Another acquisition of “Interteleco International for Modern Communication Services”. The Target Entity was incorporated to carry on the business of modern communication services and integrated services for mobile communication.

Presently, Route Mobile does not have any presence in Kuwait. This acquisition of the Target Entity will help establish its direct presence in Kuwait and thus augment its business horizons and integrate its business verticals in Kuwait.

Good results by Route mobile.

Need to watch the management commentary today .

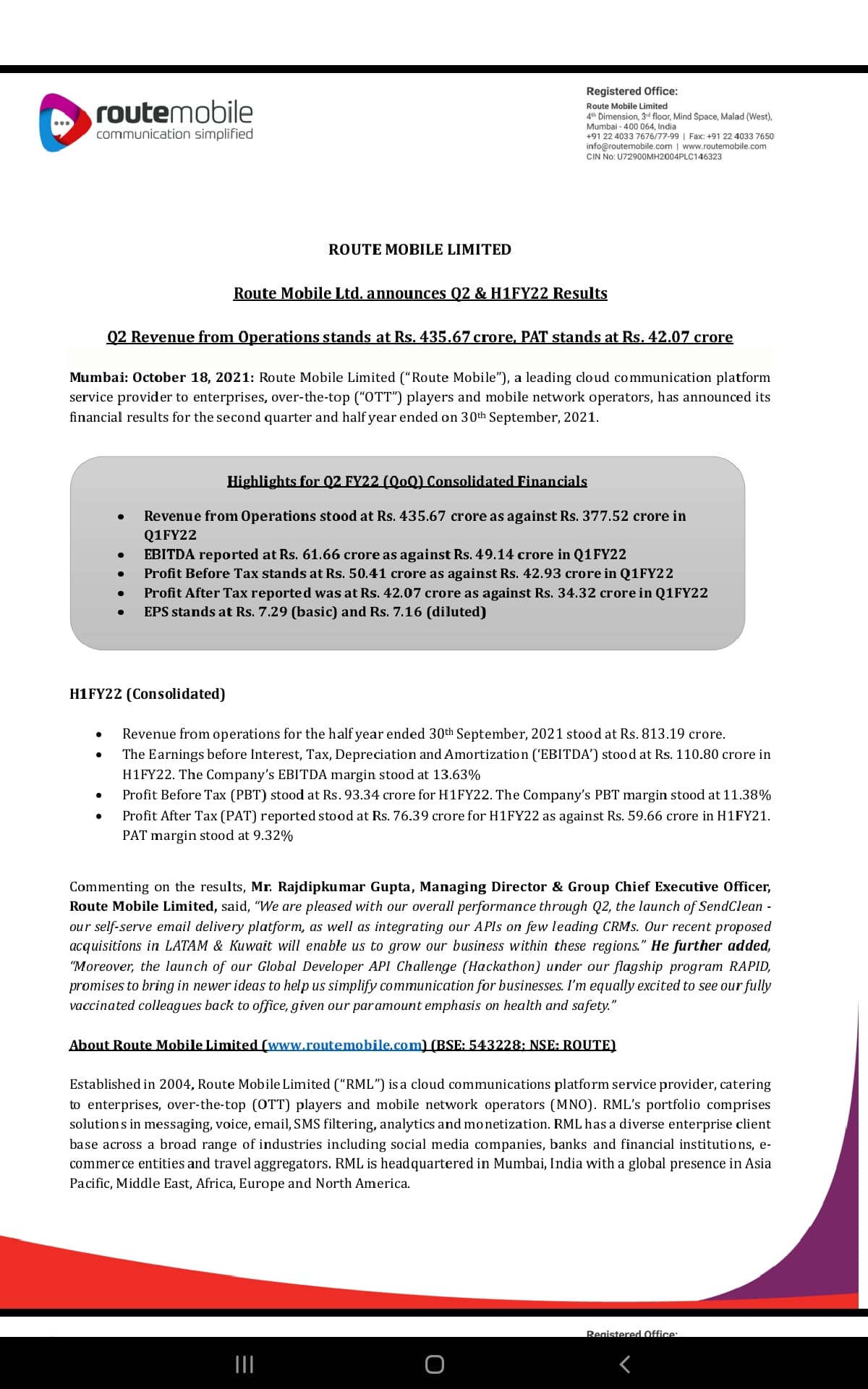

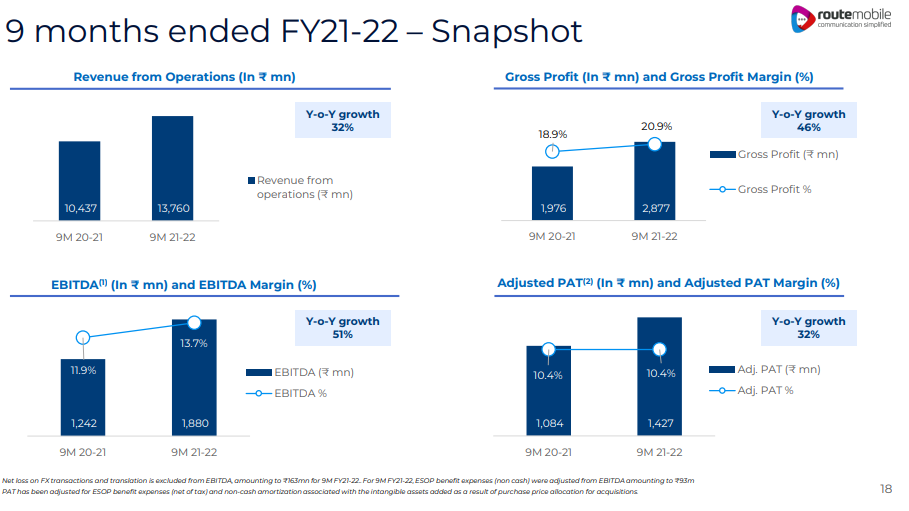

It also appears the issues of the past quarter ( DLT, data breach etc) are through , resulting in 435 crores of sales )

Growth strategy is to add geography expansion via inorganic route - focus on LATAM, Gulf - these are higher margins geo( mature though in volume growth)

Second dimension for growth is increasing products Basket and cross sell

India biz as share of whole biz going up

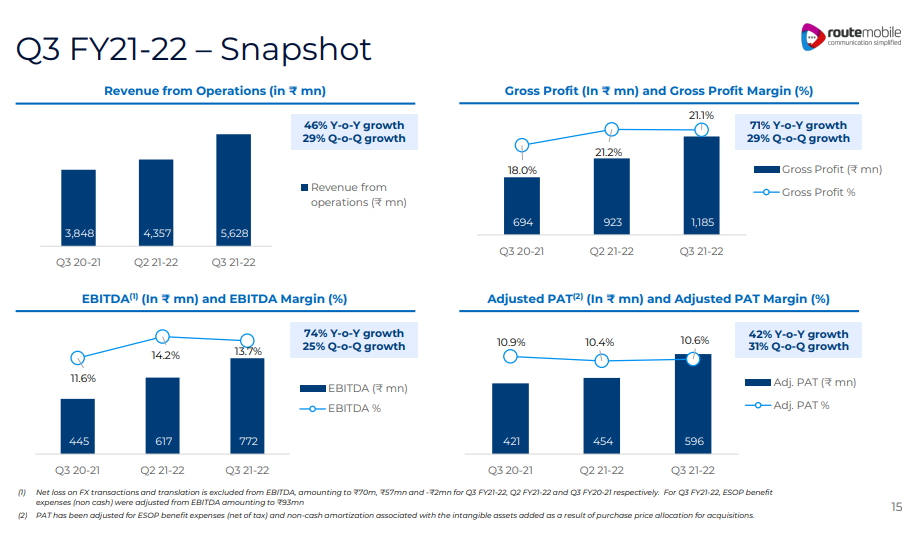

Q3 is seasonally best Quarter

Commenced 1000 seater facility for customer support, 0lan to extend this many folds over 5+ years

2000 cr to be raised( approved by board) to fund future growth including recently announced expansion

Attrition is at 19%, ESOP plan in place to help here( mgmt called out 30% of Attrition as involuntary)

Newly launched products showing good growth- sendclean, selfserve etc.

LATAM is heavy on whatsspp messages, margins profile to be better

Competetion ( Twillio) acquisition in India doesn’t affect us - neither pricing nor mkt share - mgmt view

RCS services to add in Q3

Cash balances of 400 cr

Cash flow is negative due to Tax related settlement- one time affair- (This part wasn’t clear)

Overall per msg realization slightly down due to India proportion going up

Summary - on annualized basis, at 13K cr mkt cap, 6.5 X sales and 50X EBDITA, 65 PE. CPaaS market is growing at a very healthy rate and efficient players will continue to grow at 20%-25%+ rates( combination of organic and acquisition), its a low margin and high volume game, Route seem to be clearly aggressive on Acquisition. With volumes increase there is room for operating leverage, new geo and new products can fetch higher margins. Need to watch cash flows and capital allocation efficiency.

