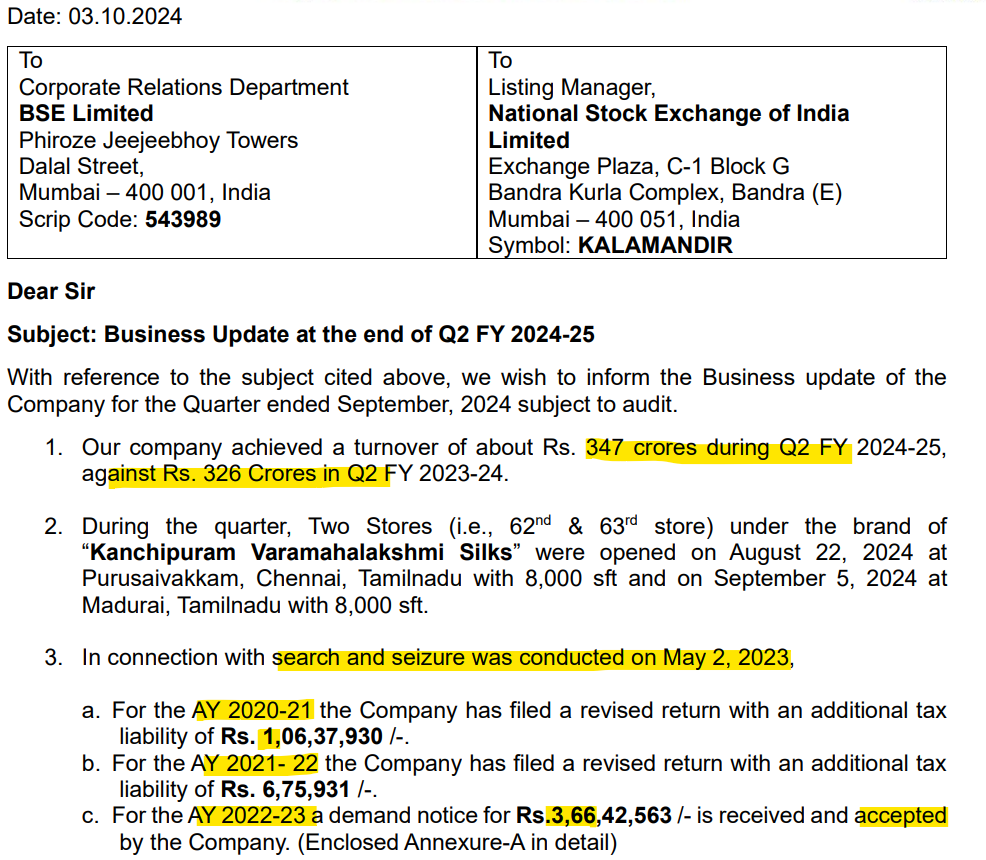

YoY revenue growth in Q2 seems mild (6.5%). Let’s wait for the results to see how operating profit grew.

