Have been reading about CESC ventures lately. but i am unable to find earnings call transcripts for it. Cant find on their website http://cescventures.com/ Or on google.

Any one has any leads?

Have been reading about CESC ventures lately. but i am unable to find earnings call transcripts for it. Cant find on their website http://cescventures.com/ Or on google.

Any one has any leads?

I don’t think they conduct earning calls. Only last 2020 AGM recording could be seen on their site. Thanks.

I would like to bring up a discussion about the management of this company. Does anyone have any information or experience or opinion on the management quality of the Goenka group?

From my understanding so far, most of the CESC empire is based on acquisitions owning so many of businesses. Sanjeev Goenka and Harsh Goenka are the 3rd generation i guess.

With enough wealth created for their family already, I am trying to figure out If they still have the passion to drive the business to newer heights or are they in capital preservation modes?

@MyCapitalNotes May i know if your views have changed after this post? This still looks like a good play to me. Things that are concerning to me at the moment are

Hi Nikunj,

Thank you so much for your question. No my view hasn’t changed. It continues to remain. I have not added more nor have I sold any CESC Ventures (now RPSG V). Same applies to my Firstsource position that goes with it as well.

The low level of disclosures or the quarterly communications don’t trouble me. With operating subsidiaries of different sizes and in different sectors, I feel looking at it annually makes the most sense. (At least from the view point of my hypothesis. Plus, without the notes to the financials, you can’t figure anything out).

There undoubtedly is a desire to grow backed by money. The moves in the FMCG space indicate that. The kind of money they’ve put into Too Yumm and then spent on building the products is significant. They seem to be employing capable people and some of the operating subsidiaries have shown significant improvement within a few quarters of their acquisition. Building companies takes time to play out (especially the type for which I’ve invested in). With 2020 being the way it was, there would be some delays as well, which is perfectly fine. This is something I’m going to sit on for a long long time unless my sell triggers show up (fraud, deviating from investing in and building businesses, reorganization of the company, etc.).

You’ve been tracking the company for awhile. What are your views?

Yes, i have been reading on this company for a while. My view is to invest for the long term. I am ready to sit on this investment for a few years. I am not invested yet and I am still evaluating the possibility to add this to my portfolio.

Do you also check the subsidiary financial statements annually?

So far, All i could find is two annual reports some poorly scanned quarterly reports.

Looking at it just quantitatively, as you mentioned in your thesis, i agree we are getting a sling shot opportunity. The brands they are incubating are quite interesting.

And since you mentioned Mohnish Pabrai in your thesis, this type of company seems to fit the spawner category which he is endorsing recently. Isnt it?

Also note that Big part of its valuation is dependent on the valuation of FSL. Buying this company would also mean one is bullish on FSL.

and maybe one amendment to the beautiful holding percentage diagram that you created is to make herbolab a 100% subsidiary

I do go through all the subsidiary statements that are published. Since most of their statements are scanned, it’s super annoying to go through it. It would have been much easier if they could only scan the relevant pages and keep rest in their original format.

It’s sort of similar and can be applied here, but the thesis I describe above is a variant of his Dhandho framework. If things work out for one of the big opportunity companies, the upside is tremendous (heads, I win). Because of a discount and a solid underlying business, there’s downside protection (tails, I don’t lose much). So this creates an opportunity where you can keep getting cash every year to invest. There’s sufficient margin of safety for them as well if they go wrong with a few investments.

That is definitely correct. Investing here would sort of mean being bullish (at least, not bearish) on FSL. But the reason I invested in FSL is because of the dividend pass through. The major source of money is dividends from FSL. I don’t see that being stopped anytime soon (timeframe here is in years). So buying FSL gives me access to the dividends coming in as well. Luckily I bought before the run up, so my dividend yield is also very good.

Thanks for that. I’ll probably get around to it the next time I have a post ![]()

I have just initiated a tracking position and would be taking a max portfolio allocation of 3-4% in this stock.

While RPG group is a reputed group but HV Goenka has more robust businesses while Sanjeev Goenka does not have such prominent businesses.

Some of the businesses under RPSG venture look promising but the risks also remain high given the lack of information.

Here is a short summary i found while researching the company

Nice. I had tracking position but had to sell as needed some cash. I am still tracking it and 100% acquisition of Herbolab was something I liked recently. I have developed a unique problem though… After my experience with another “Venture” company - It was from a different group, Max Ventures, I am a bit wary of the word “Venture”.

Somehow, these companies keep looking promising and holding lot of value till eternity. And maybe they may give a spurt of say a sudden 5X or a 10X after holding for 10 years…but even a TCS/HUL gave 10X in last decade or so, along with continuously rising dividends.

If I have to show patience, is it better to show in a stagnant HUL from 2000 to 2010 and use it for accumulation or show that in such “Venture” companies?

