Please go through the thread. These questions have been answered in the thread earlier.

5 Likes

RITES depends heavily on Govt spending. Given the immense pressure to provide economic stimulus and DT to vulnerable citizens, is it expected that there would lesser share for infra spending? RITES has strong balance sheet to whether the storm but can the order book shrink going further?

IMHO, On the contrary, after the corona incident is over there will be massive govt driven infra development to start the economic cycle and generate employment. Fiscal slippage will not be factor for this and next FY

3 Likes

Thats an interesting thought. Thanks.

1 Like

PSU like RITES, Bharat Dynamic, BEL and many more have good order book. However, main question is execution of the order and timely receiving money from the Govt. The order execution is getting prolonged as govt not releasing money timely and this become headache for such PSU as their money stuck in working capital!

1 Like

Company has good cash on hand. (~60% of market cap). What this means is, if current price is Rs. 225, buying price is already at 60% discount, so basically effective price is just Rs 90.

Though there is no denying that few upcoming quarters will be hard, but current price is providing good margin of safety.

2 Likes

We can never say where’s the bottom. Unless Ministry of Railways says the are cutting the railway budget or culling projects - Rites should be buy on dips candidate.

RITES Subsidiary mandated for management of 3 GW solar plants installation on Railway Land Link

“Besides Bid management fee in the beginning, REMCL would earn long term revenue through supply management from these installations which may amount to approximately Rs. 20 crore per year to REMCL during life of the project. Entire installation is expected to be completed by 2022-23” - Adds to the visibility in future earnings and successful completion might bring in similar projects in future

2 Likes

The situation is such that most PSUs are trailing at single digit PEs and some of them are even sitting on cash like NMDC and Cochin Shipyard with good cash flows and low-debt. The problem with some (including RITES) is that their paymen comes from the Government. And Government collections through GST will be low for the coming quarters. I would like to know if there are PSUs offering good value that are not dependent on payment from the Government?

1 Like

Hi,

I am new to valuepickr community,kindly guide via dm about relevant etiquette

1)I was trying to understand how is IRCON different from rites,Since both companies are listed which one could be a better investment and why?

2)Who are the major competitors to rites?What is rites usp apart from being a PSU?

3)What are reasonable estimates on the percentage of infrastructure consultation boom upside that rites would be able to capture?

4)What government interventions are likely to negatively affect rites that can be reasonably inferred based on present infromation?

5)Since it is a PSU,the management can be unpredictably replaced.How much would rites be affected by an incompetent new management in terms of both capital preservation and growth?

Please go through the thread from the beginning. All your questions have been answered.

Also, the ethos of VP is for people to bring something to the table first. It is not a question and answer forum where one gets to ask questions and get answers. Please put in what are your insights on each of the question put up above.

