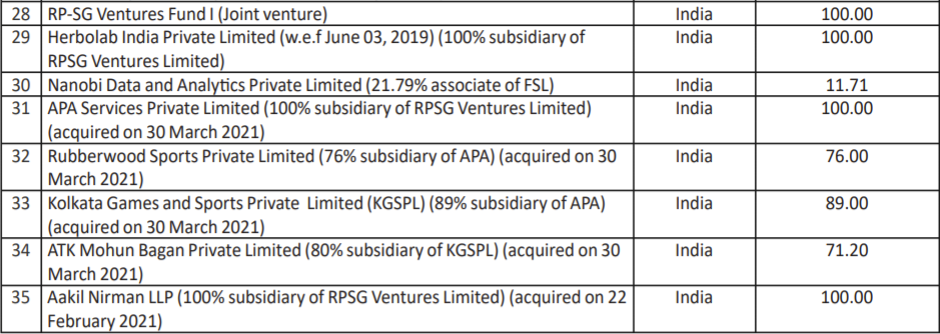

Page 119 of the annual report still lists the ownership as 100%. I’m inclined to believe this is just a change in voting rights, but here’s where I’m not clear. Usually voting power is proportional to the number of shares owned. If no equity has changed hands, classifying it as a joint venture shouldn’t give the partners an additional vote, unless the voting is done just by majority amongst the partners.

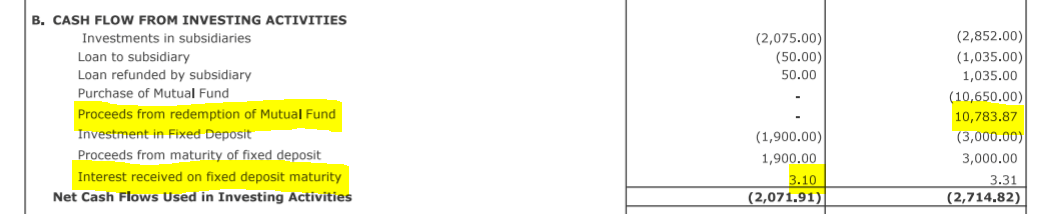

Their investments are strange. The interest received on an FD of 19 crores is only 3 lakhs (0.15%). They must have broken it early, or have made bad decisions. The interest on the mutual fund is 1.24%.

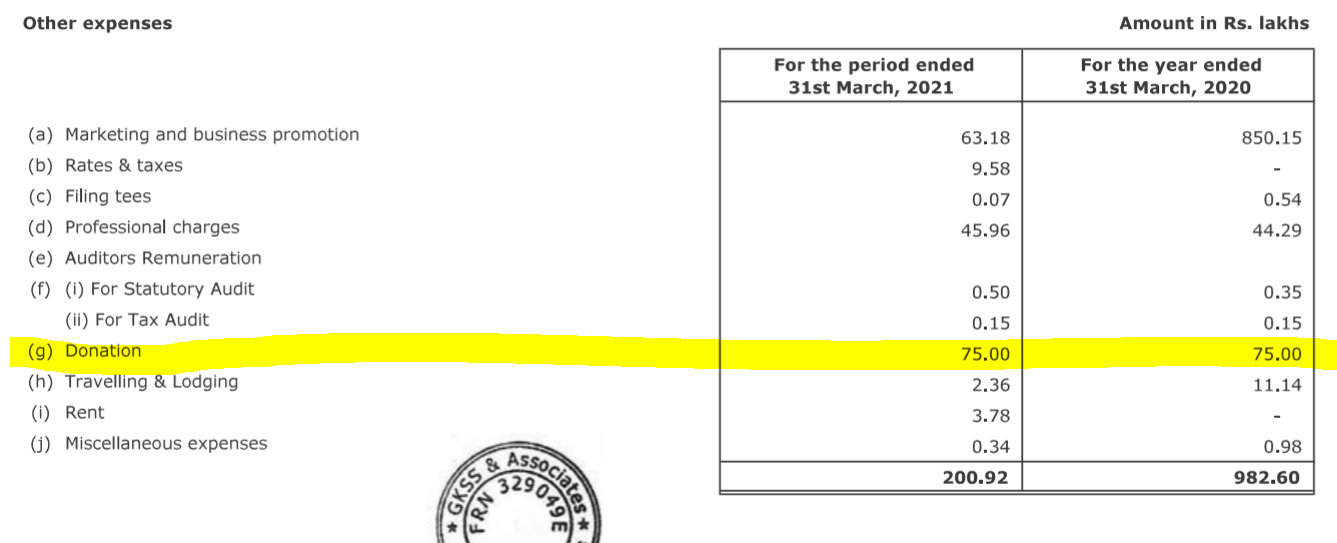

They make a yearly donation of 75 lakhs. No information on whether this donation is political or to charity.