Around 5% transactions were on RCS for which they did not charge to the customers and will start charging them from Q3. The realizations will be in between SMS and Whatsapp charges for the RCS.

One point on which there was not much elaboration from management ( nor did anyone in the concall ask much in detail) was how and when exactly will the 2000 crs be utilized ( I know they mentioned a combination of both organic + inorganic) but why 2000 crs ? 2000 crores is more than the entire sales for the company…

Can we assume that the organic portion is mostly for the planned 1000 seater facility for customer support ? Did the management share any figures for the unit economics for this 1000 seater business unit and its revenue contribution going ahead?

I am particularly excited about the commencement of RCS related billing ( from this quarter) as that will kick in more operating leverage going ahead.

I was too was hoping someone on the call would ask this. With the addition of 2000 Cr company would now have a cash of around 20% of its current market cap. RM raised 600Cr in the IPO a year back at almost 1/10th of the current market cap, quite a re-rating!

LATAM will be one of the larger market to grow CPaas after Asia. We got 2 markets covered- Columbia and Peru. We have presence in Chile and this acquisition also opens doors for Brazil. Overall combined synergies to cross sell and upsell. Eg, they are sending 400-500mn emails using 3rd party, and they will immediately start using SendClean. LATAM is whatsapp market and we will bring lot of synergies, being partner of whatsapp.

Kuwait- Limited players who are evolved. Its an integral part for our vision and story. Saudi, UAE, Qatar, Bahrain, Kuwait are key geographies.

Overall portfolio of Route is well covered but voice is only for the enterprise segment but we want to get into contract value solution option and we are looking to have some acquisition in this space. We are looking fwd to have this as part of our portfolio. Very soon we will like to do something in this space

Call2connect will increase and we have set a target to increase capacity of call center from 1000 to 5000 seater capacity within 3 years. Changed to an aggressive leadership here.

RCS monetization- 850mn messages in Q2. We were not charging anything in Q2 and already started charging in Q3. Adoption ratio is still not very high, but we are getting good response. We believe it has good future, already onboarded customers who will pay per transaction

ILD termination charges increased from July. It has increased and will add more to our revenue. Various international customers started using our platform over ILD.

Cash on books 400cr. Acquisitions will be closed in Q3

Twilio/synch entry into India to affect relationship with facebook for eg. We have deployed our firewall with 2 operators in India. That gives price advantage. We are monetizing revenue for operator in terms of providing firewall technology to them to plug leakages. None of the Indian players have that kind of stack which we have. We dont see competition, in fact we see more traffic and bigger opportunity.

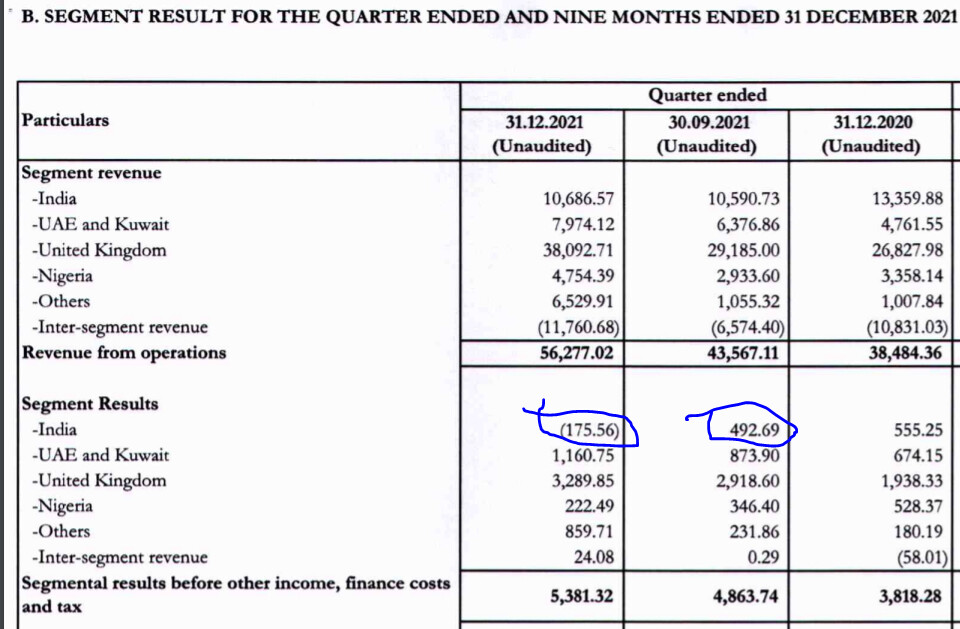

Growing in India (domestic clients and international messages terminating in India, this is captured in slide 18) at a very strong growth rate. Q1FY22 was 33% of revenue, Q2 is 54% so we are growing. We setup the India enterprise team in 2016-17 and since then India revenue has increased 5x. Market is growing and we are gaining market share.

