As of July 2023, they operate 54 stores in four major south indian states i.e Telangana, Andhra Pradesh, Karnataka and Tamil Nadu.

Share of organized retail in women’s apparel was 15% in 2015, increased to 31% in 2022, and is expected to reach 44% in 2028, amounting to 1,75,444 cr.

Too many related party transactions for rent, marketing, purchases

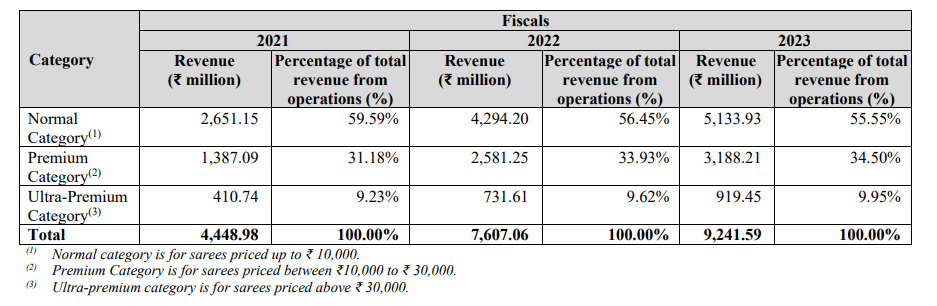

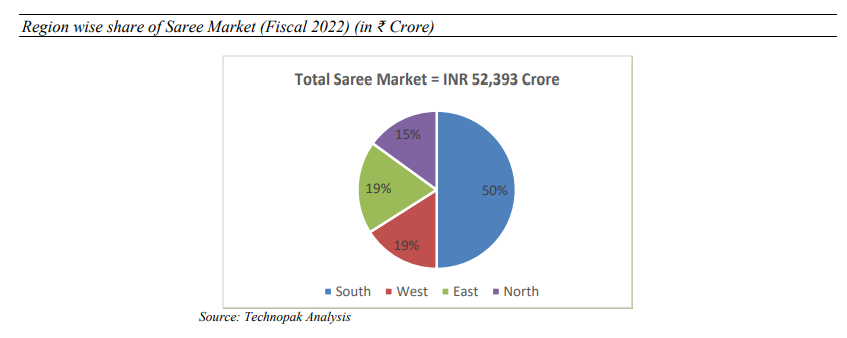

68.38% of FY23 revenue is from Women’s Sarees

Revenue split between normal vs premium vs ultra premium

Saree & Others category(Lehenga, Indian dresses/gowns) within women’s apparel is expected to grow at a CAGR of 19% from FY 2022 to FY 2027, reaching INR 1,24,837 Cr in FY 2027.

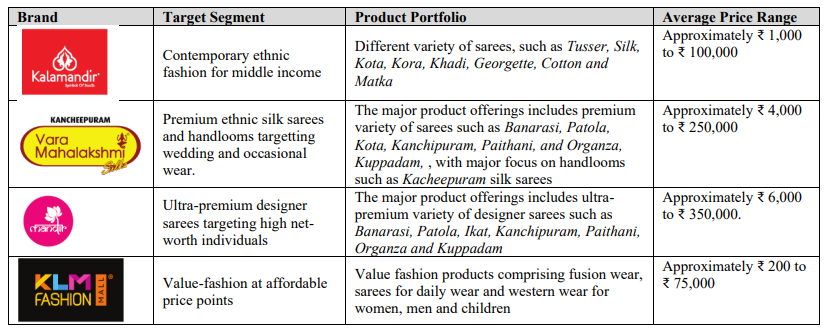

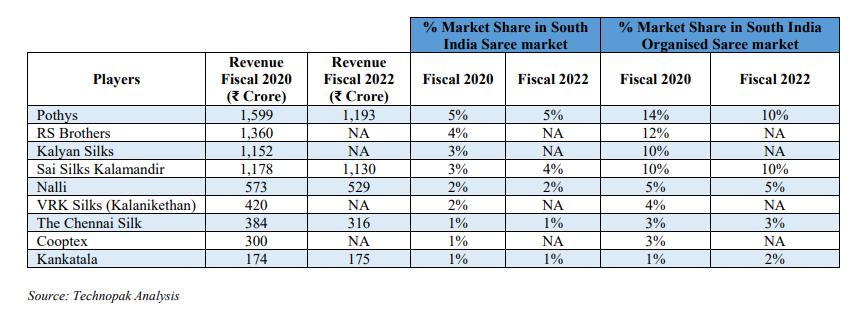

Main Competitors - Nalli, Pothys, The Chennai Silk, Kankatala, Rangoli, Neerus and VRK Retail

Women Indian Wedding and Festive wear market, which forms the largest share of this category is expected to grow at a CAGR of 23%% to reach ₹ 1,30,129 crore in Fiscal 2027 from the existing ₹ 46,211 crore in Fiscal 2022