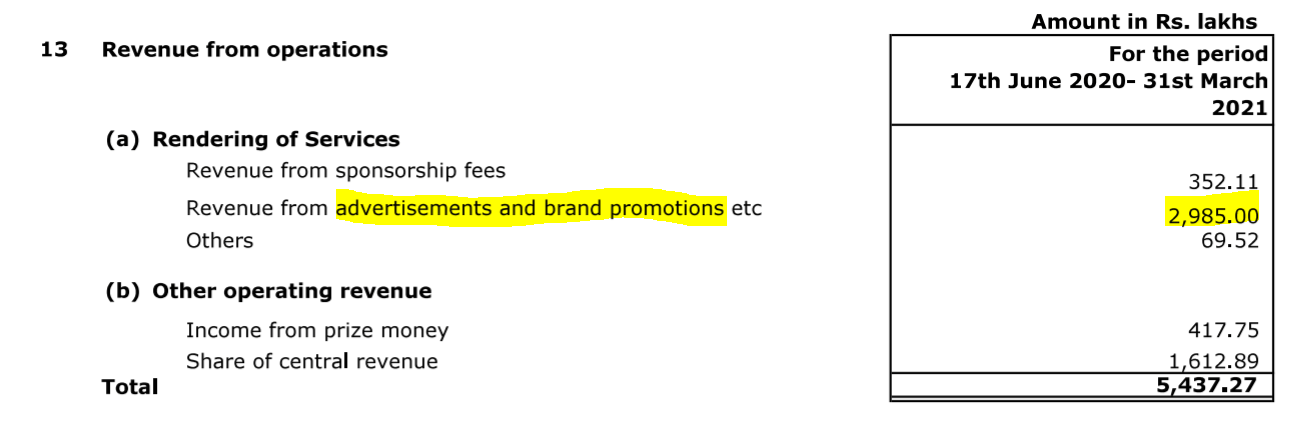

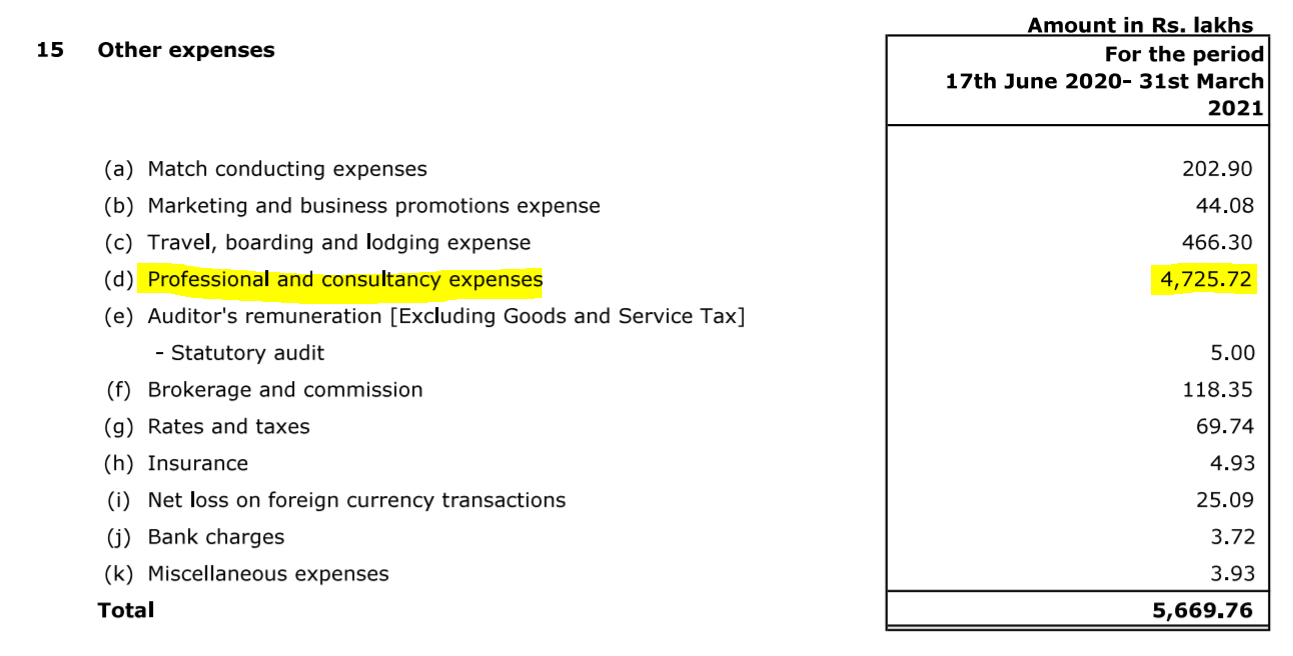

They rake in a significant amount of money from ad revenue. The major expense goes into professional and consultancy expenditure, which I think has to do with coaching / analytics.

