I have only recently started reading balance sheets so I might be wrong but I think all the advances are generally part of liability side and should not affect cash equivalents.

Despite very good fundamentals, RITES is a nomination business - – RITES gets orders because of a preferential treatment from the Indian Railways. 2/3rd of the projects won by RITES are where it’s the sole bidder, while the remaining 1/3rd are the ones where it competes with other Railway PSUs or is a part of a consortium with other consultants (again for quasi government projects). I have been trying to figure since quite some time on how would RITES hold its forte in a laissez faire economy. While it can be argued that RITES works only in govt infra projects, the latest order it won – Design of Buildings for IIT Delhi, is ideally suited to private architects too, and yet RITES has not won a single order like this in the private sector.

Even the export of locomotives outside India is facilitated by a credit line from EXIM bank for the partner country, as a part of India’s diplomatic mission and RITES simply acts as a point of contact here. Of course, RITES brings its technical skills in play through supply of spares, maintenance and training, it may not be able to compete with private players independently.

RITES is flushed with cash due to the taps opened by the Ministry of Railways. And this is a bit worrying since Indian Railways no longer has all that cash to splurge on –

| Particulars (in crores) | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

|---|---|---|---|---|---|---|---|---|

| Railway Profits | 13,615 | 11,749 | 16,838 | 19,228 | 4,913 | 1,666 | 3,774 | 1,590 |

| Financing from Govt | 289,375 | 324,662 | 368,758 | 419,124 | 471,776 | 517,324 | 573,641 | 640,408 |

| Profits as a % of O/S financing | 4.7% | 3.6% | 4.6% | 4.6% | 1.0% | 0.3% | 0.7% | 0.2% |

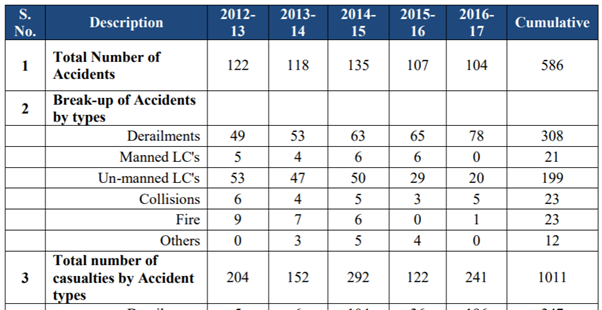

I think Indian Railways is far too gone to save based on the above. It is perhaps as big a drain on our country’s finances as the power discoms, not on an absolute basis perhaps, but on the sheer monstrosity of the wastage of resources it contributes to. Eg. The Central Government created a fund called Rashtriya Rail Sanraksha Kosh (RRSK) allocating 1,00,000 lakh crore for implementing safety works. The data sensing the need for this fund is as follows –

There are more daily casualties in Mumbai locals than the 1,011 casualties for above years combined and yet, 55,000 crore of this money has already been spent, without much success. Even the railway accounts are a swindle of sorts, with railways booking no depreciation or interest in its P&L, an investment bankers dream come true! (Profits = EBITDA)

RITES thus has a very real risk that its orders dry up as the capex for railways is hindered by its inability to service the loans borrowed, and as an investor, what one is truly betting on is Indian governments continued fiscal expansion backed by liberal monetary policies - pouring more and more money in the ever embattled Indian Railways and other large infrastructure projects like City Metros, highways and airports.

This is no place for a diatribe against moral hazards of money printing, but the real erosion I see in the value of my savings in cash compels me to look for cheap ideas like RITES, which, through its ability to gain an increasing service pie of Indian infrastructure investment whilst continuing to remain profitable can grow faster than inflation and money supply. What also separates RITES from other PSUs is their ability to cut costs by letting employees go if orders dry up, as happened in 9MFY21. Despite the revenues declining by 36%, the margins have largely remained stable, with superior cost control. Further, there is a near term trigger in terms of pending exports of 400-500 in Q4FY21 and Q1FY22.