Any change in guidance? Seeing strong momentum and this should continue.

ex-India volumes have been stable

2000cr is an enabling resolution to pursue inorganic and organic growth strategy. Inorganic strategy will be either for geography expansion (focus on LATAM, GCC) or product line expansion. My comment- companies always take a higher than required approval so that they dont need to do it again and again

Hiring focus is Sales and product developers. 30% attrition is involuntary based on poor performance. Havent seen too much attrition at senior and mid levels. Level 1 and level 2 are intact. ESOPs will help them to stay motivated.

Hi I am new to this company. The revenue from new products segment is sub 5%. any guidance from management regarding where this segment can grow in 2-3 years in terms for overall revenue contribution ?

Growing, runway is good, their Gross margins are still low , its a Saas company. And especially India business isnt providing any profitability, anybody any thoughts?

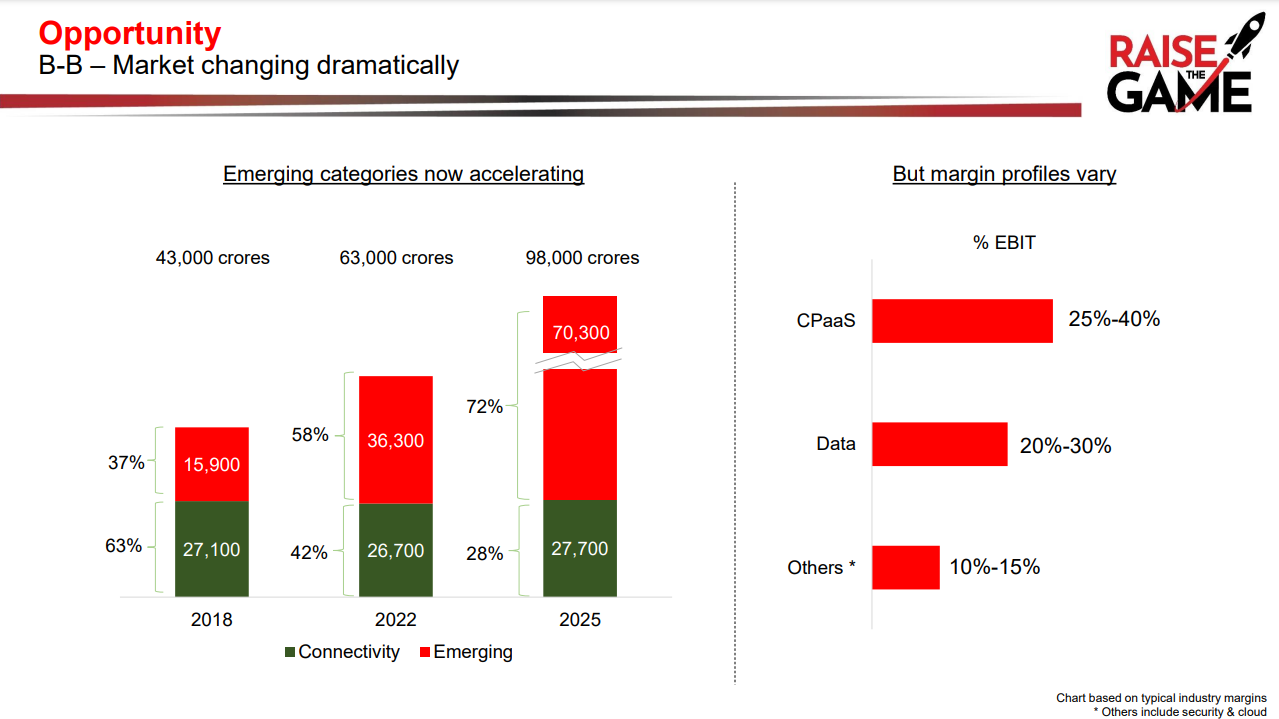

That looks like a 30% CAGR for emerging categories from 2018 to 2025

The lions share of profits in the CPaaS category are taken by Operators with EBIT margins ranging between 25 - 40%. I don’t think operators will give this up. Aggregators therefore will continue to have low to mediocre margins for their SMS business.

For CPaaS companies new product lines are the way to improve Margins. Last FY RM did around 80 crores from new product lines where the gross margins are around 40%. They intend to double this business to 160 crores in FY23, which should support their EBITDA margin target of 13 to 13.5%.

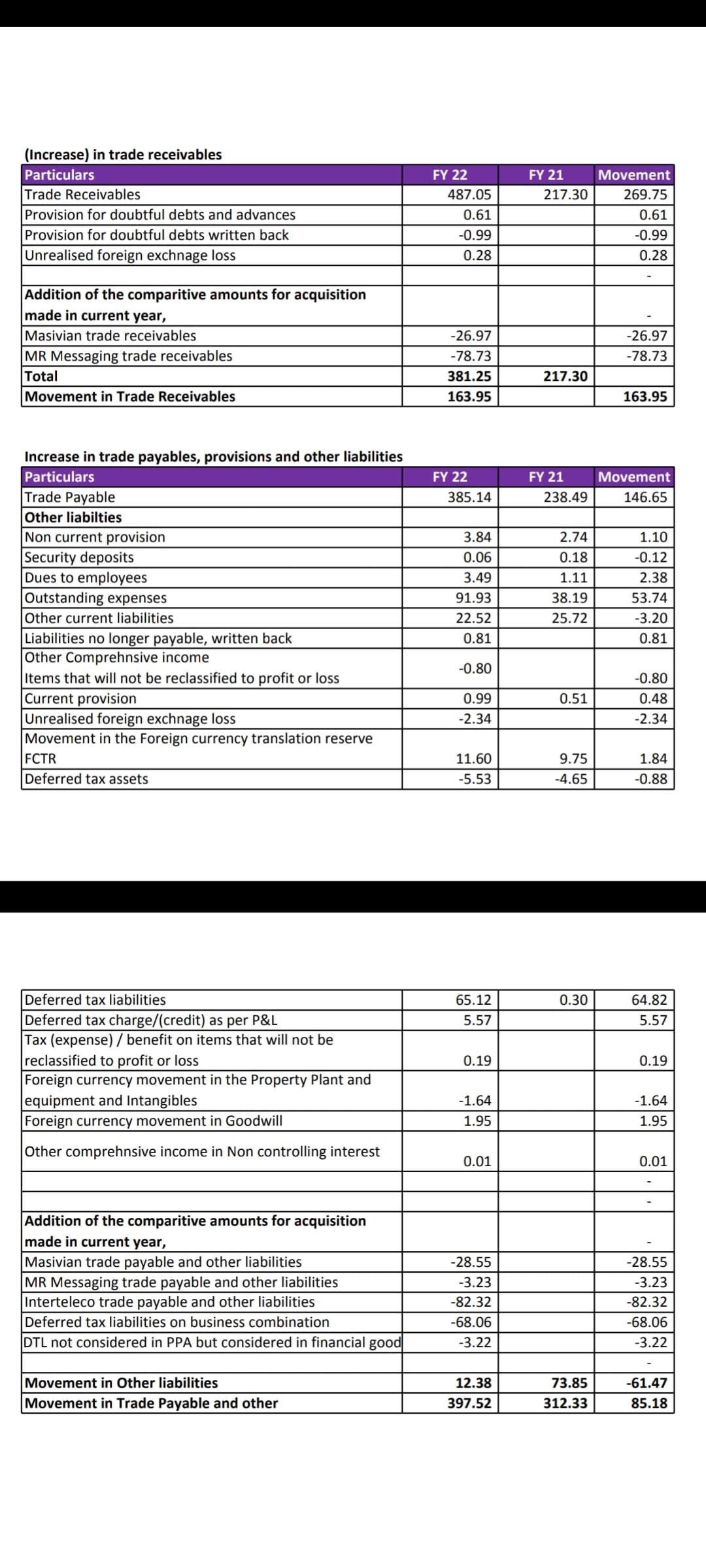

Finally i have got the clarification from management regarding mismatch in cash flow and balance sheet due to receivables and paybles Adjustment to WC in cash flow break up.xlsx (11.7 KB)

@Naveen_sharma Can you elaborate more on this clarification regarding cash flow and balance sheet which Management has given. It will help understand more on Balance sheet.