Receivables difference is mainly due to masivian and mr messaging… which the company acquired recently

1 Like

Revenue growth is a given, courtesy the tailwinds.

Margin is the KPI.

Every percentage point improvement in margin can have a disproportionate impact on Market Cap.

Can they deliver? Competition will keep chipping away at the margins.

1 Like

A big anti thesis point to CPaaS companies if following is considered and rolls out.

7 Likes

Management is going to consider buyback. Shows good intentions towards shareholders. Will be interesting to see the buyback price.

07747430-400e-4e84-a8af-69497bdc7081.pdf (317.8 KB)

1 Like

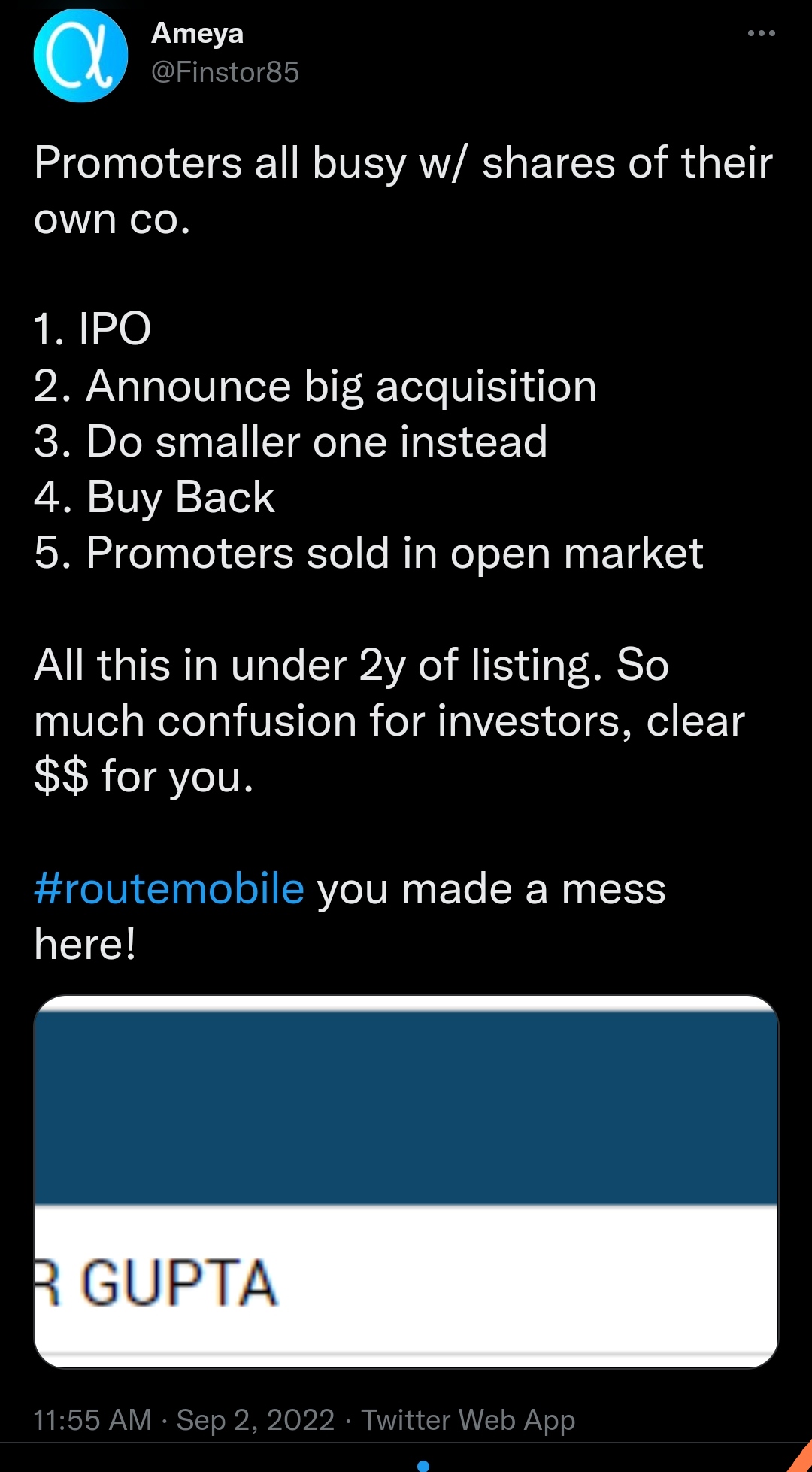

A tad confused with the buyback proposal. Obviously the market didn’t like buyback from open market at/below Rs.1700. But they did a QIP few months ago worth ~870Cr and am assuming they are using a part of that raised money to buyback from open market. A bit hard to deduce the management strategy with these moves.

4 Likes

Looks good on the face of it. Although would be waiting to know management explanation of capital allocation post QIP

5 Likes

Can anyone share the audio recording of the Q1FY23 concall ? Not able to locate the file from the exchange filing nor able to find any recordings on youtube also

There you go.

4 Likes

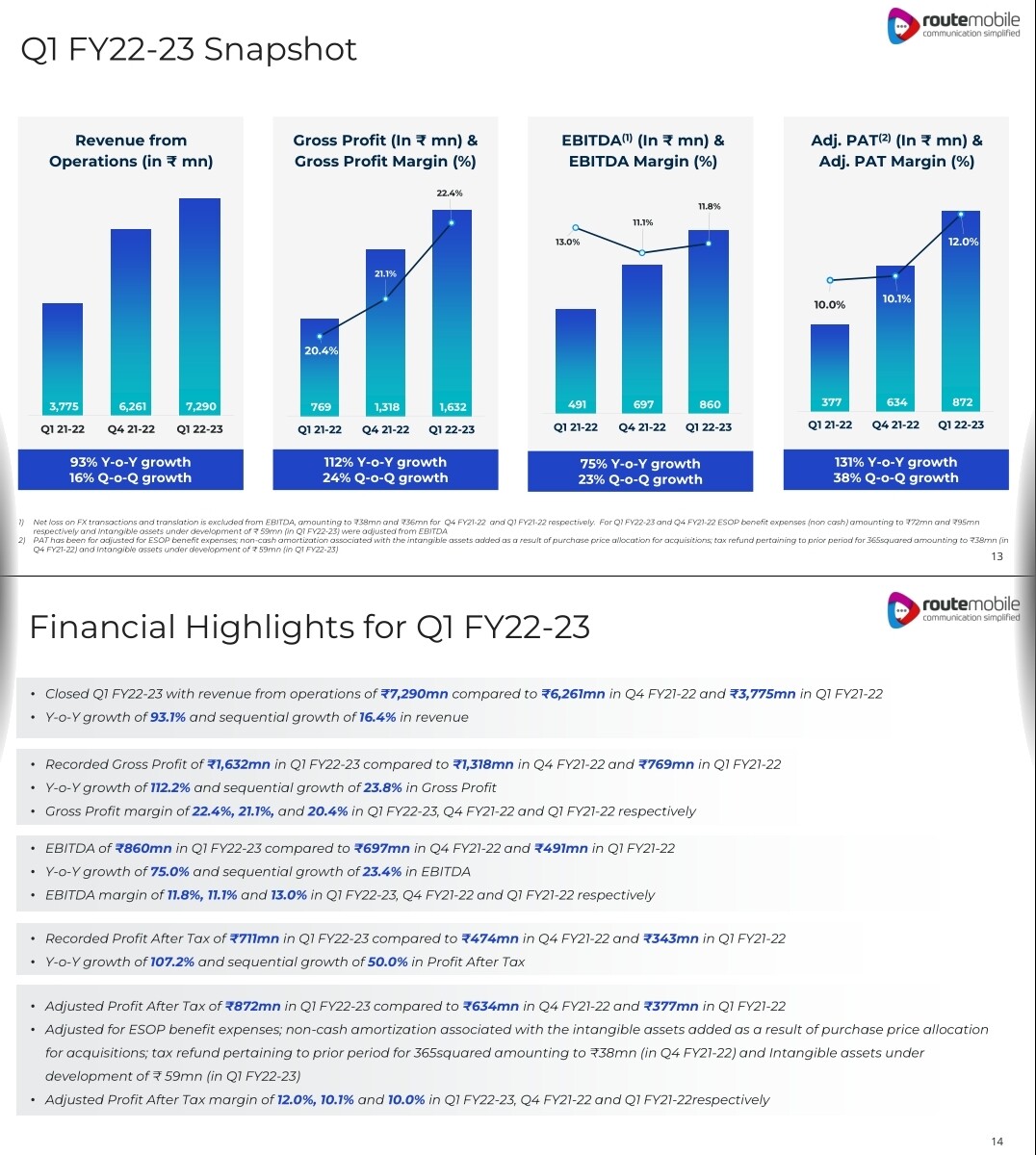

Q1FY23 Concall Highlights

Reiterate 40% growth for this FY23

Telecom companies getting into CPaaS business not very viable for them.

Looking at 100-150bps expansion on Ebitda and guiding 11.5-12%.

We are L2 vendors for a Bank account and we get 30% of traffic of that overall bank’s volume. We are already working with them for last 3 years for promotion traffic.

Route Mobile’s India overall GP 23%

Margin expansion because of increasing ILD(International Long distance) prices. Also because of MR.Messaging and Masivian which as high margin business.The domestic enterprise business in India is a high margin business and its doing well for us to aid margins.

We aspire to take the overall gross margins to 30% from current levels of 22%

Revenue of platforms - call2connect 8.34cr, 365squared 1.5million euro , mr msging 160 mil , masivian 470 mil

RCS getting good traction from corporates in the new channel business.

Onboarding of clients for whatsapp based msging is having good demand inspite of rate increase by whatsapp.Whatsapp is 55p/msg where as sms is 10p/msg

OTT clients tried to convert from ILD to NLD (National long distance) cheaper rates with govt , but they are not able to meet their regulatory requirements

sms based authentication is widely adapted and have not been disrupted by other communication networks which have been existing all these years.

Effective tax rate for the co is 15-18% as we work in different geographies

Focusing on USaaS through voice solutions & mobile identity in BFSI sector.We are working on M&A in these two spaces.

We have an agreement with Meta and only a few companies in India have this agreement. Global CpaaS players have big advantages over domestic players as we serve the

same client in 30-40 countries.We also offer different platforms of communication under a single roof.

We are doing platform integration for next 1-1.5 years , we identified excess cash inspite of the anticipated M&A so we went on with buyback & Dividend plans.

Masivian is an enterprises play. 55-60% marketshare in Columbia , 2nd marketshare in Peru.It offers range of channels like sms, voice , email & In-app notifications.

3 Likes

Raise money, again raise money even after having good cash on balance sheet, do buyback just after QIP, sell near 1% stake just after buyback!

Its high time the management should clarify all the capital allocation/ equity decision they have taken since ipo in detailed manner!

Its a MAJOR RED flag according to me!

They were proudly saying during ipo that they have never raised money and all growth was organic and through internal accruals but as the IPO gets into the market this happens:

8 Likes

Latest report from Gartner:-

1 Like

I recently read through concalls of Route, Tanla and below are few notes on the business landscape:

- Both operate on very similar businesses in CPaaS . The domestic industry might grow around 20-35% for the next 5 years.

- Route wants to expand it offering globally whereas Tanla wants to maximize on the domestic opportunity.

- They provide APIs to clients that facilitate them to provide communication services like SMS, Whatsapp Business, Video Call Support integration etc. Bulk of the revenue still comes from SMS, voice.

- They do so by being an interface between client apps and operators(mainly telecom companies but also companies like Meta etc)

- Twilio has a global lion’s share however it’s not much penetrated with domestic Indian clients as its plans are expensive.

- The competitive scope is very intense(more so globally) which can lead to both companies having margin pressure.

- Recently telecom companies have started poaching clients from these CPaaS companies by directly offering them their new CPaaS products. For Example, Airtel IQ has already launched and Jio will also come up with a similar offering. For a client this saves them money by directly integrating with telecom operators rather than Route/Tanla as the middle layer. However, the integration and customer support etc might be handled much better by Route/Tanla as it’s their niche focus area.

- Significant expense still goes to telecom operators. Margins can get impacted if there’s cost pressure from operators.

- Both companies still generate a significant revenue from SMS business however that might be at risk if RBI gives permission for push notifications etc to app providers. However cost of SMS is still very cheap in India and push notifications can’t replace OTPs etc in the near future as it is more secure way of authenticating.

15 Likes

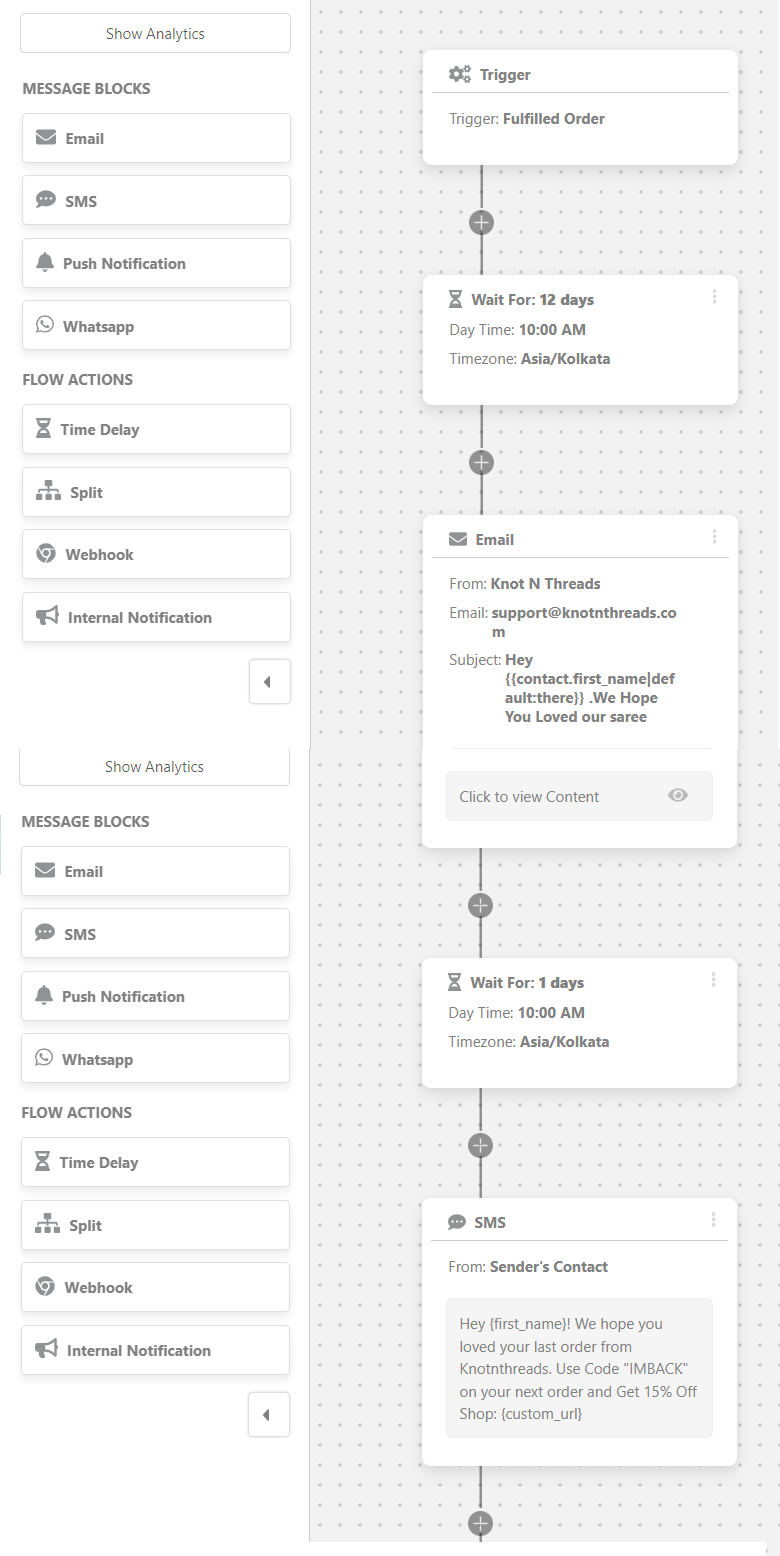

I do run ecommerce store, where recently Whatsapp manager has been introduced for retargetting by meta. Whatsapp manager is very powerful platform for retargeting waiting to expoled. Route mobile are in well suited position to capitalize this Trend. Retargetting can be done using SMS, mail & whatsapp api

1 Like

Hi, for the benefit of those of us not familiar with the terminology, could you please expand on what retargetting means? And how the whatsapp manager helps in that?

Thanks in advance ![]()

1 Like

Meta has recently allowed advertiser to message customer in whatsapp . You can easily automate flows like order status, order deliver , shippment tracking, returns using automated bot developed by company like route.

You can order using whatsapp and even payment can be done using whatsapp without going to website.

After order delivered, ecommerce website retarget thier customer with mail previously.

But now a day, ecommerce store retarget thier previous customer using mail, sms , push and whatsapp .

These flows can be set in platforms like route and tanla.

Its very powerful tool for Re-targeting customer where whatsapp open rate is more than 90% .

All tools combined like sms, mail, push and whatsapp

So whatsapp api is at early stage.

disc: watching closely, invested very little

4 Likes

Excellent details. Do you think Whatsapp management will be done through Route API more than directly on Meta’s portal?

You are right whatsapp flow can be done in route platform, combined with sms and email.

Route vs Tanla: -