13 Likes

Hi Guys,

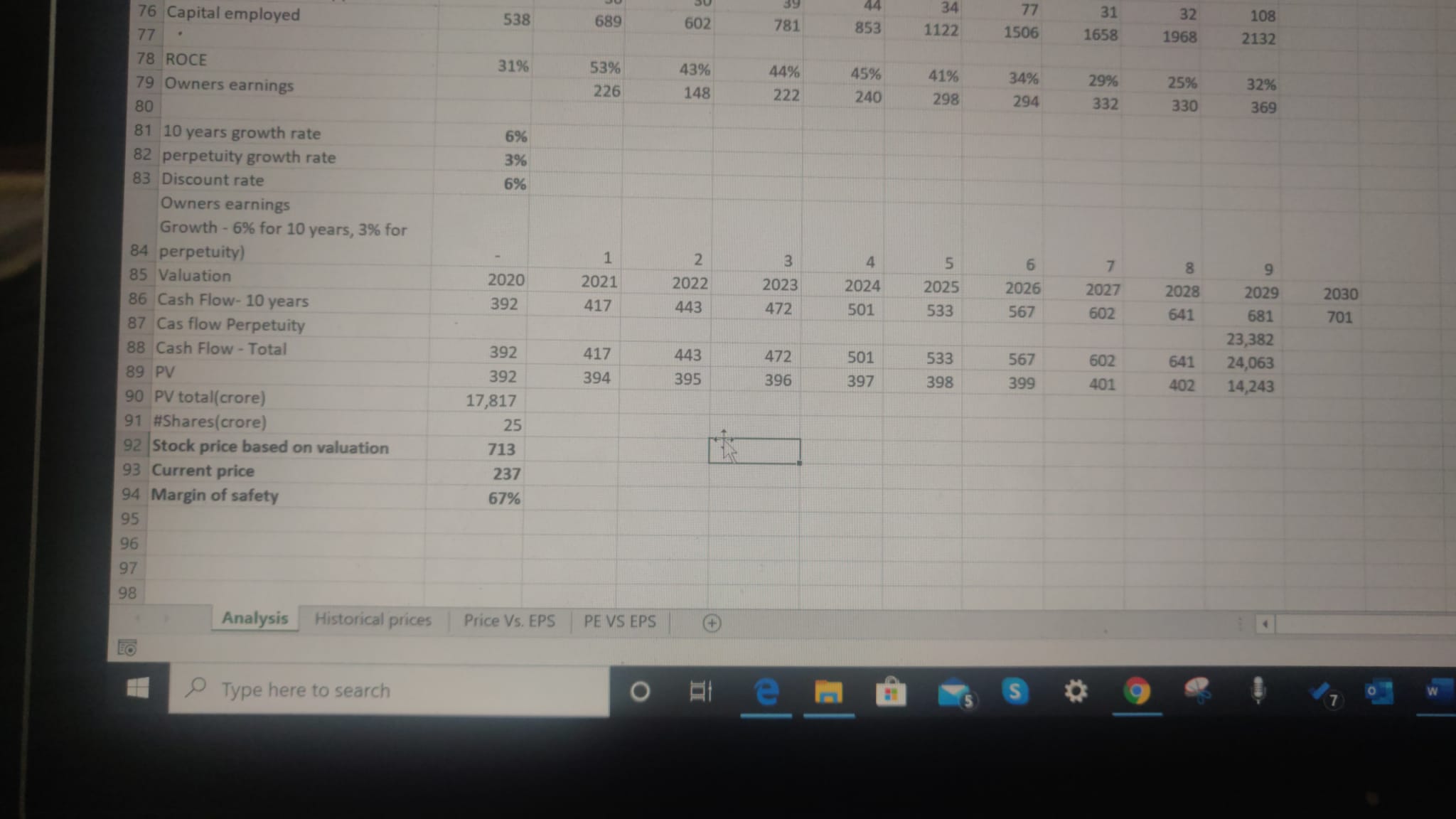

I used the dividend discount model taking insoiration from the book “Warrent Buffet way”. The data is taken from Rites annual report 2018-19.

Key findings

ROCE - has grown at strong 30-40% annualy

ROE - again a strong 20%

Owners earnings - (Profit after tax + depreciation/amortization - Capital expenditure ) - Has grown at a strong 6.3% for the past decade

Cumulative PAT(2010-19) - 2782 crore

Cum. dividend paid - 856 crore

Cum reinvested - 1926 crore

However, it’s surprising that for 1 rupee reinvested the net worth grew only 0.88. Any comments will be appreciated here

Over to the dividend discount model with margin of safety concept

Assumptions -

- 10 year owners earnings growth - 6% (replicatiing the past decade and strong railway capex)

- perpetuity growth rate - 3%

- Discount rate - 10 year govt. bond yield. I have followed Buffett’s thinking of not adding Market risk premium as daily price volatility is not a good indicator of risk. Instead I will use the Margin of safety to make the decision

Based on the parameters, I get a fair value of the company at 17.8k crore of 713/share. which is significantly above the current trading price.

As we are all learning, please do feel free to brainstorm on it so we can identify is its an uncut gem or not.

Disclosure- Invested

Cheers,

Uzi

5 Likes

quick update on the above…I realized that the numbers were on standalone basis and when I used the consolidated number, I got a fair value of around 900 per share. happy to share my file with anyone who wants a further review.