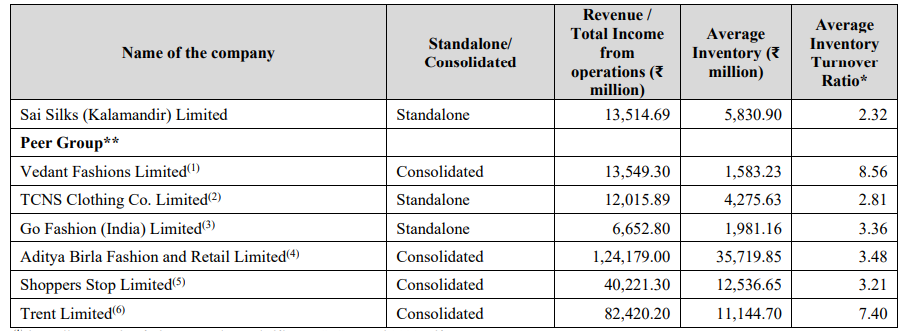

Working capital heavy business compared to listed peers (No listed peer with major revenue from sarees).

This could be a interesting play.

South india is getting lot of manufacturing business which will result to higher income in the region. A pure play in local market can be fuitfulll

The consumption growth runway in India is a popular theme and Kalamandir is an opportunity to ride this with a focus on high end Saree business while the valuation looks reasonable relative to listed peers.

If the company can grow store count at 15-16% as promised, I think this is a company that can deliver 20+% earnings CAGR over the next 5 years.

South India has produced quite a few popular consumer brands with good economics which have created significant wealth for investors.

Further, Pan-India companies like Titan, Vedant or Trent which are not South based, also have a significant portion of revenues coming from South India.

From company perspective, I like their approach of cluster based expansion and exhaustive product range covering entire gamut of south Indian Sarees.

The opportunity on wedding wear and occasional attires also is clear with their Vara Mahalakshmi and Kalamandir stores showing strong SSG with decent unit economics and ROE. Mgt comment on opening only these type of stores going ahead in both TN and Telangana is a structural positive.

TN expansion is a reasonable opportunity for the company as despite the multiple brands present in the region, the unorganised market still remains high, almost 55%.

The key risk factor here will be pace of expansion as that will tilt the market share and the growth opportunity among the organised players. TN is home to multiple Silk Saree brands Pothys to Chennai Silks and Kalyan Silks. Similarly, RS Brothers Group, Chandana Group, J.C. Brothers Group, Kalanikethan Silks, Nalli Silks etc have strong presence in AP& Telangana. The fresh proceeds from IPO does give Sai Silks the upper hand at the moment.

The companies that got listed in June-September would have filed only FY23 results in prospectus. They get 30 days post listing to file their 1Q results and from then on 2Q results will follow usual calendar.

You can expect 2Q results to also be announced by the 30th Nov deadline.

The Company has launched 2 (Two) new stores (i.e., Varamahalakshmi Silks format) at Coimbatore, Tamilnadu on 15th October 2023 & 16th October 2023.

Now Total Stores count 56.

06.11.2023: One new store in the format of Varamahalakshmi Silks at Poonamallee, Chennai, Tamilnadu.

An important aspect: Company did IPO this year and got close to Rs 475 Crores on FDR,where 7.25% interest would be Rs 17 Crores and after tax it would be Rs 12/13 Crores on profit plus interest costs saved when repaying debt. 7456e36e-54b9-4dc0-bfb3-6189fe2e9025.pdf (bseindia.com)

Existing stores are 57, company intent to open 29 more stores in next 18 months. It is almost 50% more stores.

Aims to have approximately 200 to 250 stores in South India in the next six to seven years.

Growth and Outlook:

Expects robust growth in the next two quarters due to festivals and the marriage season.

Anticipates a 5% to 10% improvement in turnover for FY24 compared to the previous year.

Targets revenue of INR 1,700 crores to INR 1,800 crores next year, with potential for better results than the 15% to 20% growth target.

Expects 20%-25% growth in the present year.

Targets a profit of INR 120 crores, with a 10% variation.

Operations and Efficiency:

Made progress in finalizing new locations for future store openings.

Identified locations for two new warehouses in Hyderabad and Tamil Nadu.

Aims to improve margins by 4% to 5% by 2026 through operational efficiencies and premium format stores.

Focusing on optimizing inventory and reducing payable days.

Expect improved margins in H2 due to higher throughputs and improved purchase efficiency.

Store Performance:

Same store growth in Q2 was approximately -5% due to the shift in wedding dates, but expects to achieve single-digit growth by the end of the financial year.

Mylapore store may have lower productivity due to metro construction.

Estimated impact of metro construction on store revenue is around INR 15 crores to INR 20 crores.

Available at 38 PE. a retailing company with long highway of growth.

Risk: Geographic concentration and single line of retail that is saree.

Disclosure: Invested and keep adding at current levels.

Market Challenges: Ethnic wear market facing slowdown due to factors like cyclone impact and reduced purchasing power in Andhra Pradesh, Telangana and Chennai due to water clogging.

