Avendus has written some fascinating long reads on the different industries in India. Each report takes you through the supply and demand side economics of the various sub-sectors, and details how the drivers for growth have changed over the years. Their report on D2C brands is freely available.

I wrote to Avendus and got permission to use the data and figures contained within the report. I haven’t been paid by them to write this post, but they are masterfully written and I wanted to break one of them down and have a discussion on the opportunities for investors going forward.

Table of contents

Introduction

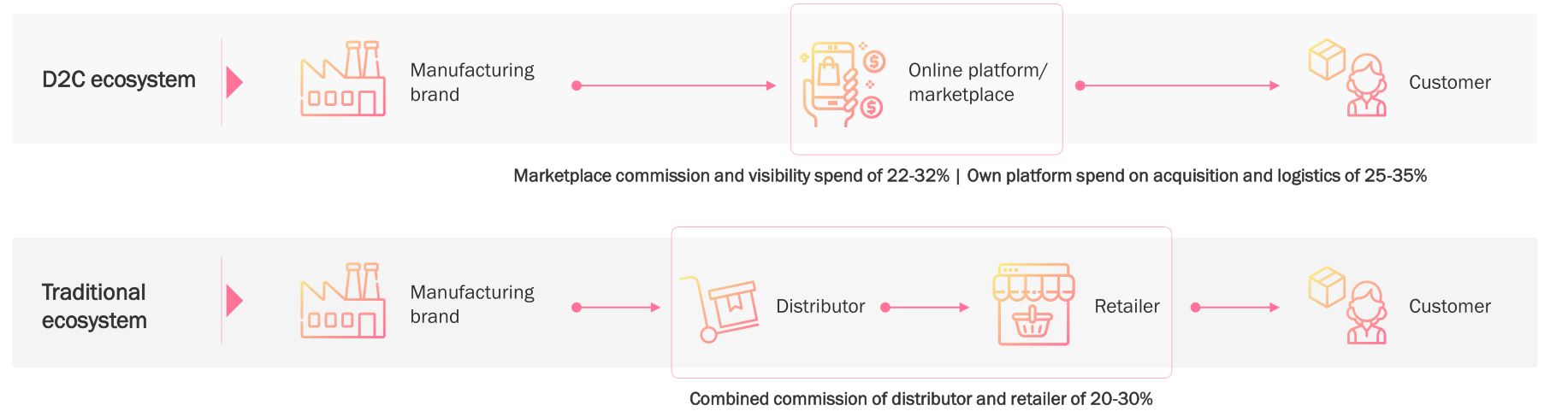

What is the D2C business model?

As you can see, the idea is to eliminate the middlemen and interact directly with your customers, taking complete ownership of the supply chain and inventory management as well as the marketing and distribution.

However with this, there comes a tradeoff. You lose a wide reach across demographics, organic product discovery opportunities, and the trust that consumers have in traditional marketplaces.

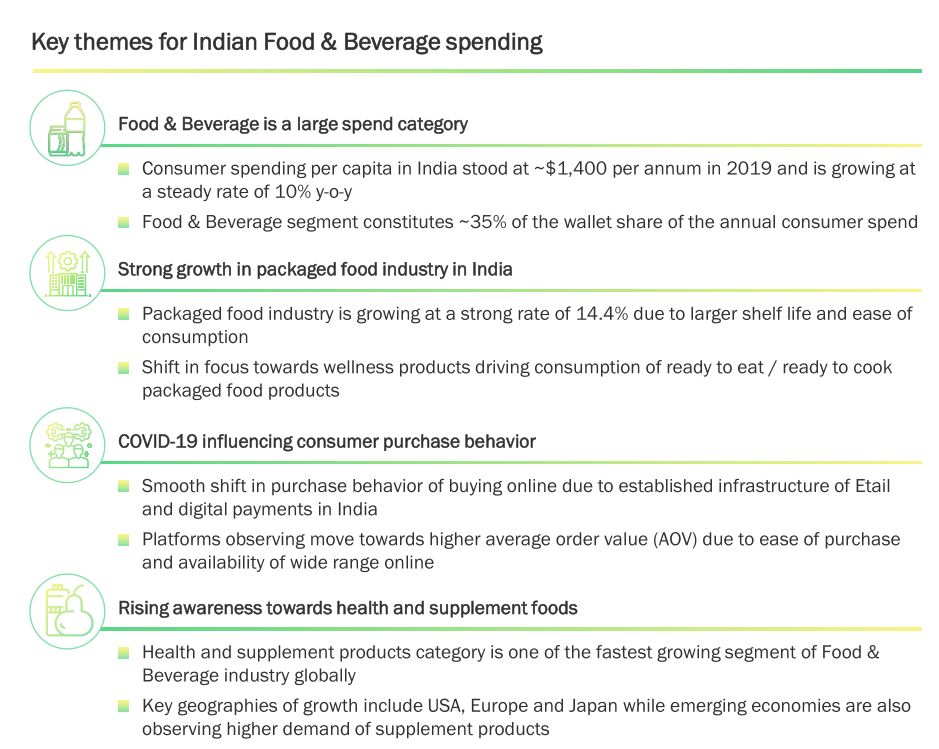

Addressable Market and Existing Landscape

There are three key things happening that make this space very interesting..

