I have done some snooping.

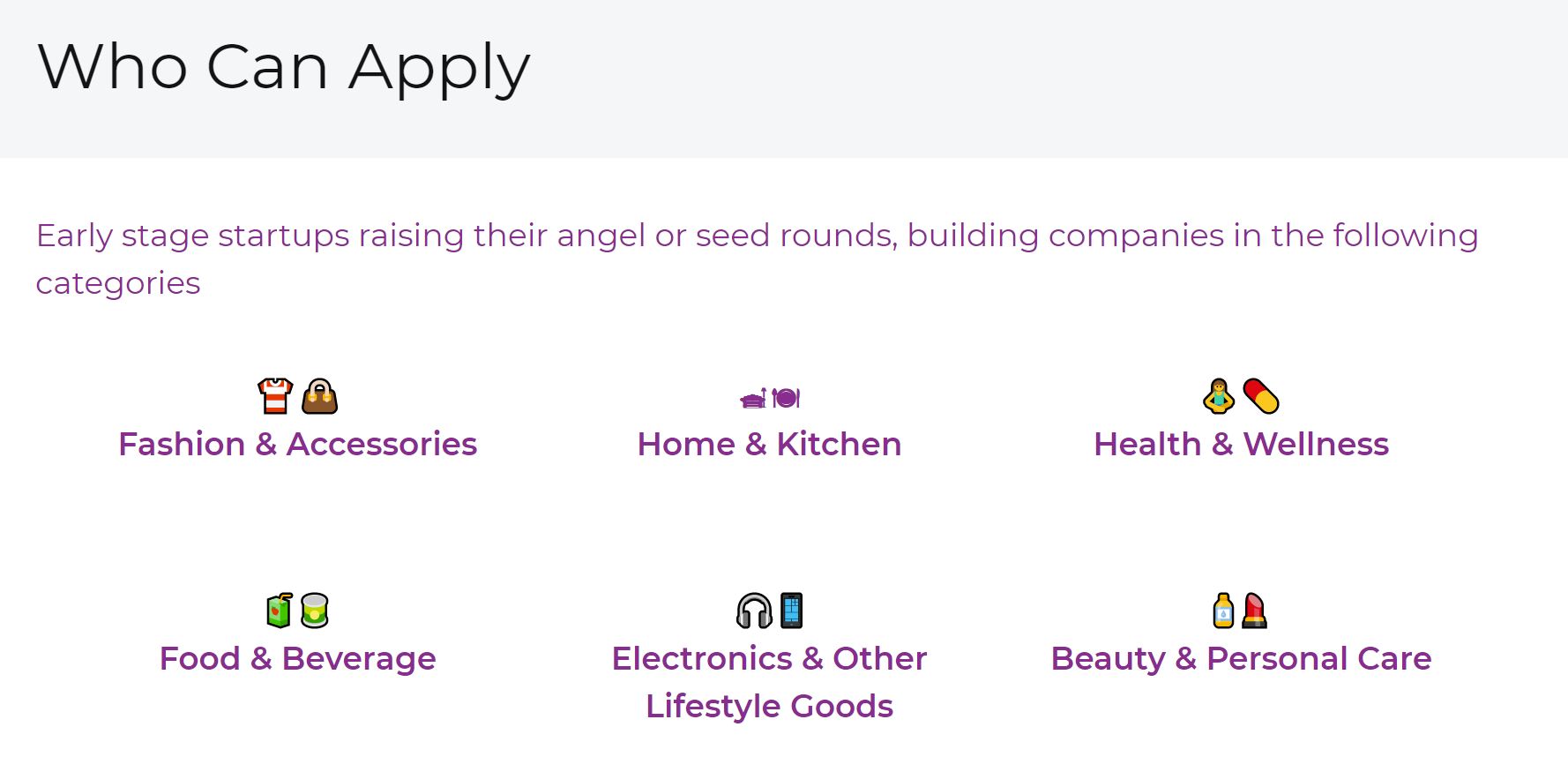

On their LinkedIn, they’re currently in the middle of something called Basecamp, where they’re looking to fund around 8 new D2C brands.

The partner for this is a company called LBB, an online marketplace with an alleged userbase of 2.2 Cr. people.

This is set to kickoff in July, and I’m hoping we get more information. For anyone interested, this is the application form if you’d like to have a glance.

Sorry to revisit this, but this is a valid concern. It was bothering me, and I spent some time to understand how we can tell when this is true, and when it isn’t.