Store Expansion: Company added 4 new stores and plans for more, indicating growth despite market challenges. In Chennai plan is to have from 2 to 20 stores. In Karnataka only have store in Bangalore. Kerala is not discovered. Andhra and Telangana can still accommodate 20 to 25 stores. 100 stores in Southern states are possible.

Financial Performance: Last year’s revenue was 378.6 crore with a gross margin of 39.80% and a net profit after tax (PAT) of 31.3 crore (8.28% margin).

Customer Base: Approximately 50% of customers are repeat buyers, highlighting brand loyalty and value proposition.

Gross Margins: Gross margins vary from 25% to over 60%, averaging 40%, reflecting a diverse product mix and pricing strategy.

Sales Growth Target: Targeting 3-4% like-to-like sales growth, indicating a focus on improving operational performance.

Geographic Expansion: Focus on expanding in Tamil Nadu, with plans to increase stores from 2 to 20, tapping into the lucrative silk sarees market. Additionally, potential for significant store additions in Kerala, Telangana, and Andhra Pradesh.

Market Dynamics: Chennai market commands a 15% premium over Hyderabad, indicating potential for higher margins.

Competition: Transitioning from unorganized to organized competition in Tamil Nadu, with 30% currently organized, suggesting opportunities for market share gains.

Market Size: Total addressable market (TAM) estimated at 50,000 crores for Tamil Nadu, indicating significant growth potential.

Marketing Strategy: Planning to increase marketing spend by 3-4%, suggesting a focus on brand awareness and customer acquisition.

Same Store Growth: Slightly negative on a blended basis, indicating the need for improved performance in existing stores.

Store expansion and revenue growth to be seen in numbers. Total Address Market is huge.

Disclosure: Invested

A innocent question Do young girls love to wear saree? Now i tried asking a few girls I know the top 5-6 reasons why they hate saree is

Uncomfortable - wearing saree is a task and even difficult to commute with saree, sarees don’t have pockets and our generation cannot live without mobile, in summer it’s makes you sweat and in rainy season it’s even worse to commute

Cost and usage: the cost of a saree does not justify occasional usage of the saree mostly they are worn for special events, else it lies in the cupboard somewhere on the corner

Age: it makes young girls feel old

Possibility of malfunction

Difficult to use washroom

Now it made sense to me that indeed wearing a saree is a challenge as these are very logical points now with india with 50% population below 30 yrs of age if not many girls love wearing a saree it filters out a majority of customers, also I feel saree is more predominant in south india rather than north india, I feel these facts weigh high and may reduce growth of this company in long run

Disclaimer: I am not invested and these are my 2 cents will love to be corrected

The question is whether demand for sarees as ethnic wear is a sustainable trend?

In my opinion (I live in Chennai and have been to quite a few south Indian weddings). Saree or the half Saree more prevalent in south, have been replaced by western wear and leggings/kurti for casual wear. But when it comes to occasions (festive/weddings), you will find a large majority still wearing Sarees. Notably, Young girls/ladies have a fancy for Silk Sarees when it comes to festive occasions.

This has actually created a niche market where Silk Sarees are becoming a premium product.

Sarees can be largely categorized as an occasionwear. They are still the default outfit in south Indian weddings and other big family occasions, at least for married women. While some investors may perceive occasionwear as a limiting factor in terms of growth, there is still repeat buying since ladies usually do not like to repeat the same saree. And there is a big gifting market as it is customary in many communities to gift sarees to extended family members during weddings and other functions.

From my interactions with family members during the recent wedding season, I gathered that Kalamandir enjoys a very good brand recall when it comes to wedding/festive saree shopping, although a majority prefers certain unbranded local shops that they trust. This is still a very disorganized market, which is ripe for disruption.

It is worth noting that Titan sees big potential in this segment and is expanding Taneira stores with a tall target of 1,000 crore revenue by FY27.

Disc: Bought multiple lots in IPO and averaged in the recent dip.

While the companies has generated a PAT of 101crore, its operating cash flow was 21 crore negative and the reason attributed by the company is sudden reduction in trade payables to the tune of 170 crore to get better bargaining power in purchases. Looks like a major red flag to me.

Thanks for your inputs. Can you pls elaborate on this point a little and some insights on what exactly this means and how big is this red flag? Is this seen at occasions in other similar small retail companies or even in bigger companies? Is there any other red flag you observe in terms of ethics & governance? Thanks!

I am quite convinced with the management reply on Q1 results due to very less or no wedding dates in the Q1.

Regarding margins I think they have different format stores, which has different margin profile. If we can get Vara maha Lakshmi stores margin profile then it would be helpful to access.

Tracing this company from last 2 quarters, I feel we will see good grown in numbers as they keep on adding Vara maha Lakshmi stores in TN & KA as avg invoice value of these stores is highest among all formats and PE expansion also should be there as they grow in numbers and expand margins going forward.