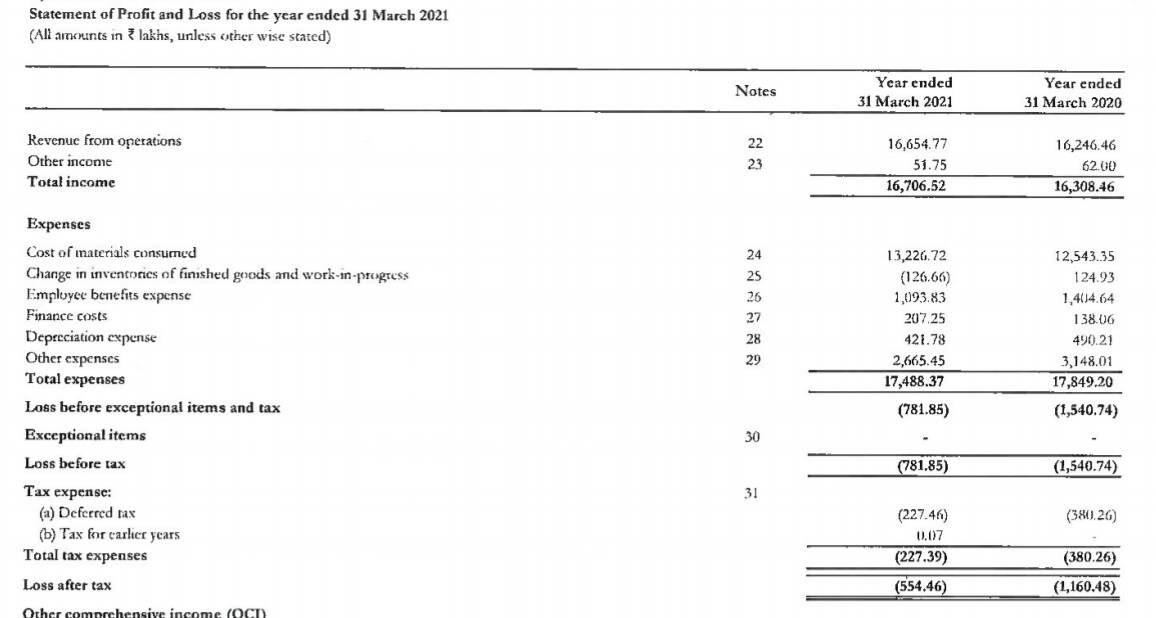

Herbolab is profitable, advertisement expenses of 21 crores ate up the entire topline. Freight and distribution makes up 25% of the topline.

Confirmation of sale of goods to Nature’s Basket and Spencer’s Retail.

3) Quest Properties Standalone

Have 95 crores of debt, payable in monthly installments at 9.2% interest. Most of it has residual maturity between 1-3 years.

Revenue of 76 crores, down from 104 crores. PAT significantly affected.

Key Highlights

Herbolab has tremendous potential with high gross margins.

