Hi All,

Good to see company adopt practices like concall & investor presentation.

There were many interesting insights in the presentation…sharing my notes below.

Regards,

Yogansh Jeswani

Disclosure: Invested

Hi All,

Good to see company adopt practices like concall & investor presentation.

There were many interesting insights in the presentation…sharing my notes below.

Regards,

Yogansh Jeswani

Disclosure: Invested

Did anyone attend and take notes from yesterday’s con call?

Would be obliged if shared.

Thanks

It’s available on YouTube : SANDUMA Stock | Sandur Manganese & Iron Ores Ltd Q4 FY21 Earnings Concall - YouTube

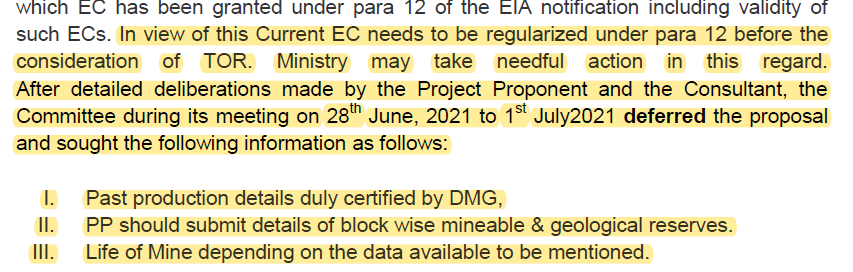

EAC meeting was held on 28th June to consider TOR for planned expansion of iron ore production by Sandur ltd.

From the committee recommendation it’s clear that they deferred the proposal and asked for few more details including the regularisation of current EC (key thing awaited by investors for the stock to get rerated).

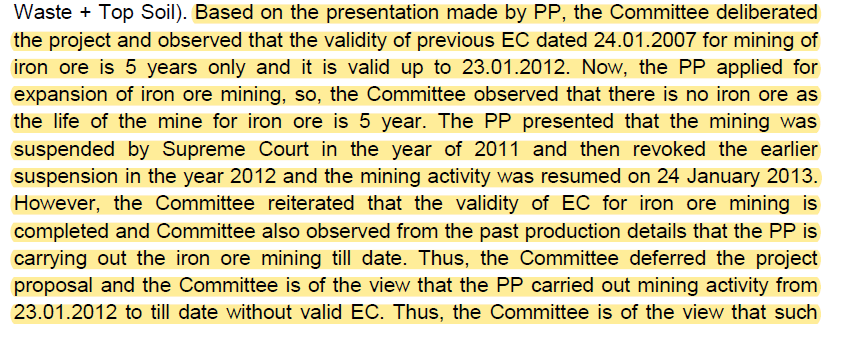

Another observation made by EAC is the validity of EC for iron ore is completed and the company has carried out mining activity from 2012 to till date without valid EC and the ministry may take further necessary action.(not sure how important is this observation considering the Sandur ltd compliance track record)

I have mailed company to get clarity on validity of EC clearence for existing iron ore production.

Hi, I have been following these proceedings closely and i think the question over the validity of their mines was raised earlier (cpl of years back) and this was the key reason why their application for expansion has taken so long. The co had to go through the agni-pariksha all over again and came out clean. The biggest positive for them was the SC document which itself appreciated the good practices followed by Sandur and that its one of the few A category mine in India which has done all the compliances and not done any exploitation.

Last Feb 20, the EC website was showing that TOR is approved however now there is again some requirement raised. The recent concall of the company was held after the above EC meeting and company seemed positive of getting approval by end of this calendar year. Lets see how it goes. Keeping fingers crossed.

Ayush

Disc: Invested in family codes and PMS.

Phenomenal results!!!

Credit rating has been upgraded:

Detailed Rationale

CRISIL Ratings has upgraded its rating on the long-term bank facilities of The Sandur Manganese and Iron Ores Limited (SMIORE) to ‘CRISIL A/Stable/CRISIL A1’ from ‘CRISIL A-/Stable/CRISIL A2+’.

