One last point about the change in process of lease renewal:

Per say AR 2015: The Government of Karnataka has vide notifications No.CI 214 MMM 2014 and No.CI 213 MMM 2014 both dated 23 September 2014 accorded sanction for third renewal of Company’s Mining Leases No.2580 and 2581 for extraction of manganese and iron ores over an extent of 2,837 ha and 378 ha in Swamimalai and Ramanamalai Blocks, Sandur Taluk, Bellary district for a further period of 20 years effective from 1 January 2014 and valid till 31 December 2033 under the provisions of Section 8 of the Mines & Minerals (Development & Regulation) Act, 195

In the meanwhile, the Government of India promulgated the Mines and Minerals (Development and Regulation) (Amendment) Ordinance, 2015 on 12 January 2015 under Article 123(1) of the Constitution amending certain provisions of the MMDR Act, 1957. The Ordinance seeks to bring in transparency and weed out discretion and accordingly, the grant of mineral concessions under the Ordinance shall only be through auctions. Unlike in the 1957 Act, henceforth, no renewal of any mining concessions shall be granted. Further, the tenure of the mineral concessions has been extended from the existing 30 years to 50 years; thereafter, the Mining Lease would be put up for auction (and not for renewal as in the earlier system)

Accordingly, the Company’s Mining Leases No.2678 and 2679 having been renewed with effect from 1 January 2014 are valid up to 31 December 2033

How does the above (change from discretionary basis to auction basis) impact lease renewal for the company at the due date (31 December 2033)?

A book keeping question: Fe Ore sold by SMIORE in FY 2020-2021 is mentioned as 1,592,000 in AR (Page 37, Director’s Report) whereas the same adds up to 3,644,000 Ton as per eAuction Bid Sheets (for Iron Ore’s ) available at GOK | Bidsheet .

Manually collated data from all the Bid sheets in below spreadsheet - Sand.xlsx (22.9 KB)

What am I missing?

My notes for this business -

What’s interesting?

Iron Ore scarcity due to non-opening of Category-C [~37 mines out of 46] mines after SC’s order

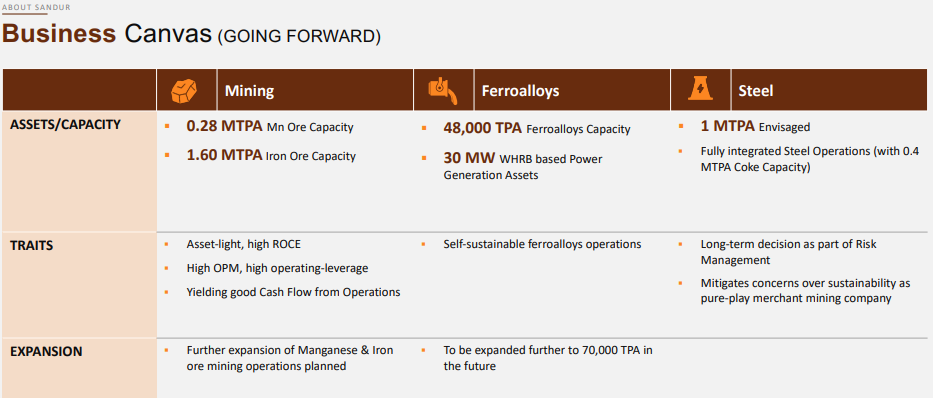

Stabilized Mining business with an ongoing license to operate the mines for ~12 Yrs

New source of revenue from Coke & energy

Improved Profitability of Ferro Alloy business due to in-house, cheap power source

