• Uptick in pace of digital adoption: For POC – earlier used to take 6 months, the same customer is now doing it in 3 weeks

• Upsell: Pitching multichannel multiproduct approach on the same client. Somebody who was buying SMS is also now buying email, also buying WhatsApp & so on. Trend is increasing month on month qtr on qtr.

• New product momentum: Have done a detailed assessment of product market fit in each geography. If in some market Viber is more popular or facebook Messenger is more popular or RCS is more popular or MMS is more popular - equipped to handle that delivery

• Under John Owen’s leadership will look to increase team strength in Europe & America.

• Phonon acquisition: Very limited overlap in clientele. They are strong in Aviation & BFSI; Business has 40 to 45% gross margin

• Acquisition update: Looking to do a few more in coming quarters to augment product capabilities further. 2% of revenue earmarked for R &D spend besides the acquisition cost

• In terms of benchmarking on platform capabilities– we are there among the top 5. Companies like Infobip, Twilio are using our platform in some parts of the world.

RM partners with Emirates integrated telecommunications Ltd for a SMS-hub as a managed service.

The SMS firewall Product will also be leveraged for revenue leakage detection.

The major MOAT for ROUTE is the relationship they have developed with existing clients and MNO, but when they enter the high margin segment of Whatsapp Business, RCA, Viber, Voice-based services, will they still be able to leverage the current network, yes cross-sell would help the company, but in SAAS Based services there is quite a higher competition from a lot of budding startups.

Thus if anyone could share their views on this

P.S.: One Possibility that may happen is ROute may start acquiring some startups in the chatbot space and other segments which the wish to grow which mgmt has directed towards .

Wonder if RM bulls have read the DRHP. Go through the related party transactions, the IT cases and other litigation against promoter and company, promoters needing IT dept permission to travel, promoters getting paid via subsidiary. Lot of muck!

Please mention specifically about which RPT, litigation, IT cases you are referring to. This will help to assess the gravity of concern.

PS: every company have something negative in their DHRP, need to see the potential impact, not in isolation.

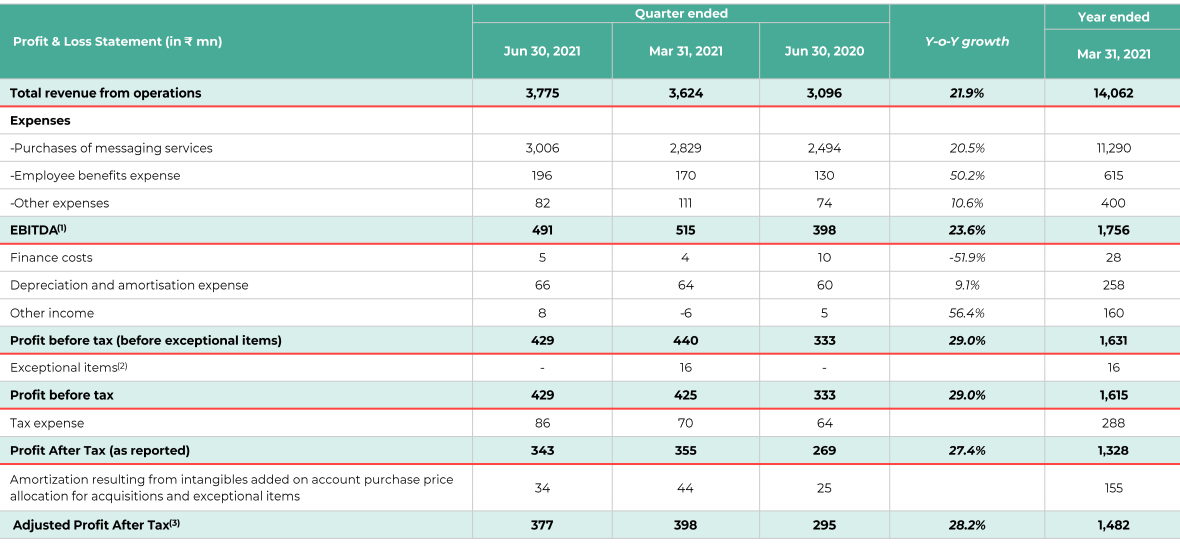

Revenues +21% YoY and +4 % QoQ. Revenue perhaps a little bit weak due to business volume impact in India and Middle East in 1Q22.

Revenue from Indian business declined by 28% YoY and 32% QoQ mainly due to DLT issue faced by enterprises and second wave of covid.

Company also had a reduction in banking traffic as there were allegations of data breach which was unfounded. 3rd party audit found no breaches and banking traffic is resuming to normalcy. However this impacted April 2021 banking revenues.

EBIDTA margin contracted by 10 bps YoY & 169 bps QoQ to 12.1%

Reported PAT grew by 27.5% YoY however declined by 3.1% QoQ

My Notes-

a. Phonon acquisition has been called off as the Phonon team stopped responding

b. The RCS business will see a good growth and already 310Mn+ messages have been sent trough RML platform

c. The RCS transaction charges will be slightly higher than the SMS for India which is 12paise per SMS. Whatsapp charges are approx 33 paise. The RCS charges will be in between the two. RML has not yet started charging for RCS messages and will start from Q2FY22

d. The new acquisitions Sarv Webs and Sendclean look interesting and they will add value to the overall ecosystem

e. India SMS business was down due to the allegation of data breach. Few financial enterprises asked for a third party audit and the transactions were stopped till the auditors gave a clean cheat

f. July transactions were back on track as per management

g. They have developed platform for developers and the same will be opened in Q2FY22. This is similar to Twilio

h. The RCS platform passed 10Million transactions per day which was huge feat as per industry analysts - Management quoted

Business model broadly comprises 2 parts:

o Self-serve model – smaller companies who will visit website and register using their card and avail services. (Smaller Ticket size ~ 200 dollars to 1000 dollars). People required would be remote account management, - 24 x 7 shifts, etc

o Larger enterprise setup like banks , etc - would need enterprise support

Target market predominantly India . 2nd market will be US (mainly self-serve mkt focus)

Technology & stack is ready – no investment needed in this

Investment mainly around human capital (100 employees – technology, product enhancement features, etc); and marketing & advertising expenses

Sendclean – more details

AI driven email communication platform (acquired from Sarv)

The kind of infra that they have built – has the potential to compete with giants of US

RCS & adoption of RCS

Have been able to onboard 10+ clients who are actively using the channel

Aggression with which India is adopting RCS is unprecedented

Did over 300 million transactions over RCS in this quarter.

Highest no of transactions sent in India. Was acknowledged by some of the stakeholders in RCS ecosystem

Saw one of the highest traffic days ~ 10 mn messages delivered in 1 day. Commendable feat compared to some global standards – as per mgmt.

Pricing for RCS

RCS – falls within operator ecosystem. Operator is losing revenue because of whatsapp. Operators likely to promote RCS as a communication channel.

Pricing for RCS will be more lucrative than whatsapp (33 paise) Preference for Whatsapp likely to diminish. All operators other than BSNL have deployed the platform

RML is not charging for RCS yet but should start Q2 onwards

Newer generation products have higher gross margin ~ 35 to 40%.

New product revenue

Drop in QoQ basis – seasonality aspect & we were grappling with 2nd wave.

YoY basis there is a good jump. Haven’t lost a single client

Quarterly run rate has been 10 cr

Continue to remain focused on new products. With whole lot of initiatives – Sendclean, other new products, RAPID, etc - intend to clock 10 mn dollar this year FY 22 (Rs 70 cr) in terms of new product revenue

RAPID 2021 initiative

Co is developer friendly. Developer API program. Things are getting better as all their APIs are thrown open to developers. Similar to Twilio.

1st phase of RAPID is a hackathon (planning to launch)- will open all APIs for people to test

Aspirationally - it will develop into a revenue line as we progress…

Points to track in coming qtrs:

a. Contribution from US & UK business – With senior hires in place, should look to scale up – there is a mention of an inorganic acquisition also here…

b. Virtual contact centre is a gap to be filled - & they should address this in the coming quarters

A link to another interview featuring the management -

AGM transcript has been uploaded on the exchange. Below are main takeaways

over INR 1420 crore , growth over 41% , EBITDA is about INR 175 crores, our PAT grew to almost INR 132.8 crore and our CFO/EBITDA was about 131%.

Processed over 32 billion transaction and added about 400 plus new customers.

We have 2000 plus active billable customers and our servers are located right now with seven global cloud data centres.

Journey- started in 2004, as a small time SMS aggregator to evolving from SMS aggregator to a large CPaas player, and then a large global CPaas player, and now moving towards the customer experience as a platform service. We support operator in terms of getting them full understanding about the revenue leakages

in last two years, we have deployed and we have spent lots of energy and money on our R & D. We can proudly say that we have our entire stack inbuilt inhouse on RCS, Whatsapp Viber and we acquired an email capability through the recent acquisition. Route Mobile has a complete stack. This stack actually explains how well we have placed an entire communication space.

Acquisitions- acquiring a company is a not a big deal but integrating the company within the ecosystem is something what Route mobile is good at and in future also, we are very much sure that if we acquire or if we grow ourselves in different geographies, we know how to drive, how to build and how to work with the founders and with this confidence, I think we are very much sure that whatever new acquisition we will have in future or whatever we have already. I think we have given the full freedom to our founders who are driving this business whether it is 365squared or Cellent or TeleDNA

SendClean: planning to invest about $12 million in next three years down the line and we are targeting about $30 million revenue coming from this business itself. we are on a growth path where we believe that email itself is a $17 billion market and it has a huge potential for Cpaas company like Route Mobile to offer the bundled solution to enterprise customer. So, we already have so many customers where we can go and start selling our email solution immediately, rather than going and cracking down or finding a customer for these services.

Comviva Partnership

SODLT- Scrubbing over Distributed ledger technology. Partnership with Comviva to jointly accelerate blockchain commerce for MNOs (mobile network operators) and enterprises globally. world is looking at curbing unsolicited spam fraud messages in a big way. Blockchain as a technology is an apt solution to mitigate such issues and ensure better governance. DLT adopted by mobile network operators in India is indeed a case study which can be adopted by the entire mobile network ecosystem globally. We have direct access to 260 plus mobile network operators, and we have the reach to almost 800 plus operators. We believe this partnership, along with our comprehensive firewall stack will ensure a secured and a seamless communication ecosystem globally.

Another aspect- international roaming and supply management within the telecoms vertical, we as a company are looking forward to work on these areas as well where after having a very long discussion with various operators globally, we identified some of the pain areas where operators are facing right now and I think we want to work with Comviva, especially in international roaming and supply management along with the DLT platform.

Want to become a $1 billion revenue 5 years, that is the vision we all are driving within the company. Every day, when I get up, I have this dream, which I know I can fulfil, I have achieved $200 million revenue in 17 years but I know I can achieve billion dollars in next five years. So whatever numbers we are talking about is definitely achievable. But it all depends on certain conditions and we are very focused in terms of 1) our technology enhancement, 2)on-boarding customer 3)scaling ourselves in various part of the world, 4) going global acquiring more companies. So, if you see the track record, if we continue in the same way, probably whatever we are dreaming of within five years, may happen before that also.

We are one of the top five tier one aggregator in the global market. Route Mobile is a global company. we are already featured in Gartner’s report or Juniper report, you refer any reports we were always there in CPaaS ecosystem

Growth triggers: Latin America is a market where we are very bullish about and there is certain technology enhancement, which we are doing and some of the technology adoption, which is right now happening in market like RCS, are probably our email solution, they will definitely add more revenue to Route mobile and in coming days, we see that the growth trajectory, what we have shown in past will continue.

Mobile based second line authenticators are becoming popular now. Google authenticators, SBI has come out with its own. No need for an intermediary between for example SBI and Airtel. I think this trend and the universal trend in eliminating intermediaries can be a problem This is my understanding pl correct if it is wrong

Don’t mean to pick on this post but this seems to be a recurring theme. This is unfortunately a limited understanding of CPaas which has many use cases. For e.g.

Notifications and alerts

Password updates

Appointment reminders and confirmation

2-factor authentication (2FA)

Status updates, such as package delivery

Real-time customer support

Anonymous communication or number masking, connecting parties while ensuring privacy (e.g., Uber, Airbnb)

Building internal capabilities to cater to all kinds of communication needs is simply too complex, involving multiple MNOs & beyond the core expertise of most enterprises. On the other hand CPaas providers offer all these functionalities at a fraction of a cost.

Moreover as various verticals within an organization realize the value of CPass they will increasingly adopt this service.

Quoting an older Gartner report which is no longer publicly available.

“Gartner often sees a business unit adopting CPaaS for a particular use case. Then other business units build their own use cases as they become aware of the CPaas value proposition”

Limiting our view only to 2 Factor authentication is a bit myopic, that is my limited point.

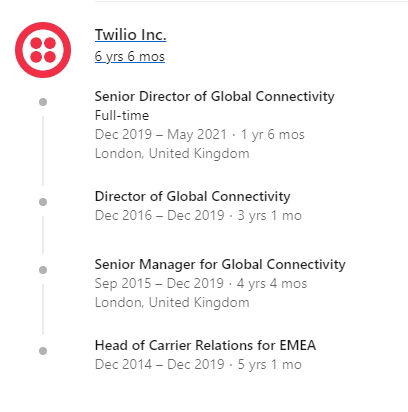

They’ve just onboarded Carl Powell as VP of Global Partnership and Alliances for Europe.

https://www.linkedin.com/in/carl-powell-7b882623/

He appears to be an industry veteran and most interesting is his stint at Twilio.

Pleasantly surprised to witness RMs ability to attract such talent, John Owen & now Carl.

P/S multiple paid was just under 5 (about 40% cheaper than RMs own valuation as on date).

Would add about 86 Crores to topline & 12 Crores to PAT both standalone (consolidated numbers aren’t published). Margin profile seems better than RM going by the numbers.