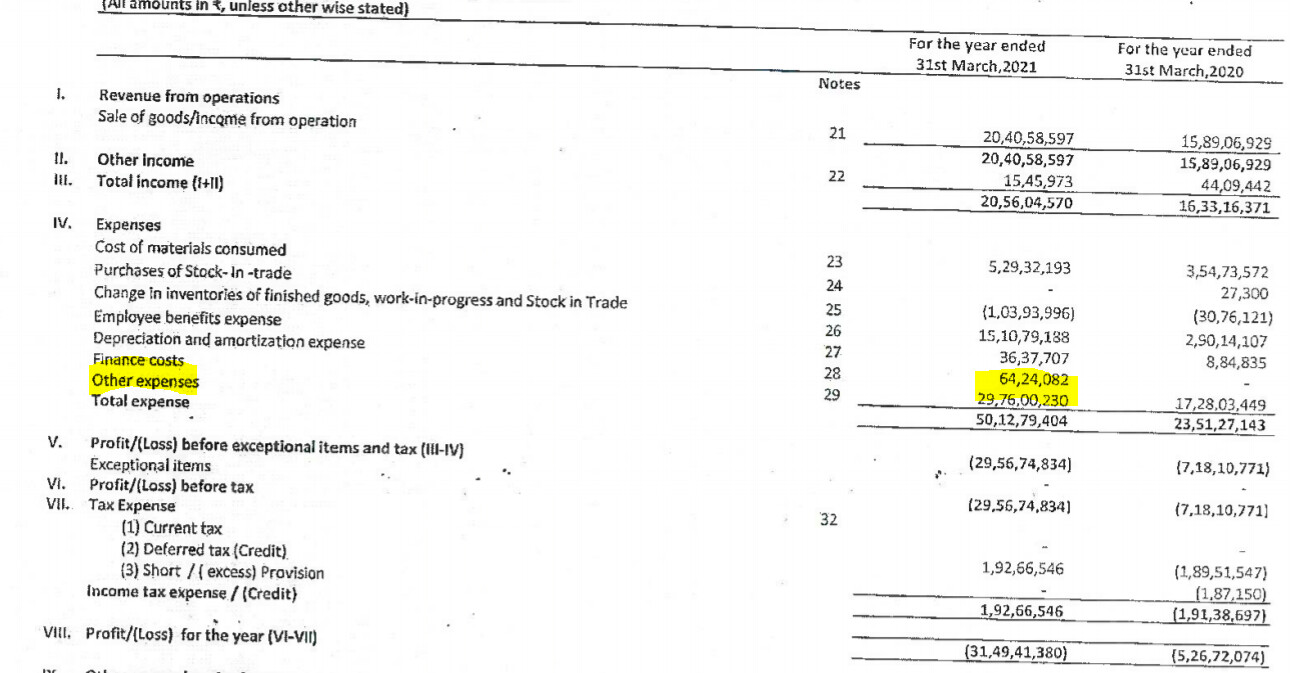

A lot of the subsidiaries are presently loss making due to significant advertisement spending.

If we discount the ad spend in forward cash flows, the numbers start to look better. There is still some way to go for the 10,000 Cr. target from FMCG, and we’re nowhere near the required run-rate to meet this by 2025. Worth watching how this thesis plays out.

In summary, let’s revisit the collaborative investment thesis:

Almost two months later, FSL’s market cap is 15,000 Cr. RPSG Venture’s is now at 1900 Cr. With a 53.7% stake in FSL, the holding company discount is 76.41%.

As a summary on the current revenues generated by the subsidiaries:

Thanks for the excellent in depth analysis @Chins. I think your comments on the subsidaries as well as the thesis sum up the picture. I also went through the Annual report, and would just like to add a few points (which I am not fully certain about considering how many entities are there, but still bringing them up)

Agree with your table on the sum of parts value including 1x sales multiples for the newer businesses considering initial stages. I just have one query - the standalone entity with the revenue of 114 Cr has actually grown from 63 Cr last year and seems to be an IT business. Considering it is also profitable, a 1x sales multiple here might be conservative considering how IT companies are selling at higher sales multiples in the market?

I think your comments on the individual ventures sum up the details perfectly. Just some additional views on the same are:-