Upcoming Events

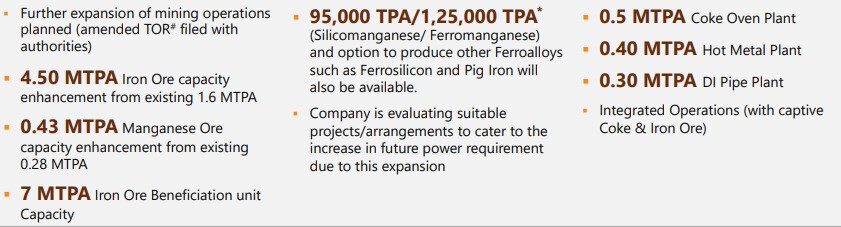

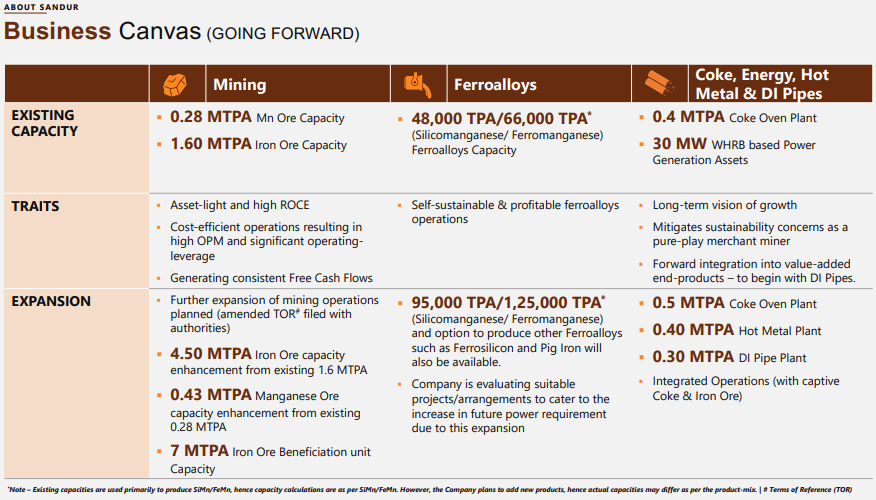

EC application for increasing the Mining Capacity [Fe Ore 1.6 to 3.85 mtpa; Mn Ore .28 to .4 mtpa]; Public Hearing recommended [In FY10, process took 1 Yr….How about now?]

Ferro Alloy [Si Mn] capacity Usage [48000 TPA to 70000 TPA]; Smelter capacity in place, Looking for power source

FC applied (Welcome to PARIVESH) for establishing Sinter Plant, Blast furnace and DI Pipe Plant [Phase-1 0.2MTPA] as well as increasing the Coking Oven Capacity [0.4 MTPA to 0.5 MTPA]

NSE Listing; Share Split

Keep in Mind

Dependency of all businesses on steel, which is in Up-Cycle.

Mining license Valid till 2033. What happens after that? Current Mining Policy - Open Auction for renewal. Steel Ministry’s Policy inclination - Ensure captive Raw material for the steel producer. Favorable Points: Journey to DI Pipe Mfg; Past record, Mine know-how

Ore from Karnatka - Sold by eAuction under the purview of committe as mandated by SC; Pellets made from Karnatka’s ore can not be exported or sold inter-state

Iron Ore Prices trend

Coking Coal Prices; Imported Raw material - Forex Risk

Disc - Still under due diligence. Started reading about Iron Ore, but now on the journey to read and understand about the entire value chain for steel.