1 Like

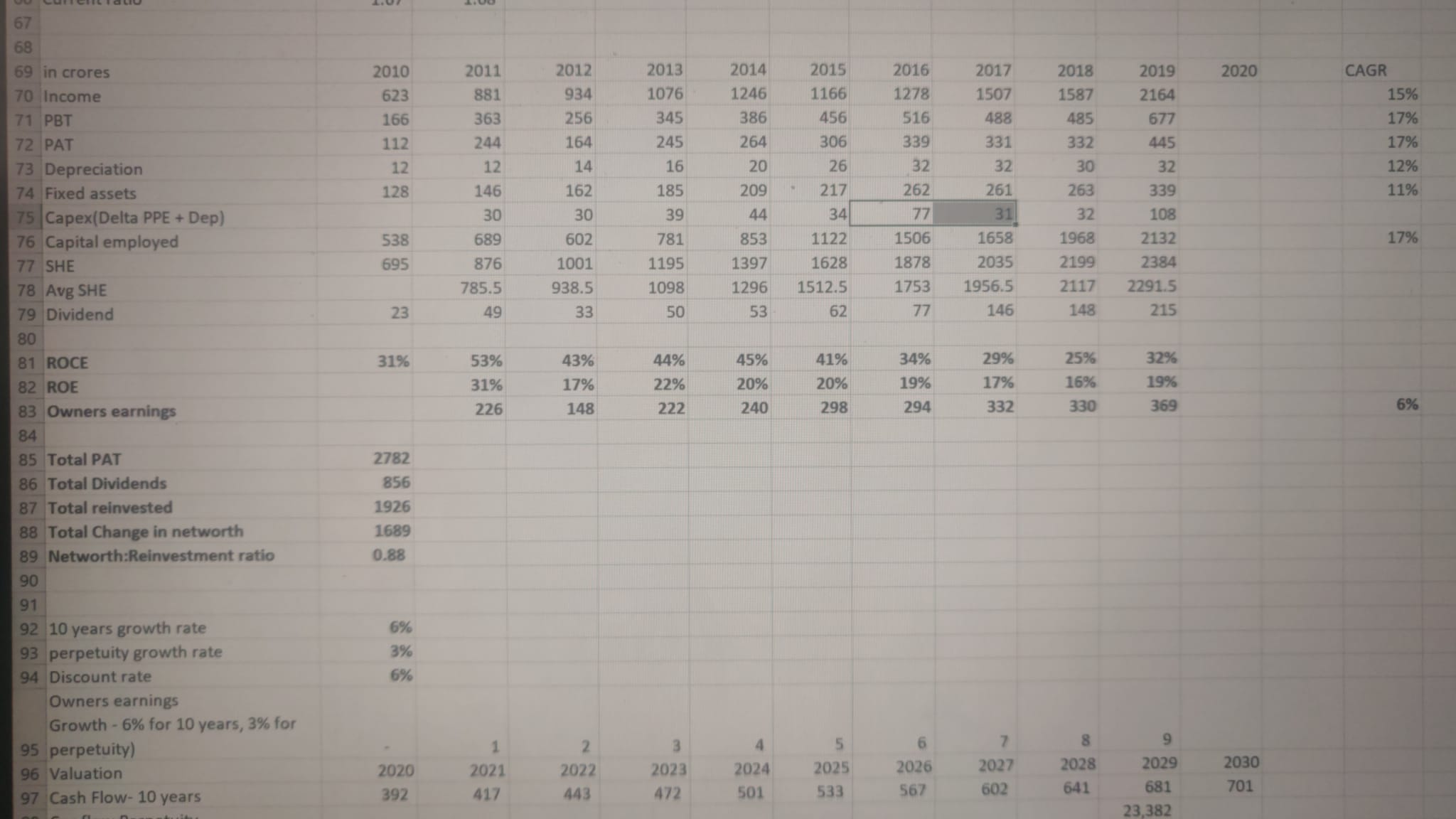

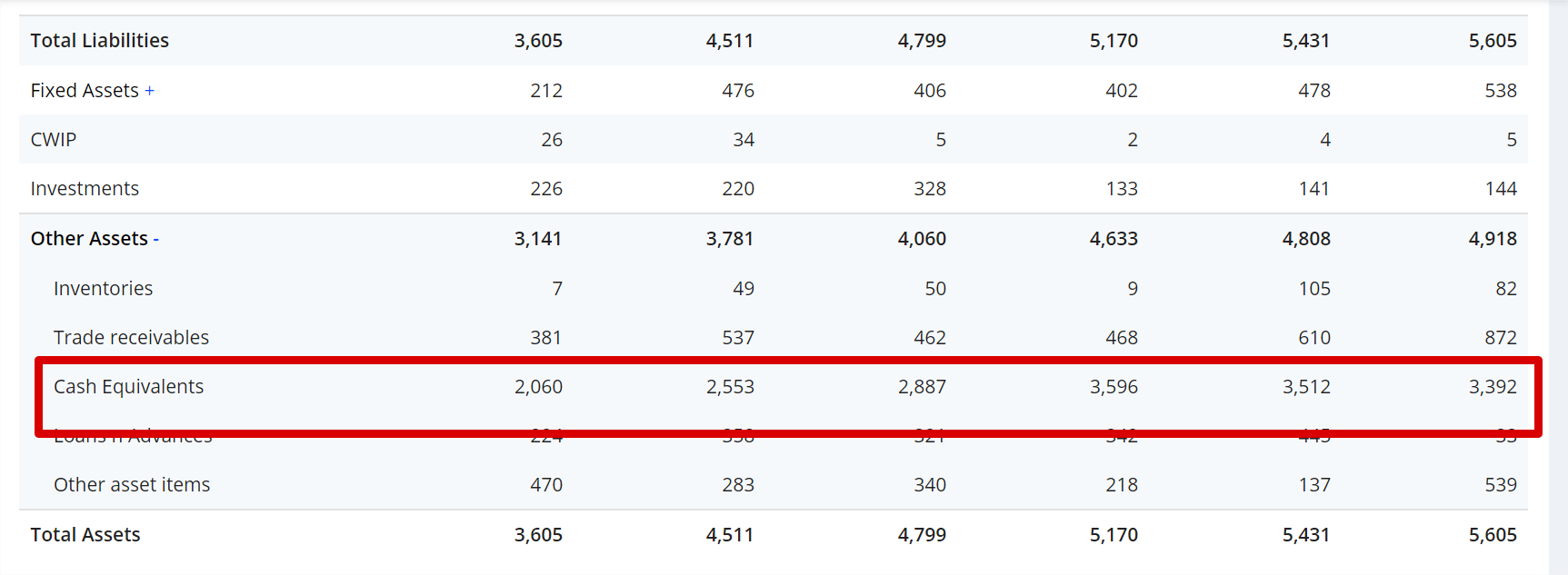

I was looking at cash and cash equivalent on screener which is 3392 cr. Market cap of the company is 6000+ crore with PE of 9. Company has no debt with good ROE and ROCE. If we consider cash equivalent, it means company is available at less than 3000 cr with PE of 4. It is available at huge discount. Am I missing something here?

3 Likes

There are two types of Cash components for this business.

Cash-Owned Fund

Cash-Clients Fund - which will be eventually returned - I understand.

Best to read the BalSheet for calculating equivalent cash. Screener would sweep everything under one entity, as it may not have a provision to separately list.

Cash- client funds are the balance the client has paid for the project. When rites finishes the project the same amount is debited to revenue account.

Rites works on advance payment since a lot of projects are turnkey which is cost plus basis.

A simple way to also identify the current undervaluation is

Cash per share : 3500/25 = 140

Dividend per share : 330/25= 13

Total cash per share : 153

CMP : 240

Effective price paid per share : 90

This holds true since company doesn’t have long term borrowing which would invalidate this method. However since long term borrowing is negligible, I’m quite confident on mispricing.

Finally running the analysis that I did, it seems that company in the past 1-2 years has increased the dividend paid compared to long term average and lowered the % reinvested. I would think that the management thinks it cannot reinvest the money above cost of capital and therefore taking the decision to give back to shareholders the excess cash. This needs a management guidance and I intend to ask them in the investor call today if I get the chance

2 Likes

Hi Uzi, could you share the excel sheet ? Sending you my email ID on personal chat.

Thanks!

Rites_valuepickr.xlsx (14.3 KB)

Hi folks,

Since few of you reached out, I’m attaching my calculation sheet here. One thing to note is that I have not subtracted working capital or added non cash charges(beyond depreciation & amortization). But since this is for 7-8 year period I feel owners earnings could be reflected through pat, deprecation, and capex combo. You can plug in 2020 numbers and evaluate the new intrinsic value.

Please leave your feedback and lets take this forward!

Cheers

Uzi

2 Likes

I think the govt is milking all its the cash rich businesses by forcing the companies to increase dividends. To help with the govt revenues. So the increased dividends may not say anything about the business prospects. Just greedy owner.

4 Likes