At least in this “Venture” case, it has very real cash source in terms of Firstsource and some meaningful FMCG business incubation. Also, the promoters are not someone who keep looking for exits and have long term commitment.

Lets see if I am able to get over my issue with “Venture” firms…Thoughts Welcome!

Disc: Above are just my personal thoughts and not a buy/sell recommendation. I am not eligible to comment on any business. I maybe completely wrong in my assessments and all these Venture firms may turn out to be excellent wealth creators

One more acquisition. Does anyone know what is APA Services? culdnt find it on google

I think Sanjeev Goenka does. Their ambition is to clock 10,000cr in sales of all their FMCG brands combined.

From Too Yum’s Website

Other Sources:

Already clocking around 600cr in sales. Rather comical that the entire company is available for 800 odd crores.

Disclosure: Studying for a few weeks, may take a position soon

i am surprised by low valuations of most Goenka group companies like RPSG ventures and Spencer retail…RPSG venture may carry some holding discounts and also lack of clear direction as venture/investment companies are mostly valued based on the valuations of their underlying companies rather than anything else…but Spencer is very much a focussed operational single company…still.it is relatively very much undervalued compared to peers…

Is there something about this group that I am missing as markets cannot be wrong out of ignorance and these are no hidden gems out of sight…not able to understand clear reason here…

Reason for asking this question was that

I am aware that Sanjeev goenka gave a statement to create a FMCG brand of 10,000cr sales by 2025. And it seems that their accquisitions in Herbolab, eVITA etc shows that they want to acquire and nurture brands under the RPSG Venture Group.

What worries is that there is no quarterly communication or calls from the management which could provide some more clarifications.

This is an interesting chart. We must follow up or try to find out how D2C brands make their next journey from 100 to 500 Cr and then to 1000 Cr.

From what I have seen by following some FMCG firms which own some D2C brands as well - the initial run (maybe first 100cr) is quick in D2C brands and then comes a stagnation due to maybe many me too products in D2C, ecommerce etc. less entry barriers, less known innovation in marketing in this D2C space and many other things which we would know once we think deeply.

For brands to finally become 1000 and 5000 cr and beyond - a significant element of traditional part is needed, well at least yet! Or maybe some of these D2C brands would prove it otherwise in due course!!

Too little information is available to predict the future of their brands but i see a lot of related advertising very frequently, this is the advantage they have as compared to independent startup that do not have the same resources. Their offerings are unique for example, Mcaffeine which has coffee/tea based products, Vedix and Skinkraft have customisable skin and hair care ayurvedic solutions, Guiltfree is focused on healthy snacking, etc. These new and innovative D2C companies have definitely impacted the market and we have seen big FMCG companies like Marico acquiring Beardo and Tata Consumer acquiring Soulfull.

I have invested a very small portion of my portfolio in this stock that i would be comfortable losing and this investment is purely for the fun and excitement of being able to invest in a venture fund. I will only consider increasing my position here if they start giving better and more detailed disclosures in the future along with better results and a clear strategy.

Almost all of the businesses they’ve acquired are weird, disruptive, and extremely forward looking in terms of capturing a younger, non traditional market.

Over time in London, supermarkets have gone from offering 1-2 vegan options in the whole store to entire sections of the stores offering healthy snack alternatives, plant based meat, and vegan alternatives to dairy. People are giving importance to environmental sustainability (in clothing too!), fitness and general wellbeing. Whether the same happens in India as products like these become cheaper and ubiquitous is yet to be seen, but it’s likelier to be accepted by the younger market.

While studying these startups, I was amazed by how good their social media presence is: they post the right kind of content frequently and engage with their customers. They’ve got pages on every platform, and a dedicated app for each startup. I’ve also noticed my friends have used these products and are now regular customers.

