Sai Silks -

Q2 FY 26 results and concall highlights -

Company’s brands -

Kalamandir - Sell ethnic wear for middle income audience. Company operates a total of 11 Kalamandir stores ( large + medium + small format ) - across AP, Telangana and Karnataka. Price range of products being sold vary from Rs 1k to Rs 1 Lakh

Mandir - Sell ultra premium designer sarees. Price points vary from Rs 6k to Rs 3.5 lakh. Company operates 4 such stores ( small format stores ) in Telangana

Vraha Mahalakshmi - Sell premium ethnic sarees and handlooms for weddings and occasional wear. Price points vary from Rs 4k to Rs 2.5 lakh. Company operates 35 ( large + medium + small format ) such stores across AP, Telangana, TN, Karnataka

KLM ethnic fashion - Sell sarees for daily wear and western wear for women, men and children. Price points vary from Rs 1k to Rs 75k. Company operates 19 such stores ( all large format stores ) across AP, Telangana, Karnataka

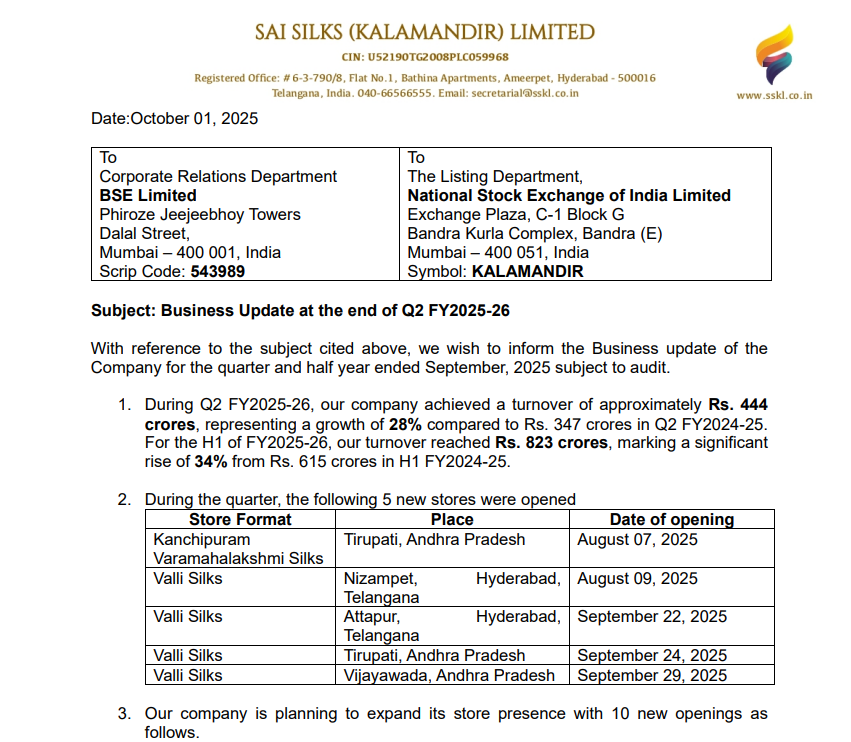

Opened 5 new stores in Q2. Total stores now @ 74 vs 69 at the end of Q1. Total retail area now @ 7.5 lakh Sq Ft

Company has started new format stores - VALLI SILK - is targeted towards lower priced silk sarees aiming at mass mkts. Valli Silk stores shall be smaller stores ( say about 5-6k Sq Ft vs 12-18k sq ft for Kalamandir stores ), focus on pocket friendly ranges of women wear + fashion items. Have converted few of their existing stores into VALLI format stores taking the total no of VALLI stores to 7 ( opened 4 stores in Q2 + converted 3 stores to this format )

At present, 50 of company’s 69 stores are in mature category ( > 24 months old )

State wise breakup of stores -

Telangana - 28

AP - 20

Karnataka - 11

TN - 15

Q2 outcomes -

Revenues - 444 vs 347 cr, up 27 pc

Gross Margins @ 41.9 vs 42.2 pc ( marginal decline )

EBITDA - 72 vs 55 cr, up 30 pc ( margins @ 16.2 vs 15.9 pc )

PAT - 40 vs 23 cr, up 68 pc

H1 outcomes -

Revenues - 823 vs 614 cr, up 34 pc

Gross margins @ 41.98 vs 41.77 pc

EBITDA @ 129 vs 74 cr, up 73 pc ( margins @ 15.7 vs 12.1 pc )

PAT - 70 vs 26 cr, up 171 pc

Early onset of festive season was a natural tailwind for the company

SSSG in Q2 stood at a strong 17 pc ( company reports SSSG only for mature stores ie > 24 months old ). SSSG in H1 stood @ 21 pc

Remain optimistic about H2 due upcoming wedding + festival seasons

VALLI Silks also has a far greater online presence and online focus. This helps the company connect with younger customers + helps cater to evolving consumer needs. VALLI Silk stores are seeing encouraging consumer response

02 more Vraha Lakshmi stores are under construction. Also aim to open another 5 Kalamandir stores in near term