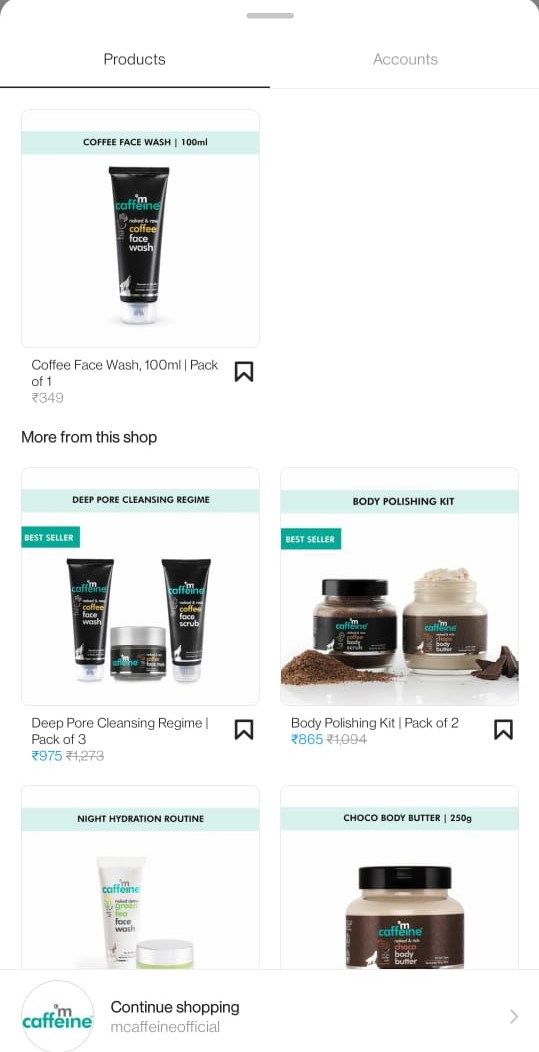

Firstly, I want to highlight that social media platforms now serve as a shopping platform seamlessly. This means that for a brand, your social media page is your store.

When you click on any of the pictures, it shows you the person modelling the products as well as a link to buy the products highlighted.

If you tap on the product, it’s designed to be non-disruptive and seamless. Also notice how smartly they also show you related products at the same time.

Let’s then address the questions of authenticity.

How do we know they haven’t bought followers from companies that offer this service?

We can’t prove a negative, but we can ask smart questions about what would point to this being the case.

If you have bought followers or used various promotions, there would be two key indicators:

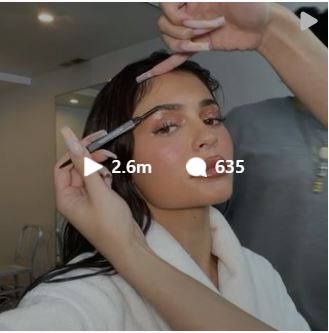

Firstly, there would be a huge discrepancy between the number of followers you have, and the number of people that engage with your posts via views, likes and comments.

The standard should be one of the biggest make up companies in the world, Huda Beauty, that has around 50 million followers. The engagement for some of their most popular content is about 5% of their following. On average, it is around 0.5 - 2%.

I’ve checked to see this is the case among other brands. They vary between 1 - 2%. Interestingly, the engagement is the highest at around 15% for personal celebrity brands. Non shopping related content has a much higher engagement, between 15-25%.

MomJunction has a following of 417k, and the engagement we should expect is in the 4000 range. Indeed, this is the case:

To be a little meta, the final benchmark I’m using is ValuePickr itself, with Hitesh’s Portfolio having over 1.2 million views. The number of comments on the post are 0.5% of the views, and overall, 1.6% of the views have turned into likes given on the post.

There is an obvious difference between the way followers and views work on Instagram versus this forum, but nevertheless…

The second way you can see if brands have bought followers is by looking at the people that follow them. If the people following a brand themselves have no posts and no followers, they’re likely to be bots. However, a cursory look across a random section reveals that they are real people that often talk about their lives.

The takeaway is that a lot of people view posts without commenting, and the nature of social media is that it’s unlikely that all of your followers see every post, but they have signed up to see your advertisements from time to time, and provide your company free advertisement by sharing your products with their friends in the comments. Ultimately, all of this drives traffic to your website, and is often the only way your brand has visibility.

Edit: Double checked the percentages for engagement.