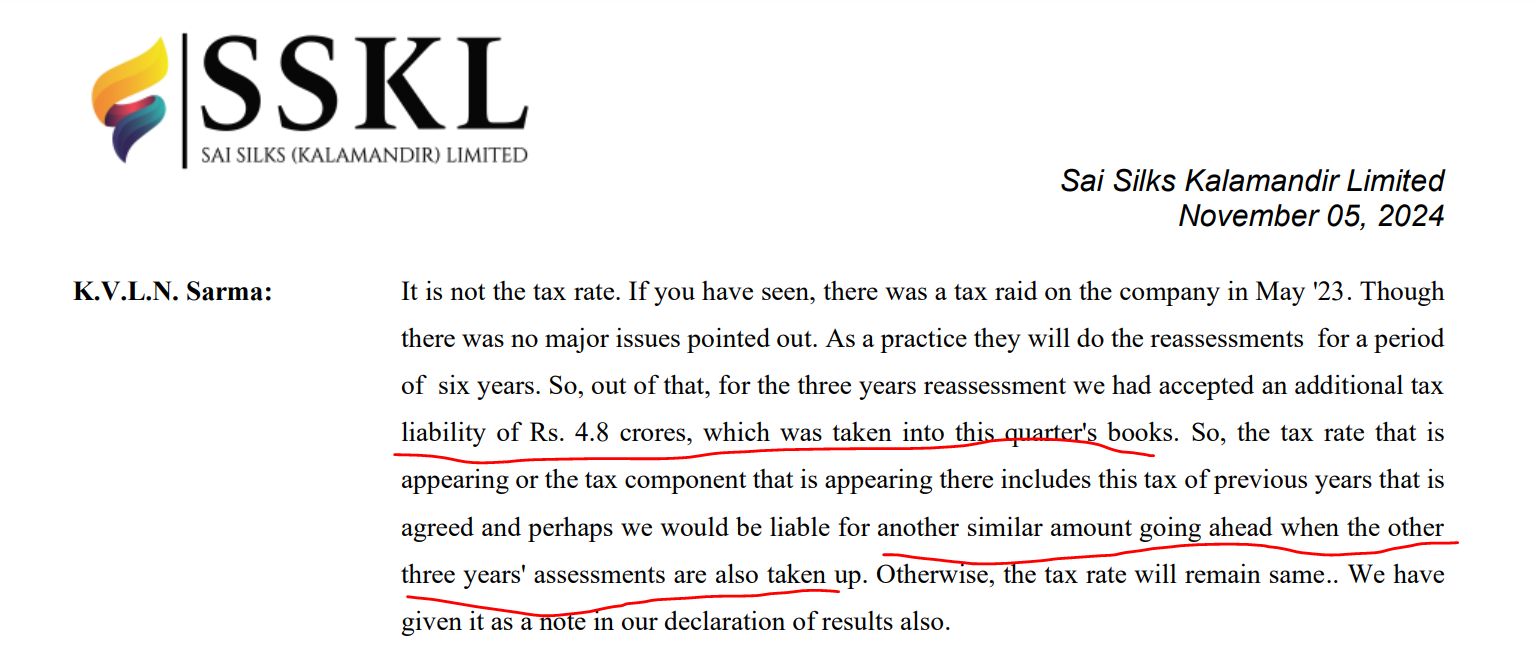

IT search and seizure outcome is reported under a regular subject: Business Update. Seems business has accepted the IT demands. Hence, revised returns for the 3 Yrs [AY20-21,AY21-22 and AY22-23].

Thanks a lot for sharing it, in my views management is completely lagging what they have promised, I don’t think they gonna be meeting their future revenue or store count guidance.

I might be wrong, but the founder of this company is extremely genuine and knowledgeable about what he is doing. I know his brands from my childhood(now I’m almost 30). I did my marriage shopping in one of his brands and had a great experience. If anyone knows Telugu, the following podcast is a must watch.

Key Extract (focus on technology) - using LLM models and computer generated

Kalamandir’s Technological Integration: A Competitive Advantage

The sources show that Kalamandir’s business model is deeply intertwined with technology. Prasad Chalavadi, the company’s founder, repeatedly emphasizes the importance of technology in their success. Here’s a breakdown of how Kalamandir integrates technology into its various functions:

Proprietary Software: Kalamandir has invested in building its own software team to develop a customized system that manages the entire business, end-to-end. This system is highlighted as a key differentiator for the company in an otherwise unorganized industry. This focus on developing and utilizing proprietary software suggests a commitment to leveraging technology for efficiency, control, and data-driven decision-making.

Data Analysis: The company leverages data analysis to gain insights into customer behavior, preferences, and trends. They track customer data to personalize experiences and improve their offerings, using this information to make informed decisions about product development, marketing strategies, and inventory management.

E-commerce and Online Presence: While acknowledging that sarees are best experienced in person, Kalamandir utilizes e-commerce and online platforms to expand its reach and cater to a wider audience. They generate content, including live shows and videos, to showcase products and provide information to customers online. This approach indicates an understanding of the evolving retail landscape and the need to engage customers across multiple channels.