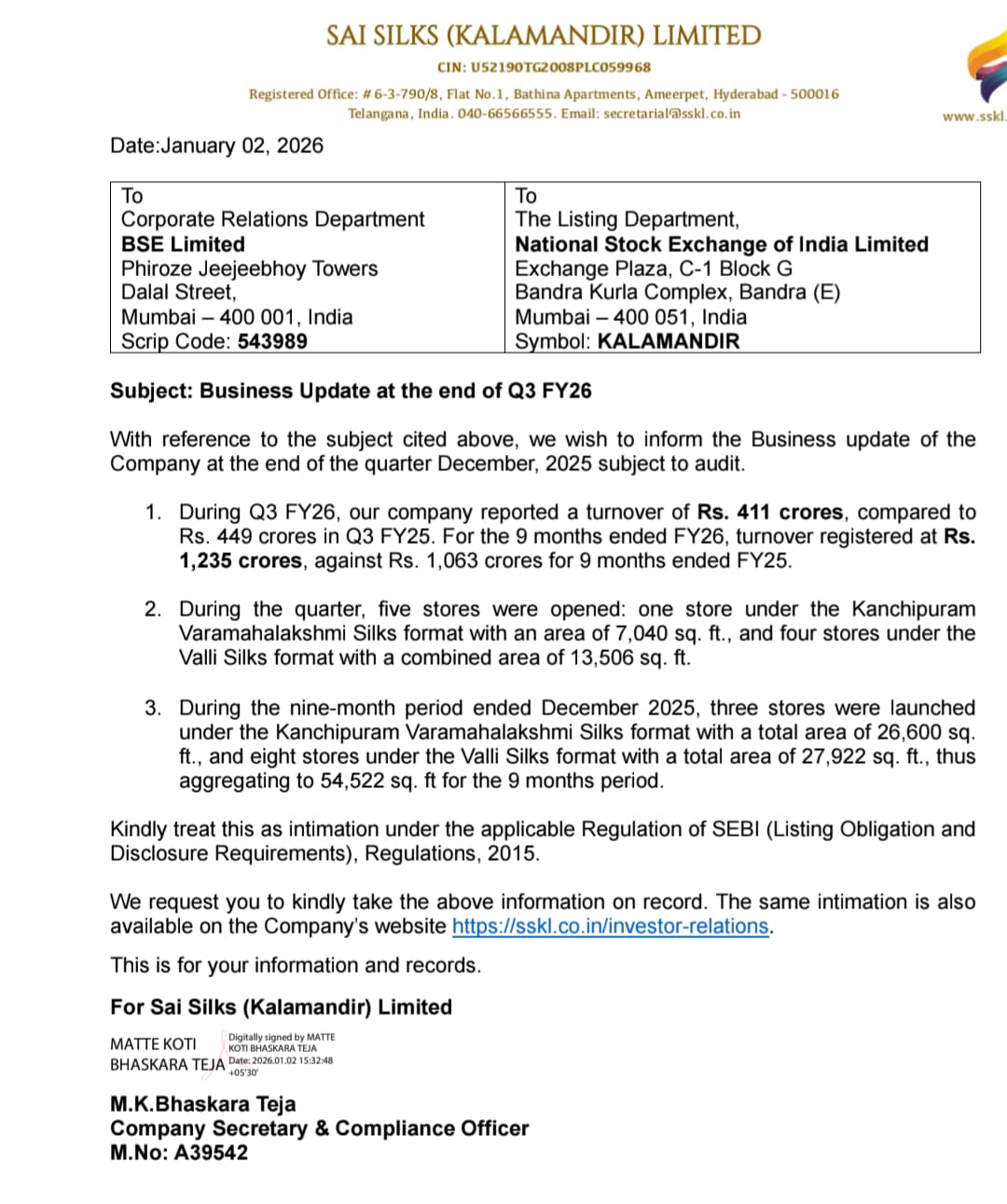

LY, third Qtr was a bumper Qtr for the company. Hence the growth rates seen in H1 should moderate going forward. On a full yr basis, company estimates - they may hit 1750 cr kind of sales vs 1462 cr clocked LY. That would mean a 20 pc kind of growth for full FY 26 over FY 25

Capex requirements and working capital requirements for Varha Mahalakshmi stores are 1.5 to 2 X that of a Valli Silk format store. Majority of clothing being stocked @ Valli Stores are priced in the < 4k / piece. With the Valli format its also gonna be far easier for the company to target the tier 2/3 mkts - because of the affordability

Should keep adding add 8 -10 pc of retail space / yr in the medium term

For FY 27, company intends to clock 8-9 pc PAT margins with a 15 pc kind of topline growth over FY 26 ( that would translate to a topline and bottomline of aprox 2000 and 160 cr respectively )

Majority of company’s sales come from Sarees. It’s a one size fits all kind of product. Its a great advantage to have in fashion retail business

Company’s primary focus continues to remain on Women’s wear ( they do sell Mens and Kidswear through their Kalamandir stores ). If they have to venture into a new product line, they would rather go towards Women’s Kurtis etc vs into different types of menswear

Should open about 5-6 Valli Silk and 3-4 Varha Mahalakshmi stores in H2

Company pays avg rentals in the range of 4-5 pc of revenues vs the Industry norm of 8-9 pc - this helps their profitability. They r able to achieve this by clocking better sales per store and good bargaining power that they command as a brand. Company generally gets into a 9 - 15 yr kind of agreement with 15 pc hike every 3 years

Disc: holding, added recently, not SEBI registered, not a buy / sell recommendation, posted only for educational purposes