The rating upgrade takes into account CRISIL Ratings’ belief that the business risk profile of the Company will continue to improve over the medium term, benefitting from ramp up of recently completed coke production facilities. This is likely to aid in diversification in the product portfolio.

The Company has setup coke production facilities with capacity of 0.4 Million Tonnes Per Annum (MTPA) and this became entirely operationalized from January 18, 2021. During fiscal 2021, the Company’s revenue grew by 26% to Rs 746 crore over the previous fiscal, on the back of contribution from sale of coke and also better realizations on iron-ore, ferro-alloys and manganese ore. The Company is likely to report strong growth in the current fiscal, with already reporting Rs 475 crore of revenues in first quarter of fiscal 2022 (year-on-year growth of 270%), despite the second COVID wave impact. Demand for metallurgical coke is likely to remain strong supported by the steel entities located in Ballari (Karnataka). Operating profitability has improved last fiscal, with contribution from coke sales, which has higher margins. This is likely to continue, coupled with sustenance of higher realization on other products. As a result, the cash accruals are likely to remain strong and over Rs 350 crore over the medium term, which will support any capital investments and also further strengthen financial risk profile.

SMIORE’s financial profile continues to remain strong, with gearing of 0.37 times as on 31 March, 2021, despite the company completing a debt funded capex. Further, the company has strong cash and equivalents of Rs 352 crore as on same date and this will support the liquidity going forward.

The rating continues to reflect a strong market position with a track record of more than six decades and large mining reserves and strong financial risk profile. These strengths are offset by susceptibility to heightened regulatory risks and vulnerability of operating margin to commodity prices.

Here are some notes from ICRA’s rating report.

• Produces iron ore with Fe content of around 58-60%, with lump to fine production ratio of 1:2

• Increased ferro-alloys capacity from 36,000 MTPA to 48,000 MTPA in FY21

• Signed MoU with pig iron manufacturer in Karnataka to sell 50% of its coke output on a conversion basis

• Contingent liability: Primarily includes disputed income tax claims of 68.4 cr. and payments related to forest development tax of 68.2 cr. as on March 31, 2021. Has been paying income tax claims under protest

• Repayment obligations of 57 cr. in FY22

https://www.icra.in/Rationale/ShowRationaleReport/?Id=106188

Disclosure: Not invested

Did anyone attend yesterday’s AGM?

If yes, would be grateful if any notes could be shared.

Basically, I am curious about:

Hey @django, I attended the AGM. Sharing my notes. (These are running notes that I took and I may have missed something or misheard something).

They feel that high iron ore prices may sustain a bit longer despite the huge fall in global iron ore prices.

On coke, they mentioned that Coking coal (their RM) prices are through the roof (same thing mentioned by Kirloskar Ferrous).

On Iron Ore EC-

Govt authorities had raised questions on the validity of the old EC and the mines. The same has been regularised and recognised by the authorities as per the laws and no illegality was found. (This seems to be a huge positive and perhaps was the reason for the delay).

Next EAC meeting is scheduled at the end of this month and they are hopeful of getting the EC by the end of this Calendar Year.

Once they have the EC they need to get approval from some authority for production enhancement. This is applicable only for Miners in Karnataka.

They seemed confident about having everything in place by the end of FY22 and hope to begin operations by Arp’22.

Once they have the EC and necessary approvals, scaling up should be easy as machines will be hired and they will have to incur very minimal capex. It seems that they can quickly scale up to 2.5-3MT as was mentioned in the concall.

Forest clearance is till 2026 for now however as per laws the same is deemed to be valid till the life of mining lease. Hence, they don’t see any problems with getting the same extended.

Manganese Ore expansion should also happen with the scaling up of Iron Ore operations.

On their Ferro Alloy operations-

Other Miscellaneous insights-

These are some of the highlights that I could take note of. Would appreciate it if others who attended the AGM can add to it and point out if I have misunderstood something.

Minutes of latest EAC meeting is updated in environment clearance website.

As the Forest Clearance (FC) obtained on 14.03.2007 is valid for 20 years i.e. till 13.03.2027, hence PP may approach to Ministry for working in forest land beyond 13.03.2027”.