Customer Relationship Management: Kalamandir utilizes technology to manage customer relationships effectively. They track customer interactions, feedback, and preferences. This data-driven approach allows them to personalize customer experiences, address concerns promptly (within 24 hours), and foster loyalty.

Employee Management: Kalamandir also uses technology to manage its large workforce, including the use of software modules for incentive schemes, performance tracking, and communication. This systematic approach likely contributes to better employee engagement and operational efficiency.

Overall, Kalamandir’s strategic integration of technology into its operations appears to be a key factor in its success. The company leverages technology to streamline processes, gain insights into customer behavior, personalize experiences, manage its workforce effectively, and maintain control over its vast and complex operations. This approach allows them to stand out in a competitive and largely unorganized market.

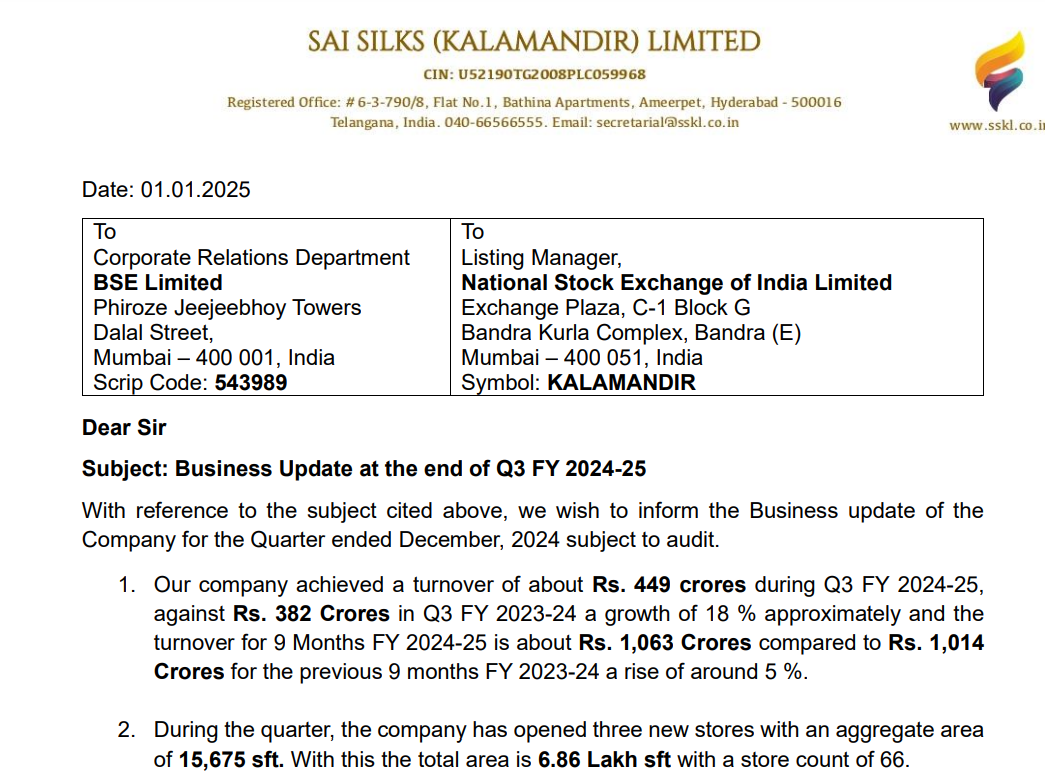

Q3 Business update, strong sales in the Q3, which includes festivals and wedding dates.

3 stores addition done as planned but the Sq ft is is quite low than anticipated.