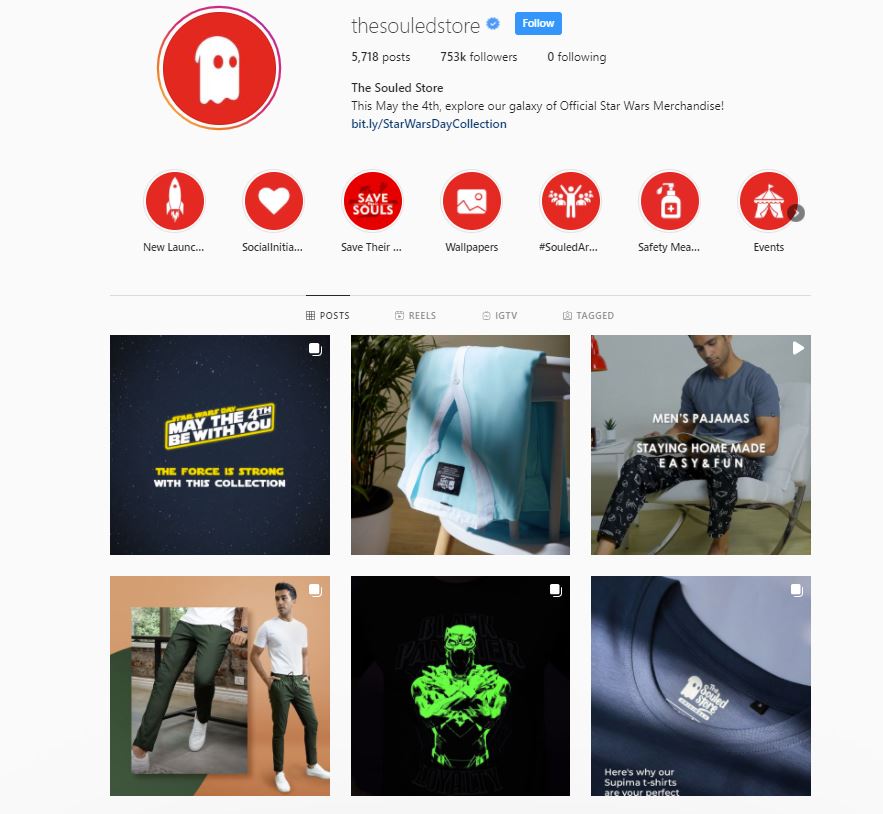

Take the Souled Store, they’ve got over 750,000 followers and over 1 million downloads on their android app.

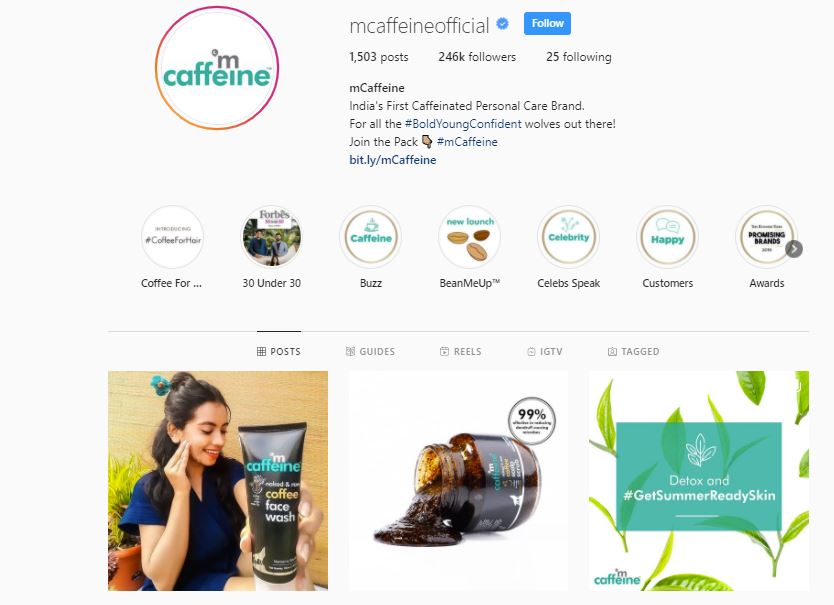

mCaffeine already has 250,000 followers.

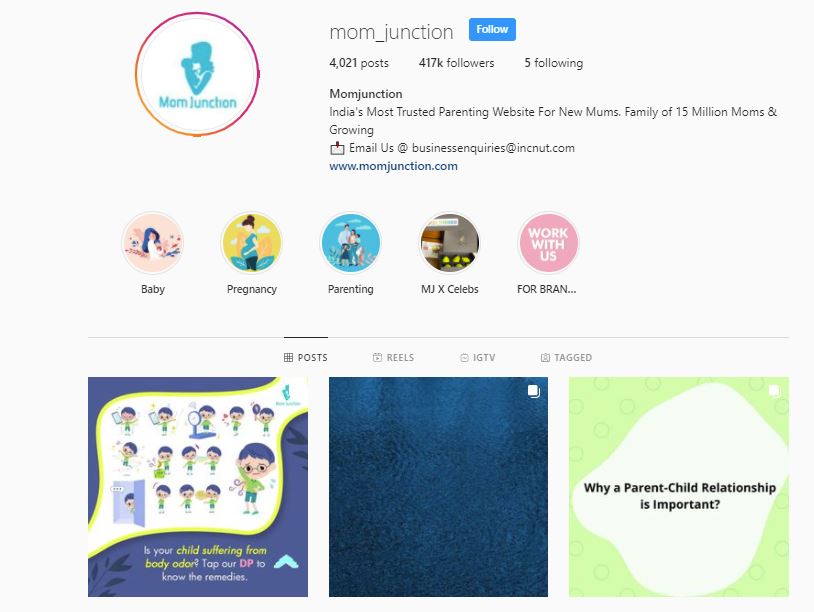

Mom Junction has over 400,000.

I’m not attaching images for all of them, but you would have noticed that they’re really good with arguably the hardest part of a new product: brand creation.

Overall,

| Brand | Followers |

|---|---|

| mCaffeine | 240,000 |

| Souled Store | 750,000 |

| Mom Junction | 417,000 |

| Style Craze | 607,000 |

| Nature’s Basket | 80,000 |

| Vedix | 282,000 |

| Dr. Vaidya’s | 40,000 |

| Spencer’s Retail | 13,000 |

| Skin Kraft | 320,000 |

| Total | 2,750,000 |

If they continue to play the social media game this well, it should be a great driver of traffic towards their products, and it’ll be worth revisiting these numbers 3 months from now to understand how their brands are being perceived. I was intrigued when I saw these names in the business structure, but it’s hard to gauge the scale of a startup from just a name on a page. Seeing that they’ve managed to get this large a following has made me sit up and pay attention.

I also noticed something while trying to understand what Bowlpedia does. Reading this thread, it looks like their waffle and toastee business is known, but they’ve silently ventured into frozen ready to eat biryani and waffles. I couldn’t find more information on google, but there’s a very brief mention of this on page 22 of the 2020 annual report. Take a look at the website.

From the instagram posts, they’re leveraging Nature’s Basket and Spencer’s Retail to sell the frozen foods. Given how unique they are in this space, and Jubilant Foodworks’ analysis on how biriyani was the most ordered food on Swiggy/Zomato, I think this venture is incredibly under-advertised especially considering how well they’ve advertised the other brands, and also considering the opportunity size. I would be shouting about this from the rooftops as much as they are with TooYumm.

I’ve also come across Sanjiv Goenka’s links to the Mamata Bannerjee administration, and this old article from 2016 is a nice read on his ability to navigate the politics of West Bengal. Given the outcome of the elections, there shouldn’t be any surprises to the story on that front, and if the relationship has benefitted the RPSG group, it will continue to do so.

Disclosure, invested in RPSG Ventures.

I would say good going and nice way to track startup brands and we must revisit these numbers every Q. Having said that, you must notice that most established of brands is least followed like Spencer’s (flagship brand of Goenka) and nature’s basket ( the turnaround acquisition from the Godrej)… So what does these numbers tell us…well something…

Also, many ecommerce brands)new brands have a very annoying way of tricks and promotions making you like their pages and what not…the only purpose this serves is some short term marketing…

Having said above I would not dilute the enthusiasm your post brings and would myself like to follow these numbers and evolve my belief…as till date I believe that even in today’s digital world, there is no substitute to the slow, grinding hard work of sales & distribution, supply chain, inventory management etc. that transforms companies from some commodity oil to branded essentials and finally to full fledged foods and personal care giants…

I agree, but I think you’ve drawn a false dichotomy between the two. Efficient sourcing, supply chain management, process automation, etc, while important, fall under the supply side economics. I’m looking at additional data points in the demand side to see if we can say anything more about these brands and products.

Of course, you’d have to have a conversation on brand visibility. I’m not claiming that there’s a simple linear relationship between followers and footfall. Spencer’s has been around since the 90’s, with over 150 stores around the country. We’ve all been to one at some point in our lives, and you’ll always see one when driving around your city. I ask you the same question with emerging D2C brands without a single physical store. How do we measure brand visibility? Where do we look for footfall? And as a corollary, if you owned a caffeine based beauty products brand, how would you even begin to make the choices on where to place a store?

There’s a lot to be said about the internet being an aggregator of niche interests, and I think they’ve been very smart with how they’ve used social media. There’s so much value that any competent data analyst could pull from their social media following / web traffic. For example, analytics from social media platforms could tell you that 44% of your following is from Bangalore, which could mean that opening a store here may be a great idea. Analytics from people that react to your content on a daily basis will by nature be far different from delivery data that you get from orders on your website. The ability of these companies to reach millions of people in exactly their target audience though their own platforms is something that drives valuations in the digital world.

If this was a trick to gain likes, you wouldn’t see content that’s being engaged with every day, and from the look of it, the numbers are consistent. In the last 24 hours, here’s what they’ve talked about:

I’d ask you to visit these pages and perhaps you’ll change your mind.

I also want to share a study on D2C brands that mentions mCaffeine and some of the other brands, will do so tomorrow.

@Chins Nice Writeup And i am equally excited about these brands which are hidden under the hood of RPSG Ventures.

Any idea about their recent acquisition of APA Services? I couldn’t find any information about it