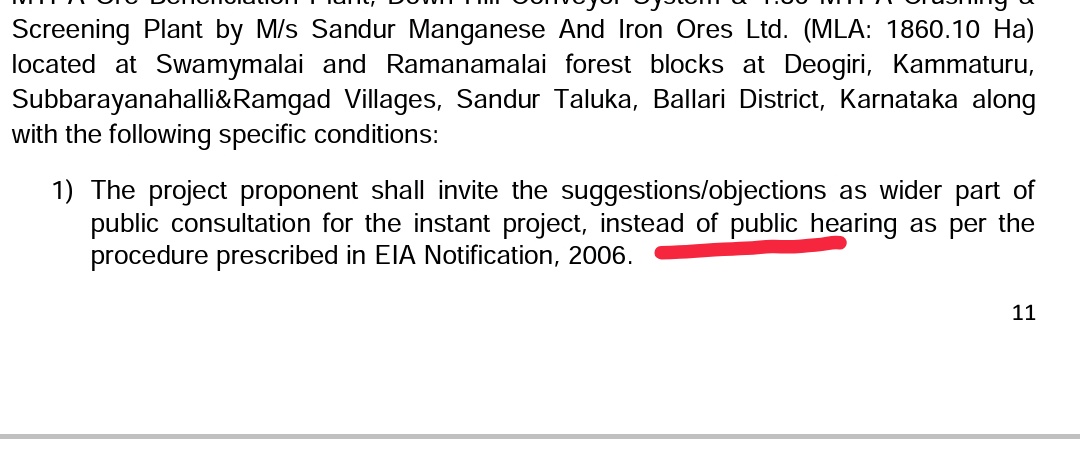

Hence, the Committee feels that the project proponent shall invite the suggestions/objections as wider part of public consultation for the project, instead of public hearing as per the procedure prescribed in EIA Notification, 2006.

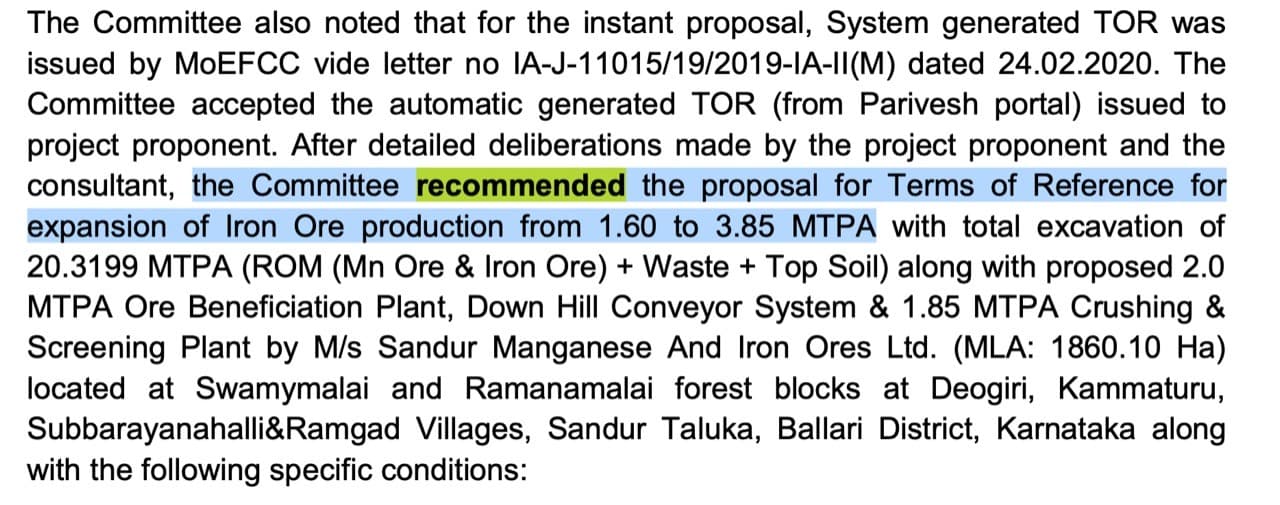

MoM also mentioned that the committee Recommended for TOR for expansion with some specific conditions:

After detailed deliberations made by the project proponent and the consultant, the Committee recommended the proposal for Terms of Reference for expansion of Iron Ore production from 1.60 to 3.85 MTPA with total excavation of 20.3199 MTPA (ROM (Mn Ore & Iron Ore) + Waste + Top Soil) along with proposed 2.0 MTPA Ore Beneficiation Plant, Down Hill Conveyor System & 1.85 MTPA Crushing & Screening Plant by M/s Sandur Manganese And Iron Ores Ltd. (MLA: 1860.10 Ha) located at Swamymalai and Ramanamalai forest blocks at Deogiri, Kammaturu, Subbarayanahalli&Ramgad Villages, Sandur Taluka, Ballari District, Karnataka along with the following specific conditions:

- The project proponent shall invite the suggestions/objections as wider part of

public consultation for the instant project, instead of public hearing as per the

procedure prescribed in EIA Notification, 2006.

Minutes of 38th EAC Meeting (Non-Coal Mining) held during 29th – 30th September, 2021.- The project proponent shall address all the concerns expressed by the public in

the year 2010 as well as latest concerns recorded during public consultation in

the EIA/EMP report.- The project proponent shall incorporate the EMP for public hearing concerns with

the capital investment as per the project cost, also to be defined in a tabular form

with measurable and verifiable capital investment in the EIA/EMP report.- The project proponent should look at different blocks and if there is a proposal of

creating water bodies, then water harvesting and water utilization should also be

studied in the EIA/EMP report.- The project proponent shall incorporate EMP for plantation at the site that should

be based on validation done for the existing capacity and consultant must show

that the augmented EMP is adequate to handle the expansion capacity.- The project proponent shall incorporate the details of Wildlife Conservation Plan

in the EIA/EMP report.- The project proponent shall obtain the certified compliance report from regional

office of the Ministry and incorporate the same in the EIA/EMP report.

So it looks like company didn’t get direct exemption and now have to go through Public consultation procedure as mentioned in EIA notification,2006. This would be inviting further delays. But how much ?

EIA notification 2006 says :

(ii) The Public Consultation shall ordinarily have two components comprising of:-

(a) a public hearing at the site or in its close proximity- district wise, to be carried out in the

manner prescribed in Appendix IV, for ascertaining concerns of local affected persons;

(b) obtain responses in writing from other concerned persons having a plausible stake in the environmental aspects of the project or activity.

Of the above, part (a) is waved off by EAC and part (b) needs to be conducted by the concerned regulatory authority and the State Pollution Control Board (SPCB) or the Union territory Pollution Control Committee (UTPCC).

Procedure for obtaining Public respose as per EIA Notification is :

For obtaining responses in writing from other concerned persons having a plausible

stake in the environmental aspects of the project or activity, the concerned regulatory

authority and the State Pollution Control Board (SPCB) or the Union territory Pollution

Control Committee (UTPCC) shall invite responses from such concerned persons by

placing on their website the Summary EIA report prepared in the format given in

Appendix IIIA by the applicant along with a copy of the application in the prescribed form,

within seven days of the receipt of a written request for arranging the public hearing.

So it looks like that the public consultation is just for the sake of formality. But there may be surprises as it is a matter involving government agencies.

Given the matters above I feel that starting production may take a little longer.

Disclosure : Invested and biased

Interesting piece of Information from Concall on Question Related to Reserves, its Validity and annual Production:

Currently company have established reserves of 110 million tonnes of iron ore and 14 million tonnes of manganese ore. And our mining lease is valid till 2033. Based on our current expansion of environmental clearance we will be operating at plus 3.5 million tonnes of iron ore production. And currently we operate at 0.28 million tonnes of manganese ore production per annum and there is scope for that also to go up.