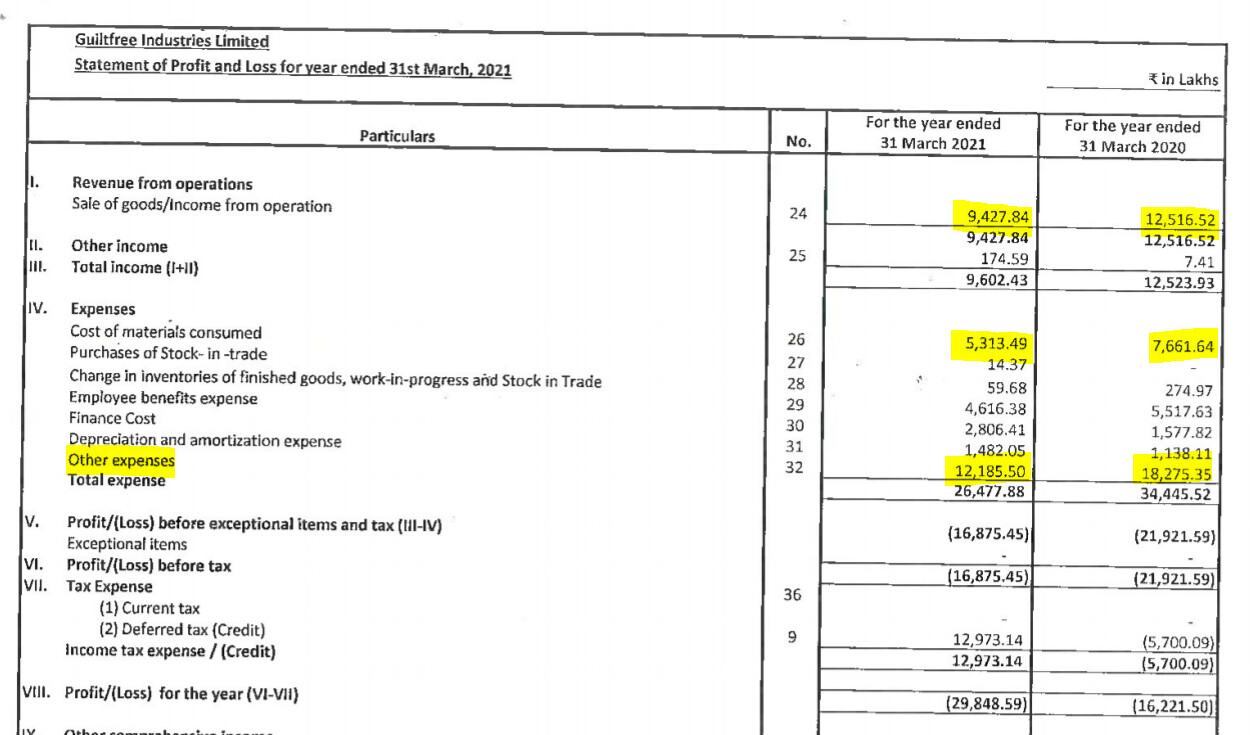

It is fascinating to see that Guiltfree’s other expenses (which would primarily be advertising?) are more than their sales for both years. This looks like front ended investments for the future so the story to be played out looks long. For my personal thesis, I am though still positive about this business - but we will need to closely track hirings/sales and distribution efforts/growth in coming years to understand if the focus continue. Additionally, Too Yumm/Potato Chips are a pretty out of home consumption sort of product, and hence I suspect should be very dependant on General Trade and Modern Trade distribution and footfalls, and would not really be compensated by E-Commerce buying. This is obviously severely impacted last year. So I would probably not look into the GIL degrowth in business with too much critique for this year. Additionally, I like the new launches in the Potato Chips category mentioned in the AR - large addressable market there.

I liked what I saw of Herbolabs in the report. Interestingly the company owns over 100 Ayurvedic formulations and also AYUSH accredited facilities with export licenses - which should be a big positive versus building this from scratch.

I think I read that Bowlopedia was reduced from 24 to 2 restaurants considering COVID and got into Frozen Snacks. Quest has also seen an impact. But looking forward, continue to look like good businesses especially Quest.

I am not that sure about APA and Mohun Bagan. Seems like an emotional bet. I am a football fan but the Domestic League and the ISL have far to go before they can be a healthily commercial part of the football ecosystem in India. I personally did not ascribe any value for this in my head.

Overall though, just adding some nuggets to the mainline overall thesis:-

I think the first post to start this topic still sums up the opportunity perfectly. There seems to be a few parts to this:-

In the short term, FSL being the major part, we could expect movement in line with FSL except for when the Holding company discount comes into play. What FSL does from here on is critical, it has really run up in valuations, but the market is viewing growth and the coming year will be interesting.

In the long term, there is a large investment opportunity if the holding company discount narrows. Again taking from the 1st post, if this discount narrows to a 30-40% or even a 60%, in the long term there should be a large value creation opportunity sometime in the long term. When this happens is anyones guess, the market is still giving it a 75-80% discount despite a massive bull run ongoing. I would think it could be very much linked to how GIL and the other businesses play out. In the long term, if the GIL business starts performing well and growing, there could be value unlocking from this opportunity incremental to what happens in FSL. I view it like this - being invested in FSL, but foregoing the dividends to be early investors in these other businesses that RPSG has, with a view that a few might create value in the long term

That said, expansion here on as well as growth needs structuring and involvement. It will be critical to understand if and when that is happening over time.

RPSG seems to have taken up a lot of businesses and buying aggressively in spaces I like including D2C, but at some point they will really need to structure these to grow individually. I see substantial investments that would be needed on distribution expansion/employees - to really make them meet the potential they have. The good part is they have the brands to support it - be it hiring good talent or expanding distribution. I do hope the management is driving this with the same vision, taking on companies to make them succeed, and not only owning them

Considering how FSL is now valued I am prepared for some short term pain if it stops delivering growth (I have no reason to think so, but I am prepared for it in case it happens). If I view this with a 5-10 year timeframe, I don’t think that should be a consideration for me as it is.

I hope in case RPSG does acquisitions now - it is more in the D2C space - and not unrelated businesses like APA. They already do have a really large pool of other businesses.

Disclosure : Invested. These are only my personal views and not meant as any investment advice. I am not a SEBI advisor/valuation expert - and these are just my best interpretations.

Spot on, hence I didn’t do the valuation and just left it in the table for everyone else to make their minds up. It’s nice they have 300+ applications and mostly sell to the parent group for the power sector. Would be nice to have clarity/guidance on the standalone business going forward, and hence I left it purely as 1x sales and didn’t attach a PE multiple. Definitely deserves more if we’re not conservative.

I noticed FSL’s margins have steadily been improving since 2015, and their BFSI segment is outperforming. Their acquisition of Patient Matters in the healthcare space is also worth watching.

