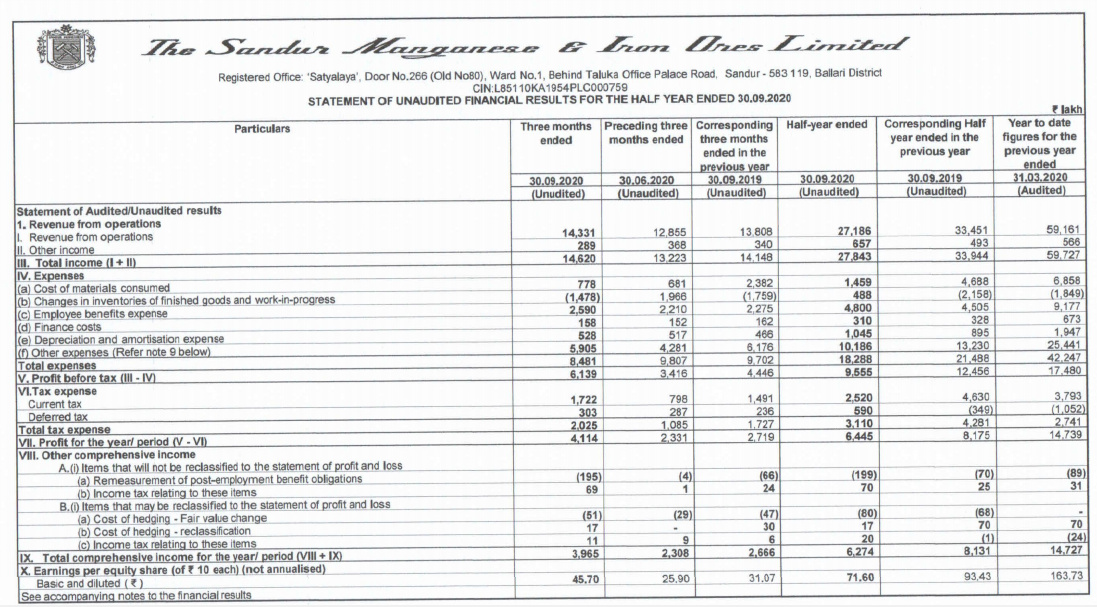

Outstanding Q2:

Disc: Invested

I have some querries regarding the CAPEX shown by company and the investment @basumallick @ayushmit sir could you please help me to understand

Second : if one study over the years of the ration “Working Capital/Sales” i found that it is on increasing trend so my interpretation is that company require high working capital . Does high WC means losing opportunity cost ??

several mines were closed in 2011 due to illegal mining issues and eeven after supreme court gave node to reopen still it takes lots of time to make them operational There is no surety that it won’t pop out again what kind or safety one can take against such regulatory actions by state govts or environmental activist ?

Hi @yourraj - my answers to your queries:

Thanks for your reply I have another concern as the health hazards in Sandur Taluk are at its peak due to mining with many people being subjected to deadly health conditions on a daily basis. I come across a web link http://newsnet.iijnm.org/health-hazards-a-haunting-reality-in-sandur/

Isn’t the organisation must be win win for all stack holders in long terms for suppliers / workers / clients …

sharing for VP brief of Leases environmental clearances : http://environmentclearance.nic.in/writereaddata/Online/TOR/08_Jan_2019_1717553776OAGT4IMAnnexure-briefnote.pdf

Hi @yourraj - thanks for sharing this, I was not aware neither have I come across more of such articles. Mining is a very very old industry and there would be some positives and negatives. Sandur seems to be much better off when compared to others in terms of compliances and taking care of employees (if you go through annual report, website etc, you will notice that they spend good amount on employee welfare) yet there may be some adverse cases. Going forward, co seems to be investing more into new technology and compliances while they aim to double their production capacity.

The link you have shared above is old. There are several new documents available on EC website which are useful reads.

Link to Sandur presentation and transcript details discussed in VP virtual meetup on Oct 30, 2020.

SMIORE has already started operating Coke Oven.

For those who are not from the industry, Coke Oven produces waste gas as a by-product which can be used to produce power. Such power’s cost is substantially low around < 1 Rs/ kwh.

Now even though the Coke Oven is not shown as commissioned (i.e. the CAPEX is still shown as CWIP), the benefit of lower power cost can be seen from turn-around of Ferro Alloys business. It has started churning out profits - which is irrespective to what happens to iron ore price.

Hence expect it to continue to add to profits.

Further, as and when the company recognizes Coke sales, there will be substantial jump in topline and bottom-line. Again this is irrespective of what happens to iron ore price in the market.