got this from the environmental clearance website

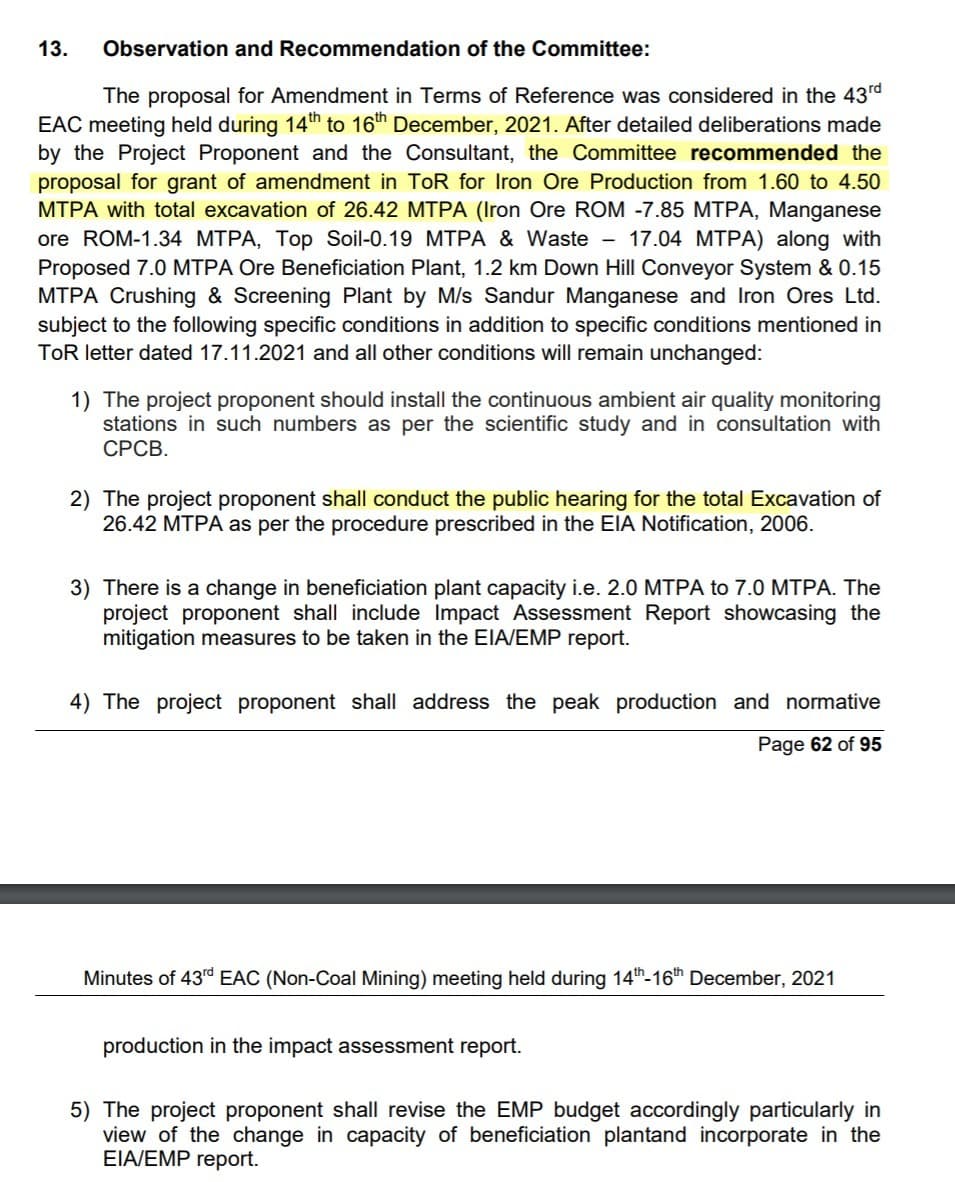

on 30th Nov 2021 Sandur has filled a proposal with the EC Increase in Iron Ore Production From 1.60 To 4.50 MTPA - earlier this was 1.6 to 3.85 MTPA. good to see the company increase it to 4.50 MTPA as they are not being exempted from public hearing they are being more aggresive to increase the capacity in one go. along with this also proposed to put 7.0 MTPA Ore Beneficiation Plant - this in interesting announcement as they are looking to put up a 7 MTPA benefication plant in one go. this will ensure that the extra iron ore they produce post the EC clearance will not be of degraded quality.

looks like the company is going to a much bigger scale in the next 2 -3 years .

Apart from this we will also have expansions in the ferro alloys capacity , and 1MTPA Steel plant in the pipeline.