Segment

Revenue

EBITDA Margins

YoY Growth

BFSI

757 Cr.

18.12%

65.82%

Healthcare

359 Cr.

15.97%

7.75%

Communication/Media

300 Cr.

19.00%

22.9%

Others

31 Cr.

23.12%

-2.8%

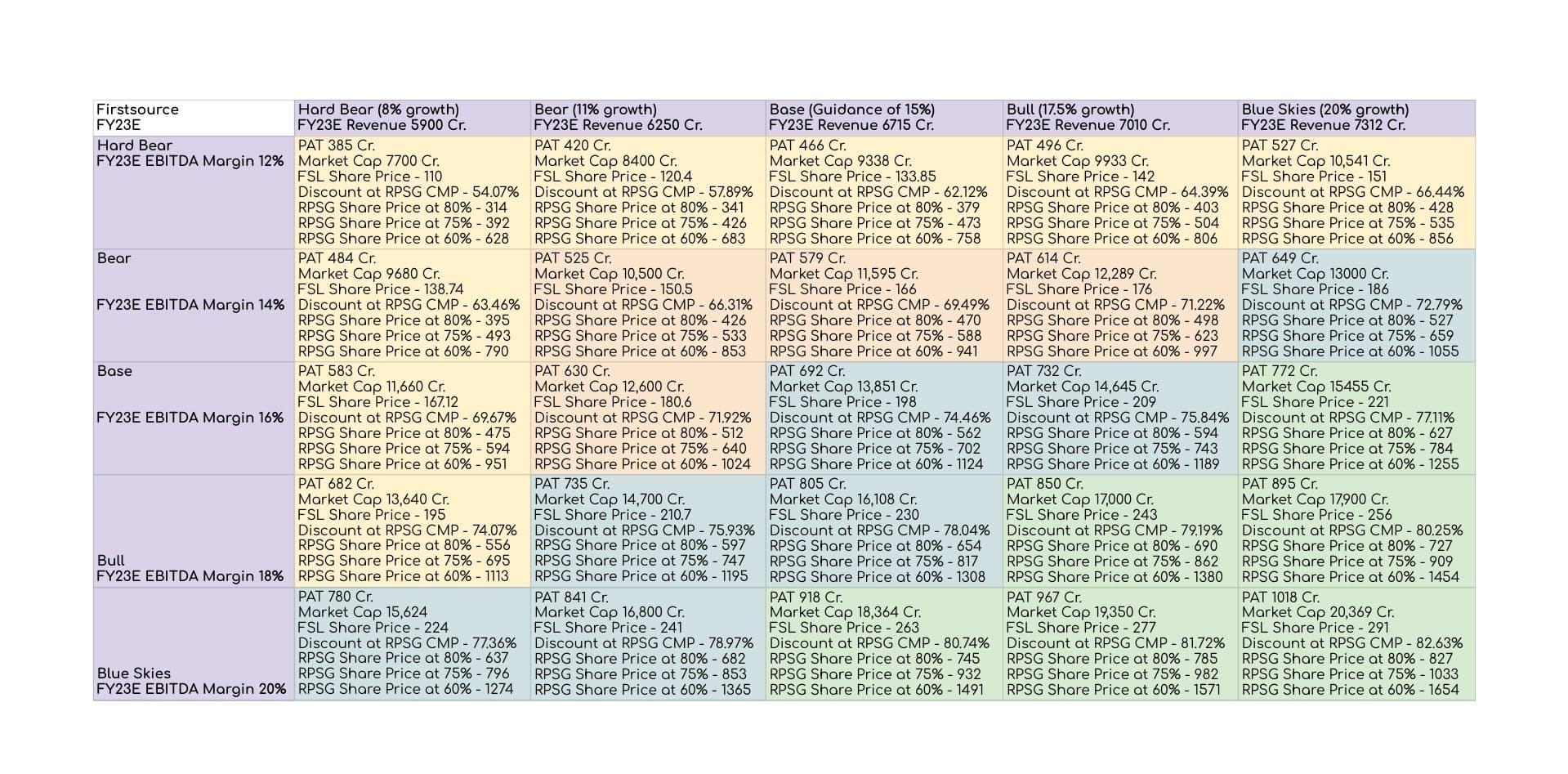

I did a quick back of the envelope bull / bear estimation of FSL’s FY23E revenue, and mapped the effect on RPSG Venture’s holding discount.

Assumptions:

Base case is the management guidance of 15-18% over the next two years.

Assumed 250 Cr. of Depreciation and 16% tax rate in FY23.

This isn’t a rigorous valuation, and I would be shot by Prof. Damodaran three times.

Assumed market cap to be a conservative 20x FY23E P/E.

Revenue mapped out from a bear CAGR of 8% to a blue sky CAGR of 20%. EBITDA margins mapped out from a range of 12% to 20%.

Colour codes reflect upside / downside and stagnation.

I’m hoping by the time the holding company discount plays out, we’ll start to see revenues of TooYumm, Herbolab and the other companies increase enough to warrant a valuation in their own right.

Completely agree. It also makes one think how much bloat RPSG Ventures will take on over time, as the team was held by the main Sanjiv Goenka group.

Thanks for the fantastic valuation table @Chins. The scenarios map out really well and just shows how the holding company discount story can be an incremental upside for RPSG.

