touched intraday low of 416 (-15%). I believe Q4 should be good given expected FX gains and margin improvement.

However, stock has corrected sharply over past one week and is now trading at undemanding PE multiple of <13 on trailing basis (ROE more than 20%). Relatively, at discount with peers PI and UPL, which are trading at 40x PE multiple. Why is it trading at so much discount vs. peers, despite consistent EPS growth and healthy ROE? What am I missing?

1 Like

Can you elaborate? Their working capital has stayed at 35% of sales for a long period of time.

Also, their CFO/EBITDA and CFO/PAT are better than industry averages.

Thats true, Euro has completely recovered vs USD.

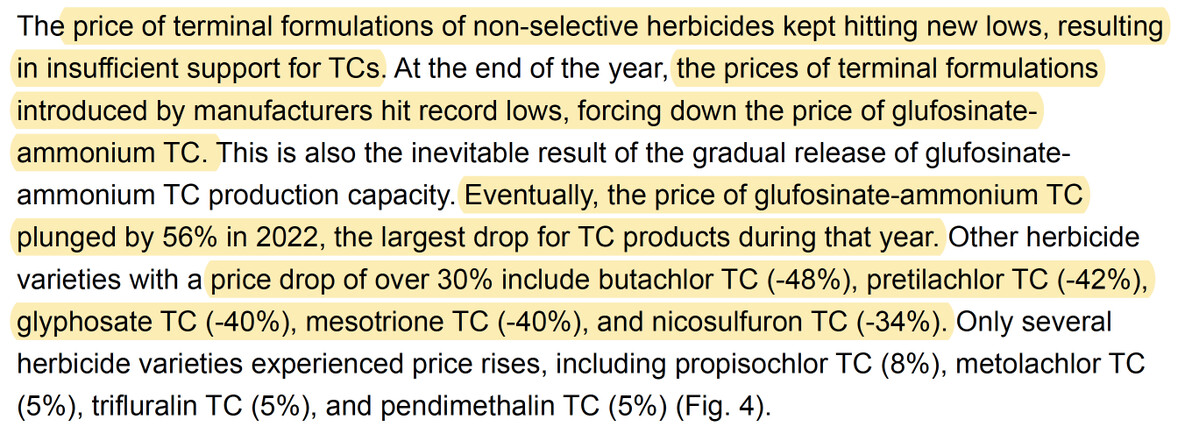

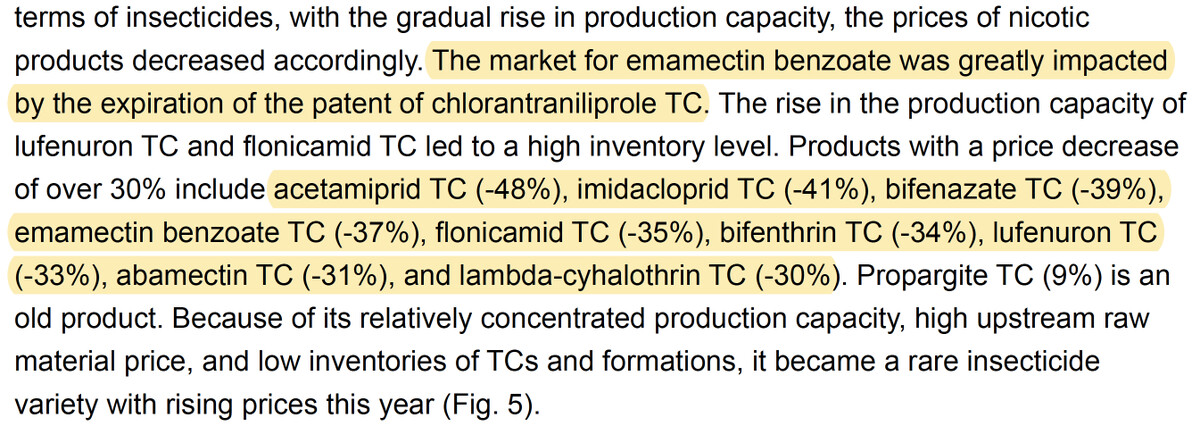

More importantly, end product prices have not corrected much and technical prices have corrected by 40-50% for major molecules (see examples below). This should be materially positive for Sharda

Disclosure: Invested (position size here, no transactions in last-30 days)

7 Likes

- I was going through some concall and Mr. Buba explained the the average payback period where they recover their investments in registration is 3 yrs.

However when I look at the Return on Assets, it is around 10%.

So, going by RoA, shouldnt the payback period translate to 10 yrs ?

Am I missing something here ?

- how long on average are the registrations valid ?

What do you mean by short term arbitrage? Do you intent to gain from currency movement?

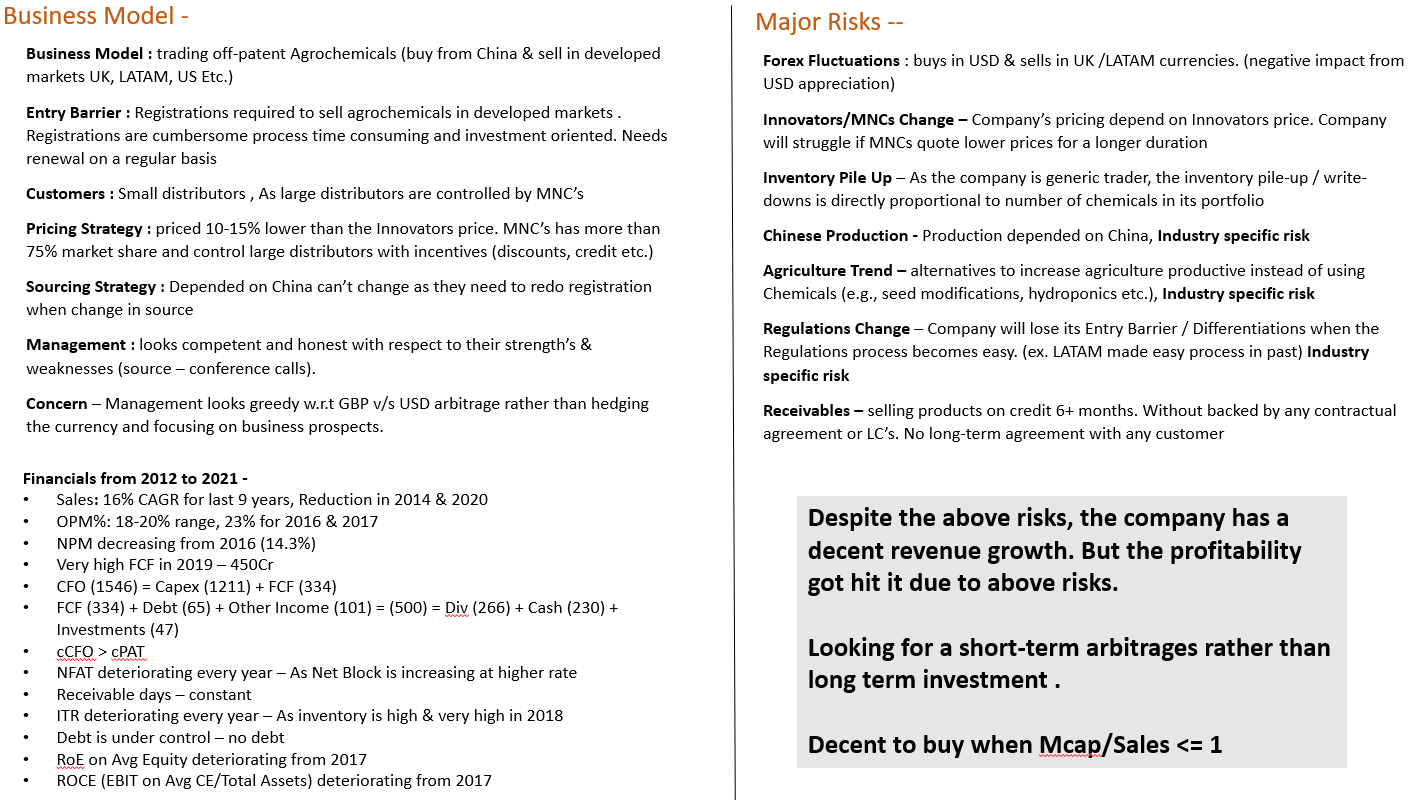

I’ll buy this when the Mcap is less than sales .and sell with 30-40% appreciation . For a short duration .

Sharda came out with reasonable results (3.3% sales growth and 12% EPS growth) which look especially better if one looks how other the results of other agchem cos have panned out. In H1FY23, they were impacted by foreign currency losses which reversed to a certain extent contributing to improvement in margins in H2FY23. Management feels confident of achieving 15-20% growth in FY24. Concall notes below.