this is my valuation -

| Particulars | Sales | PATM | PAT | Multiple(x) | Value |

|---|---|---|---|---|---|

| Consultancy | 900 | 30% | 270 | 10 | 2700 |

| Leasing | 450 | 26% | 117 | 12 | 1404 |

| Exports | 500 | 19% | 95 | 9 | 855 |

| Turnkey | 600 | 3% | 16 | 10 | 158 |

| Windmill | 50%BV | 70 | |||

| Energy Management | 80 | 45% | 36 | 12 | 432 |

| Cash Equivalents | 800 | ||||

| Total | 6,419 | ||||

| Current Market Cap | 5,880 |

I don’t hold the above valuation sacrosanct, and neither would you. I just wanted to see how the various moving parts shape up, and the above seems to be roughly right. Based on the above, I have allocated 5% of my portfolio to RITES.

for the complete thesis, you can refer here -

happy Investing!

10 Likes

This is more gov policy than monetary write up that follows below.

I would not put too much score on IR being bad as a state enterprise or Gov spending money on rail infrastructure. Simply put, world over, the experiment with privatising Rail is over. Pretty much, the entire infra is being borne by Govs, with private players taking small bits of profitable work like catering, advertisements and odd jobs. The most recent being UK where the Gov finally took over ticketing and sales 2 weeks back. Imagine!

As an investor, (have stake in RITES), as long as there is a monopoly and that no private player will spend 10,000Cr on long gestation projects with low yields, if you think there’s money there to be made in a Gov monopoly, go for it. I like this company for the Gov to Gov biz channel it opens up. Cross subsidised by Gov guarantees, what more do you want? RITES sells to B’desh, M’bique etc under a Gov aegis not to some shady operator where it has to fight it in a court for recoveries and payment. GMR filed a case against Maldives AFTER building a airport under a gov to gov deal and the new elected gov refused to pay. It won handily because the clauses are airtight unless corruption is involved.

Anyways, as long as IR is a monopoly, theres money in it for everyone, taking the right pick of companies involved in it.

2 Likes

hi, i take your points. thanks for the insights on other govts actions

despite govt spending, i do think that there is a very real risk that the govt can reduce RITES’ margins to save on its costs (40%+ margins in consultancy and leasing are rich pickings). The same has happened earlier with BEL also.

for me RITES is more of a value bet and not a quality play at all. was curious to know, what would be your top end for holding on to this company?

2 Likes

There are 3 major things only and nothing too complicated in it. I’m a strong believer in moral hazard theory,PSUs paying dividends and monopoly business. If the Gov is invested in it, I too will invest in it. The profit is mine, the loss is public taxpayer(hence moral hazard); sure I might lose money but I usually don’t get Enron’ed. The other is the idiotic dividends, essentially, gov paying itself with the money it gives to the company that it owns. Third is a monopoly, which is self explanatory.

Rest all, I pretty much don’t care; RITES might be making cow dung patties/vratties and selling it at a loss. I still get money, don’t I?

BEL, NHPC, SJVN, NTPC,PNB, NLC, IOB,SBI, IRFC, PNB Gilts, Oil PSUs are muck as far as corporate behaviour is concerned but I got them cheap, which, in a good year gives me 7%+ div yield avg overall.

1 Like

Hi, can anyone please explain - why is the CFO for rites consistently low across time periods Vs net profits?. As rites is more into consultancy & even other areas - customers pay up early or there isn’t any payment issues as such. Also is it because of higher other income contribution to total net profit?

1 Like

From Reliance sec report

What We Heard – Conference Call - Key Takeaways:

- Consultancy Segment: Domestic consultancy business returned to pre-COVID levels during the quarter with 2.3% YoY growth to Rs2.9bn. However, overall consultancy business fell by 9.8% YoY in FY21, as the initial three quarters of the fi scal were weak for domestic consultancy business. However, overseas consultancy grew by 15.5% YoY in FY21.