Overall - good numbers in my opinion and they just manage to meet the lofty expectations with the rise of the share price this quarter. There is no sequential growth as such. The no crazy one time charge makes PAT look much higher for this quarter giving the media some big headlines.

What happens from here on will be critical - so it will be an interesting conference call. I was highly impressed by Mr. Khanna the last time, and I hope they still see growth ahead and it would be interesting to see the outlook for the mortgage and healthcare business. Additionally their view on future employee costs and new deal wins will be key monitorables - I don’t know if the FSL talent is really swappable in IT and prone to attrition - but would be interesting to see.

Overall, I liked your snooze comment earlier. Sums up this story, get up, monitor, don’t react too much, and snooze and let it play out in the long term.

Disclosure : Invested, not a buy/sell recommendation, I’m not a SEBI registered advisor

amazing analysis

seems pictorial representation of Excel calculations weren’t difficult that i was scared until now

w.r.t. #FSL (subsidiaries/segments)

current Margin and Revenue Projection basis playing out base case of 17-18% revenue Growth and 15-16% EBITDA, BFSI segment is going to see erosion (i sermise) as the US & developed nations see better growth across the sectors which makes the repayment defaults lower and lower giving lower paced revenue accretion

In media : if the OTT becomes a Significant revenue grosser (50% plus ) in developed nations. The traditional media and DTH recharge etc. will take a big hit… and may end up flat

healthcare: becoming a more and more important spending arena and newer M&A in this can catapult and support higher margins as the Hospital care and Insurance guys want high no. of Patients coming to OPD lost in booking. (but this may need CAPEX ) and story pushes further to FY25 making Stock performance a daunting task for FSL.

can @Lynch / @Chins pls help me in understanding how #rpsgventures receiving dividends from #fsl be more tax efficient

disclaimer: i held RPSG VENTURES @ LOWEST LEVELS it hit and as of now i have sold my holding as it was 75% of my portfolio and plan to day trade going further

it was an unfavorable R:R proposition at such an elevated price for me

The Souled Store has secured it’s series B funding of 75 crs. I have personally used the products and I really love them. Infact this was the reason I stumbled upon RPSG.

Some of the ventures of RPSG are really promising and I like the fact that they don’t get involved in many startups. They seem to choose them very carefully. The list of the persons who have invested in series-B have some marquee names.

Just went through the entire thread - some excellent work by @Chins and others, kudos. I didn’t know till recently that RPSG Ventures is a listed entity. Its a shame, given that I have close friends right up top at The Souled Store!