Given this background, SMIORE is looking very interesting.

Discl. Invested and still adding to my position.

I was in Kirloskar Ferrous (KFIL) concall last week to understand more about their coke-oven operations. Sharing a few insights about the same-

Now, in reference to Sandur, they are also setting-up a 4L Tonne coke oven with WHR at lower cost than KFIL; the cost for Sandur is around 400-450cr. This process of converting heat into power seems to be working for KFIL and there is no reason to believe that it won’t work for Sandur. KFIL is already seeing benefits, their power cost has come down meaningfully. In fact, Sandur has already tied up with a company for 50% of their coke off-take on a fixed cost conversion basis. This company could very well be KFIL, since both have operations in Karnataka and the quantity matches. This will add a lot of value to their ferro alloy operations which was loss-making and will allow them to increase their production as well. Apart from the power benefit, sales from coke should itself generate 10-13% EBITDA as indicated by the management.

Another interesting development that I came across was that Kalyani Steels is also setting up a 2L tonne coke-oven plant along with the WHR at the cost of 211cr that will be ready by Sept’22.

Disc: Invested at lower levels.

Sandur FY21 Q3 was not as per my expectations.

I was hoping Ferro alloys division to show profits by virtue of lower power cost due to Coke oven - however, it has slipped into losses as earlier.

Will try to connect with management to understand what happened.

However, I would still be hopeful for FY21 Q4 - as Coke oven sales impact will be visible in this quarter.

Commercial operations at the 0.4. MTPA Coke Oven Plant and Ferro Alloy Furnaces have commenced w.e.f. 18 January 2021. So, the power cost benefit will be added to the numbers starting Q4 results is my assumption.

Sub: Announcement under Regulation 30 of the Securities and Exchange Board of India

(Listing Obligations and Disclosure Requirements) Regulations, 2015- Commencement of

Commercial Production for Phase I of 1 MTPA Iron and Steel Project

Attention is drawn to our earlier announcement dated 20 March 2018 informing about Bhoomi

Puja and Foundation Stone Laying Ceremony for Phase I of 1 MTPA Iron and Steel Project entailing

setting up 0.4 MTPA Coke Oven Plant, Waste Heat Recovery Boilers and 0.4 MTPA Pig Iron Blast

Furnace at Vysanakere, Hosapete on 19 March 2018.

Trials from Batteries 1 & 2 of the Coke Oven Plant commenced in January 2020, new 24 MVA Ferro

Alloy furnace in February 2020, Batteries 3 & 4 of Coke Oven Plant from November 2020 and

refurbished 20 MVA Ferro Alloy Furnace from 18 January 2021. Accordingly, the Lenders’ Engineers

have completed their visit to the Plant yesterday and are expected to issue a certificate to the Bankers regarding completion of the Project and declaration of the commercial operations w.e.f. 18 January 2021. Performance Guarantee Tests will be taken up in due course of time.

In compliance with the provisions of Regulation 30(2) of Securities and Exchange Board of India

(Listing Obligations and Disclosure Requirements) Regulations, 2015, we wish to inform that the

commercial operations at the 0.4. MTPA Coke Oven Plant and Ferro Alloy Furnaces will be

considered to have commenced w.e.f. 18 January 2021.

The Exchange is requested to take the same on record.