Thanks for bringing this to notice @Prash. I personally think this is very positive development for the company. They had been wanting to expand since a decade but due to multiple issues (earlier SC ban on industry) and later their application was stuck for last 3-5 years. And probably there was a feeling that something is wrong and they might not get this approval. But finally things seem to be falling in place:

If what we are seeing above is right then hopefully the final approval should come in next 3-6 months (if there are no negative surprises) and like the company has mentioned in concall and AGM, probably they can increase production next year.

Cheers,

Ayush

Disc: Invested in family accounts and clients accounts. I could be wrong or biased.

Management doing what they said earlier, full pledge on the promoter holding has been released.Sandur.pdf (681.8 KB)

Huge quarter! Sandur is minting money.

Balance sheet is also seeing big changes.

As on Sep, 2021, company has amassed ~ Rs 819 Cr of Cash + Other Bank balance + Current investments.

Total debt came down to ~Rs 337 Cr (Long term + short term) (This does not include current portion of long term debt)

Net liquid funds of ~Rs. 482 Cr (vis-a-vis Market cap of ~Rs 1920 Cr)

Waiting for commentary from management.

FY22 Q2.pdf (5.1 MB)

Till when will Mr. Market ignore Sandur ? I am very bullish on the stock, any pointers on what could the multiple be re-rated to?

How do we compare Sandur with Maithan?

Is it currently at a more attractive valuation?

@ayushmit sir,

I am slightly confused by the notification on Nov 17

It says “company has to conduct public hearing once again” .

This is contrary to the minutes of meeting uploaded on 28th October.

Gentlemen, Any thoughts on the below questions:

In ARs of FY10, 11 & 12, company mentions about board’s approval in place to set up: Iron Ore BENEFICATION plant, Medium sized special alloy steel plant, & 4km ropeway. However, management stopped communication about above goals in later ARs. I assume that Supreme Court’s order to suspend/limit the mining operations in Karnataka from FY11 till FY17 made these unviable. Is it so?

From FY10 till FY13, company tried TMT bars manufacturing as per arrangement with a local mini steel plant but the business could not scale up or make profit. Why so? How it will be different when steel mfg. comes in house?

While permitting to open the mining activity in 2013, Supreme Court prescribed implementation of Supplementary Environment Management Plan (SEMP). What’s the latest progress on the same as ARs do not provide the details? Progress on this is important as company needs to scale up this program as one of the pre-requisite to establish a steel plant?

What led to difficult times for almost ten years from 1996-97 till 2006-07? SMIORE was eventually discharged from BIFR in January 2007.

What’s the steel project, say phase-1 implementation and production start, timelines? Steel plant is a project under discussion from FY10 onwards.

What’s your expectation about the bottom line (with existing mining capacity) incase current up cycle ends?

Trust the keen follower of the story- @ayushmit, @django, @aga.ayush11- would share their thoughts.

@prasobh - yeah…a bit confusing. If its only public consultation, the timeline reduces.

Surender. Few thoughts on your questions:

1 & 2 - I think the co got big nos at that time and started planning multiple things. However, none of them happened due to the SC ban on mining and next few years were a setback due to this and all the time went in resolving the same. Most of the plans of those time seem to have been dropped.

4 - The reason was the change in govt incentives and policy for ferro alloy sector…the whole thing suddenly became un-compeitive. They did sell their land etc to make payment to bankers etc and resolve. The same was covered in this management discussion I think - https://www.bseindia.com/xml-data/corpfiling/AttachHis/e2e5100e-c53b-4312-a8d7-666a97ef1e4b.pdf

5 - I think they want to do the steel project to safeguard their huge mining resource and hence have been going slow and probably the same will be spread out depending on cash flows and balance sheet.

6 - interestingly international iron ore prices have crashed and are back to the point where the whole rally started. Yet in India the prices are still more than 50% higher than the average of last 5 years or so and perhaps the reason is the structural change in Indian mining industry where the cost of mining has increased a lot for new players (due to very high premiums on auctions and higher royalty). If this trend is correct then company can do much higher profits than before plus they now have 2-3 new segments like coke and ferro alloy.

Disc: same as before