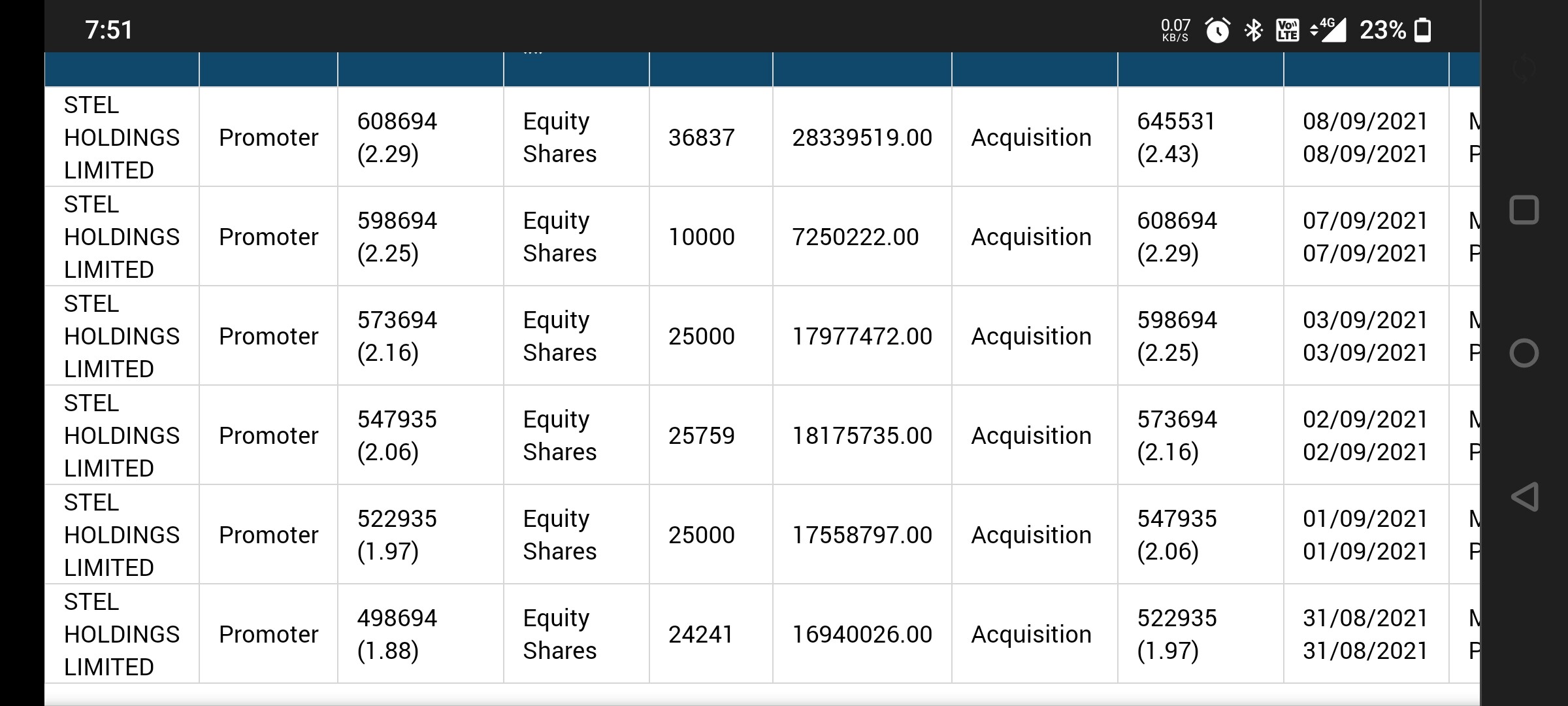

Anyway, better late than never. Over the past few days, the FSL holding discount has narrowed to close to 72% and STEL Holdings have been buying. However, we must remember that RPSG Ventures has debt equal to almost 80% of the present market cap. And so at an EV level, the discont is much lower, at slightly above 50%. This is the discount we should be tracking and not just the market cap discount.

Disclosure: Have taken a tracking position a couple of days back. Will scuttlebutt about my friend’s impressions of the management quality of Guiltfree and Herbolabs before adding to it.

Full portfolio here The Vineet Jain portfolio

The promoter is buying huge quantities every day. Do you guys see the valuation is still cheap and huge growth ahead? I am thinking to add more to my portfolio.

They have entered into Personal care and hair care products. They have launched the brand “Naturali”. This business is under their Subsidiary Guilt-free Industries.

TBH I don’t know what to make of this decision. It is good that they are taking aggressive steps in the FMCG business but I would have been more assured if these steps would have been towards the Food category.

Yes, they are not able to scale up the foods business and spreading themselves too thin. So maybe not the best move. But also remember than RPSG ventures, VC arm has invested in some good D2C brands in skincare space and would have good learnings from there. One of the D2C start-ups they have invested in, has a very high selling product on Nyka. I am sure, they will use Nyka, etc. to scale up distribution. If they are able to do that, they can get a quick feedback and can either scale up or close this new business. So, risk reward is not bad

I am not worried about their debt, all they have to do is increase dividend from FSL and they will be good. or sell some small stake in FSL. Now since real estate is picking up, sale of residential properties being developed by them will also give cashflows. And look at the group, they have never overleveraged so far and have done balanced growth so far without taking huge risks.

Agree, I am not worried about the debt either. Was just making the point that the real doscount should be viewed at an EV level and not just market cap.

Through my friends at TSS, I came across someone who worked at a very senior position at the venture fund till a few months back. This person didnot seem to think very highly of the way TooYum or Dr Vaidya’s was being run. Said also exactly what you have said, that the strategy seems to be a bit all over the place and RPSGV is spreading thin without building depth. While such impressions may naturally come with their biases, it is good to take note of and not be too excited about the medium term prospects of the FMCG business.

For the long run, its anybody’s guess how these businesses will do. FMCG is a long gestation business, needing a lot of investments and cash burn. ITC has been investing heavily in its FMCG business for two decades and it is only now that their margins have turned positive, in spite of all the distribution advantages it enjoys. While using platforms like Nykaa etc may reduce the go to market costs initially for some of RPSGV’s brands, large investments will be needed to achieve any reasonable level of scale. The space is getting more and more crowded, and the larger companies will start getting more aggressive going forward.

In my view, this is largely an FSL discount catch-up story, but viewed from the lens that the cash flows being routed into businesses may or may not generate any meaningful returns in the future - pretty much like how the ITC ciggerate cash flows were being used for all these years.

Tha said, the promotor has been buying shares in bulk from the open market which is a positive sign. At least they are confident of the trajectory of these businesses.

fully agree with what you mentioned. ITC like perspective is interesting. So, its more like a value play with optionalities. Worst case if their fmcg ventures fail to take off, they can sell Too Yumm brand at good value. Players like ITC can lap it up

The buying has continued over the last two weeks, STEL holdings now owns a further 2% stake in the company.

There are rumours that the RPSG group has purchased a tender to bid for one of the two new IPL teams introduced for the next season. The date of the announcements coincides with the start of the promoter buying. This is complete speculation right now, but perhaps an IPL team is on the cards.

The auction is expected to happen before the end of October, we should know more from reliable sources by then.