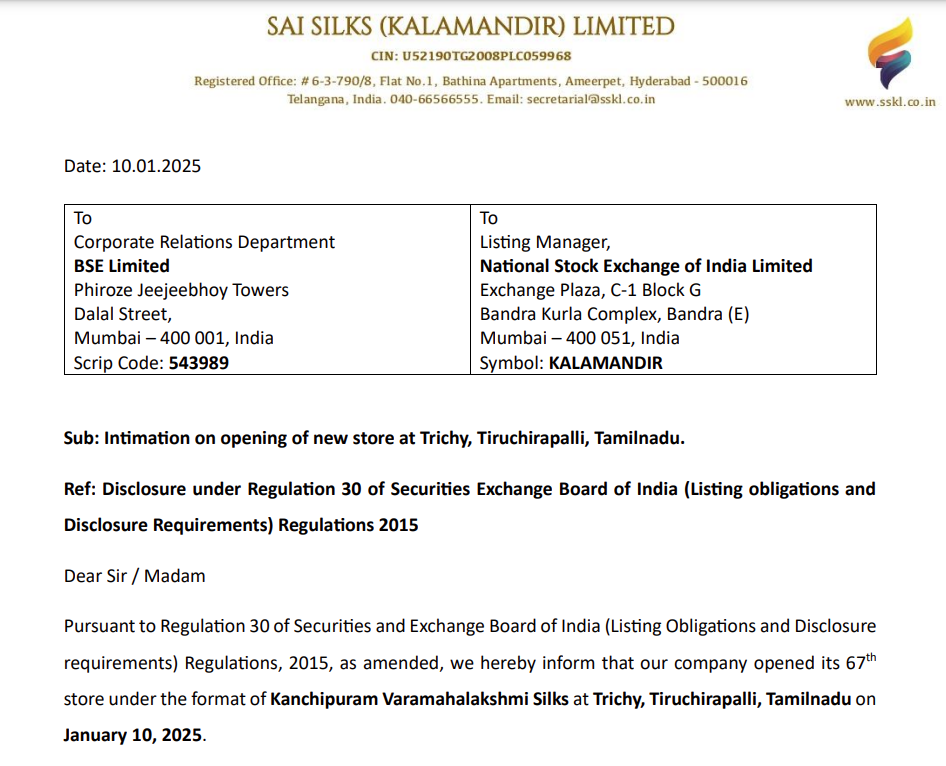

In Q2 call they mentioned opening stores in tiruchurapalli & Tiruvanamalai in Q3 but these stores not yet opened. In Q4 new stores number could be might increase due to backlog.

Over all results would be interesting, especially any margins improvement would helpful to increase bottom line.

The company is planning to open 86 stores till FY26. Their per store revenue stood between 22-25 cr at present. As per the company their store takes hardly one year to attain the mature stage. Therefore 86*25=2150 cr(Total revenue potential for FY27). By taking everything as such EPS for FY27 would be around 10(No growth except store expansion is taken). So for FY27, it trades around 17 PE. Which is a very minimal case for the consumer sector. In the same category, other Brands get around 70-80 PE.

Positives-

: Inventory management through AI/ML

: SSSG would be a big positive.

: Store expansion

I agree with the No of stores number, its would be ~ to 80 or 800k Sq ft.

New stores execution also more or less on track by Q3 end total stores are 66 and we can expect to end FY25 by 70 stores and they may add 12-16 stores in FY26.

Revenue from the newly opening VML format stores would be much higher than the normal KM, KML stores.

I have gone through few research reports also, we may see 18%+ margins by FY27 as these stores maturing and these new stores are of high margins (32-34% at store level) as compared to KLM (23-24%).

As per my view they may hit EPS 10 by FY26 end it self with 2000 Cr top line & PAT ~200 Cr.

if things go as per our illustration then PE rerating (at least 30-50) should be there at 20-25% consistent growth.

Yes, if not they will be almost near to that.

Q3 business update boosted my conviction, we may see 500 Cr mark in Q4 if they can open 1-2 new stores in this month.

In FY26 also we will see 1 quarter with a big hit ( Rev ~ 200-300 Cr only) like Q1FY25 due to very less or no wedding dates but with remaining 3 quarters they can easily manage 2000 Cr top line.