Thanks for the update @Shikhar. Yes, it’s very interesting to see that the company is getting aggressive to mine out more iron ore given the huge reserves they have…this is a logical move. They have revised the application to increase output to 45 lac tonne from the current 16 lac tonne. The smart move is that this output will be of a higher grade as they would actually be increasing production by 5x to 75 lac tonne and will beneficiate the same and sell 45 lac tonne of a better grade. So the iron ore mining revenues can go up perhaps 3-4x once they get approval and they are able to scale up production. On the flip side, the government has asked them to go for public hearing and this delays the expansion by at least 6 months to 1 year.

As per the latest update on EC website, the govt authority has approved the recent application of the company to go for higher output, subject to public hearing etc:

Q3 results well in-line with expectations

Great to see Fe-alloys and Coke oven divisions continuing to add to bottom line.

I was especially worried about Fe-alloys division - was wondering whether its last few quarters profitability was a fluke. But now feel pretty confident!

I think these are pretty good nos. Q3 usually has had lower mining volumes (waiting for presentation for confirmation) plus the prices in India had corrected 30%+ in recent months after the huge rally over last 1 year. Even the current prices in India are very lucrative and Sandur makes fantastic margins being one of the lowest cost producer in India. Good thing is that iron ore pricing have started rising again on the back of a sharp rally in international prices. Another good thing is that mining is only 50% or so of the business and other segments have also done very well!

About the future - let’s see how things evolve. They are getting aggressive as they have laid out aggressive expansion but perhaps they need to work on quicker approvals.

some specific info about expansion plans…1L tpa increase in coke, new 4L hot metal plant 3L DI pipe, specifics of ferro alloys capacity expansion, 4.5 m iron ore and 7mn beneficiation plant…

Sandur has been running for last few days, while PE has reached ~18. Having said that iron-ore price are positive, Though I am skeptical on how much increase in EBITA/NP can be achieved until price stay firm or upwards and new mine open up

The company has received EC Approval for setting up 0.3 MTPA DI Pipe plant, expanding Ferro Alloy operations, and increasing the coke oven output to 0.5 MTPA from 0.4 MTPA earlier.

Some listed comparable companies in the DI Pipe industry are Tata Metalliks, Electrosteel Casting, and Jindal Saw. Sandur will be the only DI Pipe manufacturer with Captive Iron Ore which should give them a significant advantage if they are able to secure cheap power for which the company has mentioned in the earlier calls that they are working on some Renewable Energy sourcing.

The total capex outlay and timeline is yet to be officially communicated by the company but it looks like most of it can be internally funded given the huge cash generation in FY22 and expected cash flows in FY23.

Looking at the past average realisations of DI Pipe, with a 0.3 MTPA capacity, they should be able to do 1200-1500cr revenues at 90% utilisation with 15-18% margins (given Iron ore advantage).

Two interesting things to note in this EC-

They will be able to increase coke output by 20-25% without any additional cost. This should also help them generate some additional power from the WRHB.

The company having scaled up its current Ferro Alloy operations in a highly profitable way due to cheap power from the WHRB, is now planning to double its capacity by refurbishing an old furnace which should not cost more than 20-25cr. The incremental ROCE on this will be very high given captive Manganese Ore. How the company will source power for this is a key thing to monitor.

My guess is that it should take around a year for coke and Ferro Alloy to scale up and around 2-2.5 years for the DI Pipe operations. Stabilising the DI Pipe plant can be a challenge as seen in other listed companies. In the meanwhile, if they receive the Iron Ore expansion EC then consistent growth can keep coming in over the next 5 years.

For DI pipes manufacturing, two key raw materials are required i.e. Iron ore and Coking Coal/Coke. For Ductile Pipes manufacturing, more coking coal/Coke will be produced by Sandur and that will lead to more power generation. This power generation can be then used for more production of Ferro Alloys for which cheap Power is the key factor to remain profitable. Sandur is now very well integrated for all of its end products.