FY23Q4

- For FY23, volume (-)4.6%, price & product mix change (+)15%, currency exchange (+)2.5%

- For Q4, volume (-)3%, price & product mix change (+)2%, currency exchange (+)4.3%

- Gross margins improved due to higher European sales

- FY24 growth: 15-18% with 18-20% EBITDA margins and 30% gross margins

- Gross margin breakup: EU (36%), NAFTA (24.5%), LATAM (26.5%), ROW (22%)

- FY23 capex: 355 cr. (~400 cr. in FY24)

- Forex losses of 58 cr. forex losses in FY23 (82 cr. losses in H1FY23 offset by 24 cr. gains in H2FY23)

- NAFTA region is facing hardships which has resulted in inventory challenges which has also resulted in higher working capital. Higher inventory for Sharda is largely in NAFTA where margins may suffer. In other markets, Sharda’s inventory is low and they should benefit from lower technical prices

- Reduction in PPE (from 14.4 cr. in FY22 to 5 cr. in FY23) is due to depreciation of leased assets

- Chinese prices have seen a lot of correction in last quarter and this will have positive impact on Sharda’s business (volume + margin wise)

- Other expenses increase is due to general inflation in Europe

- Better performance vs peers is due to more nimble business model where they don’t have fixed manufacturing costs

- In newer products, competition is very low and margins are higher for Sharda

- Cost of registrations have increased by 20-100% in past 3-4 years

- Don’t drop prices more than 10% vs innovator prices

Disclosure: Invested (position size here, no transactions in last-30 day)

11 Likes

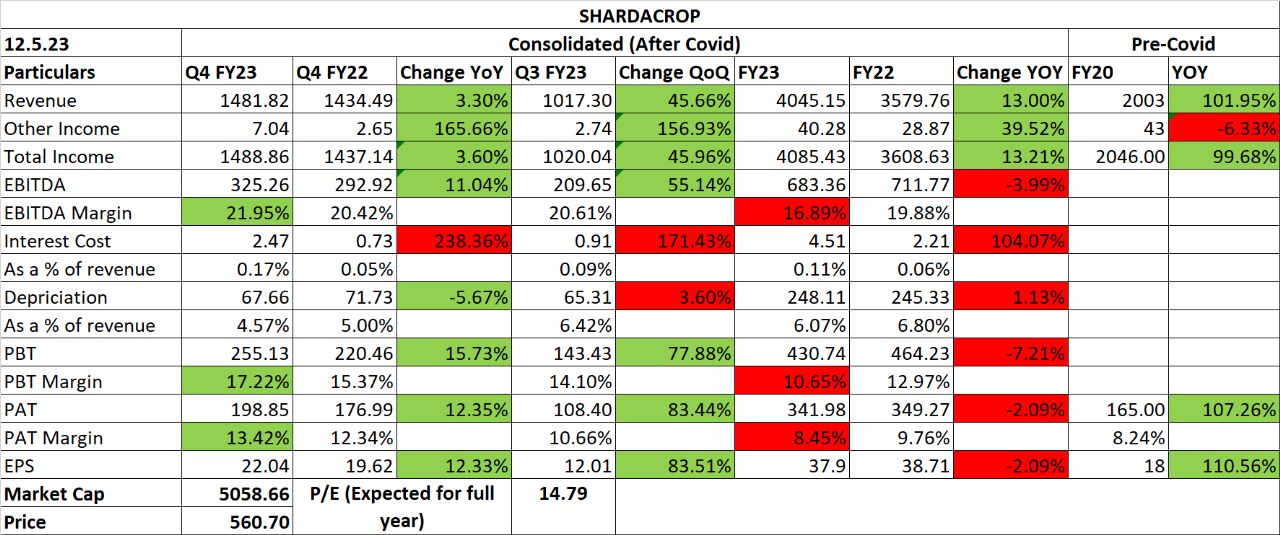

SHARDACROP Q4 FY23 Result Update:

Way Forward:

- Forward Integration: Build Sales Force

- Continual Investment in Product Registrations

- Focus on Operational Efficiencies (Margin improvements & better cost management)

- Expand & Strengthen Distribution Presence

Highlights:

- Revenue growth led by better product mix & price realization in Q4 FY23.

- Gross Margins have improved by 240 basis points due to increased sales in Europe and better margins in Q4 FY23.

- EBITDA margins reduced due to increase in local freight costs in Q4 FY23.

- Favourable impact of Forex gain.

- Gross Margins have been impacted by weakening of €/$ leading to increased input cost mainly in H1 FY23.

- ROCE & ROE have reduced from 25.7% to 20.8% YOY and from 19.8% from 16.5% YOY respectively.

- Debt reduced from Rs. 38 crores to Rs. 3 crores YOY.

- Cash increased from 300 crores to 328 crores.

5 Likes