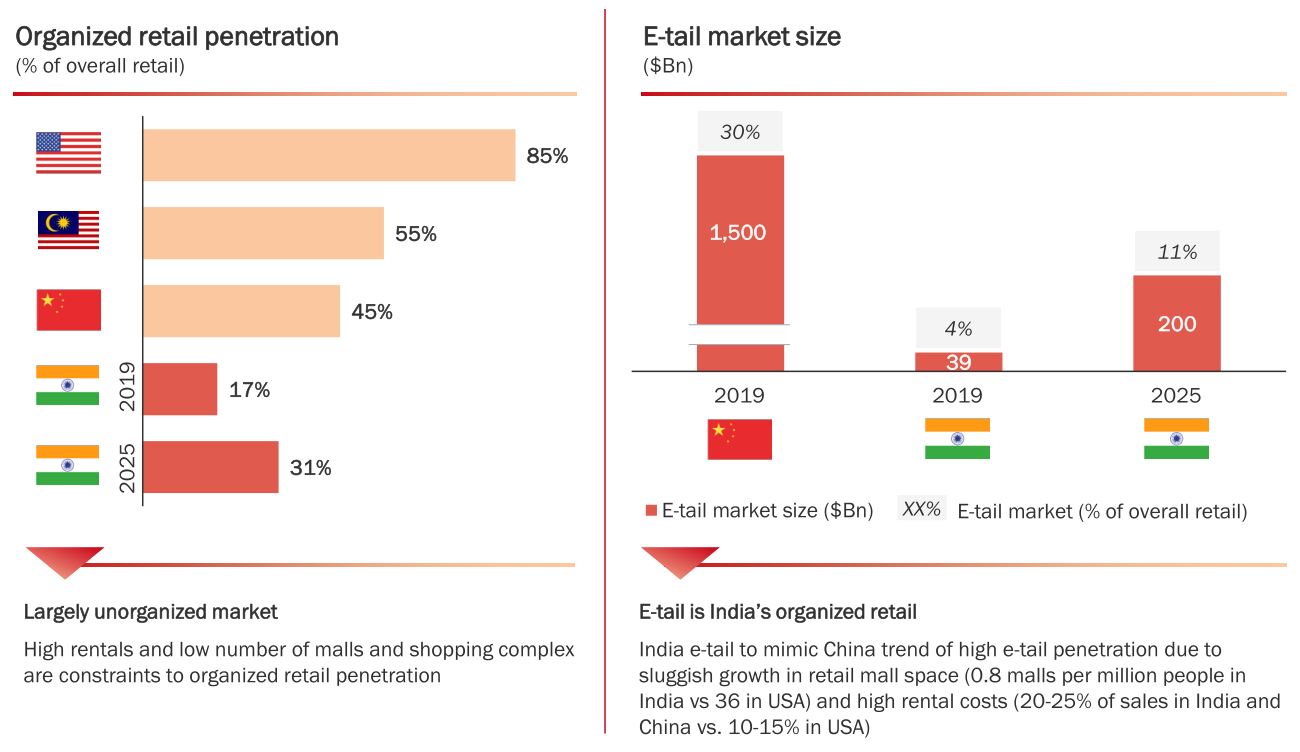

1) Market Size and Retail Penetration

The retail market is expected to grow at 11% CAGR until 2025, but the penetration of organised retail is much lower than other nations. Online retail is expected to pick up exponentially in the next five years:

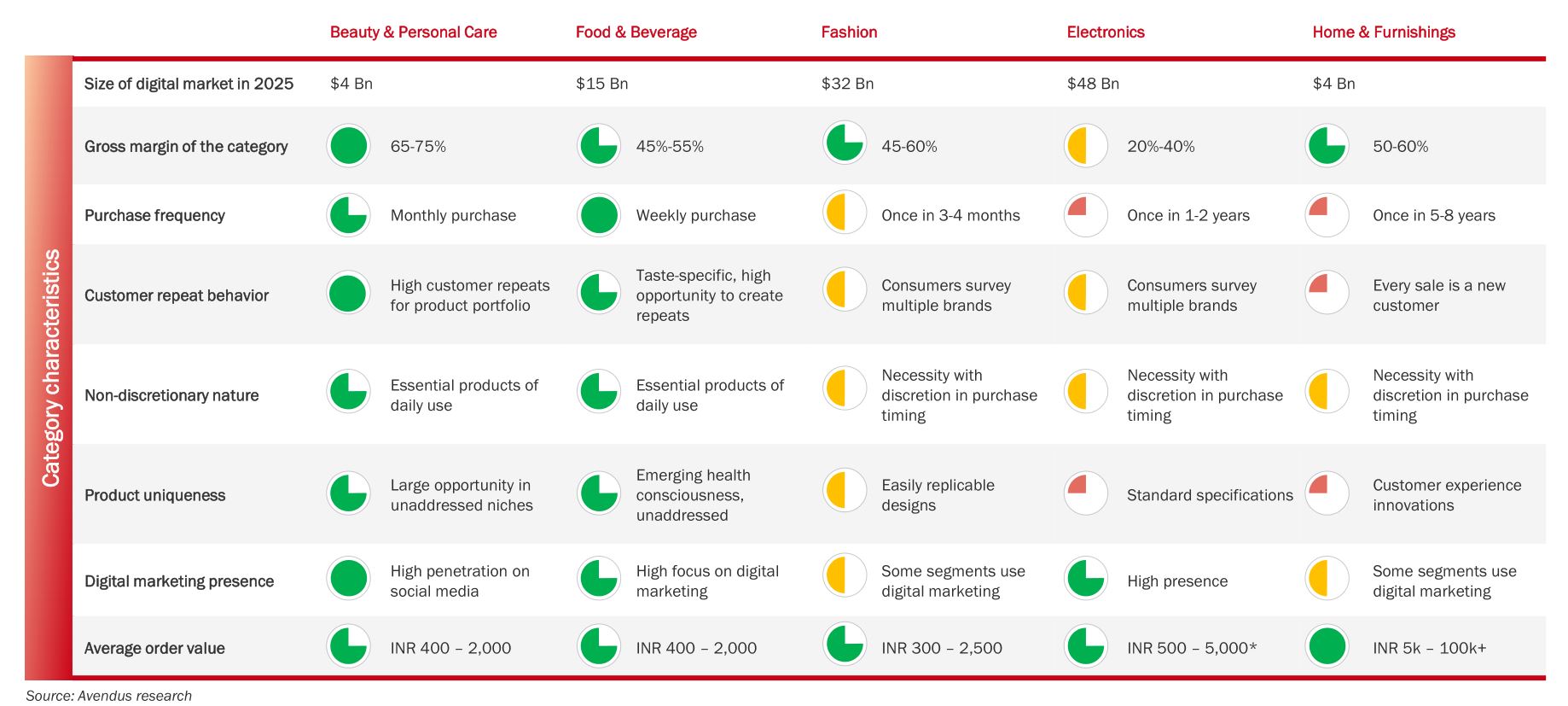

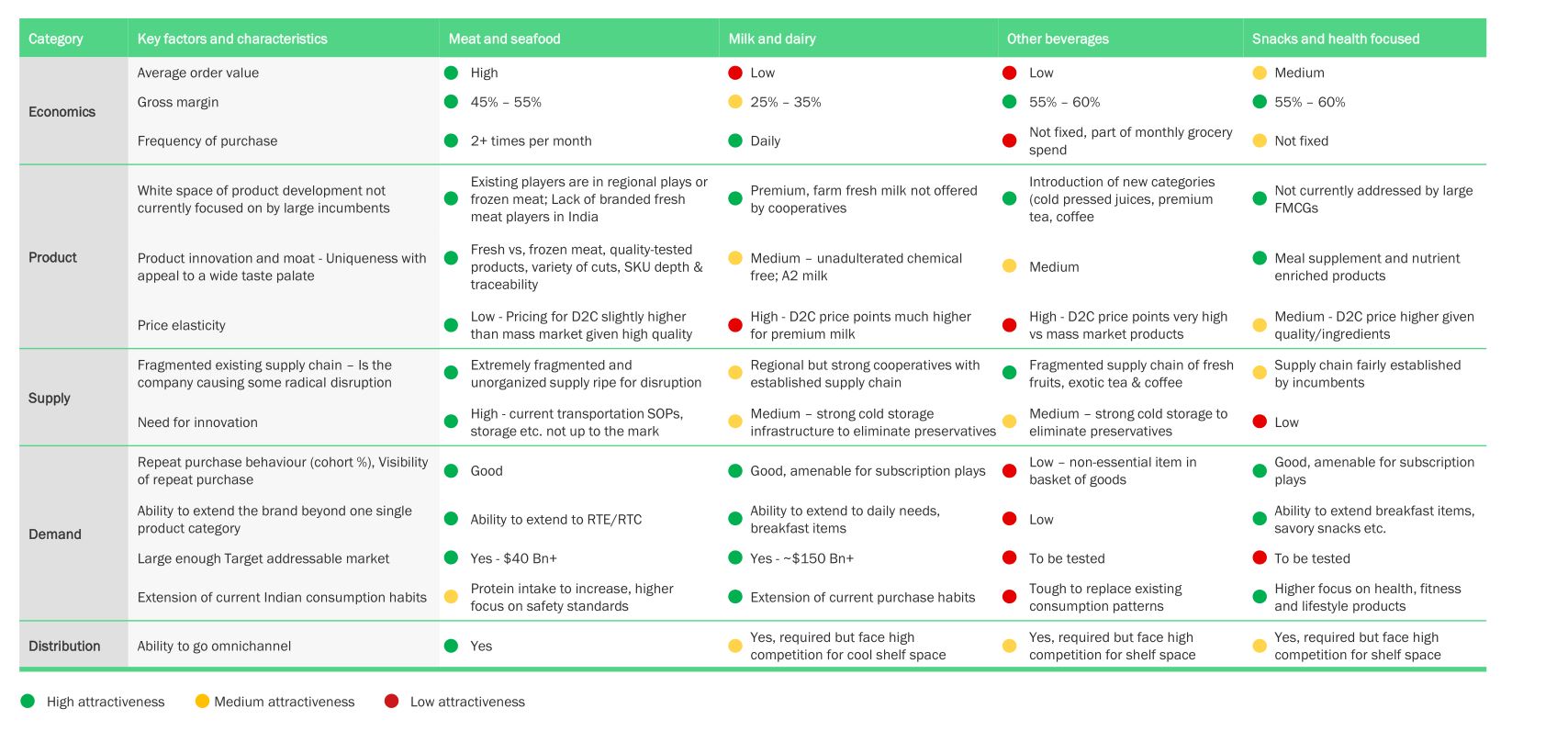

2) Untapped Gaps in Present Sectors

The circles showcase how attractive/conducive the particular parameter is to D2C business models. Some observations:

-

Electronics and fashion have the highest addressable market size, but a nuanced look showcases why personal care / FMCG are more attractive sectors despite having a smaller market.

-

Frequency of product purchase is the highest in personal care and FMCG, while people buy furniture infrequently.

-

Beauty and personal care have the highest margins. This deserves a deeper look when we consider pricing power, brand stickiness, and cost of production for various brands. It’s intuitive why electronics are not extremely high margin businesses.