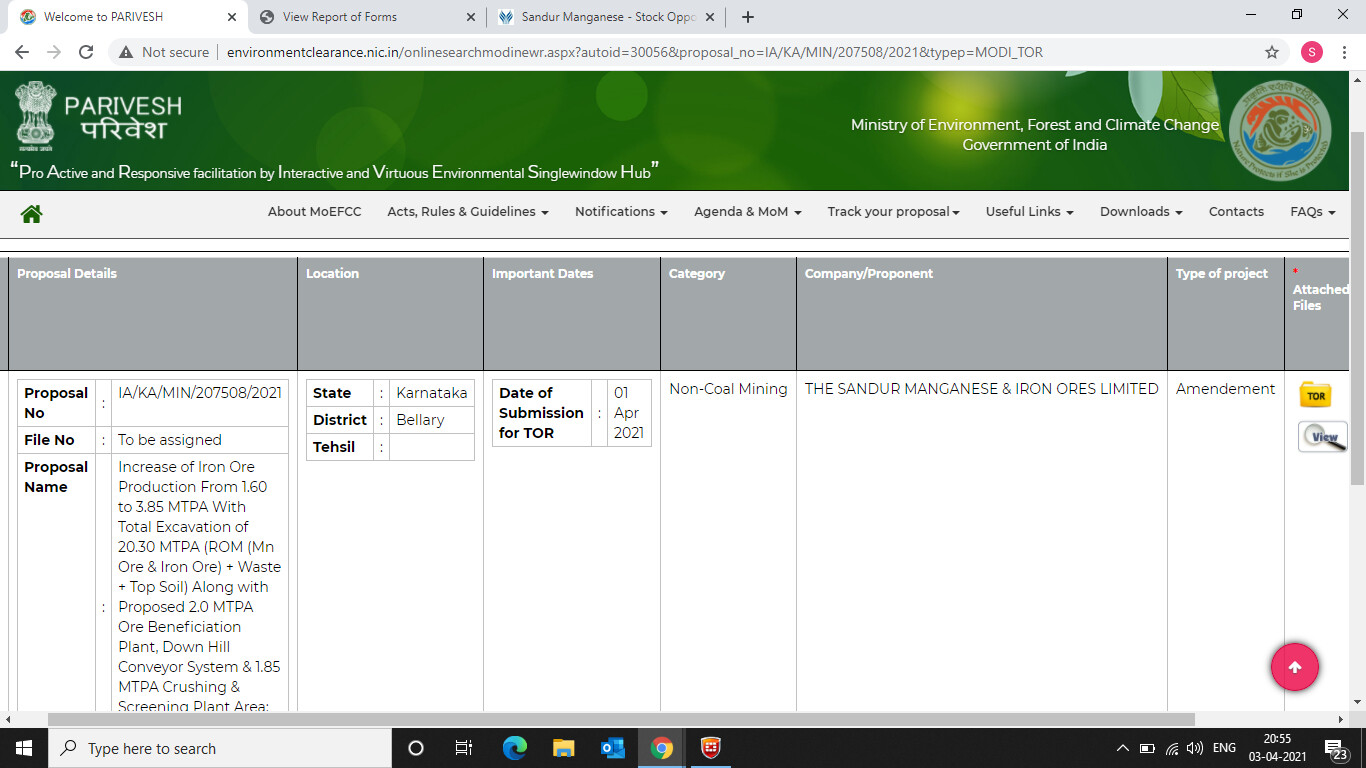

Update on Increase of Iron Ore Production From 1.60 to 3.85 MTPA

Sandur has submitted amended Terms of Reference (TOR) dated 01 April 2021 seeking exemption for Public hearing as it was already conducted for same proposal on 30th April, 2010. And the proposal was pending due to Hon’ble Supreme Court Strictures on Mining in Bellary area during that period.

If exemption is granted then we can expect a faster EC on expansion of iron ore extraction.

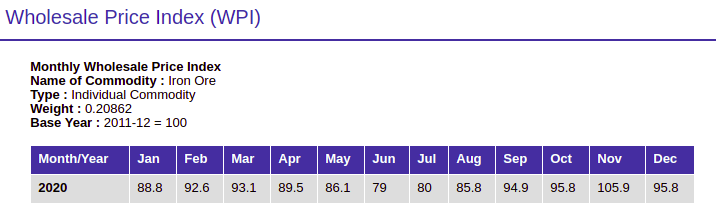

Another round of increase in Iron Ore prices in India - https://www.bseindia.com/xml-data/corpfiling/AttachLive/a2c96487-17c1-440b-b14d-5bdeee93c80f.pdf

This should bode well for domestic miners.

Iron Ore prices mentioned in this June announcement is the same as in last month’s (12th May) announcement:

https://archives.nseindia.com/corporate/NMDC_12052021121028_prices.pdf

Sandur has been placed in ASM LT Stage 1.

Any views on how it would impact the stock or its perception in the market?

Finally some coverage -Monarch Networth Capital comes up with a buy on Sandur with 62% upside !! not uploading the report here as I am not sure whether its paid report or not (though I got the report as whatsapp forward ) .

Discl :Invested

The report is available free here:

https://vid.investmentguruindia.com/report/2021/June/MNCL-SandurManganeseandIronore-Stock-Idea.pdf

Stupendous results!!

Coke oven has come in as a shot in the arm.

Fe-Alloys division has sprung into profits.

FY21 EPS is 171 Rs/ Share (as compared to 126 Rs estimated in the Monarch report earlier)

FY22 full year EPS could be much much higher as this will be first full financial year for CO and revamped FeAlloys div.

Around 38 Cr of Debt repaid between Sep to Mar period.

Highest ever dividend (10 Rs/ Share)

These show management’s confidence and intentions.

Hope to see more upside and more recognition to Sandur.

Sandur has given an excellent Investor Presentation, I think for the first time, way to go: