Some idea about whats in store for FY 21

Plans to limit companies to 4 in each sector could mean that RITES might be forced to use its cash to buy stake on other railway related companies. I fear that they might loose their ability to choose asset light projects. Any thoughts on this please?

RITES is consulting company and might continue to be so. RVNL and IRCON are EPC cos.

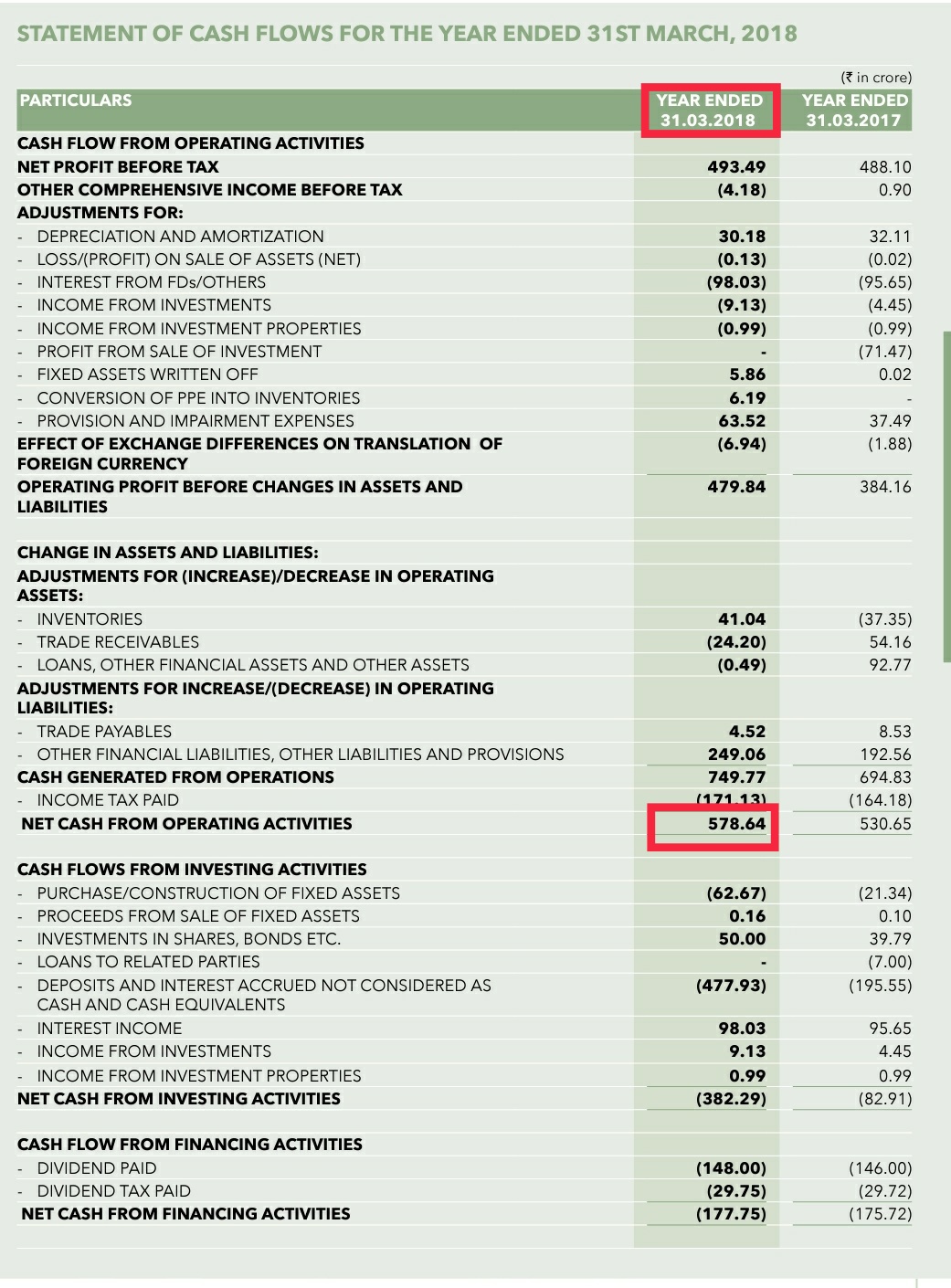

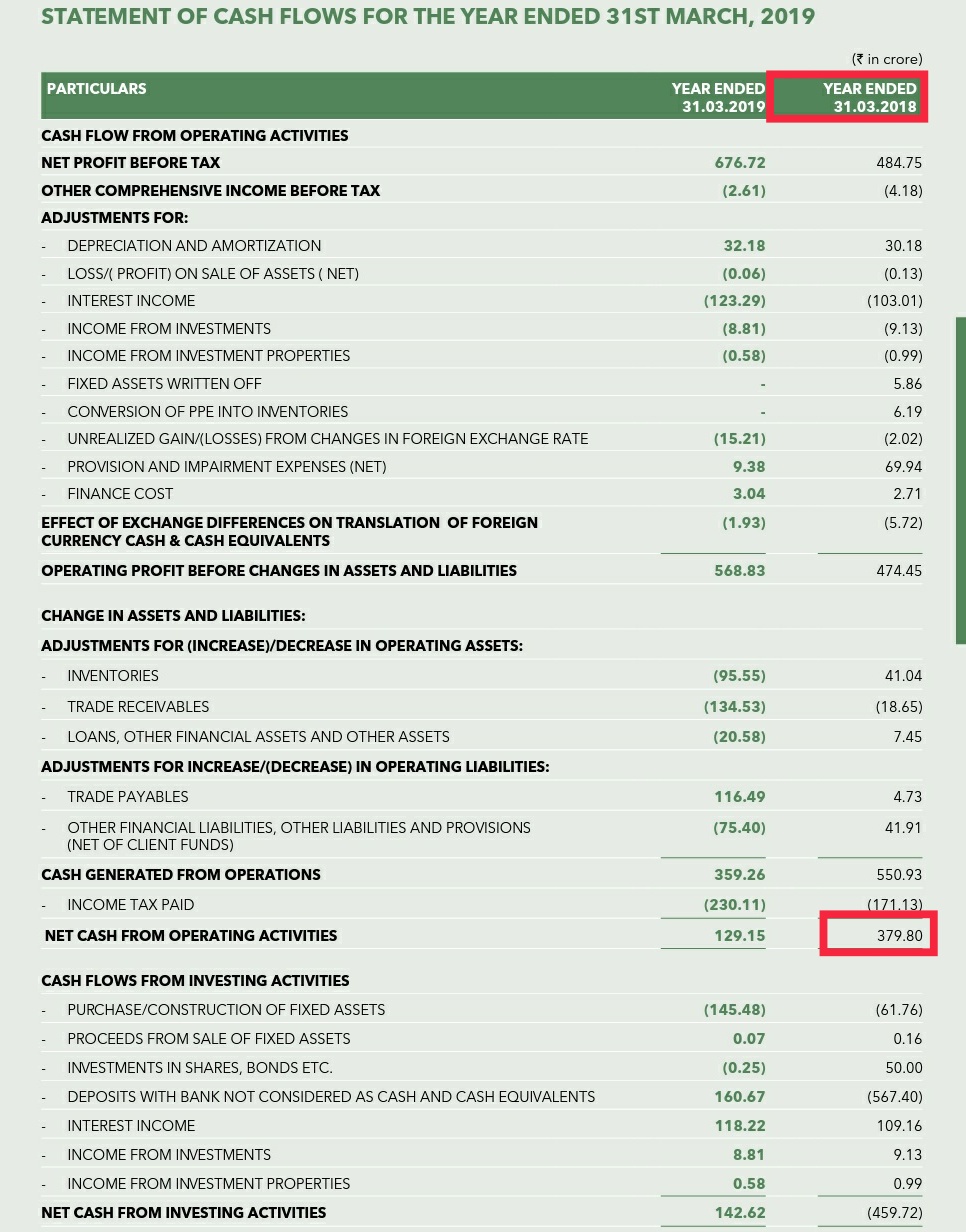

Hi, can some one explain me why op cash flow for same year different in two annual reports ? And why did other current financial liabilities came under operating liabilities in CF statement ? Thank you.

Q4 and FY 20 Investor Call Transcript

Business

- Consultancy

- revenue of Rs. 1066 crore. This is in comparison to Rs. 1092 crore in 2018-2019

- consultancy suffered in FY2020. we remained almost flat or had 2% fall on annual basis

- Major Numbers

- railway sectors - Rs.609 crore

- Airport - Rs.47 crore

- highways - Rs.67 crore

- metros and urban transport put together is around Rs.134 crore

- Quality assurance - Rs.360 crore

- The order book of consultancy has gone up despite delivering about Rs.1100 crore of turnover in consultancy, our order book in consultancy is at almost Rs.2400 crore, which is higher than the opening

- All other businesses (Leasing, REMCL, IRSDC) have emerged because we are predominantly a consulting company. We are a consultant and that is why, we could spot export opportunities, we could spot leasing, we could develop the open access model through REMCL for railways. we are able to do the solar or the renewable portion required to be met by railways

- National Infrastructure Pipeline of Rs.110 lakh crore

- RITES as the consultant gets into the formation stage or pre-formation state or we call it pre-feasibility, for mega projects. Once a project goes to DPR stage, normally we get associated with several of these projects and then once these projects go for detailed engineering, at that stage, again we get a chance to do this, and third stage is when the construction starts, then we do project supervision. It is not necessary that we get into all the three stages in all the projects, we may get one in some, may get second also in some, may be all the three in some

- NIP is a very strong guide, and we may soon see projects emerging out of it. I think, RITES will be one of the biggest beneficiaries of this because we are into railways, metros, highways, ports, airports and not only in India but also outside India.

- Leasing

- 38% to 40% as sustainable margins

- Exports

- still hold on to - Rs.550 crore to Rs.600 crore kind of top line in FY2021

- Mozambique

- signed this contract only in June 2020. May be in Q4FY21, we will target some income from this new order also

- REMCL

- Government of India has mandated our subsidiary company REMCL for installation of 3000 megawatts of solar energy generating systems

- This 3 giga watt transaction is in three components

- Tranche 1: developer model

- this scheme is of 1 giga watt

- developer has to put equity and our job is to see that all are done as per technical specifications and then we get around 5-7 paisa per unit throughout the life of the project

- no equity is involved from REMCL

- Tranche-2: PSU investment model

- this scheme is of again 1 giga watt

- this company (REMCL) is owned by RITES and Railways and can avail MNRE subsidy available under CPSE Scheme. this should be counted as own generation or own consumption

- would be following the CERC guidelines of investments, the return on investment is good and the buyer is railways, so there are no risks of revenue realization

- it is necessary to put some equity. Out of this 1000 megawatts, we have so far identified land only for 400 megawatt and for this 400 megawatt, a tender has already been issued on June 15, 2020

- This might actually spillover to 2022 onwards because 400 megawatts, we have just tendered out

- It is estimated that for the total investment, equity of about Rs.350-360 crore will be required, half of which i.e. 51% would be done by RITES and balance by Ministry of Railways

- we are in the process of ascertaining the rates first, at what rate, on railways land this project would be doable and tie up for finances. Once the financial closer is nearing, if the rates are found acceptable, then only we will go for investment approval and this may need about Rs.180 crore to Rs.200 crore as equity

- equity stake for RITES to invest in REMCL could be in the range of Rs.180 crore to Rs.200 crore spread over two years FY2021-FY2022

- Tranche 3

- this is another 1000 megawatts, and on land parallel to the railway tracks

- this will again be on developer mode and railways will buy the power. Our role is to supervise and again see the technical issues and supplies throughout the life of the project and we get paid around 5-7 paise per unit

- This scheme is very big and this is the first step. Let me tell you the potential is still more and once we successfully do this, more such land parcels which are in the process of being identified, would be opened up by railways

- For all Tranches

- Revenue Potential

- around of Rs.20 crore for fee component

- If 5 paise to 7 paise per unit of fee would be agreed, then this would give at least Rs.20 crore per year

- ROE: first 20 years that is 16.45% and after that 17.87%

- Revenue Potential

- Tranche 1: developer model

- It is informed to railways that the land which is being provided for tranche one, can actually take 1600 megawatts. Therefore, we have already written to them that the first tranche can be increased to 1600 MW and reduce the capex model to 400 MW

- IRSDC

- IRSDC is a beginning, there is a lot to happen in the segment and we as an engineering consultant hope to make significant revenue from there also. Every station would be a huge investment, a major station may need Rs.100 crore to Rs.400 crore

- it is an equity participation, we do hope to get some technical work because we have a strong team, which has been trained in structural designs and construction supervision and that was one of the objectives

Order Book

- order book for consultancy as on March 31, 2020 stands at Rs.2464 against opening of balance Rs.2317

- in exports Rs.1086 opening was there, we have ended year with Rs.1436

- the order book of turnkey has gone down by almost Rs.500 crore because many of the orders are on the verge of being executed in 2021 or already done in 2020

- execution cycle for our order book - around two years

- Bidding Pipeline

- We are working for Metros, major DPRs, bridges, ROBs, flyovers, highway tunnels, a major order in the Ladakh for three tunnels, road projects etc

- in metro alone, about Rs.1500 crore worth of bids we have submitted and we must get at least a reasonable share there

- We have worked very hard to get a project of highway in Bangladesh. We have been declared eligible for one more rail consultancy project in Bangladesh

Financials

- Dividends (Response to questions by @Uzair_Fahmi)

- We are offering Rs.16 per share total, Rs.6 is the final dividend and Rs.10 already paid

- we are still retaining about one-third of the current years’ profit, which we will be using for investments like the solar investments or the station development

- To summarize the position on dividend, we have best two years, the best two years have seen best two payouts We have cash, we have opportunities and we will make sure that we keep evaluating the possibilities continuously.

- Payment Cycle

- We rather get, about 20% money upfront as the project advance and then we spend out of it, so the possibility of being out of cash for these projects is actually not there

- Capex

- available cash of around Rs.1102 crore, out of which we are keeping 400 crore for working capital

- rest is now planned for investments

- Equity participation in REMCL, IRSDC and SRBWIPL - Rs.200 crore

- capex for building including workshops for locomotives - Rs.150 crore

- capex for locomotives - Rs.80 crore

- Dividends - Rs.150 crore

- survey equipment, software, computers etc - Rs.40 crore

- miscellaneous around Rs.40 crore

10 Likes

hey thanks for mentioning. I didn’t know that they published it

2 Likes

Kindly forgive me for posting this - as i don’t follow this thread it may be a little contribution to the members

Summary

Impacted from disruption, RITES Ltd (RITE) Q1FY21 revenue declined by 38% YoY and PAT at Rs0.7bn was down 36% YoY. However, it expects execution to improve from 2H and for FY21E guidance is to deliver single digit revenue growth. Company has reduced headcount by ~10% and aims to maintain margins by cost management. In Q1FY21 Order Book at Rs 61.5bn (3x TTM revenue) has seen new orders of Rs 2.7bn. We maintain estimate and on unchanged TP of Rs300, retain BUY rating. Stock is trading at 10x FY22 EPS (which is avg. valuation since its IPO) and we value the stock at 12x FY22E EPS. Our positive outlook is supported by experience of the management, capital allocation policy leading to 20%+ ROE, order book (equals to 3 years TTM) and dividend yield of 5%.

Key Highlights and Investment Rationale

-

Covid disruption in Q1: RITE revenue at Rs3.3bn (down 38% YoY) was impacted by negligible delivery in the export segment. Its key segment, consultancy revenue declined by 22% YoY. Leasing and Turnkey revenue was lower by 20% and 11% respectively. However, business is improving every month and in Q2FY21 RITE is working with 75-80% of its usual run rate.

-

Order book at Rs61.5bn: In Q1FY21 Order Book stood at Rs 61.5bn and RITE has secured Rs2.5bn in Q1FY21. Company expects to secure order of Rs5-10bn in bidding. In exports, RITE sees immense opportunity in Africa for rail infra.

-

Upside risk to our estimate: In FY21E, we have model revenue to decline by 5% and versus management guidance of revenue growth, there exist an upside risk to our estimate of 10-15%.

RITE_RR_14082020_Retail-14-August-2020-1951148894.pdf (572.7 KB)

1 Like

Board to meet on 18th September to consider share buyback…

What could be the size of buyback? My guess is around 300 Crs.

Disclosure: Invested

Buyback makes sense with cash on books. The important question - What would be the buyback price.

Disclosure: Invested.

1 Like

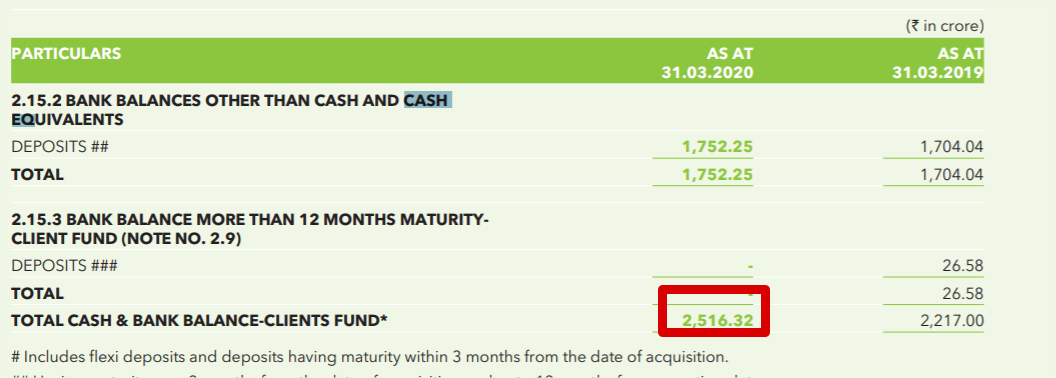

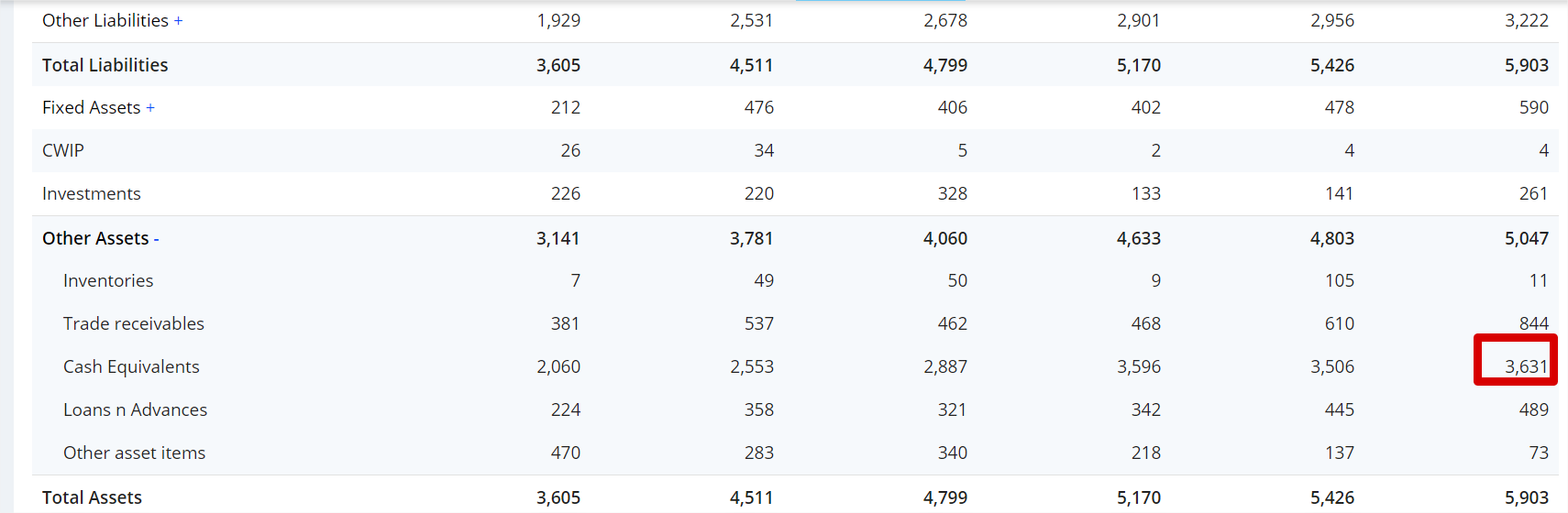

Hi, Does anybody know how much company has cash and cash equivalent? I am seeing below in the annual report. But screener shows 3631 cr. So I got confused.

RITES has approved buyback:

4 Likes

Sensible decision. I’m not too keen on looking at its price movement for now for in my analytical belief I think it’s a solid company that’s asset light, diversified ( in its sector) and a monopoly. No debt and majority of current liabilities are actually advances from clients so again no reason to doubt fundamentals.

4 Likes

Rites buyback offer is 1 share for every 7 shares you hold and closes on 10th november

1 Like

Hi All,

Did anyone else received the buyback settlement confirmation today? Almost 90% acceptance for retail happened as per the msg received by me.

Received confirmation from co. as well today. 90% acceptance ratio against the initial expected 15%.

For future references only, just trying to dig in as to why the AR went so high - was it only because many retail investors didn’t tendered?

Dividend declared 5 Rs per share. Great dividend yield, bonus shares, buy backs and growth potential. Other than high debtor days does it have any more negatives? Maybe being a PSU is a drawback but I also consider it a strength because they can benefit a lot from India’s growing bilateral relations with other emerging markets.

I know I’m not supposed to get attached but I like this company a bit too much

Disc: invested

3 Likes

RITES.pdf (1.1 MB)

3 Likes

Will the budget allocation to railways / metro ,expansion / upgradation etc, be positive for Rites ltd ?

Edit: Added Q3 FY21 conference call notes

Rough notes from management commentary:

- Railway investment very positive for RITES

- Export orders are getting ready. Could not do it in Q3, but will happen in Q4. The first shipment to Sri Lanka is planned for 25th Feb. Mozambique order also getting ready.

- Consultancy and quality assurance work was hit (land acquisition issues, steel prices running away), this is a temporary phenomenon, but things are getting better day by day. Power management business returning to normalcy.

- Still seeing disruption in the supply chain. There will be a lag between production-ready to shipment. Q1 next year should be better.

Q3 Conference call:

Takeaways:

- Impact on consultancy was because of PMC and QA - manpower issues and supply chain disruptions. Despite a good order book, we could not execute, clients delayed QA work. Expect Double digits growth as compared to FY20 NOT FY21 (FY21 was a wasted year)

- Around 1200MW (65% of IR load) goes through RITES, with more electrification happening and entire broad guage n/w to be electrified, the overall requirements of Indian Railways will be 4000MW, which mean their power procurement from us can get doubled. This year we saw 1/3rd or 1/4th demand because IR was not fully functioning. This energy income was impacted, but as IR gets back we will see this income come back. Business model remains intact. We get 0.05 paise and with load being at 4000 MW we should see this go up (Inferring a 65% of IR load this would translate to 10 to 13 crores of revenue).

- Did not get a DFC order, we didn’t want to cut corners and compromise on margins for the sake of price. This order went to the private sector.

- Regarding the Mozambique export order, for the first time Cape Guage (South African standard) order is going out of India, this shipment is important and can bring new customers.

- There is one 240 coach broad gauge tender that we are discussing. Can’t name the country, this can have a lot of potential.

- On Capex

a) This year we have not done much capex. Started work on an office building in Kolkata. Have acquired property on Bareilly. Looking to optimize our capex. The total earmarked amount of 200 Crs may not be utilized in 2021-22.

b) REMCL - We had thought of investing up to 200 Crs, those tenders are not yet decided, we can say this will not happen in FY21 but most likely happen in FY22.

9 Likes

Rites has cash equivalent of Rs 3200 Cr, which is really high for company with barely 6000 Cr Market Cap. Rites along with Consultancy services offers turnkey project as per my understanding in turnkey project client has to pay in advance for its implementation.

- Can someone with more knowledge on it elaborate more on how much percentage of 3200 Cr is advances for turnkey project and how much is actual reserves company has which it can reinvest or distribute as dividends.

Disc: Invested

5 Likes