-

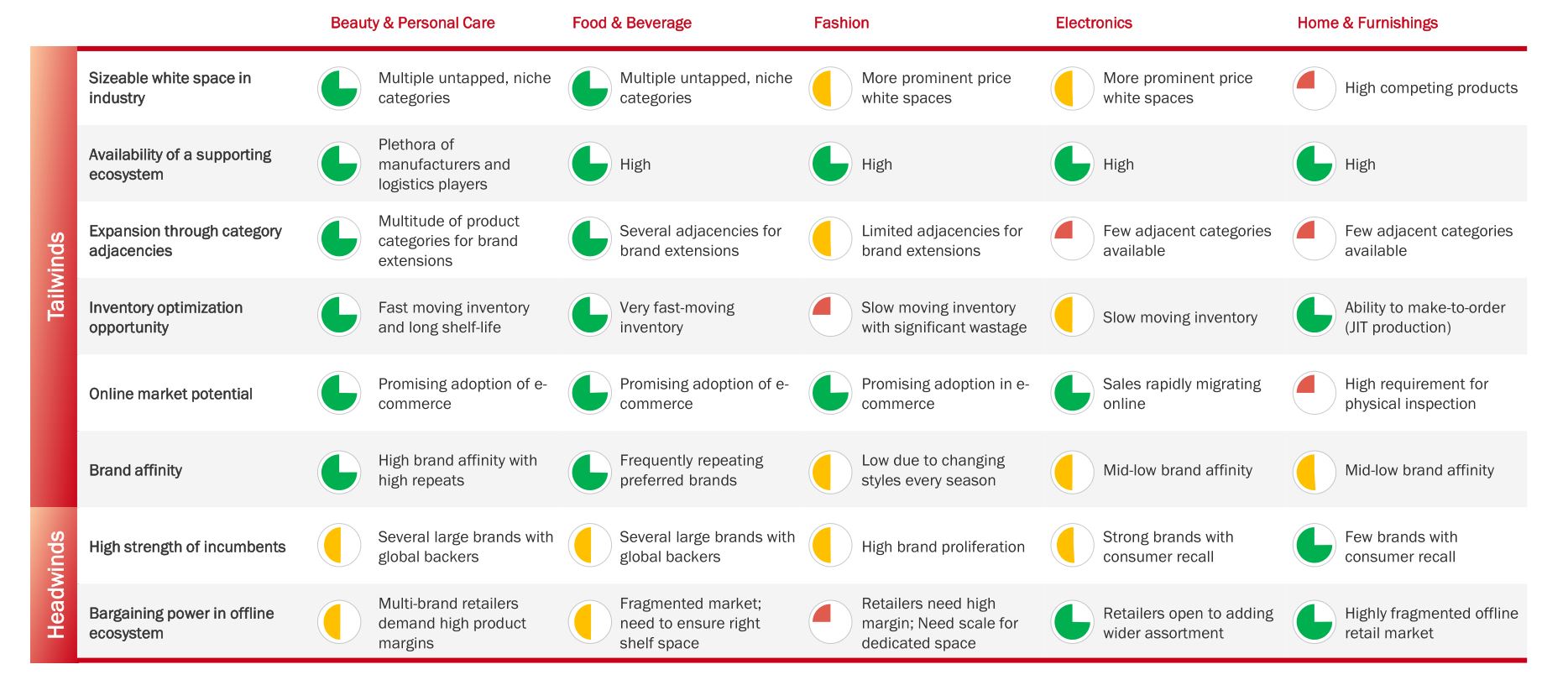

FMCG and Personal care have the highest percentage of repeat customers, and also clear gaps in the market. Within personal care, niche products are unaddressed, and as we’ll see later, products are either low cost or premium, with a large cap in the mid range prices. It’s worth noting the emerging health consciousness in the demand side.

This echoes personal care and FMCG being the most attractive sectors for upcoming D2C brands. There are multiple tailwinds on the supply side, but the largest headwinds concern incumbents in this space, and the ability to place niche products in traditional ecosystems. It’s worth noting that this is different for players in the furniture space.

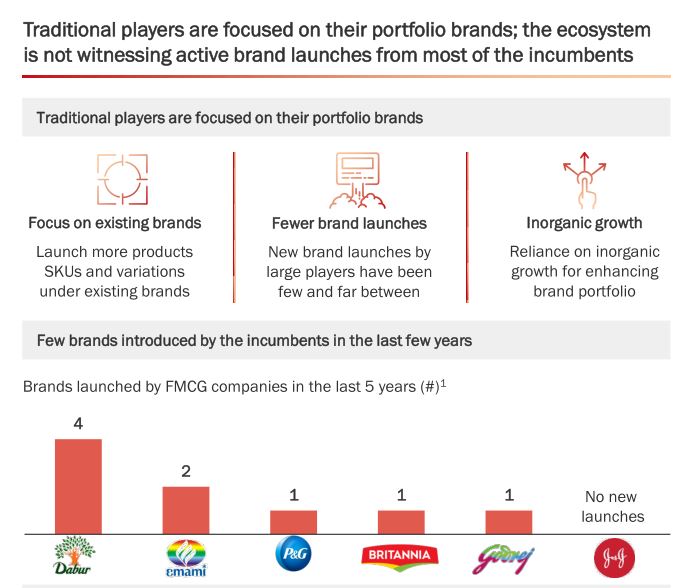

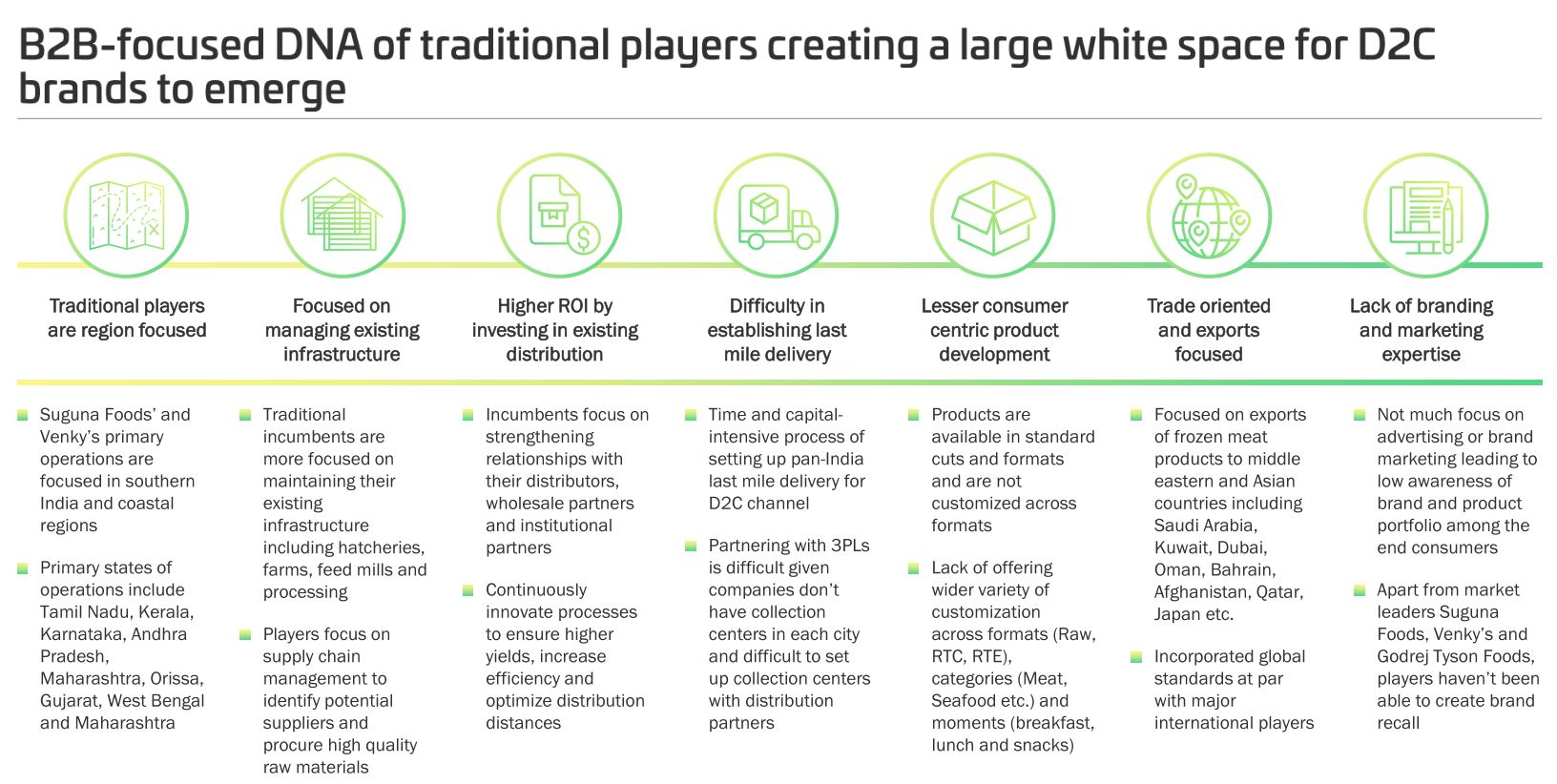

However, this is where we can make a lot of observations about traditional players, and whether they are addressing these gaps in the market.

So from this we can say two things: 1) Traditional players are not launching many new brands but are consolidating and building existing brands. 2) Traditional players are hesitant to explore niche markets due to a largely unadressable market size, a large opportunity cost in terms of strategy, and prefer to start brands in safer segments. This then means there’s a significant lag for these players to make a move, and an early mover’s advantage in niche segments.

Two key questions to answer:

- What is the opportunity cost for new players to enter niche markets?

- Is the best strategy to invest in good emerging D2C brands, or invest in large players that have either ventured into untapped markets late, or acquired D2C companies via M&A…

This leads perfectly into…

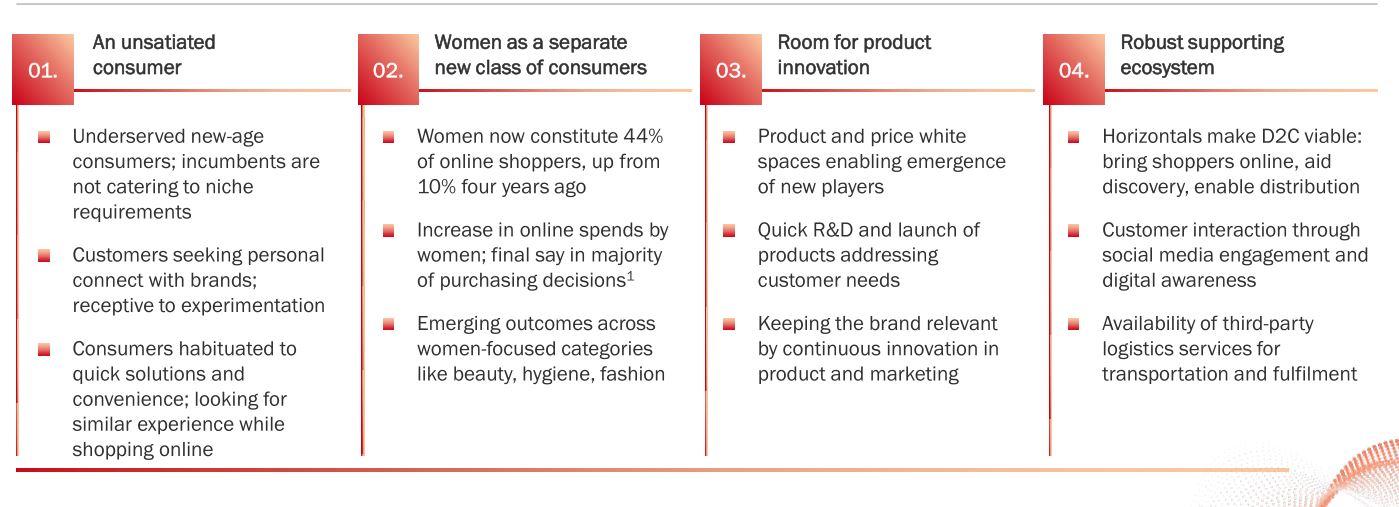

Entry Barriers and Success Stories of D2C Brands

A rise in contract manufacturing lowering the entry barrier for brands such as these to launch their own products, the rise of advertising and shopping directly via social media platforms such as Instagram, the availability of a supporting logistics ecosystem, and the sheer power of the internet to aggregate niche interests has lowered the entry barriers for new players in these markets. The pandemic further accelerated the growth that these D2C players have seen. The report highlights some of these:

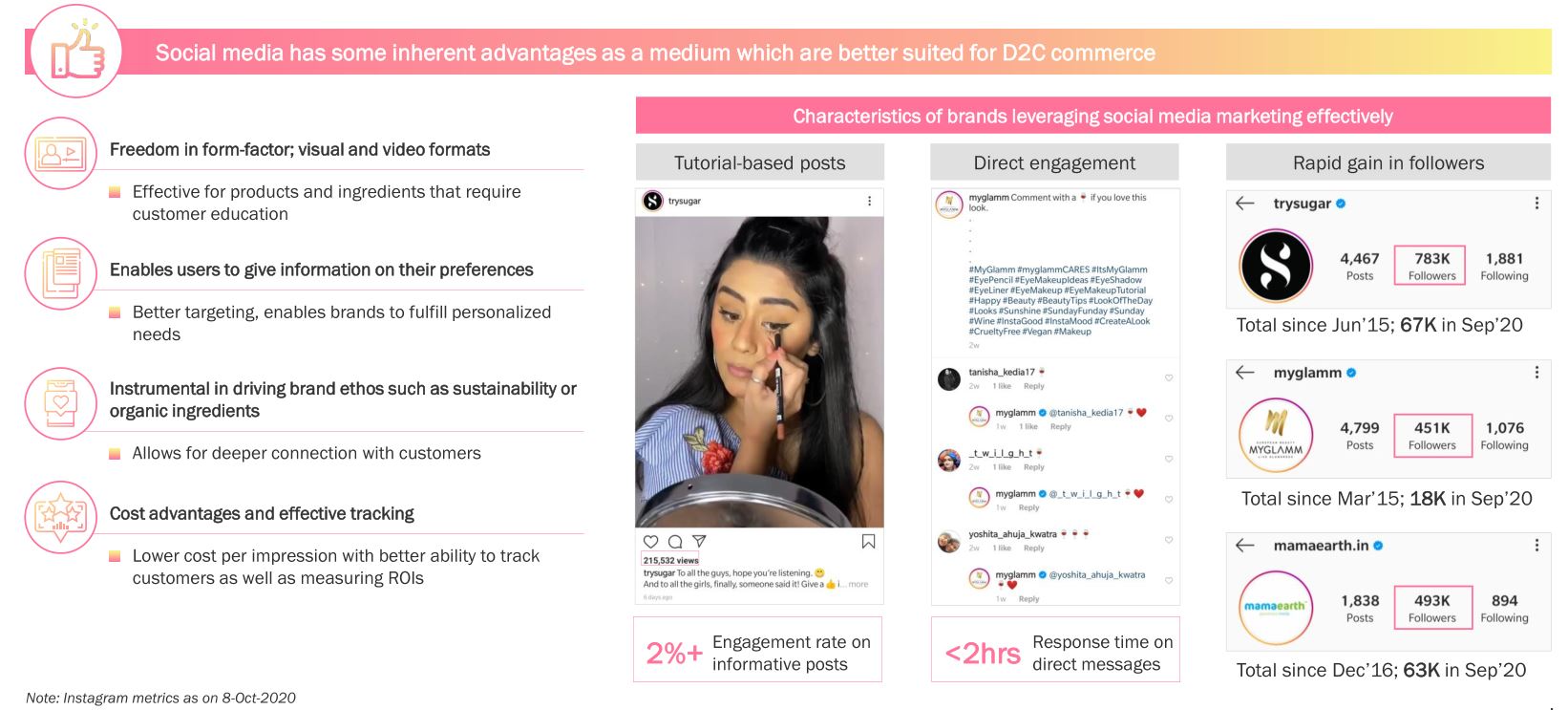

And here is the value that early movers have created by succesfully leveraging social media, and the tailwinds we spoke about earlier:

My takeaway from this is that a good social media policy regarding advertisement as well as customer engagement makes or breaks an idea. Within 5 years of moving into an untapped market, these D2C brands have managed to reach billion dollar valuations, as well as a high revenue growth. This also means there’s a significant early mover’s advantage, and raises questions of how traditional players can enter into these spaces organically. I would like to point out that on social media platforms, there’s a level playing field between large corporations and new entrants. Both start with no followers and your social media policy along with targeted advertisement determines the reach you have. We will see later how D2C brands in India have managed to gain a following.

Personal Care / Beauty

The online personal care segment is expected to grow at 29% CAGR until 2025.

The gaps are very prominent between the entry and premium range, and it’s worth noting that a lot of the premium products are from global brands. It’s worth looking to see if D2C brands enter that space after gaining a significant following. Incumbents have not yet understood how to effectively have an online presence, with online revenue streams being less than 5% of total revenue.

What does it mean to have an effective social media policy?

| Brand | Followers in October 2020 | Followers as of May 6th 2021 |

|---|---|---|

| Sugar | 7.83 Lakhs | 12 Lakhs |

| MyGlamm | 4.51 Lakhs | 5.46 Lakhs |

| Mama Earth | 4.93 Lakhs | 8.17 Lakhs |

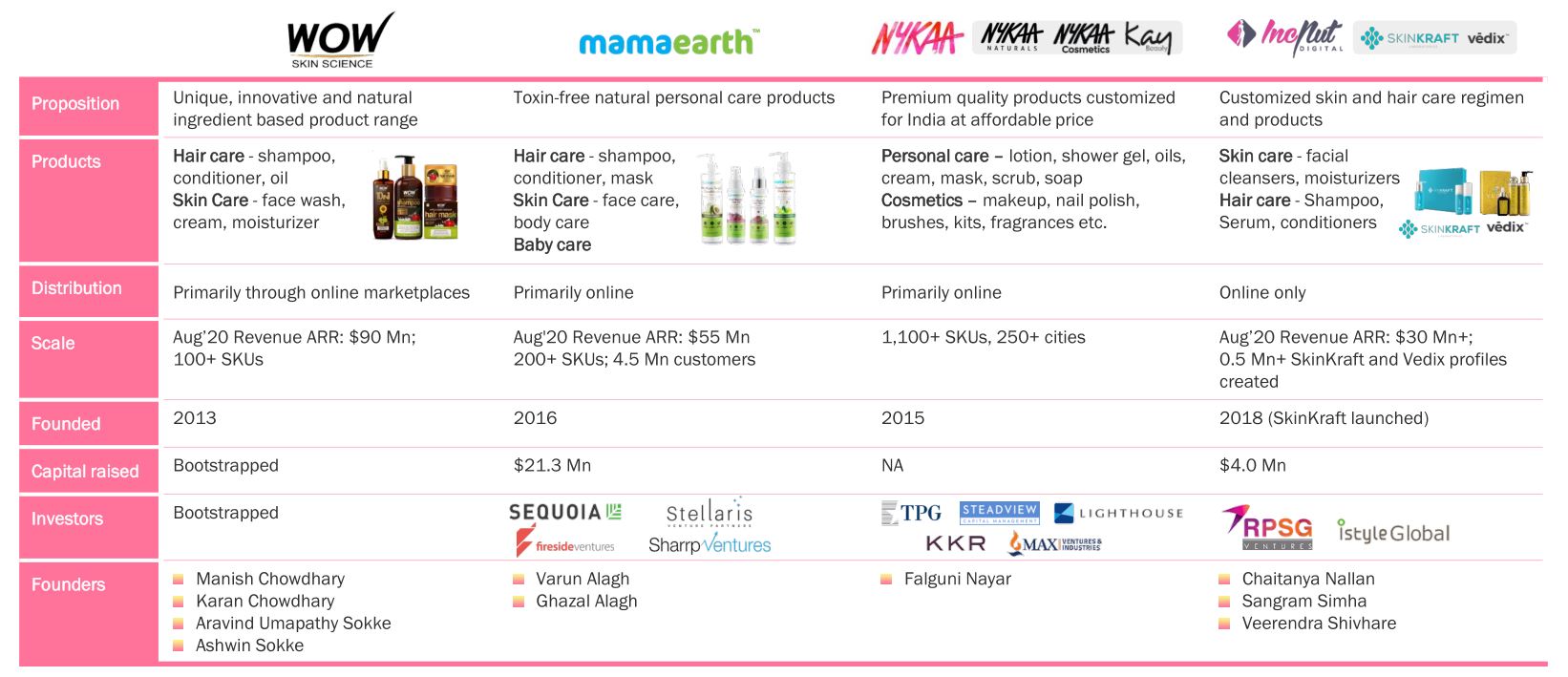

Here are a few players in this space:

Meanwhile, traditional players have started acquiring up and coming D2C brands…

FMCG Sector

The same factors on the supply side regarding logistics, quality control and consumer behaviour apply to the FMCG sector.

However, within the FMCG sector it’s clear that entering into the beverage industry is not the most attractive option. This is due to the fact that there aren’t many untapped spaces within beverages, and traditional brands have already launched products with many flavours and sugar free options such as Coke Zero or Pepsi Max.

While it looks like meat and seafood is the most attractive segment for upcoming D2C brands, there’s still enough room within the other segments for new entrants.

To me it looks a little too early for meat brands to fully disrupt the market, and watching the development of the last mile delivery in the next few years is the key trigger to making sure fresh meat reaches the destination on time. That said, in the UK, brands like Amazon have resorted to new ways of delivering fresh meat and even frozen food: they freeze low cost packets of water and pack meat and frozen foods separately within the ice. However, given that the UK generally has lower temperatures of 8 - 12ºC, this solution will definitely require closer warehouses in India.

Should we see these triggers change in the next five years, D2C meat companies could become very attractive.

On the healthy snacks front, there’s genuine revenue growth for D2C entrants:

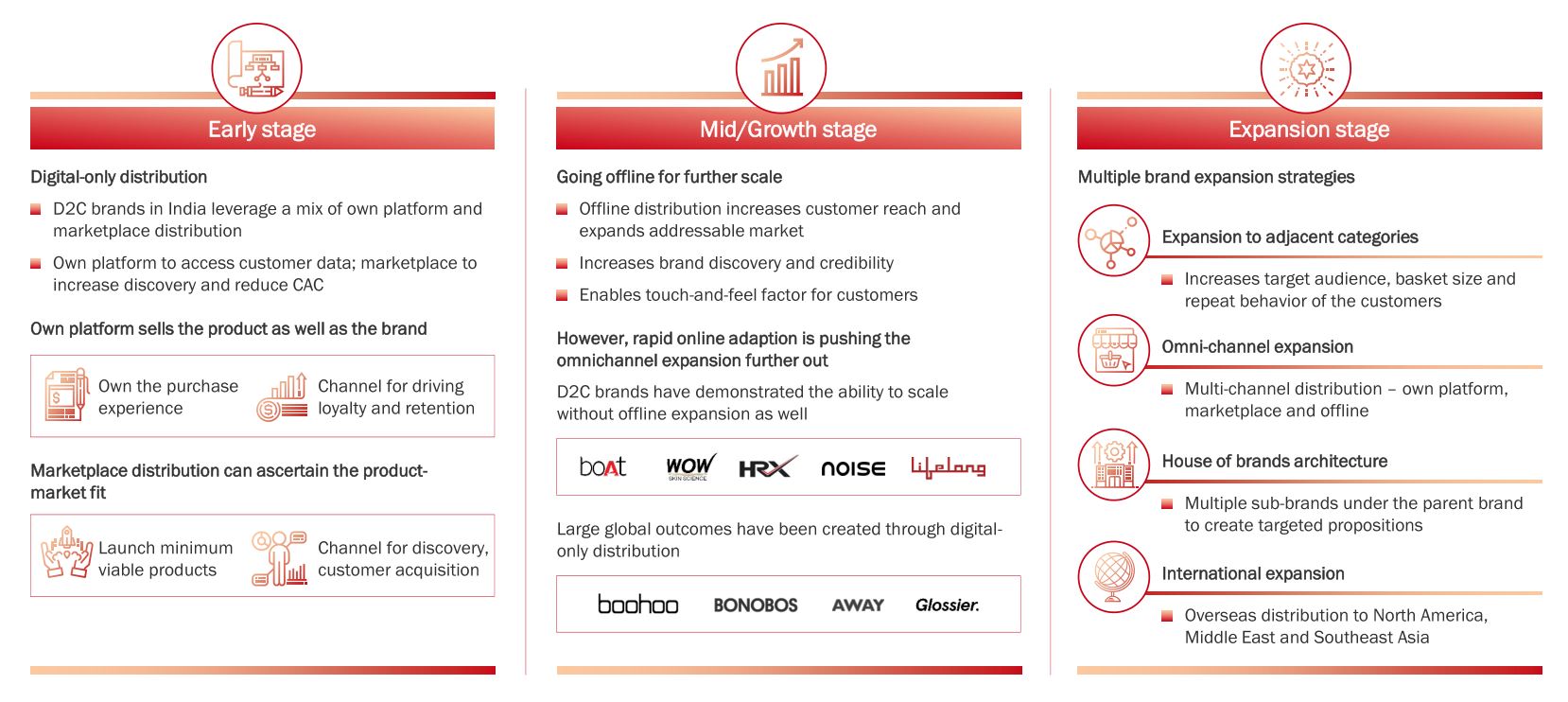

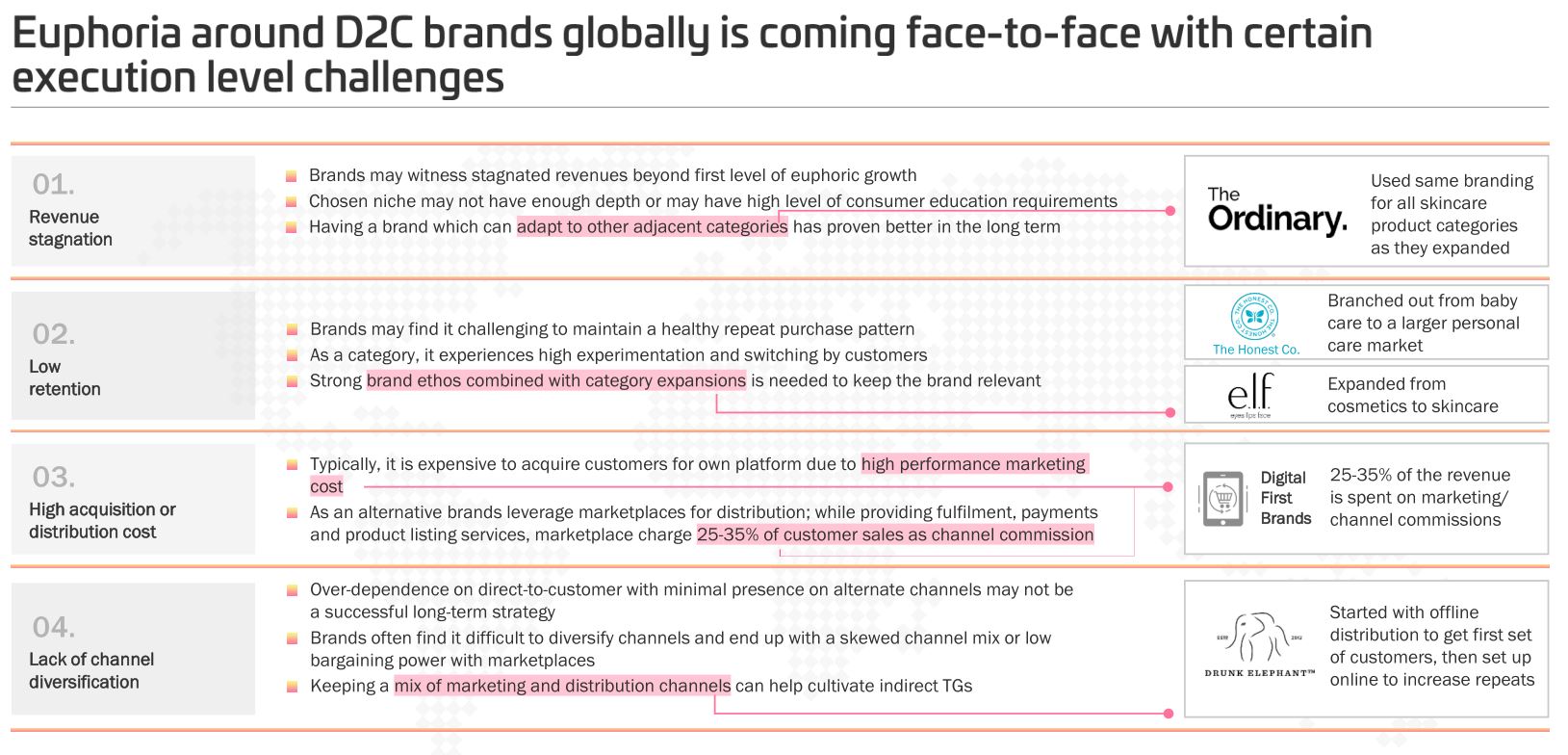

Business Cycle and Challenges

Interestingly, D2C brands that don’t have an exit strategy via M&A have started opening physical stores once they know where the demand for their products lies. Nykaa is the case in point, which I’d say is in the Mid/Growth stage.

The biggest hurdle these D2C companies face is revenue stagnation, and the lack of an alternative channel to bolster their sales:

The questions to ask going forward are:

1. Should investors look to invest in funds that own upcoming D2C brands and IPOs such as Nykaa’s that is reported to be in the works?

2. Is it a better strategy in the long term to invest in traditional players that could potentially acquire D2C brands. The tradeoff here is twofold: the really successful D2C companies may have no interest in selling, but traditional players have multiple revenue streams to drive stable growth. Secondly the upside for catching upcoming brands early is more explosive and ofcourse much riskier than investing in giants like HUL…

3. Would a proxy play on this sector via contract manufacturers be more attractive in the long run? This leads to a conversation between specialised manufacturers such as Galaxy Surfactants in the personal care space, versus diverse manufacturers such as Hindustan Foods.

4. How do we view traditional distribution networks in spaces such as Fashion?

5. What advantage do traditional players have that own their own retail stores? Acquiring D2C players on top of these retail stores would have synergies.

I will expand on the retail sector in this thread in a future post. I wasn’t sure if this analysis was better placed in my own portfolio thread, but I chose to create a new thread given that it’s a discussion on an entire industry and business model that has consequences for many listed companies.

Disclosure - Invested in multiple companies that are in this space. While the research belongs to Avendus, choice of data presented and inferences may be biased This post was to share my readings on the industry, and is not a buy/sell recommendation.