Consultancy business – which contributed 54% to its total FY21 revenue – remains the focus area of the company. The management expects the revenue-mix to remain the same at least till FY23E with consultancy contribution target of >50%. Current consultancy order book stands at Rs25.25bn with delivery time of 2-3 years. The management has guided for 10-15% segmental revenue growth in FY22E on the back of strong order book and optimism due to the record railway capex budget of Rs2.15 trillion. - Export Segment: After complete washout performance in the 3 initial quarters of FY21, exports business picked up again in 4QFY21 with 55% YoY growth in revenue to Rs912mn.

Though 30 coaches were ready to be shipped as of FY21-end, disruption in shipment resulted in revenue being spilled over to 1QFY22E. Another 30 coaches have been produced, which will be dispatched after the shipment of fi rst lot of 30 coaches. Export order book stands at Rs13.33bn, most of which will be executed in FY22E. Enquiries for new orders have been received but it will take at least a year to materialize. The management highlighted slowdown in capital purchases in some countries. - Leasing Segment: Segmental revenue declined by 6% YoY and 10% YoY in 4QFY21 and FY21, respectively. Segmental margin moderated to 35.6% in FY21 from 38.6% in FY20 due to reduced requirement of loco during 1HFY21 and depreciation.

- Turnkey Solutions: Aided by higher execution, segmental revenue rose by 31% YoY to Rs1.98bn in 4QFY21. Segmental order book stood at Rs22.16bn as of FY21-end including electrif i cation projects worth Rs17bn (L1). The management expects segmental EBIT margin to remain in the range of 3.5-3.75% in the near-term.

- Other Key Highlights: • The management expects 10-15% revenue growth in FY22E on the back of strong order book and optimism of robust order pipeline owing to the record railway capex. • Revenue, EBIT and PAT of Railway Energy Management Company (JV) declined by 5.3% YoY, 17.7% YoY and 22.4% YoY, respectively in 4QFY21 owing to only 1/3rd power requirement by the Railways.

1 Like

Hi

Is the management commentary of 10-15% revenue growth against FY21 base or FY2020?

Considering the hefty order book, a major proportion will be realized this year? Any cues you could get?

Q4, FY 21 Concall

1 Like

- RVNL proposed to be merged with IRCON

- Braithwaite & Co Ltd to be merged with RITES

- RailTel to be merged with IRCTC, CRIS to be wound up

- A new PSU to be formed to head Railways’ 8 production units

Principal Economic Adviser Sanjeev Sanyal has proposed a widespread rationalisation plan for government organisations and PSUs under the aegis of the Ministry of Railways which could see several mergers and closures, an official document accessed by PSU Watch shows. It is still in proposed stage.

Relevant Documents to understand business of Braithwaite & Co and its impact on Rites (Not latest ones)

-

Annual Report of 2019-20

https://www.braithwaiteindia.com/financials/BRAITHWAITE_ANNUAL_REPORT_ENGLISH-1920.pdf -

Credit Rating of Braithwaite & Co

https://www.brickworkratings.com/Admin/PressRelease/Braithwaite-Co-29April2020%20.pdf

Disclosure: Invested and re-evaluating if proposal gets executed.

4 Likes

Discl: My PSU basket has some of these Railway Stocks. These were bought by me quite some time back with an objective of getting High Dividend yield.

It is not an investment advice. Prices have already gone up quite a bit. PSU stocks also carry an inherent risk of frequent change in Govt Policy which may or may not be conducive to investor interest…though Govt has heavy Capex plans and most PSU railway stocks order book is full for next 4-5 years. Please do your own assesment before investing.

2 Likes

Professor Sanjay Bakshi on Rites

3 Likes

Prof has used 2019 analysis in his 2024 blog. I think he should have refreshed his analysis before writing the blog.

Fundamentally a lot has changed for the company since 2019- There’s margin compression as more projects are moving from nomination to competitive bidding. Revenue too is expected to be flattish for next year, management is trying its best to maintain the bottom line.

At a 1 year forward P/E. of 26, this is the highest valuation the stock has ever traded at.

Disc: Invested from lower levels

5 Likes

I think the competition is for foreign projects, not for domestic. Is that right?